![]()

Cover Story

Lead Ban To Test Supply Chain's Mettle

Market Data

Communications Loses More Ground

Market Mix Percentages for 44 of the Top 50 EMS Provders in 2002

IDC Explores Outsourcing in Servers and Handsets

World Markets

More Business in Eastern Europe

News

Competition Heats Up in Cell Phone Design

Three-Five Makes Asset Purchase

Last Word

Whether or not it makes sense to take lead out of electronics, the question was largely settled when the European Union passed the Directive on the Restriction of the Use of Certain Hazardous Substances in Electrical and Electronic Equipment. Also known as ROHS, this directive mandates that starting July 1, 2006, certain electronic equipment sold within the European Union must be free of a number of hazardous materials including lead. For affected products, the conversion to lead-free soldering will require a major undertaking throughout the supply chain. Indeed, this will prove the greatest change to hit the manufacturing world in many years. It's bigger than the elimination of CFCs and may be even surpass the transition from through-hole to SMT.

Thilo Sack, an advisory engineer at Celestica and the person responsible for providing overall direction for the company's lead-free activities, was around for both the adoption of CFC-free processing and the change to SMT. He says, "Those two things absolutely pale in comparison to the amount of effort involved on the lead-free front."

Lead-free soldering will place heavy demands on the entire supply chain. Component suppliers will have to requalify entire product lines for higher soldering temperatures and lead-free terminations. PCB fabricators will need to prove out lead-free finishes as well as laminate systems to withstand higher temperatures. EMS providers must demonstrate lead-free processes that result in high levels of quality and reliability over a wide range of board size and complexity. Repair service providers must be able to handle returned products with leaded and lead-free alloys. And OEMs must ensure that their product transitions to lead-free occur on time without logistical mix-ups.

It's a tall order, but not everyone is on the hook. A significant portion of the EMS market will not be required to comply with the ROHS directive. Exempted from the directive are network infrastructure equipment for switching, signalling, transmission and telecom network management; servers, storage and storage array systems; medical devices; and monitoring and control instruments. The European Commission will review the exemptions for network infrastructure equipment and servers and storage systems with a view toward setting a time limit for these exemptions. Servers and storage systems are already exempted until 2010. In addition, ROHS does not list either military/aerospace systems or automotive electronics as equipment covered by the directive.

Unable to consider such exemptions, the EMS industry has been gaining experience with lead-free soldering. For example, Solectron is approaching 2 million units of lead-free production, mostly in the printer, camera, cell-phone and notebook-computer spaces. To support Japanese customers who have opted for lead-free products, Solectron is utilizing its sites in Singapore, Malaysia, Taiwan, China and Japan. Sanmina-SCI is now producing lead-free board assemblies in three countries and plans to roll out the lead-free technology to its other EMS plants by year end. Celestica is providing lead-free manufacturing in the consumer space for a handheld scanner scanner product and cell phone/radio type product.

Celestica's Sack argues that current products designated lead-free are not truly so because only the SMT process is free of lead. Components have not been requalified, and other processes such as wave soldering and repair may still be leaded.

Although ROHS went into effect this year, providers such as Celestica and Solectron have been working on lead-free processing for a number of years. Their efforts have been directed both internally and through consortia.

The consortia work done by EMS providers, OEMs and others is now paying off as a standard lead-free alloy is emerging. Momentum is building around the Sn3.9Ag0.6Cu alloy proposed by NEMI (the National Electronics Manufacturing Initiative). But its melting point is 217º C versus 183º C for the standard tin-lead alloy. Both Celestica and Solectron, for example, are promoting the Nemi alloy for customers outside Japan.

Japan is a different case because Japanese OEMs, which have led the rest of the world in lead-free assembly, have selected a plethora of alloys. Solectron's Nakaniida facility, a former Sony plant, uses six different alloys to support Japanese customers. But where possible, both Solectron and Celestica are advocating Sn3.0Ag0.5Cu for Japanese OEMs. The melting point of this alloy is close to that of the NEMI alloy, which is good news for providers that must use both materials.

Based on the process development work that has been done with the NEMI alloy, the EMS industry has the process basics necessary for a roll-out of lead-free soldering. "Basically, we have the fundamentals for SMT and wave solder for doing lead-free implementation," says Kim Hyland, director of process integration at Solectron. But a number of obstacles still stand in the way of widespread adoption of lead-free soldering.

It is becoming clear that component availability presents the greatest barrier today. The components issue actually has several facets. The first, and most obvious, is the lack of components qualified to the IPC/JEDEC standard J-STD-020B, which sets forth higher peak reflow temperatures associated with lead-free soldering. "Very, very few component suppliers have requalified their parts to those new specifications," says Celestica's Sack. These temperatures - 245º C for components larger than 350 mm3 or thicker than 2.5 mm and 250ºC for smaller, thinner devices - establish the always critical moisture sensitivity level to prevent outgassing defects. According to NEMI, moisture sensitivity in general goes up by one level with every 10º C increase in temperature. The higher the level, the shorter the floor life. Without being redesigned and requalified for a higher peak temperature, some components would end up with an unacceptably short floor life or none at all.

Component lead finish, particularly plated tin, is another issue. Plated tin has long been known to produce tin filaments, or whiskers, with the potential to cause shorts or break off within the assembly. Component users and suppliers are seeking a better understanding of this defect and a test methodology that can be used to emulate it.

Despite concerns about tin whiskers, Motorola Semiconductor Products Sector is backing plated, or matte, tin for component leads.

"We think that it is going to be the most cost effective technology of those that were proposed in the beginning," says Alan Woosley, lead-free program manager at Motorola SPS.

For Motorola, tin whiskers are not an issue because of its plating technology. "We think we have a solution internally that simply doesn't produce this effect, and that's what we're spending a lot of time evaluating," says John Theiss, director of quality data process systems for Motorola SPS and the person overseeing its green products.

"We're reasonably confident that matte tin is going to be the industry solution," says Woosley.

Backward compatibility crops up as yet another unresolved issue with components. Spurred by the drive to lead-free by Japanese customers, component suppliers have started to offer devices that are intended for both the tin-lead and lead-free environments. A provider like Solectron must ensure that in such cases a component's new lead-free metallurgy will work in the company's existing soldering process. "I'm not quite sure I'm ready to drop into all my sites, say, a BGA with tin-silver-copper spheres [to solder] in my tin-lead paste process. Physically, it can work. Do I have all the information that I feel comfortable to tell my customer that this is a good thing? No, not at this point," says Solectron's Hyland.

Component issues aren't the only barrier to broad acceptance of lead-free assembly. To date, most lead-free soldering has been done with consumer-type products. Industry has yet to prove that it can process large, complex boards to yield the necessary reliability. Small consumer boards heat up more easily than large boards, which are prone to thermal gradients. In addition, there is the question of hole fill with large, thick boards, and Solectron, for one, will be doing a lot more work this year on lead-free wave soldering of large boards.

More reliability data are also needed for the NEMI alloy. "Right now, there isn't enough data to be statistically significant..., but early indications are that is it more reliable," says Celestica's Sack.

Although not a burning issue today, managing the logistics of components, boards and finished products as they transition to lead-free will become a major challenge. "How are you going manage the inventory so that eventually at July 1, 2006, you don't have any leaded inventory left in stock?" asks Sack. He adds, "In talking to a lot of our customers, they're finally coming to the realization that it's going to be a bigger challenge than they originally thought it might be."

"The logistics from our suppliers through our factory through the OEM supply chain into the field is something that will be an interesting problem for us all...," says Hyland.

Last but not least is the question of cost. With this question in mind, Phil Zarrow, president of the consulting firm ITM (Durham, NH), has been asking plastics suppliers about component molding compounds for lead-free temperatures. "They're telling me these plastics are available, but they cost more. It's the same way with PC board materials. In some cases, we may be looking at stuff beyond using normal glass epoxy FR-4. We may be looking in some cases at BT epoxy. It's going to cost more," says Zarrow. He also points to other added costs including those associated with royalties paid on alloy patents as well as equipment costs, which will be covered in part 2 of this series next month.

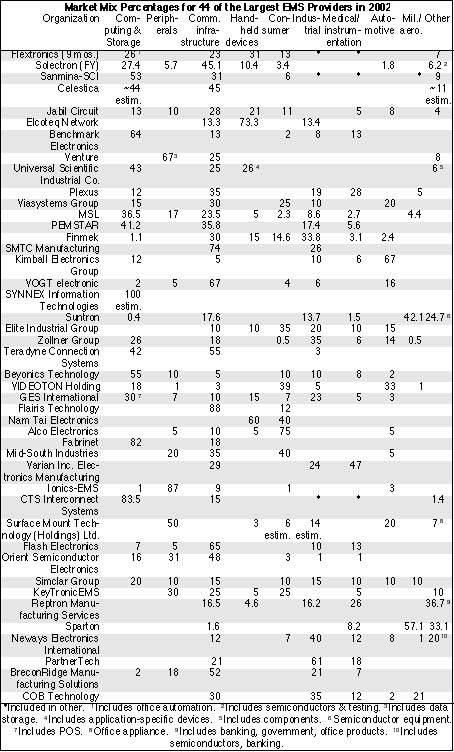

Data from 44 of the MMI Top 50 EMS providers show that communications infrastructure equipment slipped to a 31.9% share of their combined sales in 2002 (see chart). Communications infrastructure barely held on to its position as the largest EMS segment, as computing and storage came in just one percentage point behind at 30.9% of revenue from these providers. Not only that, the two computer-related sectors, computing and storage and peripherals, together accounted for more business than did the communications infrastructure segment.

Market mix percentages are listed for each of the 44 Top 50 providers (see table). These 44 providers accounted for 2002 sales of $64.9 billion, or about 70% of the EMS market. Given this weighty proportion, MMI believes that the 44 companies largely reflect the market at large and provide true market statistics as opposed to estimates. But there is a caveat to this statement: data from tier-one provider Foxconn (Hon Hai) is absent. Because Foxconn primarily serves the computer industry, the computing and storage segment could be underweighted by as much as 9%.

How much has this communications segment shrunk? In 2001, 45 Top 50 providers, including the same tier-one companies but with a somewhat different group of lower-tier providers, relied on communications infrastructure for 38% of aggregate sales (April '02, p. 4). So assuming the two groups were representative of the overall EMS market, comm infrastructure lost about six share points last year.

Two of the sectors gaining share were consumer and handheld devices, reflecting increased penetration of outsourcing in 2002. Compared with the 2001 Top 50 statistics, the consumer segment increased from 5% of the market to 6.7% in 2002. Likewise, handheld devices grew from 11% to 12.6% last year. Although storage was added to the computing category for the 2002 analysis, it appears that computing alone also gained share from 27% in 2001.

For the first time, it was possible to break out the automotive sector, which is underpenetrated at 2.1% of the 2002 market. Unfortunately, the industrial, medical/instrumentation and military/aerospace segments were not reported separately in the case of several providers (table). As a result, MMI was unable to compile statistics on these segments, which had to be included in the other category that accounted for 11.7% of sales for the 44 Top 50 providers.

Note that it was impossible to capture all end markets within the tabular listings for each company. For example, semiconductor equipment and banking were placed in the other category. Office automation was included in two different categories.

Market Mix for 44 Top 50 EMS Providers in 2002

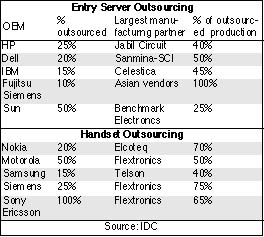

Breaking new ground in market research, IDC (Framingham, MA), recently studied outsourcing by OEM and product category. Two of the categories analyzed were entry servers, defined as selling below $100,000, and handsets. According to IDC, both product areas offer a healthy amount of untapped potential for outsourcing.

Based on data for the second half of 2002, IDC found that outsourcing claimed 26% of entry server production and 34% of handset units. In each product category, IDC looked at how much production was outsourced by the top five OEMs and what portion of outsourced production went to the OEM's largest manufacturing partner (table below).

IDC found that HP, the largest manufacturer of entry servers, only outsourced 25% of their production, and just one top-five OEM, Sun, outsourced above 25%. These figures, of course, do not include IBM's server outsourcing announced in January and expected to bring the outsourcing level at IBM near 100%. Given second-half production of 2.6 million entry servers, HP, Dell and IBM accounted for leading market shares of 22.6%, 15.7% and 13.2% respectively. Yet two EMS providers - Sanmina-SCI at 6.4% share and Jabil Circuit at 3.7% - also took appreciable slices of total production. Indeed, these two providers also had the highest market shares of outsourced production. Sanmina-SCI handled 27% of contracted production, while Jabil did 16% of it.

With 34% of production farmed out, handsets are another area expected to see continued outsourcing. According to IDC, Asia has already become the hub of handset production as 63% of manufacturing occurred in the region.

Of the 234.2 million handsets made in the second half of 2002, 29.5% came from Nokia. Flextronics was the second largest producer at 11%. Motorola, Samsung and Siemens followed with shares of 9.5%, 9.2% and 6.5 % respectively. Within the outsourced portion of handset production, Flextronics and Elcoteq led with shares of 33% and 19% respectively. Flextronics served as the largest manufacturing partner for three out of the top-five handset OEMs (table below). In the case of Samsung, its largest partner is a Korean company, Telson.

IDC took a four-step approach to this study. The firm started out by compiling its own outsourcing data and filling in any gaps with estimates. Then IDC asked the OEMs in the study to confirm this information. "They all responded and they all responded in detail," said Kevin Kane, the IDC analyst who headed up the study. IDC got OEMs to participate because the firm convinced them that the data would be published anyway. In the last two stages, IDC discussed the data with the EMS providers in the study and verified top-level data with component vendors.

Not all the findings were positive, however. IDC was not encouraged by the outsourcing data from Japanese OEMs. "We expected them to be low in general, but the uniformity across all segments was a bit surprising," said Kane.

"If you're looking at a segment that has not outsourced dramatically, but is made up primarily of Japanese vendors, the increased penetration of outsourcing in that segment may not be as significant in the near term as you might expect," he added.

The IDC study also covered two other products areas - notebooks and PDAs. For more information, contact kkane@idc.com.

China gets all the attention, but there are signs that Eastern Europe is also benefitting from the OEM quest for lower costs.

Consider Flextronics. The EMS provider is hiring again in Hungary, and a major handset program, on the order of $500 million a year, will primarily rely on Hungary for manufacturing. According to a Reuters report, Flextronics will hire 500 workers by June for its Sarvar facilities, whose work force will expand to 3500. This job growth follows a cutback that occurred last year when Flextronics moved European production of Micosoft's Xbox game console to China.

"Hungary is quite busy now. We've won quite a number of programs," said Flextronics CEO Michael Marks during a February conference call. The provider uses Hungary for consumer products and Poland primarily for infrastructure products.

What's more, Taiwan's Hon Hai, better known by its Foxconn trade name, saw dramatic growth in its Czech operations last year. Reuters reported that Foxconn's Czech unit almost quadrupled sales to $1.18 billion in 2002 as it built a combined two million computers for Compaq and Apple.

Moreover, MHM, a market research firm based in Ayr, Scotland, forecasts 29% growth for the EMS industry in Eastern Europe this year. EMS business in the region will reach $14.83 billion in 2003, up from $11.5 billion in 2002, predicts MHM. The firm expects EMS revenue in Western Europe to increase by 5% to $19.97 billion this year from $18.96 billion last year. In addition, MHM predicts that Eastern Europe will take a majority share of the European EMS market by 2005.

Flextronics (Singapore) came out of the blocks first with its low-cost cell-phone design, PhoneOne, and sprinted ahead in the development of other handheld platforms (March, p. 4-5). Now Elcoteq (Espoo, Finland), which has manufactured over 100 million mobile phone products, has entered the race to sell mobile phone design platforms to OEM customers.

Elcoteq's platform designs include mobile communications, PDA, e-mail, messaging, camera, and multimedia capabilities. The company can equip a mobile phone with features such as a PDA with advanced business and data capabilities, integrated digital camera, photo album, caller ID with photo display, EMS messaging, e-mail, MP3 player, MP3 alarm clock, games, and an MMC card slot for mass memory storage.

Besides original design, Elcoteq will provide supply chain management, volume manufacturing, product and technology transfer, NPI, and post-manufacturing services. Elcoteq can also engage in codevelopment engineering services.

Despite these original design offerings, Elcoteq does not want to be called an ODM (March, p. 5). The company believes customers would view it as competition if it were labelled an ODM.

More news in design services...Design Solutions Inc. (Santa Barbara, CA), a provider of PCB design, engineering and prototype services, has opened a design center within a Nashua, NH facility of Teradyne Connections Systems, an MMI Top 50 EMS provider that also offers high-performance circuits and connectors. Located within Teradyne's high-performance circuits (HPC) facility, the new center will allow the two companies to team up for the delivery of HPC design and layout services....The engineering team of Top 50 provider Sparton Corp. (Jackson, MI) has joined the Motorola Design Alliance Program (June '02, p. 3). As a member of this program, Sparton will gain access to a variety of resources - such as training, tools and technical support - to enhance the provider's design engineering services.

New programs...Reuters is quoting a Sony spokesman as saying the company will move production of all PlayStation 2 game consoles to China in the next fiscal year. That means more business for two of Sony's existing suppliers, Hon Hai Precision Industry (aka Foxconn) and Asustek, both of which are Taiwanese companies. Reportedly, production will be shifted primarily to the Chinese facilities of these two providers....A Japanese manufacturer has ordered from Nam Tai Electronics (Hong Kong) more than 1 million front light panels for handheld video game devices. Nam Tai has also received an order to manufacture 50,000 attachable cameras for a new customer's cell phones....iSECUREtrac Corp. (Omaha, NE) has chosen Altron (Anoka, MN) as primary manufacturer for a GPS tracking product for the criminal justice industry....Aspeon (Irvine, CA), a supplier of point-of-sale systems and services, has made Pinnacle Electronics (East Pittsburgh, PA) contract manufacturer of Aspeon's circuit boards. Pinnacle has replaced another CM....Fujitsu Transaction Solutions (Frisco, TX), a subsidiary of Fujitsu, has selected ExpressPoint Technology Services (Golden Valley, MN) as the multivendor depot repair and logistics provider for two retail equipment service contracts.

Emerging EMS provider Three-Five Systems, or TFS (Tempe, AZ), has acquired Philippines manufacturing assets of Microtune (Plano, TX) and will assemble and test Microtune's RF tuner modules and wireless module products in TFS's existing facility in Manila, Philippines.

Under the agreement, which went into effect on March 31, Microtune sold the equipment and inventory of its Philippines' manufacturing facility to TFS and outsourced to TFS all of Microtune's current demand for fully-assembled RF subsystems. TFS paid about $2.8 million for the equipment, to be transferred to its Manila operation. Volume production will start in Q2. TFS expected to hire 450 to 500 Microtune employees for the TFS facility in Manila.

In addition, TFS plans to add this RF expertise to its design and development capabilities and eventually offer these expanded capabilities to its other customers.

As a result of this deal, TFS expects 2003 revenue for its Integrated Systems & Displays division to range from $150 to $170 million.

Three-Five Systems is evolving from a supplier of display products to a provider of design and manufacturing services. This transition was marked by the company's acquisition of EMS provider ETMA (Redmond, WA) last year (Dec. '02, p. 3-4). TFS said the EMS capabilities it added through ETMA allowed TFS to win new customers such as Microtune.

Military contracts...TTems Ltd (Rogerstone, UK) will produce PCB assemblies for high-frequency (HF) military radio units made by Harris Systems Ltd, a UK subsidiary of Harris Corp. (Melbourne, FL). Harris will supply about 10,000 HF radio systems to UK Defense Forces....Northrop Grumman Electronic Systems has awarded LaBarge a $4.7-million contract to produce electronic chassis used in radar upgrades for the US Air Force's F-16 aircraft as well as a $1-million contract to build PCB assemblies for an airborne surveillance radar system.

New EMS companies...Singapore-listed Goldtron, which has both components distribution and EMS businesses, is spinning off its EMS unit in Shanghai, China. Goldtron has received an eligibility-to-list letter from the Singapore Exchange for a proposed listing of the unit under the name Radiance Electronics Pte Ltd. The Radiance unit, which has been profitable for the last three financial periods, provides EMS principally for the satellite communications industry and to a lesser extent, for computer peripherals. Goldtron will continue to retain a controlling interest in Radiance. Goldtron's EMS business conducted through its Shenzhen subsidiary will not be part of Radiance....Rich Breault, whose former company Netco Automation was known for its BGA services and prototyping, has founded a new EMS company, Lightspeed Manufacturing in Methuen, MA. Drawing on the expertise of some former Netco employees, Lightspeed will also offer BGA services, its primary focus. These quick-turn services include rework, reballing, inspection, ECOs and upgrades. The new company will also offer optical fiber splicing as well as traditional PCB assembly services. Breault's former company was acquired by Chase Corp. in 2000.

Expanding in Mexico...Suntron (Phoenix, AZ) has expanded the capabilities of its Tijuana, Mexico facility to include SMT production. As a result, the Tijuana operation is now capable of processing double-sided SMT boards down to 10-mil pitch, with full test capabilities. Focusing on high-mix, complex EMS, the Tijuana facility serves hi-rel commercial and aerospace markets as well as medical and semiconductor equipment segments.

Restructuring continues...After closing an operation in Boise, ID, Jabil Circuit (St. Petersburg, FL) is moving production out of its Coventry, England site. But Jabil is not finished cutting. The provider expects to take additional restructuring and impairment charges of about $16 to $36 million during its fiscal 2003....SMTEK International (Moorpark, CA) has sold its operation in Craigavon, Northern Ireland, to a group of local investors for nominal consideration. The sale will reduce SMTEK's liabilities and debt structure. It is expected that the two parties will enter into a strategic alliance....Elcoteq has started negotiations with worker representatives to reduce the work force at its Lohja, Finland site by up to 160 employees. The Lohja site currently employs about 600 people.

More unpleasant news...A number of law firms are participating in class action lawsuits on behalf of purchasers of Solectron stock between Sept. 17, 2001 and Sept. 26, 2002. These complaints allege that Solectron failed to write down in a timely manner certain obsolete inventory in its Technology Solutions unit....Boundless Corp. (Hauppauge, NY), which operates an EMS subsidiary called Boundless Manufacturing Services and a display products business, has filed for reorganization under Chapter 11 of the US Bankruptcy Code.

Some financial news...Solectron will pay cash to those who want the company to buy back zero-coupon convertible notes due in May 2020. The value of the notes as of Feb. 28 was about $522 million....BreconRidge Manufacturing Solutions (Ottawa, Canada) has received an equity investment of $30 million from EdgeStone Capital Partners. Gilbert Palter, COO and managing partner at EdgeStone, and Guthrie Stewart, an EdgeStone partner, are joining the BreconRidge board....In Form 10-K for 2002, MSL (Concord, MA) has recorded an increased reserve of $5.4 million against a note receivable with a former customer that filed Chapter 11 bankruptcy last month. This increased reserve changed MSL's previously announced Q4 2002 net income of $0.1 million to a net loss of $5.3 million....For the quarter ended Jan. 31, publicly held SigmaTron International (Elk Grove Village, IL) earned net income of $1.6 million on sales of $25.5 million. Net income was up 178% versus a year earlier, while sales rose 13%.

People on the move...Antti Piippo, Elcoteq's principal shareholder, has rejoined the company's board as chairman (Feb. '02, p. 8). Also, Elcoteq has appointed Esa Retva its VP of sourcing. He came from Nokia Mobile Phones Sourcing....Bernard Doorenbos, CEO of Neways Electronics International (Son, The Netherlands) will resign this year. The company said restructuring has reduced it to a size that calls for a two-member Executive Board....IEC Electronics (Newark, NY) has named Brian Davis as CFO and corporate controller. He joins IEC from Thermo Spectronic, where he served as VP of finance....Nam Tai Electronics has appointed Guy Bindels as its R&D director. He had been product development manager of Atlinks Hong Kong, a subsidiary of an Alcatel-Thomson joint venture in multimedia....Integrex (Bothell, WA) has hired Thomas Mrowca as VP, business development. Reflecting a background in the medical segment, his past positions include VP of sales and marketing at SeaMED, which was acquired by Plexus, and VP of sales, marketing and product development at Horizon Medical Outsourcing....Steve Petracca has left PEMSTAR (Rochester, MN), where he was executive VP, business development, to become president and CEO of BuilderDepot (San Diego, CA), which sells home improvement and building supply products online. Petracca is a former adviser to MMI.

Top 50 update...Ionics-EMS (Laguna, Philippines) reported its 2002 sales of $190.0 million after the MMI Top 50 was published. MMI had estimated sales of $245 million, which gave Ionics-EMS a higher rank than it deserved. The company actually ranked 37th instead of 29th. In addition, 14 Top 50 companies showed growth over 20%, not 13 as originally reported.

The lower manufacturing and material costs in China do not come risk-free. Popular thinking sometimes skips over this point. It is patently false to believe that you can serve the US market from China without taking on some risk.

Most OEMs are well aware of some non-zero probability that their supply-chain from China could be interrupted. Unlikely as it seems today, end market demand could increase such that disruptions occur. This idea has been advanced more than once by none other than Flextronics, a provider with a large presence in China. Political instability and terrorism are often cited as other risks to sourcing product from Asia. For instance, what if Taiwan and mainland China won't back down from a dispute?

To these risks, a new one must now be added - health. The emergence of severe acute respiratory syndrome, or SARS, from Southern China has created a concern about traveling to China and other parts of Asia. There is no cure for SARS, and because it is so new, researchers need to learn more about the disease.

SARS is already having an effect on the electronics industry. Reportedly, Intel is pulling out of trade shows in China and Taiwan, and Sun is also withdrawing from a show in China. What's more, Nokia is among the companies restricting travel to Asia. Not only that, the disease reportedly has caused Motorola and HP to briefly shut down plants in Singapore and Hong Kong, respectively. Indeed, the World Health Organization is advising people to postpone nonessential travel to Hong Kong, Beijing, and the Chinese provinces of Guangdong and Shanxi. Toronto also joined the list. Similarly, the US Centers for Disease Control and Prevention is recommending that travellers put off nonessential trips to China, Hong Kong, Hanoi in Viet Nam, and Singapore.

These warnings have not gone unnoticed within the EMS industry. For example, Celestica has suspended all but the most essential travel to the Far East. Still, a company spokesperson said there is no impact on its supply chain, and other than the travel restrictions, operations in the region are conducting business as usual.

Then there's Hong Kong-based Nam Tai Electronics. The provider has instructed employees to minimize business travel and has issued respiratory masks to its people in Hong Kong and China. Although Nam Tai does not believe that SARS has had a material impact on operations, a prolonged outbreak or further limitations on its activities could hurt future results. As of this writing, neither Nam Tai nor Celestica has found any cases of SARS among employees.

Will SARS hamper new business development for China? It's probably too early to tell, but the potential exists. Some OEMs might delay plans to outsource to China if they feel their employees would balk at traveling there. Plant qualifications could also be affected.

Despite the buildup of EMS capacity in China, a supply pipeline from China has always presented some risks. By increasing those risks, SARS should bring more attention to them.