![]()

Cover story

Solectron To Add C-MAC's Brand of Vertical Integration

Tech Trends

Providers Making Optical Investments Despite Downturn

News

Lucent Moves Ahead with Divestitures

Teradyne To Gain Enclosure Company

Solectron Adds Services Firm in Japan

Last Word

Solectron (Milpitas, CA) and C-MAC Industries (Montreal, Canada) have reached a definitive agreement that will allow Solectron to effectively acquire C-MAC through an all-stock deal. This is the second union of two top-10 providers announced in less than a month (see July). Although there are differences between this deal and the Sanmina-SCI merger, both combinations echo a common theme - vertical integration. These deals are being struck in anticipation that an end-to-end solution aided by vertical integration will win the day when OEMs pick their partners for the large-scale outsourcing projects being planned.

Under the terms of this latest agreement, Solectron will issue 1.755 shares of its common stock for each C-MAC common share. Based on Solectron's closing price of $17.20 on August 8, the deal valued C-MAC's stock at $30.19 per share, amounting to a 33% premium over its closing price. At that point, the deal was worth about $2.7 billion, including the assumption of about $30 million in debt net of cash. Closing is subject to customary conditions, including approval by both companies' shareholders and regulatory bodies. The transaction is expected to be completed by the end of this year.

Solectron will be acquiring a company employing more than 9000 people and operating 52 manufacturing facilities in ten countries. They are Belgium, Canada, China, France, Germany, India, Mexico, Ireland, the UK and the US. These operations are supported by eight design centers in North America and Europe. C-MAC's sales for the last 12 months totaled $2.0 billion. Adding C-MAC's sales will widen Solectron's revenue lead over its nearest competitor, which at present appears to be the Sanmina-SCI combination (see table below).

During a conference call with analysts, Solectron listed a number of benefits to be derived from this transaction:

C-MAC's strength in high-end systems. "C-MAC has a strong high-end systems integration capability including complex electromechanical design and assembly with strategic backward integration at the metal and backplane fabrication [end]," explained Koichi Nishimura, Solectron's chairman, president and CEO. C-MAC's large-frame enclosure capabilities for telecom and networking will complement Solectron's recent acquisition of Sing-apore Shinei Sangyo, which supplies smaller form factor enclosures (June, p. 5). What's more, C-MAC Engineering, a division of C-MAC, provides electromechanical engineering and design, and the group's services include product approvals, testing and evaluation. According to C-MAC's annual report, it has one of the largest non-captive electromechanical design groups in the industry. Note that C-MAC was one of the first EMS companies to acquire capabilities in the electromechanical space.

Backplanes form another building block for high-end systems, and this deal will give Solectron the ability to manufacture backplanes internally. Note that SCI also cited this same benefit for its merger with Sanmina (July, p. 2).

In addition, Solectron will gain C-MAC's ability to produce optical networking components (see also article on p. 3).

C-MAC's strategy of selective vertical integration. Solectron will be able to leverage this brand of vertical integration, which allows C-MAC to capture margins on internally produced items such as PCBs, backplanes, sheet metal products and microelectronics components. With this strategy, C-MAC uses a make or buy approach that allows the company to sell a portion of internally produced items to outside customers. "We try not to buy any more than 40% of our own produced product in house," said Dennis Wood, C-MAC's chairman, president and CEO, during the conference call. By selling product this way, C-MAC aims to ensure that internal business units remain competitive.

There's another advantage to selective vertical integration. "In challenging economic times such as these, we've had the flexibility to pull in some of our outsourced production until such time as conditions improve," said Wood.

Entry into the automotive market. Through C-MAC, Solectron will gain access to the automotive sector, which accounts for about 8% of C-MAC's sales. How large is the automotive electronics market? "It's a minimum of 19 to 20 billion dollars," said Wood. "All we really want of that for next year is 5% of it." According to C-MAC, the market estimate goes up when multiyear contracts are considered.

C-MAC reports the automotive market has accepted the idea of asset divestitures. "I think that's one of the advantages of the combination of Solectron and C-MAC. It will position us to take advantage of these transactions because they are major transactions. We're not looking at 50-, 100- million-dollar transactions. I mean these are billion-dollar transactions, and we need the critical mass to be able to do it," said Wood.

C-MAC's automotive business utilizes PCBs as well as ceramic-based circuits. The latter are designed to withstand the harsh environmental conditions often required for automotive applications. In planar form, these ceramic-based circuits are known as thick-film hybrids. Newer technology called LTCC (low temperature co-fired ceramic) creates three dimensional circuits within a ceramic module. Having built up automotive capabilities over the last five years, C-MAC reports it has achieved the status of full-service supplier to that industry.

Other expected benefits of this deal include added revenue through cross-selling, enhanced service offerings in networking and telecom, and a greater presence for Solectron in Canada.

The deal also addresses a specific need that C-MAC has. To participate in large OEM divestitures, the company recognized that it would have to acquire additional high-volume PCBA capability. Solectron easily meets that need, while saving C-MAC the time and effort of buying or building the capability.

C-MAC has over 500 regular customers, of which 270 have a purchase run rate greater than $1 million. The company's largest customer, Nortel, accounted for 51% of revenue in its Q2 ended June 30, up from 42% in Q1. For Q1, 79% of sales was communication-related.

On the microelectronics side of C-MAC's operations, the company produces modules, interconnect systems, frequency-control products, sensors and control devices. Solectron intends to use C-MAC's component capabilities in the networking and automotive markets as an entrée to new business in those industries.

As a result of this deal, Solectron expects to generate an estimated $60 million to $120 million in synergies through cost savings and revenue opportunities. The company expects the transaction to be accretive to fiscal 2002 earnings.

C-MAC's Dennis Wood will oversee the integration of the two organizations. He will chair a committee to be formed from Solectron's board and focused on selective vertical integration and corporate strategy. Solectron will invite a second C-MAC board member to join the Solectron board.

For C-MAC's Q2 ended June 30, the company posted revenue of C$764.1, up 32% over a year earlier, and expects Q3 sales to exceed C$575 million. Net earnings before goodwill amortization per share diluted were C$0.45 for Q2 and are expected to be about C$0.10 to C$0.15 for Q3.

Meanwhile, Solectron has increased the scope of its restructuring plans. In June, the company said fiscal Q4 restructuring charges would amount to $50 million; now the company is planning to take an additional Q4 restructuring charge of up to about $210 million. That brings the restructuring total for the quarter to about $260 million. Solectron also expects to incur a $58-million charge related to credit and other exposures from a number of smaller accounts that are in or near bankruptcy.

The company expects to generate fiscal Q4 sales of $3 billion to $3.5 billion and fiscal 2002 sales, excluding the C-MAC transaction and other potential acquisitions, in a range of $16 billion to $18.5 billion.

With the communications market in its worst slump ever, it's no time to be investing in EMS capabilities for optical networking gear. Or is it? Not only are a number of EMS providers investing in optical capabilities, in some cases they are outstripping what OEMs typically can do. Providers are vying for technology leadership in a field that they see as increasingly important despite its current state.

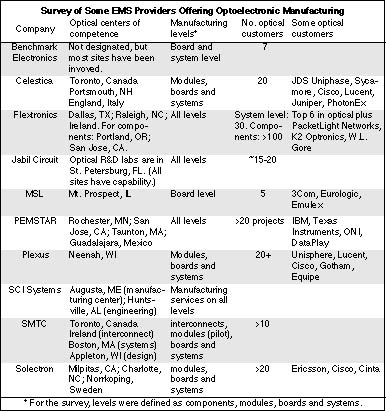

Not everyone has the same approach to building optical capabilities. MMI surveyed a number of providers to see how they are investing in the optical area (see table, below). Here's what we learned:

· A number of companies are setting up what some have termed optical centers of competence. Usually supported by a lab, these centers typically develop processes and tests for new optical products. Manufacturing may also be done there or it may be transferred to another location. One of the most visible examples of this strategy is Celestica (Toronto, Canada). The company expects to go from four optical centers at present (see table) to eight by early next year. Celestica plans to add centers in Raleigh, NC, and Thailand by the end of this quarter and two more in San Jose, CA, and Brazil by Q1 2002.

Under this model, Celestica can use an optical center to stabilize processes for products that are destined for volume manufacturing in a low-cost geography. For example, the company is manufacturing an optical transceiver in Monterrey, Mexico after the product was moved from Celestica's optical center in Toronto, Canada.

But others such as Jabil Circuit (St. Petersburg, FL) and Plexus (Neenah, WI) perfect optical processes in a central location and then transfer the technology to other sites.

· Optical capabilities, of course, can be acquired. Solectron (Milpitas, CA) serves as perhaps the most recent example of this type of optical investment. The company recently took over Cisco's DWDM (dense wave division multiplexing) module manufacturing in West Columbia, SC (June, p. 5).

Probably the most aggressive acquirer of optical capabilities to date is Flextronics (Singapore). Since the fall of last year, the company has made three acquisitions on the optical side (Feb., p. 10-11, Oct. '00, p. 9-10). These deals have allowed Flextronics to add high-end capabilities, particularly in optical components, faster than it could have on its own. For instance, the acquisition of Photonic Packaging Technologies in Portland, OR, gave Flextronics a team with hundreds of years of experience in photonics. "It's certainly a lot easier to go buy that capability," says Ron Keith, VP and GM of Flextronics Photonics, and then grow the team under Flextronics. He points out the company puts a lot of money and effort into deploying the technology it acquires.

Market conditions have not forced Flextronics to the sidelines. The company continues to be on the lookout for optical acquisitions.

· Despite the downturn, providers are also investing to build capabilities from the inside. MMI found a number of examples in its optical survey. PEMSTAR (Rochester, MN) has invested $6 million so far in fiscal 2001, with $11 million planned for fiscal 2002. The optical budget for SMTC (Toronto, Canada) is $5 million for 2001, and the company anticipates spending over $10 million in 2002 as market conditions change.

Also, SCI Systems (Huntsville, AL) recently made a seven-figure capital expenditure for R&D equipment. Through this investment, SCI is expanding its capabilities in such areas as splice tray design and assembly, splicing of dissimilar and polarization-maintaining fibers, undersea cable design and cable dispensers, automation for high-volume production, and production test technology. What's more, SCI is developing an advanced optical interface technology (patent pending) that, says SCI, may have a significant impact on reducing the cost of fiber-optics manufacturing and may help to solve critical reliability issues related to fiber-to-the-home technology.

Although optoelectronics is a fairly new area for outsourcing, some providers have already reached beyond manufacturing to invest in design. Take Plexus. The provider is now offering an OC-192 (10 gigabits/sec) reference design, "which has just about every optical technology on it," says Bob Kronser, executive VP and chief technology and strategy officer at Plexus. This approach saves development time. "You're picking up anywhere from four to six to maybe eight weeks in the development cycle," he points out. The reference design also acts as a sales tool for Plexus. "Obviously, if we understand the product at a level to design it, then we can build it and test it as well," says Kronser.

Jabil is another case. The provider has invested in developing a design group to provide optical and RF engineering skills to customers needing additional resources for development.

Investing in a technology of the future sounds like a good idea. But with the communications sector in the tank, why do it now? "Last year, the optical electronics portion of the networking business was about 24 billion [dollars]," says Rodolfo Archbold, chief technology office for Manufacturers' Services Ltd. (Concord, MA). "The optimistic projection shows that growing to 28 [billion]. Even if it doesn't grow, it's still a substantial market that's beginning to outsource. So we see opportunities there."

Archbold sees that customers are more comfortable about outsourcing optical manufacturing that they once considered crown jewels. This change, he believes, stems from today's need to cut costs as well as the growth of optical capabilities in the EMS industry.

In fact, an OEM assessment is underway to determine where those capabilities now stand.

Smaller optical OEMs, with no intention to manufacture in the first place, offer another source of growth. Plexus' Kronser describes the recent case of a company whose entire business plan depended on the company capping its size at 100 employees. "So obviously, they will have to look at their supplier for design, test development, manufacturing, and that's really where we come in," he says. Plexus has seen a growing business from such customers over the last couple of quarters, and an estimated half of the 20+ customers added in each of those quarters have some tie to optical.

What's more, Plexus bears good news from the development side, where it takes an optical product anywhere from 12 to 24 months to reach the market. "While we see some of it being delayed, for the most part the optical designs are staying on track," says Kronser. "They were always targeted more for 2002...and if it went into 2003 because of some technology barriers, that was sort of understood." According to Kronser, Plexus has not seen any real change in the optical development side.

Development work is one of the emerging opportunities for PEMSTAR. "Much of the immediate outsourcing opportunities are for cost reduction purposes, but we are starting to see a desire to outsource product development and integration work," says John Chen, PEMSTAR's director of technical marketing.

Still, optical networking is suffering the problems of an immature industry. "The fundamental reason that the fiberoptics telecommunications industry is in such a state of chaos is that fiberoptics is still an emerging technology, characterized by technology breakthroughs, lagging standards, over investment, too many companies competing for the same space, and a lack of high-volume automation processes," states SCI. The company believes its opportunity lies in reducing manufacturing costs, which are still too high. That in turn will bring down the cost of bandwidth.

If there is a common denominator for these optical investments, it is a belief that optical technology is the answer for future bandwidth demand. What will create that demand? For Dan Shea, senior VP and chief technology officer at Celestica, 3G cell phone technology holds the most promise. Compared to today's cell phones operating at 9600 baud, "third generation cell phones take you up above 2 megabits a second. And that is two billion new Internet subscribers coming on-line overnight," says Shea. As a result, a lot of dark fiber will need to be lit up.

Celestica and other providers assume that at some point the optical business will recover. Flextronics' Ron Keith says, "I think when it comes back we'll see a steady 20% per year growth industry for a decade. I don't think we'll ever return to the ridiculous 70% growth."

"We actually are quite pleased with the downturn," says Keith. "The downturn has done a couple of things. It's made everybody reevaluate their captive manufacturing strategy. All the [optical] component guys are reevaluating it. All the module guys are reevaluating it. And that bodes well for our industry." The second thing is a shakeout in the optical component space. "That's going to change the price competitiveness in the marketplace, and it will be good for everybody. Additionally, it's making some potential asset acquisitions available to us at very attractive prices," Keith notes.

He finds companies - whether they produce optical modules, systems or components - now open to asset divestitures. "Nine months ago, if you would have approached some of these companies and said, 'let me buy a factory in location x,' they wouldn't have talked to you," says Keith. "Now they call me three times a week and say, 'we'd like to talk to you about something strategic.' And strategic is now the new euphemism for I want to sell you a plant."

Lucent is a case in point. The company has informed employees of its optical systems plant in North Andover, MA, that it will seek a buyer for manufacturing operations other than system integration, which will be retained (see News, section).

Some EMS providers are not only taking over optical manufacturing processes, they are improving upon them. MMI observed such activity during a recent visit to Celestica's Toronto plant.

"Many of the OEMs in this space have gone out and picked up a suite of equipment, whether it's test equipment or assembly equipment," says Celestica's Dan Shea. So an OEM might end up with a set of fusion splicing equipment from a single supplier to strip, clean, cleave, splice and protect. But buying a suite of equipment goes against the grain for a provider like Celestica used to picking out the best machine for each SMT operation. So Celestica applied its equipment evaluation skills, including experiment design, to find the optimum piece of equipment for each step of the splicing process.

While a provider must be able to splice the various types of fiber as well as dissimilar fibers, that is only one of the optical disciplines that a provider must master. Testing opens up a whole new set of challenges. Problem is, the tests that an OEM's developer uses to validate a design are often not ready for production. They may take too long and require a high level of technical skill and a lot of button pushing.

To automate the process, Celestica has written Labview drivers for test instruments such as bit error rate testers and optical spectrum analyzers. Those drivers also allow Celestica to collect much more data than feasible with button pushing. In the optical world, data becomes essential for such things as calibration at the next level of assembly.

With the drivers in place, Celestica is writing generic test code for subsystems that the provider considers building blocks in the optical networking world. These building blocks consist of optical transceivers, optical amplifiers such as EDFA (erbium doped fiber amplifiers), multiplexers, demultiplexers, optical switch fabrics, dispersion compensation modules and optical performance monitors. Representing an estimated 40% to 70% of what is needed for production, the generic code will save test development time and resources.

Strides are also being made on the component level. In active components such as transmitters or receivers, precise alignment must be achieved since one is dealing with a fiber core, at 9 microns, coupled to a source or detector chip. Flextronics has a patented process that achieves alignment below 0.2 micron. The company has actually licensed this technology to some component companies. Also, Flextronics possesses a proprietary process for direct coupling of a lensed fiber to an active photonic element such as a laser.

But when it comes to advancing the state of the art within the EMS industry, optical OEMs do not make it easy. That's because they have a penchant for secrecy. "We have yet to find a customer that doesn't have intellectual property concerns in this space," says Celestica's Shea. At Celestica, for example, it is not uncommon in the optical area to find one customer team unable to share customer information with another team. In such cases, advances made with one customer cannot be used to benefit other customers.

The industry is also grappling with other issues including the perception on the part of some OEMs that the industry is not ready to build optical systems.

Investing in optical capabilities will help providers solve these problems and pave the way for more outsourcing.

Lucent Technologies (Murray Hill, NJ) has entered into a manufacturing agreement with Celestica (Toronto, Canada) by which Lucent will outsource manufacturing operations in Columbus, OH, and Oklahoma City, OK, to Celestica. These operations had been for sale for some time (Feb., p. 9). What's more, Lucent has told employees in North Andover, MA that it intends to retain a system integration center there, but divest other manufacturing operations.

Under the deal with Celestica, the EMS company will get a five-year supply agreement valued at up to $10 billion. This is the largest transaction that Celestica has announced. Celestica will buy the Columbus plant and property, lease the Oklahoma City facility, and purchase selected equipment and certain inventory. The purchase price is estimated at between $550 and $650 million in cash, representing a "modest premium" over book value, according to Celestica. That price variation reflects the inventory portion of the transaction.

This agreement will make Celestica the primary EMS provider for Lucent's North American demand for switching, access and wireless networking products. Celestica will supply a range of services including NPI, PCB assembly and test, enclosures, system assembly, repair and supply chain management.

But this deal departs from typical divestitures of the past, where production at a divested plant would continue as before. In this case, Celestica plans to transfer most of Lucent's PCB assembly at Columbus and Oklahoma City to existing Celestica plants, some of which are in low-cost geographies. The benefit to Celestica, of course, is that the transfer will raise utilization rates at existing plants and help to counter the effects of the downturn. Lucent also gains by sourcing PCB assemblies from more cost effective sites.

Also in contrast with most earlier divestitures, Celestica will not be taking on all of the manufacturing people at the two sites. That is not surprising given the above plan to move PCBA work elsewhere within Celestica. The provider expects to employ less than half of the sites' combined work force. Lucent reports that a total of about 4500 people are presently involved in manufacturing at the two facilities. Still, some number of people will stay with Lucent to staff a systems integration center in Columbus, and Lucent will also maintain an administrative support center in Oklahoma City. Employment at the two sites had already been reduced from earlier levels (Feb., p. 9).

Neither is Celestica planning to occupy all the space at these two mammoth facilities. The Columbus facility, which produces wireless products, measures just under 2 million ft2, while Oklahoma City, which turns out switching and access systems, takes up about 1.8 million ft2. Space unused by Celestica or Lucent will be mothballed.

At Oklahoma City, Celestica will end up providing basically a complete manufacturing solution for Lucent. "They're not going to be touching hardly anything when we fully complete the deployment of the new model that we're putting in there," said Eugene Polistuk, Celestica's chairman and CEO, in a conference call. Polistuk calls this scenario involving complex system build a wave-five model. Indeed, the Lucent deal will add capabilities for high-end system assembly and test to support the wave-five model.

Celestica will also expand its relationship with Lucent, which began nearly three years ago. "The size and scope of this transaction recognizes the track record and trust that has been built up between the two companies over this time," said Polistuk. He reports that Celestica was the first tier-one provider that Lucent selected.

In addition, the Lucent deal will broaden Celestica's communications portfolio and meet its financial criteria. The provider expects the deal to be accretive to cash earnings within the first year.

Subject to normal closing conditions, the transaction is expected to be completed before the end of Q3.

Celestica also has unfinished business with regard to the unionized workers at Columbus and Oklahoma City. The company does not yet have a ratified agreement with them. But Celestica points to its success in reaching an EMS-competitive agreement with the unionized employees that came over with the Avaya acquisition (Mar., p. 6-7).

In fact, the Avaya deal can be viewed as a precursor to the present one. The earlier deal included the transfer of work to other Celestica facilities and the mothballing and closure of facility space. But Celestica is not the only provider looking for alternatives to the classic take-it-as-it-is divestiture. Ingalls & Snyder analyst Alex Blanton points out that Ericsson is closing two cell phone plants in the UK after Flextronics took over cell phone operations at Ericsson. Ericsson is responsible for the costs of shutting down those plants, just as Lucent is paying severance costs for jobs that are lost in connection with the Celestica agreement.

More recently, Celestica has obtained a $500-million revolving credit facility that brings its total credit facilities to $1 billion. As of the Lucent announcement, Celestica had not drawn against its line of credit. In addition, the company had $1.3 billion in cash at that point. The company must fund both this deal and its acquisition of Omni Industries (June, p. 1-2).

Meanwhile, Lucent is shifting the outsourcing focus to its optical systems plant in North Andover, MA. Late last month, Lucent told employees there that it would keep the system integration portion of North Andover operations and outsource other manufacturing. The company is looking at a variety of alternatives for outsourcing some level of optical subassembly. Selling the entire plant at about 1.95 million ft2 is one option.

According to Lucent spokesperson Mary Ward, the only thing known for sure is that Lucent will be retaining between 600 and 800 manufacturing people for a system integration center. About 2400 people out of about 4000 site employees are engaged in manufacturing at North Andover. Lucent is hoping that an EMS provider will take on the affected 1600 to 1800 employees because of their experience in the optical area. The remaining 1600 jobs in other departments are not impacted by this decision.

Lucent wants to complete a transaction by the end of this year. The company has just begun work on bid documents.

Europe is also on Lucent's outsourcing agenda. The company just met with at least one European workers council to start discussing its restructuring plan confidentially. According to spokesperson Ward, nothing has been decided yet.

What's more, Reuters is reporting that Lucent is seeking buyers for its base station equipment plant in Nuremberg, Germany, with over 700 employees. Up to 600 manufacturing jobs are at risk, according to Reuters.

Teradyne (Boston, MA) has entered into an agreement to acquire a substantial majority of the domestic assets of E-M-Solutions (Fremont, CA), an enclosure manufacturer, and the stock of its foreign subsidiaries. E-M-Solutions has filed under Chapter 11 of the U.S. Bankruptcy Code. The acquisition will expand the capabilities of Teradyne Connection Systems, a Teradyne division based in Nashua, NH.

The agreement calls for a purchase price of up to $85 million. Teradyne expects the deal to be accretive in 2002, adding over $200 million of revenue. Subject to bankruptcy court approval and regulatory review, the transaction is expected to close in Q4.

"This acquisition will strengthen TCS's position as an electronic systems integration partner with our customers," states Rick Schneider, president of Teradyne Connection Systems. "E-M-Solutions' capabilities, including metal fabrication expertise, integration facilities and skilled employees, will enhance TCS's ability to offer vertically integrated electronic manufacturing solutions."

Teradyne has also signed an agreement to acquire GenRad (Westford, MA), a supplier of automatic test equipment and related software.

Solectron (Milpitas, CA) has acquired MCC-Sequel Ltd., a provider of repair, recycling and manufacturing services in Japan. Solectron Global Services previously owned 19% of the company.

The Solectron unit will take over a headquarters operation in Tokyo and a plant in Koriyama. Customers currently served in Japan include Cisco, Compaq and IBM.

New program...Manufacturers' Services Ltd. (Concord, MA) will provide EMS for networking infrastructure products of Enterasys Networks (Rochester, NH), a new company derived from Cabletron. MSL becomes Enterasys' second EMS partner.

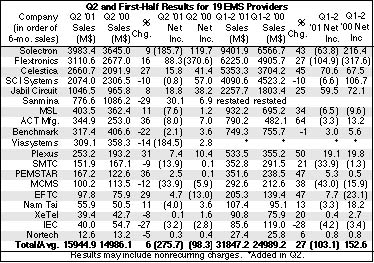

If the EMS industry has one bedrock belief, it's the ability to continue to grow by further penetrating the OEM market. In the past, that ability seemed to be almost unlimited because the industry's market penetration was so low. But the downturn has shaken some widely held beliefs (April, p. 1). Chief among them is the assumption that the industry will grow by 20% or more every year. The downturn has shown that a loss of end market demand, at least over a short period, can overwhelm any growth contribution from outsourcing. If growth is no longer a given, maybe it's time to examine more closely the outsourcing potential that undergirds that growth.

The number that effectively determines the EMS industry's growth potential is OEM market penetration. To calculate penetration, one typically divides EMS market value by cost of goods (COGS) for electronic equipment worldwide. Studies by Electronic Trend Publications and Technology Forecasters put COGS for 2000 at $689.4 billion and $771.8 billion respectively (Nov. '00, p. 7). If the market reached between $112 and $115 billion in 2000, as MMI estimated (Mar., p. 1), then one arrives at a market penetration between 14.5% and 16.7%. Nothing out of the ordinary here. These numbers support the popular rule of thumb that puts penetration in the 15% to 20% range.

But MMI recently came across some numbers that don't jibe with this calculation. As reported in May on p. 4, Bear Stearns & Co. released a new outsourcing poll that found a penetration rate of 28%. This COGS-weighted result represented 105 OEMs accounting for COGS of $576 billion, or 73% of the available market, according to Bear Stearns. The firm attributes this higher than expected rate to a limited participation of Asian OEMs in the poll. Still, if one assumes that the rest of the market (27%), primarily Asian OEMs, outsourced at about 10% on the average, then one can compute a penetration rate of 23% for the total OEM market.

Other outsourcing polls have found much higher penetration rates. An SG Cowen Securities survey of 79 OEMs reported an unweighted penetration average of 54% last year (Sept. '00, p. 4-5). The company said this result might have been biased by OEMs that outsource heavily. More recently, a Technology Forecasters poll found that 53% of participants' COGS was outsourced. Again, this firm points out that its sample was weighted heavily toward OEMs that outsource.

So what is the actual penetration percentage? MMI is not sure of the real number, but the preceding data show MMI that the rate may be above 20%. MMI believes at least part of the difference between calculated and survey penetration rates lies in what OEMs count as outsourcing. Computer OEMs include work done by ODMs, representing well over $18 billion in 1999, as outsourcing. When OEMs buy subassemblies such as disk drives, off-the-shelf motherboards, chassis and power supplies, they are outsourcing in effect. ODM contracts and subassemblies bought by OEMs should be added to EMS sales when estimating the current level of outsourcing. Only then will the EMS industry have a true picture of how much more can be outsourced.