![]()

![]()

Cover Story

CEO Predicts EMS-ODM Consolidation

Market Data

Logistics

Q&A with Flextronics’ Tom Wright

News

Solectron To Divest Seven Activities

SMS Parent To Acquire TotalEMS

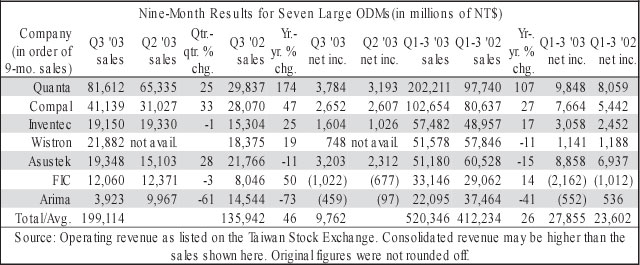

Nine-Month Results for Seven Large ODMs

Clearly, the EMS and ODM industries are converging (Aug, p. 1), and several EMS-ODM deals have come to light. Will there be more consolidation among EMS and ODM companies? One prominent CEO in the EMS industry thinks the answer is yes. “I am on record as having said that I believe this will be a more robust trend in the future,” said Flextronics CEO Michael Marks during a conference call this month.

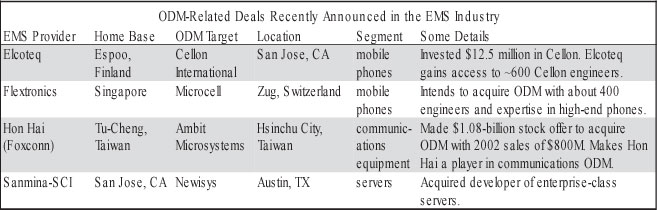

One can cite evidence that EMS-ODM consolidation is underway. Three EMS providers have each announced an acquisition of an ODM-type company in recent months, while a fourth provider made an equity investment in an ODM (see table).

EMS providers are using ODM acquisitions to quickly establish or expand offerings in the ODM space. Hon Hai’s proposed acquisition of Ambit Microsystems will make Hon Hai a player in the ODM niche of communications equipment (Nov., p. 1). Flextronics intends to extend its ODM offering for cell phones into high-end designs with its plan to purchase Microcell (Aug., p. 1-2). And Sanmina-SCI added an ODM capability for enterprise-class servers when it bought Newisys (July, p. 3-4; Aug., p. 2).

These acquisitions reflect a broader trend – the migration of EMS providers into the ODM space. How big is this trend? “I believe that this is actually the direction the whole [EMS] industry is going to move for major segments of the space – not the real high-end, complicated products. But in the consumer space, I think that this is going to be very much a major driver for our industry,” said Marks.

So far, EMS providers for the most part have steered their ODM efforts clear of the PC segment, which is dominated by the Taiwanese ODMs. None of the aforementioned acquisitions involve laptop or desktop PCs. But the bulk of the ODM market still resides with these PCs. If the EMS industry is to penetrate the major segments for ODM products, it must at some point move into the PC side of the ODM space. By the same token, if the EMS and ODM sides are to consolidate in a big way, EMS companies will have to start acquiring major Taiwanese ODMs that are noted for designing PCs, especially laptops.

Recent acquisitions indicate some degree of EMS-ODM consolidation is taking place. But a major melding of the two sides requires that some EMS providers adopt a PC strategy for their ODM businesses. Only when EMS providers decide that they need to acquire ODM capabilities in the PC segment will consolidation begin in earnest.

Flextronics has already dipped its toe into the ODM side of the PC market through its ODM enclosures business. The company is now talking about further participation such as integrating power supplies into its enclosures. What’s more, it has designed a laptop product that combines computing and TV viewing. If Flextronics’ ODM business is headed into the PC market, will other providers follow? The answer to this question will have much to do with how extensively the two industries consolidate.

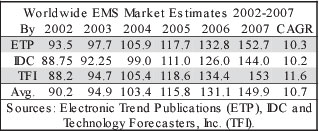

Technology Forecasters, Inc. (TFI) of Alameda, CA, has issued a new five-year forecast for the EMS industry. Reflecting improving end markets and continued outsourcing, the forecast calls for growth to resume this year, followed by a double-digit increase in 2004.

The consulting firm estimates that the global EMS market totaled $94.7 billion this year, up 7.4% from 2002. Next year, the market will grow by 11.3%, topping the century mark at $105.4 billion, predicts TFI. In 2005, the EMS industry will increase sales by 12.5% to $118.6 billion, according to the firm.

TFI’s forecast extends to 2007, when the EMS market is expected to reach $153 billion. This end point corresponds to a CAGR (compound annual growth rate) of 11.6%, which is slightly above but basically in line with two other forecasts in the 10+% range (see table). TFI becomes the third firm to project a future without the dramatic growth that the EMS enjoyed during its boom years (July, p. 1). By averaging the start and end points of the three forecasts, one can compute an overall CAGR of 10.7% for the three (table).

The average market estimate for this year is $94.9 billion, which represents a 5.2% increase over the 2002 average of $90.2 billion. For 2004, the mean forecast for the three firms works out to $103.4 billion, which is 9.0% above the 2003 average.

TFI has lowered its 2002 to 2006 numbers from last year’s forecast (Dec. ’02, p. 2). For example, the 2004 projection dropped by 9.3%.

Compared to the EMS market, the ODM side of outsourcing will see markedly higher growth from 2002 to 2007, based on the TFI forecast. The firm predicts that the ODM market will grow at a CAGR of 21.9% over the forecast period. ODM sales totaled an estimated $41 billion in 2002, and TFI expects the ODM market to hit $110 billion in 2007.

For more information, go to www.techforecasters.com.

IDC (Framingham, MA) has tweaked its forecast from earlier this year (June, p. 1). New projections call for an EMS market size of $92.25 billion this year, or 3.9% above 2002 sales (see table). The firm increased its estimate for 2003 by $2.25 billion from an earlier forecast of $90 billion. In the prior forecast, IDC had expected a flat 2003.

For 2004, IDC foresees growth of 7.3%, bringing market size to $99.0 billion. IDC raised projections by $1 billion for each of the years 2004, 2005 and 2006. For further details, go to www.idc.com.

Some OEMs have reached the point of outsourcing entire supply chains. That means more business for EMS providers that can handle manufacturing and logistics. But a question arises. Do providers rely on logistics companies to supply the logistics network or build their own? Flextronics is betting on the latter, and so far that bet is paying off.

Despite the downturn, Flextronics’ logistics business has flourished. The company entered the business when it acquired Irish Express Cargo in 2000. Since then, the provider’s logistics unit has more than doubled the number of its employees. In September, Flextronics said the unit was up to 7000 employees. Yet little has been published about this thriving unit.

To find out more about it, MMI sought out Tom Wright, president of Worldwide Logistics at Flextronics. Among other things, MMI wanted to know why the company’s logistics business is growing, how large is the logistics network that Flextronics has built, and how this business compares with the competition. Here’s what he had to say.

MMI: Flextronics’ logistics business has been described as booming. Why is this so?

Wright: If you look back over the latest tech boom that got everybody in trouble, supply chains became enormously complicated. Our message is that we’re simplifying the supply chain. Not only is the message resonating well, but the results of our business are resonating well. We’re tying solutions together that help our customers manage their inventory more efficiently and help them get product to market. If we can help our customers to become more nimble, obviously the risks in their business are minimized. I think a combination of all those things is the reason for our success.

Today, many OEMs continue to struggle with how to make their supply chain more demand flow enabled. They have the ability to take information and move to a pull model as opposed to a push model. I’m not going to say that what we provide is the perfect pull model. But the combination of what we offer between logistics and manufacturing and how those functions are integrated today within Flextronics really do give our customers a much better opportunity to enable a pull model for their own supply chain.

The other piece of this offering is repair and reverse logistics. We have purposely not gone the acquisition route on the repair side. Obviously, Flextronics has made many acquisitions. But in this particular space, we just thought that we would be much better off building a greenfield system and integrating it with our standard ERP.

The reverse logistics piece is not an adjunct to the supply chain offering that we provide our customers. It’s part and parcel of the whole solution.

MMI: What can you say about the growth of your logistics business?

Wright: It’s big. This has turned out to be a very big business.

MMI: How many logistics centers do you operate and where are they?

Wright: Today, we have 18 primary logistics centers around the world. These are dedicated facilities. Floor space is over 9 million ft2. Clearly, it is not the largest physical logistics network in the world. But it’s pretty formidable. We’re in all three primary geographies – the Americas, Europe and Asia.

MMI: Do you have any plans to expand within those geographies or elsewhere?

Wright: Right now, we’re pretty satisfied with how the network is located. The dedicated logistics centers either are part of our campus strategy or reside right in the middle of a primary market close to our OEMs’ customers.

Quite frankly, we don’t see extending that network much farther as part of our strategy. This could happen over time, but you have to account for the distribution channels and the retail channels. Already they have a fairly extensive distribution infrastructure both in Europe and in North America. We want our logistics network to feed efficiently into those networks.

MMI: We assume Flextronics does not own any transportation carriers. How does your logistics offering compare with third-party logistics providers?

Wright: We actually do have a small transportation business in Ireland and the UK. But that is not core. It’s just part of a legacy acquisition.

What differentiates us from the third-party logistics suppliers and maybe distribution companies is that we don’t outsource the logistics function. It’s not that we won’t partner with a third-party logistics supplier, but we think a key part of our value proposition is that we are actually in direct management control of the logistics operation. Where possible, we pull manufacturing processes into the logistics operation because there are lots of like processes between logistics and manufacturing – quality, engineering, new product introduction and so forth. So the logistics operation leverages what we’ve already established and matured within our manufacturing operations.

The difference between the third-party logistics suppliers and us basically lies in how they drive revenue versus how we drive revenue. We will actually take inventory ownership where it’s appropriate. We won’t take market risk, but we’ll take the inventory risk through the point of product transfer to our OEM customer.

MMI: Other EMS providers say they also offer logistics. How do you differentiate Flextronics’ logistics offering?

Wright: First and foremost, it’s not an add-on service. I don’t want to knock our competitors, but I think most of our competitors have teamed up with third-party logistics suppliers as opposed to building their own logistics network. We believe that having control over the logistics operation is key.

For an end-to-end solution, I think that we can demonstrate a higher degree of credibility because we are actually operating both ends of the supply chain, the logistics and distribution end as well as the manufacturing end. It’s tough to be a legitimate option where end-to-end solutions are concerned. I think you must have logistics operations as a core competency.

MMI: Carriers often have their own logistics businesses. Yet you’re depending on them to move stuff around. Is there any conflict there?

Wright: I’d say yes and no. Just the services side of the logistics business in the US is about $100 billion. So there’s plenty of market share to be spread around.

I think we’re OK living in a world where sometimes your competitor is your supplier or vice versa. We successfully work today in that type of a marketplace. The playing field tends to be a fairer going forward when you have these very complicated relationships within the supply chain.

MMI: Because they keep people honest?

Wright: That’s just one man’s opinion. I have large partnerships where, if I’m not playing fair on a deal when competing with partners head to head, it will come back to haunt me.

MMI: Flextronics has said its logistics business has an advantage over independent logistics companies because its logistics business can leverage the corporation’s SG&A.

Wright: This is where we have a big advantage just because of our ability to leverage things such as engineering, inventory management practices, HR and our campus structure.

We know that we are top of class in that area.

MMI: Flextronics has also said that its logistics business does not require as much capital as some other businesses do.

Wright: We like the logistics business because it doesn’t require as much capital. The capital requirements for the logistics business tend to be tied up in lower-level materials and physical infrastructure that typically doesn’t require as much capital. Capital requirements aren’t great, but that doesn’t make the business simple. It’s a very complex business.

MMI: When it comes to facilities, you’re not buying SMT equipment and expensive testers. You’re basically putting up warehouse space. Correct?

Wright: That’s right. The biggest investment tends to be IT when you really boil it down.

MMI: Is your business able to generate margins that are higher than in the EMS business?

Wright: Generally, the margins are higher, but they’re not a whole bunch higher. Keep in mind it’s all relative because on the contract manufacturing side of the business you have a very high material content, large volumes and lots of revenue. So the margins there will be smaller.

The logistics margins, though they tend to be slightly higher than on the contract manufacturing side, are related to the value add and material content. Quite frankly, we have some logistics deals that look very much like an EMS deal because there’s a high degree of product transformation at the logistics center. That means lots of material content and low value add.

MMI: What percentage of your business is logistics only? Do you expect this percentage to shrink?

Wright: A fair guess is that it’s less than 15%.

MMI: So it’s not that significant.

Wright: It’s really not. I think over time it’ll shrink, probably staying somewhere between 10 and 15%. As part of our strategy, we always want a diversified revenue portfolio. So we’re not abandoning logistics-only deals.

We want to keep our infrastructure efficient. Part of doing that is making sure you have a diversified revenue portfolio.

MMI: How important has logistics become in winning manufacturing programs?

Wright: We believe that we have already made a great deal of progress and continue to make progress in helping our customers move their products to the low-cost regions. Going forward, we see great opportunities partnering with our customers to help them manage their total product life-cycle costs and how their products physically reach end markets.

MMI: Flextronics acquired HP’s distribution center in Memphis this year. How is it being used?

Wright: Through acquisitions, we had operations in Nashville and Memphis. This particular acquisition gave us an opportunity to consolidate Nashville into Memphis and to have a very large presence in Memphis. The transportation networks between Asia, Europe and Memphis are very robust.

In our build-to-order business, we want to be able to take orders today, configure them today and ship them today. You really can’t do that from any other location but Memphis.

Memphis also represents an opportunity for us to utilize our infrastructure more efficiently. We don’t have 7 o’clock courier cutoff times like we would have in Nashville and maybe other parts of the country. We’re tendering shipments to FedEx and carriers after midnight for delivery next day. So you’re taking inventory out of the supply chain by increasing the velocity of the supply chain.

It’s also important to give customers the ability to be nimble so they can respond to their customers very quickly. We can configure product to the specific customer requirement and get it directly to the [end] customer very quickly. Not in all cases is delivery next day, but it’s within one to three days as opposed to weeks.

MMI: It appears that IT is the secret sauce of the logistics business. What can you say about your IT?

Wright: Our secret sauce is that we have committed to a standard platform – a standard ERP system as well as the complementary systems that are around that ERP system. So there’s a standard model that every site uses whether it’s in logistics or in manufacturing.

MMI: What are your challenges besides growing the business?

Wright: Logistics is trickier than manufacturing because when you’re outsourcing logistics, the processes that define logistics are much closer to the OEM’s end customer than the manufacturing side. We’re touching the OEM’s customer in a much more profound way than we would have by manufacturing and shipping product from Mexico or from Asia. So trust must be built up over time. But it’s a challenge for us to get on that path with the OEM.

I would also point out that we have some competitors that are pretty aggressive and very good. I think that’s always a challenge. But it’s a good challenge because it keeps us on our toes.

Back to TOC

Solectron (Milpitas, CA), which has been shopping noncore businesses, has disclosed all but one of the activities to be divested (Oct., p. 7; July, p. 6). The company has signed a definitive agreement to sell its Dy 4 Systems business to Curtiss-Wright (Roseland, NJ) for $110 million. In addition, Solectron will divest Stream International, SMART Modular Technologies, Kavilco, Solectron’s Micro Technology division, Solectron’s 65% interest in U.S. Robotics, and an unnamed company. Solectron plans to identify this company when the process of divesting it is further along.

With annual sales of about $72 million, Dy 4 is a supplier of commercial off-the-shelf embedded computing solutions for the defense and aerospace markets. Dy 4, a business unit of Solectron’s Force Computers, became part of Solectron when the company acquired C-MAC Industries in 2001. C-MAC had acquired Dy 4 the year before.

Solectron’s plan to divest Stream International, a call-center business acquired in 2001, shows that call centers no longer figure in the provider’s strategy for postmanufacturing services. Solectron has also decided that the memory modules, memory cards, and communications products supplied by SMART Modular do not fit in with Solectron’s plans. In addition, Kavilco’s sensors and the Micro Technology division’s hybrid circuits and frequency products have been deemed noncore as well. Solectron obtained Kavilco and the Micro Technology business when it acquired C-MAC. Finally, Solectron is giving up its stake in U.S. Robotics, a supplier of wireless and wired networking products and modems. Solectron gained ownership in U.S. Robotics through its acquisition of NatSteel Electronics in early 2001.

Dy 4 has primary operations in Ottawa, Canada, its home base; Leesburg, VA; and the UK. Key customers include BAE Systems, DRS Technologies, General Dynamics, Northrup Grumman, Lockheed Martin and Raytheon. According to Curtiss-Wright, Dy 4 is profitable.

When the transaction is completed, Dy 4 will operate as a business unit of Curtiss-Wright Controls (Gastonia, NC), a subsidiary of Curtiss-Wright. The deal is expected to close in early 2004.

Founded by the Wright brothers and aircraft designer Glenn Curtiss, Curtiss-Wright is a multinational provider of metal treatment, motion control and flow control systems for the aerospace and defense industries.

Spectragraphics Corporation (SGC), the parent company of EMS provider SMS Technologies (San Diego, CA), has signed a definitive agreement to acquire TotalEMS (Logansport, IN), another EMS provider. The purchase price was not disclosed.

TotalEMS will operate under the name Total Electronics once the deal closes by the end of the year. This acquisition forms a combined company of over 300 employees with manufacturing in California, Indiana and Reynosa, Mexico. The two SGC divisions will operate independently as wholly owned subsidiaries, but will share resources and technology.

SMS primarily serves the medical, telecom, computer, aerospace and military segments. TotalEMS has a strong presence in the automotive, industrial, HVAC, security and memory module markets with customers located mostly in the Midwest. Major customers of TotalEMS include General Motors, Delphi, CEI, The Trane Company, Brunswick, Dover Industries, Landis & Gyr (Siemens), LSI, Valeo and Bombardier.

Deals done...Advanced Digital Information Corp., or ADIC (Redmond, WA), has finalized its outsourcing agreement with Benchmark Electronics (Angleton, TX). As part of the agreement, about 150 ADIC employees from affected operations joined Benchmark (Oct., p. 4). The provider also assumed ADIC’s lease on its Marymoor facility in Redmond and purchased inventory associated with the outsourced work. The agreement expands an existing outsource relationship to include a significant portion of ADIC’s entry-level and workgroup tape automation product line….Chase Corp. has sold its EMS subsidiary, Sunburst Electronics Manufacturing Solutions (West Bridgewater, MA), to the Edward L. Chase Revocable Trust in exchange for shares of Chase common stock currently held by the trust. The purchase price was $3 million.

New programs…Celestica’s Kidsgrove, UK facility will supply PCB assemblies to ITT Defence for radios supplied under the UK Ministry of Defence’s Bowman program for voice and data communications within the UK armed forces, according to EE Times UK. Some 40,000 ITT radios will be manufactured in Basingstoke, UK, for the Bowman progam. Also, Celestica will produce vehicle data recorders for Safety Intelligence Systems and IBM, who together will supply the black boxes and build a crash-data network under an agreement with the Irish government, Business Week reported recently. Earlier this year, IBM and Celestica entered into a partnership to supply telematics devices (May, p. 6). Finally, Celestica will provide EMS for Gametrac products from Tiger Telematics (Jacksonville, FL). Coming to the UK market, the Gametrac flagship device is a handheld wireless console that combines 3D gaming, SMS text, MP3 music with remote download, video playback and a digital camera....Acopia Networks (Lowell, MA) has selected Jabil Circuit (St. Petersburg, FL) to perform PCBA and subassembly work for Acopia’s family of network switches….Elcoteq Network (Espoo, Finland) will manufacture various GSM and UMTS related subsystems for Kathrein-Werke KG, a communications OEM….Start-up Mangrove Systems (Wallingford, CT), which is developing a family of multiservice switching systems, has chosen IEC Electronics (Newark, NY) to provide all of Mangrove’s EMS requirements….SMTEK International (Moorpark, CA) has landed a medical contract expansion worth about $6.5 million and two new contracts totaling about $9.5 million in aerospace and industrial instrumentation. The medical work will go to Thailand, while the other two programs will be handled in the US....Nam Tai Electronics (Macau, China) has received orders to manufacture CMOS image sensor modules for Appeal Telecom, a Korea-based provider of CDMA mobile handsets and an ODM partner of Motorola. This win marks Nam Tai’s entry into the Korean manufacturing market.

More new programs...DRS Technologies (Parsippany, NJ) has won defense contracts with a combined value of $5.0 million. The company will supply card assemblies, cables and harnesses for several platforms, including the US Navy F/A-18 Super Hornet, the US Army’s M-270 Multiple Launch Rocket System, Japan’s F-2 jet fighter and a satellite program. This work will take place at the DRS Flight Safety and Communications unit in Carleton Place, Ontario, Canada….Lockheed Martin has awarded LaBarge (St. Louis, MO) a $6.6-million contract to produce complex wire harnesses for the Atlas V launch vehicle. In addition, Rockwell Collins has named LaBarge a preferred supplier for cable assembly. ...Winland Electronics (Mankato, MN) has entered into a supplier-managed inventory agreement with EMS customer Select Comfort, a bed retailer, which has increased its orders to Winland by about $4.8 million. Included are two new assemblies that had been produced in China. Parker Hannifin, Electromechanical Division (New Ulm, MN) has also contracted Winland to manufacture board assemblies, which are expected to generate about $1.5 to $2.0 million in annual sales for Winland. The Parker division, a new customer, designs and manufactures DC servo motors, motor controllers, amplifiers and linear motion products….CirTran (Salt Lake City, UT), a provider of PCB assemblies, cables and harnesses, will serve as the primary supplier to Meret Optical Communications (San Diego, CA), a subsidiary of Sorrento Networks.

Flextronics (Singapore) has reached a settlement in the Beckman Coulter lawsuit, where a jury handed down an unexpectedly large verdict (Oct., p. 6). The provider has agreed to pay Beckman $23 million to make the jury’s $934-million verdict go away.

“Although the settlement remains larger than we believe the law would have allowed, it relieves the company of the significant burden and distraction that the original verdict imposed,” stated Michael Marks, Flextronics CEO.

This month Marks told analysts, “We determined, as many companies do in similar situations, that the cost of pursuing the 100% victory was too high. We determined that our costs to pursue that appeal in time, money and potential business disruption were greater than the cost we agreed to pay to settle.”

As a result of the settlement, Flextronics will take an unusual charge of about 3 cents per diluted share in the December quarter. This charge accounts for the amount of the settlement in excess of the company’s previous accrual about $8 million set aside for this matter.

In September, Marks said Flextronics believed that its liability would be no more than $10 million. According to Marks, the company later stated that its liability most likely would be $8 million.

“We are even more convinced today that we had a strong legal position as court decisions were issued in the last few weeks that again say that punitive damages should be held to a small multiple of the actual damages awarded, which in this case were only $3 million. We also remain convinced that tort claims in which punitive damages can be awarded are not allowable in disputes over performance of a business contract,” said Marks in this month’s conference call with analysts.

Back to TOC

More financial news… For the November quarter, Solectron reported that sales from continuing operations totaled $2.70 billion, up 11% from the prior quarter and 1% from a year earlier. The net loss from continuing operations was $52.2 million, including $27.0 million in restructuring and impairment charges from those operations. GAAP net loss was $120 million….Jabil Circuit recorded November quarter sales of $1.51 billion, a gain of 41% over the year-earlier period. Net income for the quarter climbed to $42.5 million, compared with $8.4 million a year earlier….For the quarter ended Oct. 31, SigmaTron International (Elk Grove Village, IL) reported a 5% increase in sales year over year to $23.8 million. Net income for the quarter amounted to $1.8 million, up 59% from $1.1 million a year earlier. For the first six months of fiscal 2004, sales grew by 10% to $45.9 million, while net income went up 78% to $3.1 million…. Last month, Nasdaq notified SMTC (Toronto, Canada) that its stock failed to comply with the minimum bid requirement under Nasdaq rules and therefore is subject to delisting. Seeking a continued listing, the company has requested a hearing before a Nasdaq panel. The stock will continue to trade on Nasdaq pending a determination of the panel.

Some Asian results…Q3 sales for Venture (Singapore) increased 36% year over year to S$921.5 million, while 9-month sales grew 45% to S$2.30 billion. Q3 net profit after minority interests amounted to S$65.8 million, a gain of 39% over a year earlier….PCI (Singapore) reported Q3 sales of S$74.4 million, up 120% year over year, and Q3 profit after minority interests came to S$4.0 million….In Q3, GES International Limited (Singapore) saw its ODM sales increase 27% from a year earlier to S$56.1 million, as EMS revenue declined to S$41.5 million from S$46.3 million. Profitability from ODM and EMS activities improved by 27% to S$5.8 million….For the six months ended September, VTech (Hong Kong) reported that its EMS sales decreased by 11% to $48.1 million, while profitability was stable.

In an unusual move for an EMS provider, Pinnacle Electronics (East Pittsburgh, PA) has used a subsidiary to acquire a products business. The subsidiary, Pinnacle Point-of-Sale, has purchased from Aspeon (Irvine, CA) certain assets that include the technology for Javelin point-of-sale products that Pinnacle Electronics had been exclusively manufacturing and distributing since July. This acquisition gives Pinnacle sole rights to manufacture, market and develop the Javelin POS equipment.

With a history spanning more than 100 years, Pinnacle Electronics designs and manufactures PCB assemblies and electronic/electromechanical systems for a diverse customer base. Markets served include medical, instrumentation, factory automation, transportation and communications.

Operating a 144,000-ft2 facility in East Pittsburg, the company posted a 47 percent revenue gain for the three-year period from 2000 to 2002. The Pittsburgh Business Times recently ranked Pinnacle as the second fastest growing company among privately owned Pittsburgh-area companies in the manufacturing sector.

New offices…Fabrinet (Bangkok, Thailand), an MMI Top 50 EMS provider in 2002, has opened its first European office in Mommenheim, Germany. The office will provide sales, engineering and customer service in support of Fabrinet’s expanding European customer base. Offering a cleanroom environment for manufacturing, Fabrinet can provide either high- or low-volume production in Thailand….Elcoteq Network (Espoo, Finland) has moved its Americas headquarters to a new facility in Irving, TX. Growth in sales and services and an increase in personnel created a need for the new offices, which are 60% larger than the old space.

New facility…Sparton (Jackson, MI) has purchased a 110,000-ft2 manufacturing facility in Albuquerque, NM, from Honeywell. The control products facility will serve as the new center of operations for Sparton in the Southwestern US. The company will close its facility in Rio Rancho, NM, and move operations to the new center, due to be occupied in the spring of 2004 after it is remodeled. Compared to the old facility, the new center will accommodate products with greater technical requirements as well as provide more floor space.

Certifications…Sanmina-SCI’s Defense and Aerospace Systems division in Huntsville, AL, has achieved AS9100 certification. AS9100 is a quality system standard for suppliers to the aerospace industry….The Moorpark, CA facility of SMTEK International has also been certified to AS9100….Electronic Product Integration Corp. (Rochester Hills, MI) has announced that its EPIC Technologies facilities in Norwalk, OH; El Paso, TX; and Juarez, Mexico, have attained certification to ISO/TS16949:2002. This is a new global standard for automotive quality systems (Sept., p. 3-4)….Able Electronics (Hayward, CA) has achieved compliance to ISO9001:2000 for both its Silicon Valley and Mexico facilities….TeligentEMS (Havana, FL) has also earned certification to ISO9001:2000….VTech’s EMS business has attained ISO13488 and TS16949 certifications, allowing VTech to produce medical equipment and automotive products respectively.

Finland’s Elcoteq has chosen a new CEO from within its ranks to succeed its current CEO, who will join another Finnish company next year. The new president and CEO will be Jouni Hartikainen, now president, Asia Pacific. On Jan. 1, 2004, he will take over from Lasse Kurkilahti, who will leave at the end of May 2004 for the Finnish chemicals group Kemira, where he will become its president and CEO. Until then, Kurkilahti will handle special duties for Elcoteq.

The provider has also appointed Jukka Jäämaa to the newly created position of executive vice president, also effective Jan. 1. He currently serves as president, Communications Network Equipment/Industrial Electronics, Europe.

More personnel changes…Dave Purvis has joined Solectron as executive VP, worldwide design and engineering services. Most recently he was senior VP and chief technology officer at John Deere….The non-executive chairman of Venture (Singapore) died this month. Also, the company has named Soo Eng Hiong as executive VP and GM of business development. He comes from within the Venture Group of Companies….Kimball Electronics Group (Jasper, IN), the EMS subsidiary of Kimball International, has promoted Kevin Smith to VP of North American Operations. He will oversee four plants….PEMSTAR (Rochester, MN) has hired Steven Goreham to lead its Communications Business Unit. He is a 25-year veteran of the communications industry.