![]()

![]()

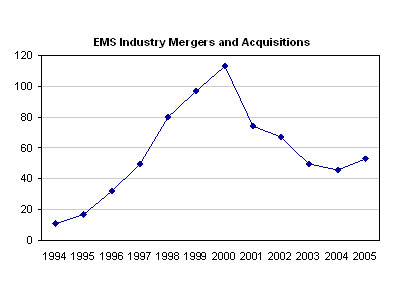

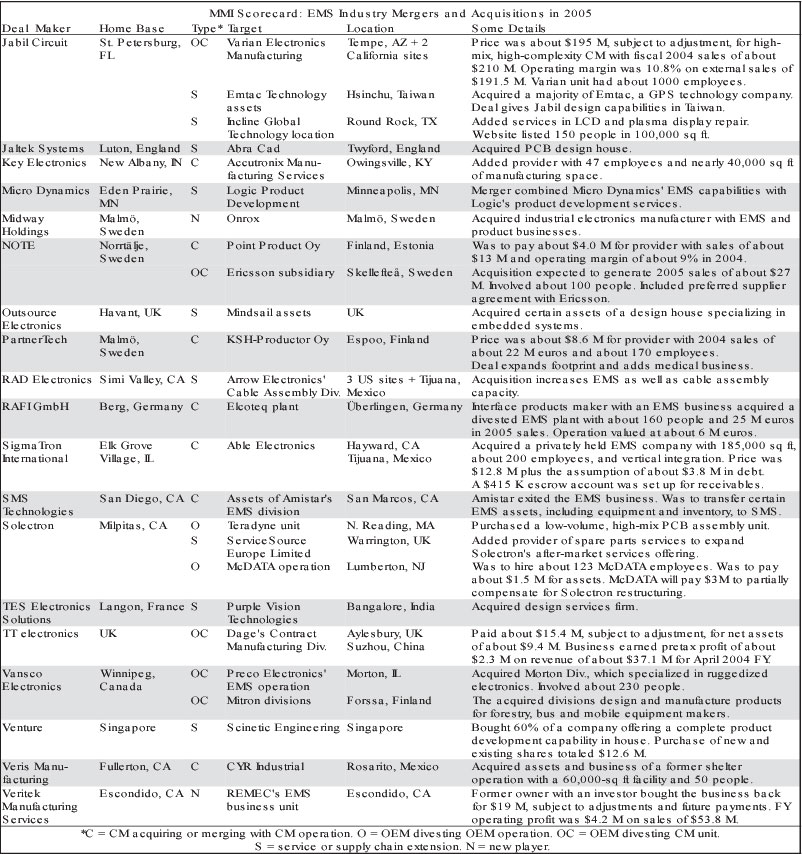

After four straight years of decline, the number of EMS industry mergers and acquisitions increased 15% last year. The total of industry transactions in 2005 rose to 53 from the previous year’s sum of 46. Not only has the downward trend in acquisitions been arrested, the deal making line has taken a turn upward (chart below). Note that last year’s transactions exceeded the number made in 2003. While one data point does not signify the birth of a new cycle of increasing acquisitions, it does show that deal making has at least stabilized over the last three years.

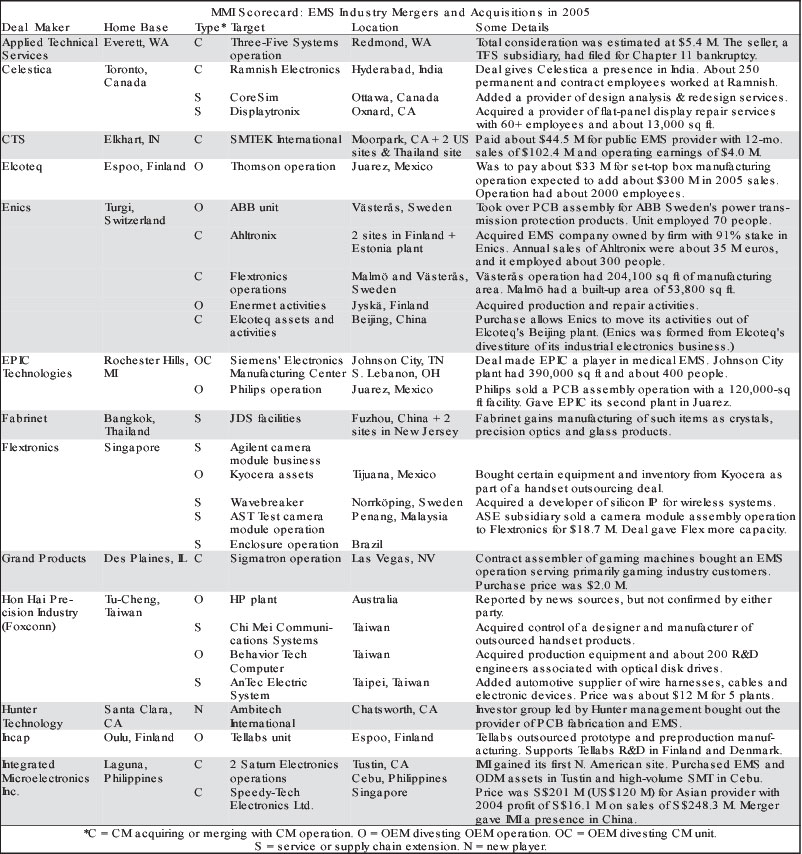

M&A activity persists despite the fact that the EMS industry has consolidated at the top and is maturing within its ranks. MMI’s annual Scorecard of M&A deals lists the EMS industry mergers and acquisitions completed in 2005, as tracked by the newsletter. (See first table below.)

Providers continue to find reasons for making acquisitions. As in the past, motivations vary, and for 2005 MMI has come up with five deal categories, reflecting different rationale behind last year’s transactions.

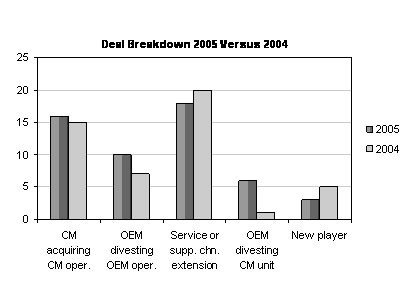

As in 2004, the most common reason for making an acquisition in 2005 was to add capabilities, either to build up non-manufacturing services in such areas as design or repair, or to expand supply chain offerings vertically in components or related areas. MMI calls such deals service or supply chain extensions, and they are labeled “S” on the Scorecard. Last year, 18 transactions of this type were completed, down somewhat from 20 in 2004 (see chart below).

Service or supply chain extensions allow a provider to add capabilities much faster than would be possible if they were developed internally. For large providers, these deals often require relatively small amounts of capital, another selling point. But such deals are typically more expensive than home-grown capabilities. And one top-tier provider, Flextronics, recently announced that for this reason it will eschew acquisitions in the development of its power supplies business. If this home-grown strategy gains traction among other providers, it will have a dampening effect on future M&A.

Another M&A motivation arises when an EMS provider’s growth strategy includes acquiring the assets of another EMS provider. Designated “C” on the Scorecard, such deals usually add revenue and customers and often expand the acquirer’s geographic reach. The acquired businesses may well involve market niches that buyers want to grow in. Restructuring also spawned some transactions where a provider acquired one or more facilities divested by another provider.

In 2005, acquisitions of EMS assets from another provider held nearly steady from a year earlier. The 2005 Scorecard contains 16 transactions of this kind, versus 15 recorded in 2004 (chart above). In only one case, was this type of acquisition made by a tier-one provider. In general, such deals appeal to smaller providers that are looking to expand their business and footprint through the acquisition of a local or regional operation.

Providers also picked up EMS assets through a less common transaction in which an OEM sold off a contract manufacturing unit. With more and more OEMs treating manufacturing as a noncore activity, one might have questioned whether such transactions were still possible. But in 2005, MMI found six cases, marked “OC” on the Scorecard, where an OEM divested an EMS business. By comparison, in the previous four years there was but one transaction in this category, and the deal closed in 2004. (That deal was reclassified as OC after a review of the 2004 Scorecard.)

The divesting OEMs determined, as others before them, that it no longer made sense to devote resources to an EMS business. OEM-owned EMS operations hark back to an earlier time when some OEMs sought to keep their manufacturing and sell excess capacity.

By considering the foregoing two types of transactions, you can obtain a measure of consolidation. The idea is to calculate the number of EMS providers subsumed by acquisition. Starting with 16 EMS operations acquired by other providers, you subtract four EMS facility divestitures by providers that continued with other EMS operations. To the remaining 12, you add the six EMS operations sold by OEMs for a total of 18 EMS providers lost to acquisition. Using the same method for 2004 deals and adjusting for the debut of one new EMS business, you would come up with a net of 15 providers subsumed. So by this measure, consolidation did increase as acquisitions claimed 20% more providers in 2005 than in 2004.

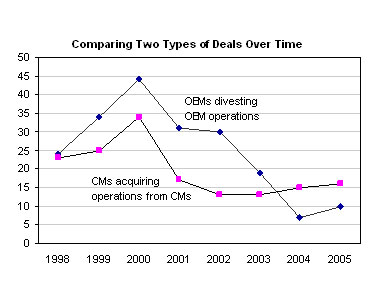

Outsourcing agreements sometimes create yet another type of transaction. There are cases, labeled “O” on the Scorecard, where an EMS provider buys assets of an operation being outsourced by an OEM. Often, but not always, in this kind of deal the provider takes over the OEM operation. Although these deals are not as numerous as in their heyday (see chart below), they did account for ten transactions in 2005, up from seven the year before. Interestingly, there was not a single multisite transaction among these deals.

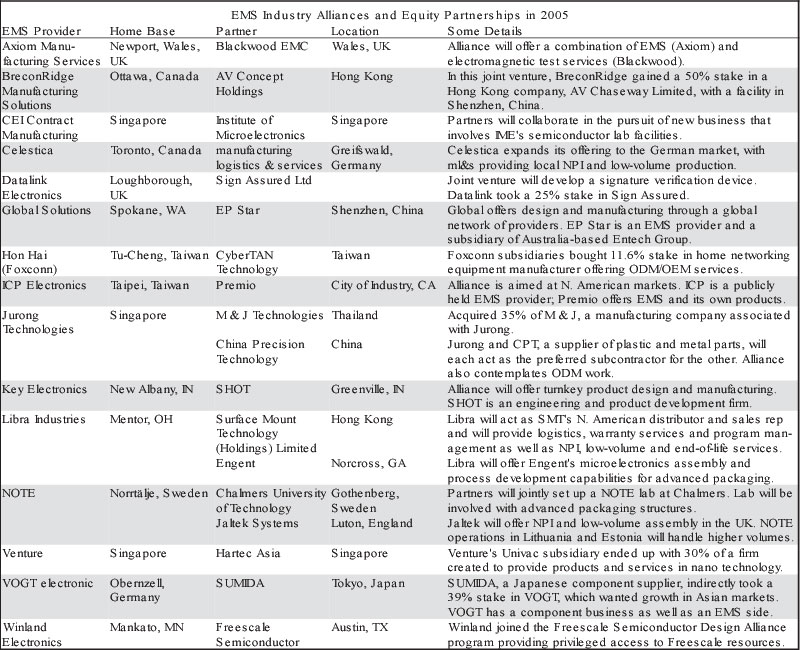

Celestica (Toronto, Canada) will acquire Powerwave Technologies’ manufacturing operation in the Philippines under a new agreement that will result in Celestica becoming Powerwave’s preferred outsourcing provider.

The tier-one provider will pay about $19 million in cash for the Powerwave operation, including buildings and all inventory and equipment at the site, located in Cabuyao Laguna, near Manila. In addition, the operation’s entire work force – about 600 strong – will join Celestica.

The site, which mainly produces power amplifiers for wireless infrastructure networks, will continue to manufacture products for Powerwave (Santa Ana, CA), a supplier of wireless network equipment. In September 2005, Powerwave obtained the facility in an acquisition of wireless assets from REMEC.

As part of the outsourcing deal, the two companies have entered into a multiyear supply agreement, which will expand Celestica’s relationship with Powerwave. Celestica has served Powerwave as a strategic EMS provider since 2002.

Subject to certain closing adjustments and conditions, the transaction is expected to close in March.

“With a highly skilled work force and low cost structure, the Philippines remain a very strategic manufacturing locale for Powerwave,” stated Ronald Buschur, the company’s president and CEO. “This arrangement allows Powerwave to leverage the electronic manufacturing services model to maintain operational flexibility and reduce costs, yet still have access to technical talent and manufacturing capacity.”

For Celestica, the deal adds new capabilities and capacity in the Asia-Pacific region, according to a statement released by both companies.

The deal will also mark Celestica’s second acquisition in the Philippines, a country mostly bypassed by global providers during their expansion into Asia. In 2004, Celestica purchased NEC assets in the Philippines.

More new programs…Celestica has also expanded its relationship with Thales, a international electronics and systems group serving defense, aerospace, security and services markets. Under a new agreement, Celestica will serve as a dedicated EMS provider for Thales’ products. Thales has been a Celestica customer since 2004. Celestica is the second tier-one provider in recent months to announce an agreement with Thales (see Jan., p. 7).…Telco Systems (Foxboro, MA), a provider of carrier-class transport and access solutions for IP and TDM networks, has selected SMTC (Toronto, Canada) as a provider for PCB assembly and full chassis fabrication, integration and testing. Telco is a subsidiary of BATM Advanced Communications….Sparton (Jackson, MI) has secured three contracts, totaling more than $24 million, for the manufacture of sonobuoys for the US Navy….L-3 Communications Security and Detection Systems has awarded LaBarge (St. Louis, MO) a contract valued at over $18 million to produce subassemblies for an airline baggage screening system. When added to an L-3 contract won by LaBarge last spring, this award expands the company’s involvement to the production of higher-level electronic assemblies for the explosives detection system.

Flextronics (Singapore) has purchased World Wide Licenses Limited (WWL), a Hong Kong-based subsidiary of The Character Group chiefly engaged in the design, development and manufacture of digital cameras.

The purchase price amounts to about $17.98 million, which consists of $16 million in goodwill and about $1.98 million relating to the value of stocks and assets. Flextronics is holding back about $1.8 million for one year as security for any claims against WWL.

MMI’s take on this deal is that it will bolster Flextronics’ efforts to build an ODM business in digital cameras. In September 2003, Flextronics told investors that it planned to develop a series of cameras. Since then, the company has said little, if anything, about this ODM activity.

WWL comprised Character Group’s Digital Division, whose key role is the design and development of digital interactive products. Having entered the digital camera market in 2000, WWL has supplied well over two million digital cameras.

The Group stated that the sale of WWL will allow it to focus entirely on development of its toys, games and gifts businesses.

In the fiscal year ended Aug. 31, 2005, the WWL business recorded profit before tax of about £0.8 million.

Meanwhile, Nortel and Flextronics have agreed to postpone the transfer of Nortel’s manufacturing operation in Calgary, Canada, to Flextronics. Part of a larger pact, the transfer has been rescheduled from Q1 to Q2 2006 to allow for completion of several major information systems changes.

PartnerTech (Malmö, Sweden) has bought all the stock of Th Kristiansen AS (Moss, Norway), a contract manufacturer specializing in sheet metal working as well as development, production and distribution of complete systems and machinery. The acquisition further strengthens Partner-Tech’s presence in the Nordic market.

For the Th Kristiansen stock, PartnerTech will pay up to NOK 55 million ($8.1 million), consisting of cash and about NOK 30 million ($4.4 million) in PartnerTech stock. A small percentage of the cash will be disbursed within one year. Surplus values and goodwill will total an estimated NOK 15 million ($2.2 million).

Annual sales of the acquired business exceed NOK 170 million ($25.0 million), and it employs some 140 people. Th Kristiansen is located near Oslo, not far from major PartnerTech customers in the manufacturing, engineering and medical technology sectors. PartnerTech describes the acquired company as having “top-notch expertise in sheet metal working, particularly when it comes to complex mechanical solutions.”

The acquisition “not only provides us with a good platform for further expansion in the Norwegian market, but also enhances our own skills in special competence areas,” stated PartnerTech CEO Mikael Jonson.

The takeover is retroactive to Jan. 1, 2006 and is expected to have a positive effect on PartnerTech’s earnings.

Universal Scientific Industrial (Nan-Tou, Taiwan), a top-ten EMS provider in 2004, plans to enlarge its motherboard business through the acquisition of ABIT Computer’s motherboard division to be carried out by a new USI subsidiary.

USI will pay NT$350 million ($10.8 million) in cash and 20 million preferred shares of the new subsidiary for the motherboard division, which includes ABIT’s brand as well as patents, products, business and people. Adding ABIT’s annual motherboard shipments of about 2 to 2.5 million units, USI expects its annual motherboard output to increase to more than 10 million units in the future.

Adaptec (Milpitas, CA), a supplier of storage solutions, has signed a definitive agreement to sell its block-based systems business to Sanmina-SCI’s ODM subsidiary, Newisys. This deal follows on the heels of an agreement by which Adaptec will divest its Singapore manufacturing facility to Sanmina-SCI (Jan., p. 7).

Under the terms of the new agreement, Newisys will assume most OEM contracts for Adaptec block-based systems customers. Through a licensing agreement, Adaptec will continue to supply certain hardware and software components to Newisys. Similarly, Newisys will provide Adaptec with block-based system products for sale through the channel.

Block-based systems products are based on a modular platform of interoperable components, systems and software that can be leveraged to deliver unique storage solutions.

JDSU (San Jose, CA), the broadband and optical equipment supplier formerly known as JDS Uniphase, has entered into a definitive agreement to sell its manufacturing operations in Ottawa, Canada, to Fabrinet (Bangkok, Thailand), its contract manufacturer. This agreement follows Fabrinet’s acquisition of three JDSU sites in 2005 (June 2005, p. 7; May 2005, p. 5) and two JDSU operations in 2004 (Nov. 2004, p. 6).

The deal is expected to close in the March quarter. Upon closing, Fabrinet will manage ongoing production and the transfer of Ottawa manufacturing activities destined for Asia. This transaction marks the final phase in JDSU’s plan to move all optical communications assembly manufacturing to Asia.

Flextronics recently revealed that it is building an industrial park in Ukraine, an up-and-coming source of low-cost labor in Eastern Europe.

During an earnings conference call on Jan. 31, Flextronics CEO Mike McNamara mentioned that the company is building industrial parks in India and Ukraine. Flextronics had already announced its plan to locate a campus in India (Oct. 2005, p. 3), but this was the first mention of an industrial park in Ukraine.

More new facilities…Flextronics is also expanding its rigid PCB fab capacity in China with a new factory, expected to come on line in the December quarter. A new flexible circuit plant in China is slated to begin volume production in the June quarter. In addition, Flextronics recently opened a Beijing design center that has added some 250 engineers to the company’s cell-phone design activity. The company has centered the development of GSM phones in Beijing….CTS’s Electronics Manufacturing Solutions business is setting up a microelectronics assembly capability, comprised of a Class 10,000 cleanroom environment and wire bonding, at its Moorpark, CA, headquarters.…Nortech Systems (Wayzata, MN) has entered into an agreement to purchase a 140,000-ft2 manufacturing facility in Blue Earth, MN. The new space will support the growth of Nortech’s Aerospace Systems division, which specializes in custom-designed wire harnesses and cable assemblies.

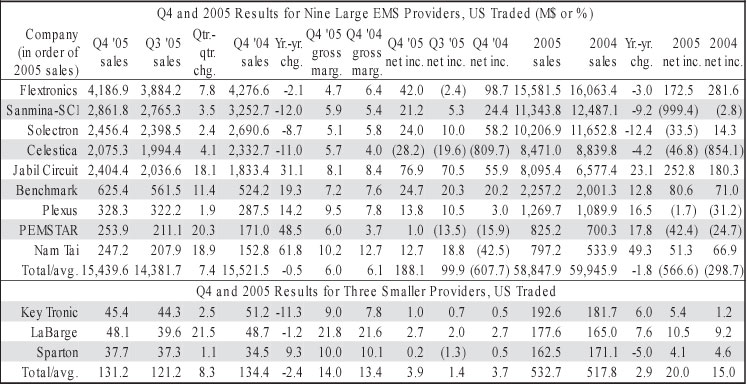

Some financial results…Elcoteq (Espoo, Finland) saw its 2005 sales rise 43% to 4.17 billion euros from 2.92 billion euros in 2004. Operating income in 2005 increased 34% to 76.5 million euros, while net profit went up 35% to 41.3 million euros.

People on the move…Solectron (Milpitas, CA) has appointed Paul Tufano as CFO. Like Solectron’s president and CEO Mike Cannon, Tufano is a former president and CEO of Maxtor, where he started out as the company’s CFO and later added COO duties.…Celestica has named James Rowan executive VP, worldwide operations. Rowan, who joined the company in January 2005 as president, Celestica Europe, is replacing Marvin MaGee, who is leaving the company to pursue other opportunities….Nam Tai Electronics (Tortola, British Virgin Islands) has appointed Patinda Lei as both CEO and CFO. She had been in charge of new product business for Nam Tai’s key component subassemblies area….Venture (Singapore) has made Tan Kian Seng its CFO, a position that had been open since September 2005….Suntron (Phoenix, AZ) has named Thomas Sabol, a company director, as CFO, replacing James Doran who had been interim CFO since October 2005. Sabol served as Plexus’ CFO from 1996 to 2002 and its COO from 2002 to 2003….Mack Technologies (Westford, MA) has appointed John Whetten as GM of its facility in Ciudad Juarez, Mexico, and Tom Dineen as GM of its facility in Melbourne, FL. Whetten most recently worked for Arrow Electronics, while Dineen was director of supply chain management for Mack Technologies, a subsidiary of the Mack Group (Arlington, VT)….EPIC Technologies (Rochester Hills, MI) has promoted Todd Baggett to VP of business development. He joined the company in February 2003 from Jabil Circuit....La Barge (St. Louis, MO) has hired Tim Matthews, formerly a consultant, as director of operations.

Restructuring in the UK…Sanmina-SCI intends to close a PC manufacturing facility in Greenock, Scotland. The Greenock business will largely be transferred to some of the company’s low-cost sites. IBM sold the operation to Sanmina-SCI in 2003.…Benchmark Electronics (Angleton, TX) plans to shutter its 55,000-ft2 facility in Leicester, England.