![]()

Cover Story

Market Data

Study Predicts Uptick in Assembly Market

News

IBM and HP Tap Sanmina-SCI for PC Outsourcing

Celestica To Gain NEC Factories in Japan

The severity of last year's downturn left many EMS providers with no choice but to take out capacity. In some cases, lots of it. This year, the onus will be on EMS providers to show that their restructuring efforts will pay off with improved performance - whether or not the electronics industry rebounds in the second half. That means achieving higher capacity utilization, better margins, more cash flow, and higher inventory turns.

In 2002, the EMS industry may or may not return to its historic growth rates of 20% or more. At this point, despite the continued growth of outsourcing, uncertainties still abound. Unable to count on robust growth, providers will need to focus on the basics of execution. Those that can improve performance will grow stronger; those that cannot will fall behind. With execution as a backdrop, here are seven trends that MMI sees as important for the upcoming year.

This year's mantra will be higher inventory turns and a shorter cash cycle.

Last year's inventory surpluses from the downturn had a brutal effect on inventory turns within the EMS industry. As inventory has been bled off, inventory metrics are improving. But more work needs to be done, and EMS providers will continue to push inventory reduction efforts such as vendor-managed inventory and updated IT systems.

Lowering inventory levels is a sure way to improve the cash cycle, sometimes called the sales cycle. Inventory is one of three components in the cash cycle, a measure that has been applied to the EMS industry since the second half of 1990s. (Cash cycle equals days of inventory plus days of receivables minus days of payables.) The cash cycle will become more prominent this year because Celestica, for one, has made the cash cycle a major goal for the company. Celestica recently told analysts that it is now working toward a cash cycle of 25 days. This goal is beyond industry norms, even before the downturn.

In effect, Celestica is issuing a challenge to other tier-one providers. If Celestica is willing to set such a goal, one may ask what are other providers are doing about the cash cycle. Moreover, the company is encouraging analysts to monitor its progress toward a 25-day cycle. With analysts paying more attention to this metric, they will be inclined to query other public providers more closely about their cash cycles.

The cash cycle gives providers a way to see how well they manage their working capital. The shorter the cash cycle, the shorter the time that working capital is tied up. Less working capital means less invested capital and a higher return on invested capital. Note that ROIC is a favorite benchmark used by both analysts and EMS companies.

The tier-one group will remain divided essentially three to two with respect to vertical integration. But smaller CMs can also adopt this strategy.

To varying degrees, Flextronics, Sanmina-SCI and Solectron have adopted vertical integration. Celestica and Jabil Circuit have not. MMI does not expect this split to change during 2002.

The downturn exposed perhaps the main disadvantage with vertical integration. Fixed assets in such areas as PCB fabrication and enclosures become underutilized, causing a drain on profits. For example, both Flextronics and Sanmina-SCI have been forced to downsize their board fabrication operations to compensate for a loss in board demand. But now that painful actions have been taken, the two companies are looking forward to participating in the PCB market when growth returns to it. A growth market brings out the financial advantage of vertical integration - the ability to generate and capture higher margins.

Now that the vertically integrated companies have gone through the pain of restructuring, they are not likely to abandon their vertically integrated operations. On the other hand, the two nonbelievers have seen the downside of the vertical strategy. Celestica has made it clear that it will continue to eschew vertical integration, and Jabil has offered no indication that it will switch over.

One might assume that vertical integration is the province of tier-one providers. And one would be wrong. Although PCB fabrication, a capital-intensive activity, does not favor smaller providers, enclosures and cables can be more easily integrated. Look for smaller providers such as Able Electronics, EFTC/K*TEC, SMTC and Western Electronics to push their vertically integrated operations this year as growth returns. In addition, some Asia-based providers including Alco Electronics and Elite Industrial Group can provide a vertically integrated solution (Nov. '01, p. 4-5).

As smaller providers increase the amount of system build in their facilities, the temptation grows to put in metal bending equipment or acquire sheet metal capability. More providers will be considering their options this year with respect to vertical integration. Although the tier-one group is clearly split, the line between pro-vertical and anti-vertical is still being drawn among other EMS providers.

Another option is to create a vertically integrated supply chain by alliance. CTS Corp. through its CTS Interconnect Systems unit is possibly the first to put together such an alliance (see News, p. 5). This type of alliance allows members to maintain their independence while offering a vertically integrated solution. Time will tell whether this approach can deliver all benefits of the vertical model.

Asset divestitures will be the medicine that the doctor ordered for large providers this year. Smaller providers will look for a growth prescription elsewhere.

Based on reports from tier-one providers, the pipeline of asset deals remains robust. The big question for large providers is how many deals will come to fruition this year and how large will they be. The answer will have a lot to do with how fast larger providers recover this year. Problem is, one usually has no visibility of these deals until they are announced. In fact, not all the deals that were proposed last year will make it through the pipeline. OEM cutbacks last year in some cases affected their divestiture plans.

Still, data that MMI has reported is encouraging (Oct. '01, p. 7). As of October 2001, Solectron had counted 49 divestiture-type opportunities, which exceed the total number of OEM divestitures in all of 2000. And a Merrill Lynch survey conducted over the summer of 2001 found some $19.5 billion in deals to be hatched in the first half of this year. That figure alone represents somewhere around 20% of the 2001 market. Certainly, the IBM and NEC deals with Sanmina-SCI and Celestica respectively bode well for the coming year. HP's plans are another good sign (News, p. 4-5).

Large providers will only take over facilities in high-cost areas when there is no other way to get the work done. And then they will build risk protection into their agreements.

Smaller providers, especially those below $500 million in sales, will not benefit from divestitures as large providers are expected to. But don't count the smaller players out. Both small and large providers will gain more business from system build work this year. And for some smaller players, the increase in box build work will likely be more dramatic. MMI believes that system build is the secret sauce for business growth this year, particularly in the US market where PCB assembly is heavily outsourced.

Don't expect the large players to acquire other players the way they did last year. But mergers and acquisitions among smaller providers may increase.

Flush with capacity, tier-one providers are not in mood to acquire other providers. Last year, Celestica, Sanmina and Solectron made major EMS acquisitions to enhance their footprint, capabilities or both. That is not likely to happen this year. Of course, acquisitions of smaller companies adding strategic capabilities in such areas as design and postmanufacturing services will likely continue.

But among tier-two and smaller companies, the motivation to combine or acquire has never been greater. Some of these providers want to offer their customers the same global solution that the big boys have. M&A deals offer a quick way to expand a company's footprint, as Plexus' 2002 acquisition of MCMS assets shows (News, p. 6).

Last year was hard on many EMS companies. That experience will make some private owners more inclined to sell this year. Some will want to cash out; others will see the advantage of combining into a larger player with more facilities, purchasing power and financial resources. In addition, the downturn has put more companies than usual in jeopardy, creating other buying opportunities.

With communications depressed and the computer market iffy, providers will look increasingly to other markets for growth.

Communications and computers along with peripherals probably make up at least 60% of the EMS market. The rest is mainly split among automotive, consumer, industrial and medical.

Unfortunately, providers cannot expect immediate gains from sales efforts in some of these remaining markets. Take automotive. The gestation period for automotive programs is measured in years, not months. And that assumes a provider has already been qualified, a time-consuming process in itself.

Before a provider can do medical work, there are FDA certifications to consider, based on the product. Medical programs may also require substantial engineering time from the provider before any manufacturing dollars can be realized.

Then there is industrial, an amorphous segment where customers can be difficult to pinpoint. Finally, the consumer segment favors those who can offer the lowest costs, a bind that many providers would prefer to avoid.

So the remaining segments do not necessarily offer a quick or easy fix for 2002 growth. In automotive, medical and consumer, the pickings may be slim since tier-one and -two providers are already plucking the juiciest programs. On the other hand, industrial will continue to be a fertile area for smaller players.

The Japanese market will be the X-factor in market performance this year.

While Japanese OEMs have accepted the concept of outsourcing, no one knows for sure how much Japanese work will flow from the pipeline this year. The good news is that NEC has already pumped out two asset deals recently (News, p. 5; Nov. '01, p. 1-2). If Japanese OEMs award some major programs in the first half, the effect on the EMS market will be palpable.

Of course, the potential among Japanese OEMs is huge. For instance, the top six Japanese OEMs accounted for internal PCB assembly valued at $73.3 billion in 2000, according to a new study from Electronic Trend Publications. ETP estimates the total assembly market in Japan will be $142.6 billion this year (see next article).

Back-end services will offer new growth opportunities.

EMS providers are only now plumbing the full extent of postmanufacturing services. Besides depot repair and refurbishment services, there are number of other areas that could be added to menus for after-sales services. These areas include call centers also known as CRM (customer relationship management), fast hubs, field service, logistics both forward and reverse, network installation, recycling and reselling.

By putting together a complete service offering, a provider can position itself to re-engineer and then take over the entire after-sales operation for an OEM. That is Solectron's pitch, at least, and more OEMs will be listening this year. If OEMs will contract out an entire manufacturing operation, they should be willing to outsource management of their after-sales chain or a big piece of it. Does this mean EMS providers will scramble in 2002 to add every conceivable capability in the back-end chain? Probably not. But more providers will be looking at where it makes sense to expand after-sales services. After all, Solectron pegs the available market for after-sales services at $177 billion.

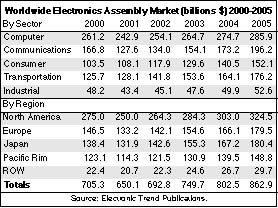

After a dismal 2001, a new report from Electronic Trend Publications (ETP of San Jose, CA) is forecasting modest growth for the worldwide electronics assembly market this year. The ETP report, entitled The Worldwide Electronics Assembly Market, Second Edition, puts the 2002 assembly market at $692.8 billion, up 6.6% from last year's $650.1 billion. Still, this year's market for assembly is expected to fall short of the year 2000's estimated total of $705.3 billion (first table). The worldwide assembly market consists of PCB and box assembly, both in-house and outsourced.

In 2000, some 31% of the worldwide assembly market was outsourced, according to the report. This percentage includes OEM-to-OEM outsourcing as well as traditional contract manufacturing. ETP expects the outsourcing penetration of the market to grow to 47% in 2005.

The computer sector maintains its position as the largest assembly segment throughout the report's forecast period from 2000 to 2005 (first table). Nevertheless, the ETP study estimates that the computer sector will lose market share over the period. A 37.0% share in 2000 will decline to 33.1% in 2005. Also predicted to lose share is the communications segment, which will start with 23.6% in 2000 and end with 22.7% in 2005. Due to last year's downturn in communications, this segment lost its number-two status to transportation in 2001, but will regain that position starting in 2003, according to the study.

The report finds that the consumer and transportation sectors were the only two assembly segments that did not decline in 2001 (first table). ETP expects both sectors to expand consistently over the forecast period and gain market share. According to study forecasts, transportation's share will increase from 17.8% in 2000 to 20.4% in 2005, while the consumer segment will see its share grow from 14.7% to 17.6% over the period.

In addition, the study breaks down the assembly market by region. While North America will remain the largest regional market from 2000 to 2005, ETP projects strong market growth from Europe, the Pacific Rim and, to a limited degree, the rest of the world (ROW). The report likens Japan to a sleeping giant with respect to outsourcing. ETP predicts Japan's assembly market value will increase from $131.9 billion in 2001 to $180.4 billion in 2005.

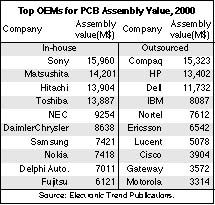

The study ranks OEMs by both in-house and outsourced PCB assembly value (second table). The top five OEMs based on in-house PCBA value are all Japanese.

See www.electronictrendpubs.com.

IBM and Hewlett-Packard intend to increase outsourcing of their PC manufacturing by divesting operations to newly merged Sanmina-SCI (San Jose, CA). The provider has won from IBM a desktop PC manufacturing contract worth about $5 billion over three years. In addition, HP plans to sell PC manufacturing activities in Isle d'Abeau, France, to Sanmina-SCI.

In the IBM deal, Sanmina-SCI will acquire IBM's NetVista PC manufacturing operation in Research Triangle Park (RTP), NC, and manage IBM's outsourced PC production in Scotland. IBM is outsourcing a "significant portion" of its desktop PC manufacturing to Sanmina-SCI, according to a statement from the two companies.

IBM currently manufactures NetVista PCs in RTP for customers in the US and Canada. Fullarton Computer Industries (FCI of Kilwinning, Scotland) manufactures the product line for IBM in Greenock, Scotland, to supply customers in Europe, the Middle East and Africa. FCI is part of UK-based Laird Group.

As part of this agreement, Sanmina-SCI will acquire IBM buildings totaling about 200,000 ft2 and equipment related to desktop manufacturing in RTP. In addition, the provider will take over management of IBM's existing contract with FCI and acquire IBM manufacturing equipment in Scotland. Assets to be acquired also include inventory.

Sanmina-SCI intends to use the existing locations in RTP and Scotland to fulfill IBM's desktop manufacturing needs. Under the agreement, IBM will transfer about 900 permanent and temporary employees in RTP and 80 people in Scotland to Sanmina-SCI.

Terms of the sale were not disclosed, but Sanmina-SCI's total cash outlay will be less than $200 million, according to the company's CFO, Rick Ackel. Subject to regulatory approvals in the US and Europe, the transaction is expected to close by the end of February. It is also expected to be accretive.

"The acquired operations will complement our existing EMS and enclosure operations in the Raleigh area," said Ackel during a conference call.

IBM said the deal will allow it to lower its costs further. The company will continue to design and market the NetVista line of desktops, which are part of IBM's e-business offerings.

The agreement does not involve any of IBM's other desktop manufacturing operations worldwide, but eventually will affect IBM's desktop manufacturing requirements for Mexico and Latin America, which are now handled out of IBM's plant in Guadalajara, Mexico.

Meanwhile, HP is in talks with the French workers council regarding its Isle d'Abeau site and intends to proceed with Sanmina-SCI as the potential buyer. Completion of the Isle d'Abeau transaction is subject to a number of conditions including these talks and the execution of definitive agreements. HP also expects to outsource at certain PC manufacturing sites in other locations.

Japan's NEC has decided to divest certain facilities in Miyagi and Yamanashi, Japan, to Celestica (Toronto, Canada) and enter into a five-year supply agreement worth about $2.5 billion in total revenue to Celestica. This deal will give Celestica a manufacturing presence in Japan. NEC had earlier announced its intention to outsource manufacturing activities at the two locations (Nov. '01, p. 1).

NEC's Miyagi and Yamanashi facilities develop and manufacture advanced optical transmission systems, including wavelength division multiplexing and SONET/SDH, as well as network access systems such as xDSL. As part of the deal, Celestica will assume supply chain management, subassembly, final assembly, integration and testing for a broad range of NEC's optical backbone and broadband access equipment.

About 1200 NEC employees will join Celestica - 800 from the Miyagi operation and 400 from the Yamanashi operation.

The deal will provide Celestica with "great factories that will be a tremendous base for us to expand in the fourth wave of outsourcing, which we refer to for Japan," said Eugene Polistuk, Celestica's chairman and CEO. He described the NEC factories as a good base to bring business through and maybe send it to other parts of Celestica. But Polistuk added that these factories are also good place to make products, especially the mid- to high-end kind, for Japanese customers. In addition, he expects these facilities to offer non-Japanese customers an opportunity to have manufacturing done in the Japanese market, where in some cases that makes sense.

Do perspective Japanese customers prefer Celestica to have facilities in Japan? "For the customers that we've talked to, they find that attractive. The only debate is how much you have," Polistuk told MMI. "I don't see an environment where we have ten factories in Japan. But obviously, we don't believe in the model that says we have no factories in Japan."

While the deal's purchase price was not disclosed, MMI asked whether or not a premium was involved. "I can say that it's not out of line with things we've done before," Polistuk replied. Yet Celestica also recognizes "the downward trend in prices," he added.

Not part of the deal are NEC Miyagi's design and development activities for optical transmission systems and NEC Yamanashi's Otsuki Plant, which is involved in manufacturing optical devices and optical submarine cable systems. The transaction is expected to close by March 31, subject to normal closing conditions.

"I expect there will be a lot more transactions in Japan. I expect some of the business will end up in low-cost geographies, and some will continue to be made in Japan," said Polistuk.

"I've talked to many Japanese OEMs. They're all thinking about outsourcing to various degrees, much the same way as it is in Europe," he reported.

Alliance expanded...Eagle Global Logistics (Houston, TX), a global transportation and supply chain management company, and Amphenol Interconnect Products Corp., an Amphenol subsidiary that manufactures connectors and cable and interconnect systems, have joined an alliance formed by CTS Interconnect Systems (Glasgow, Scotland). Other members of the CTS alliance are Pentair Enclosures, WUS Printed Circuits Co. and PPC Electronic AG. The alliance is offered as an alternative to vertical integration (July '01, p. 2; Sept. '01, p. 5). CTS Interconnect Systems is part of publicly held CTS Corp. (Elkhart, IN).

Flextronics (Singapore) has acquired an engineering design operation from DNA Enterprises, a wholly owned subsidiary of TeraForce Technology Corp. (Richardson, TX).

DNA's technical staff offers expertise in hardware, software, systems engineering and embedded digital signal processing for the embedded and high-speed communications marketplace. The deal will give Flextronics Design 25 engineers, who will join 42 Flextronics engineers in Richardson, TX.

TeraForce said the design services operation has become inconsistent with new product initiatives.

As part of the deal, initial cash proceeds and additional credit issued to TeraForce can be used by TeraForce to access Flextronics Design's engineering services.

Meanwhile, Flextronics has completed its 91% acquisition of The Orbiant Group from Sweden's Telia (Nov. '01, p. 7). This deal allows Flextronics to expand its Network Services business.

In another transaction, Flextronics paid $118 million plus the assumption of certain liabilities for Xerox's plants in Toronto, Canada; Aguascalientes, Mexico; and Penang, Malaysia. This is the first in a series of asset purchases from Xerox (Oct. '01, p. 1). About 2545 Xerox employees in these operations are joining Flextronics. The provider will assume manufacturing of Xerox office products and related components during a one-year transition. Flextronics will also begin manufacturing of some Xerox electronic parts and subsystems during the first half of 2002.

INNOVATIVE Electronic Solutions, a new private company, has acquired Blue Horizon EMS, an EMS provider with a 32,000-ft2 manufacturing facility in Alpharetta, GA, and sales and repair locations in Tampa, FL, and Houston, TX.

The Alpharetta facility, in its second year of operation, accounted for fiscal 2001 sales of over $2 million, and INNOVATIVE is estimating over $5 million for 2002. "We're very excited about our growth this year and for coming years," said Mark Wachtendonck, INNOVATIVE's GM. "We're very fortunate to steer clear of the significant downturns in the economy."

Already, the new company has expanded repair operations by opening a third repair site in Nashville, TN.

INNOVATIVE describes its niche as the ability to respond immediately for turnkey, consigned or repair requirements. The company is offering on a 24/7 basis both low- and high-volume capabilities as well as a specialty repair service. In addition to repair, offerings include full PCB assembly, final integration and test development. INNOVATIVE's three largest market sectors are wireless, medical and industrial controls.

"Our financial strength is a real asset we have to offer our customers. We have no long-term debt and strong open credit lines with our suppliers," said Wachtendonck. "Our backlog includes annual contracts for systems solutions and ongoing PCB support for the wireless industry. All of these are turnkey agreements. But we also provide consigned PCB assembly for current customers that have run over 25,000 boards per week."

Alpharetta-based INNOVATIVE employs close to 40 people.

Another deal done...Plexus (Neenah, WI) has completed its acquisition of MCMS assets (Dec. '01, p. 4). Plexus will continue to operate MCMS plants in Penang, Malaysia; Xiamen, China; and Nampa, ID. But Plexus will close the MCMS facility in Raleigh, NC, and combine the MCMS operation in San Jose, CA, into Plexus' San Jose operation.

ACT Manufacturing (Hudson, MA) has become the second top-50 provider to file for Chapter 11 of the US Bankruptcy Code in recent months. MCMS filed earlier (Sept. '01, p. 3).

ACT's filing came after the provider exhausted other efforts to fund its North American operations. The company had used up available liquidity of its domestic credit facility, and its domestic banks, led by The Chase Manhattan Bank, would only continue funding under the provisions of Chapter 11. ACT had been operating under a third waiver to its credit agreement. That waiver expired on Dec. 14, leaving the provider in default under the agreement.

Unlike MCMS that utilized Chapter 11 to sell assets, ACT has filed a petition for reorganization under Chapter 11. ACT says its overseas operations are unaffected by the filing. The company has received $9.5 million in debtor-in-possession financing, which is a short-term arrangement. ACT is also negotiating with its lenders to obtain longer-term financing for a substantially greater amount.

ACT reports it has suffered as a result of the weakness in the telecom and high-end computing sectors.

The company has taken a number of steps in an attempt to restore profitability. These include work-force reductions. In October, ACT cut over 1000 employees, reducing its work force to about 5000. The company started 2001 with about 8800 employees and let about 2800 go during the first nine months.

Also, ACT has closed a portion of its facilities in San Jose, CA, and Hermosillo, Mexico and has consolidated PCBA operations in Ireland into its England facility. That action leaves the Ireland facility as a dedicated cable operation. Other manufacturing plants are located in Georgia, Massachusetts, Mississippi, France and Thailand. While ACT has leased 100,000 ft2 for a facility in Dallas, TX, the company has changed plans for this facility. As of the latest 10Q filing, the provider had 12 manufacturing facilities with a total of about 1.6 million ft2.

For Q3, ACT's revenue dropped 39% from a year earlier to $225.9 million. Included in a net loss of $24.1 million were pretax restructuring charges of $35.3 million. Among those charges was $10.5 million in receivable write-offs from discontinued customer relationships and other disputes. Inventory provisions accounted for a charge of $9.9 million. Still, ACT generated positive cash flow for the quarter.

ACT had two customers over 10% of sales for Q3. EMC represented 22.2%, while Emerson accounted for 10.8%, up from 3.2% in Q2. Emerson has become a more significant customer following ACT's acquisition of an Emerson operation in the UK in July. For the first nine months, EMC and Efficient Networks contributed 21% and 12% of sales respectively. In 2000, Efficient, EMC and Nortel were all 10% customers. During Q3, ACT added six new accounts, worth about $70 million in projected revenue for 2002.

ACT expects revenue to decline in Q4 and is planning operations based on Q4 revenue at 70% to 75% of Q3 levels.

The company recently named Joseph Driscoll as CFO to replace Narendra Pathipati, who was laid off.

Robert Bradshaw has left Sanmina-SCI, where he was recently named president and GM of its EMS division, and joined Manufacturers' Services Ltd. (Concord, MA) as CEO and president. Kevin Melia, an MSL founder, has stepped down from the CEO position that he held from the company's inception in 1994, but will continue as chairman of the board.

MMI asked Bradshaw why MSL is making this management change now. He replied that the company's directors "are interested in moving MSL to a new level in customer performance and in the customer set that they're currently doing business with and would like to do business with. To do that, they felt they needed to add some strength to the management team, to develop some of the processes [for that], and to prepare MSL for the kind of growth and stature in the industry that they we're looking for.

"Kevin Melia had been here for many years as a founder and had done an excellent job as an entrepreneur starting the company. But clearly, the board and Kevin felt that the time was right to broaden the leadership team to move MSL to the next level."

Bradshaw has set his sights on MSL becoming a recognized leader in customer satisfaction. By attaining "unparalleled customer service, I believe we will enjoy the growth and opportunities in our industry that will position us to be recognized as a major EMS player," he said.

Another objective is to make MSL's footprint fully global. "MSL has been working towards providing that global footprint. To do that, we certainly have to look at other geographies like Mexico and Latin America and certainly Asia. So I clearly will be focusing on how we can expand that footprint...," said Bradshaw.

Acquiring MCMS assets would have given MSL a presence in Mexico and more sites in Asia (Sept, '01, p. 3). But MSL was outbid by Plexus (Dec. '01, p. 4).

For Bradshaw, taking the top job at MSL was the right move at this stage in his career. He said, "It was a point in my career where I thought I was ready and had prepared myself for the opportunity to lead a company." For the past two years, Bradshaw served as president and COO of SCI Systems before its merger with Sanmina. Prior to that job, he held senior executive positions with Solectron, which he joined after spending 20 years at IBM.

Bradshaw believes that MSL has an opportunity to broaden its customer set through his experience and customer relationships.

"One of the first things we're going to do strategically is to focus on our customer set, our market segments and our geographical footprint to determine where we think we want to be in the next six to twelve months," Bradshaw told MMI.

Bradshaw will also need to find a new COO to replace Bob Donahue, who intends to resign from MSL in March.

More people on the move...With the resignation of Robert Bradshaw from Sanmina-SCI, the company has appointed Hari Pillai, who comes from the Sanmina side, to replace him as president and GM of Sanmina-SCI Electronic Manufacturing Services. Other Sanmina executives tapped for key posts within Sanmina-SCI include Randy Furr, company president and COO; Steve Bruton, president and GM of Sanmina-SCI Printed Circuit Board Fabrication; Michael Clarke, president and GM of Sanmina-SCI Enclosure Systems; and Daniel Vick, president and GM of Sanmina-SCI Cable Systems. David Rees, who had been senior VP Europe for SCI, has been promoted to president of Sanmina-SCI Europe/Middle East. SCI executives given leadership roles within the EMS division include David Dutkowsky, executive VP of Latin America; George King, executive VP of North America; Santosh Rao, executive VP of Asia Pacific, and Mike Missios, executive VP of PC operations. In addition, Bhawnesh Mathur, who ran SCI's supply chain management group, has become executive VP of Sanmina-SCI's supply chain group. Dr. Sundar Kamath, from Sanmina, has assumed the role of senior VP of Global Technology Solutions....Michael McNamara, president of the Americas at Flextronics, has been given greater responsibility, which includes all assembly, enclosures, backplanes, logistics and photonics operations worldwide. McNamara and some other executives have been assigned key accounts, for which they will oversee selling and servicing of Flextronics' full offering. Also, Ronny Nilsson, president of Flextronics Western Europe, has been named president of Flextronics Network Services....EFTC (Phoenix) has named John Kulp, formerly VP of sales at FlexTek of Illinois, as VP of sales and marketing....David Osowski has resigned his position as VP and CFO at XeTel (Austin, TX). Reportedly, this was strictly a personal decision. Angelo DeCaro, president and CEO, will serve as acting CFO until the company can find a replacement. ...SMTC (Toronto, Canada) has appointed Frank Burke as CFO. He previously served as VP and treasurer of Magna International, an automotive supplier..

New programs...Juniper Networks (Sunnyvale, CA) has awarded a contract to Solectron (Milpitas, CA) for production of OC-192 PC assembly cards within high-end Internet backbone routers. Also, Surgient Networks (Austin, TX), has made Solectron the sole EMS provider for a platform that provides for the convergence of networking, storage and computing functions. Finally, Solectron is positioned to provide enclosure services to Brocade Communications (San Jose, CA) for its SilkWorm 3800 Enterprise Fabric Switch....Aperto Networks (Milpitas, CA), a developer of fixed broadband wireless access systems, will outsource to Jabil Circuit (St. Petersburg, FL) Aperto's manufacturing operations for all products, including base stations, subscriber units and radios. Jabil will manage the entire supply chain....Instron Corp. (Canton, MA) has named IEC Electronics (Newark, NY) as its key EMS provider. IEC will be providing PCBA and full systems build for over 24 products. Instron supplies instruments, systems, software and accessories for materials testing.

Facility projects...Plexus has completed the expansion of its 25,000-ft2 new product introduction facility in Fremont, CA. The company calls such facilities NPI Plus sites....Fullarton Computer Industries (FCI of Kilwinning, Scotland) is setting up a new plant in Tianjin, China, south of Beijing. Due to start production early this year, the 100,000-ft2 plant will have manufacturing capabilities for metal, plastics and cables in addition to final assembly. The new plant will complement FCI's existing capabilities in North America and Europe....According to the Asian source DigiTimes.com, Taiwan's Hon Hai Precision Industry Co., better known by its Foxconn name, plans to invest $23.8 million in its Beijing, China subsidiary for the purchase of mobile phone assembly equipment. The company will also invest $33.8 million in a new factory in Suzhou. Intended for making components and connectors, the Suzhou factory is likely to begin producing motherboards as well, reports DigiTimes.com.

EMS company news...As a result of the C-MAC acquisition, Solectron is adding a fourth business unit - Microsystems - which provides microelectronics modules, interconnect systems, sensors and control devices. After taking a restructuring charge of $73 million in the quarter ended November 2001, Solectron said in the next one or two quarters further actions may result in $250 to $350 million in restructuring and impairment charges. Through restructuring actions, Solectron had taken out about 25,000 people, about 490 lines, and 4 million ft2 as of its December conference call....Group Technologies Corp. (Tampa, FL), a subsidiary of Sypris Solutions, has changed its name to Sypris Electronics LLC.