![]()

Cover Story

Market Data

News

The last two years have taught the EMS industry some hard lessons. Perhaps the harshest one is this: Lack of end market demand can overwhelm the industry and leave it in a prolonged state of overcapacity. No longer can the EMS industry assume that outsourcing will result in growth year after year. That's a bitter pill to swallow for the industry and those who depend on it. However, one can argue that taking this medicine now will lead to better health in years to come. Here's why.

The telecom debacle and computer industry softness have forced many providers to look outside those sectors for growth. Such diversification is a good thing for the long-term health of the industry. Not only does it reduce the industry's dependence on these two sectors, but it also turns providers' attention to other segments with growth potential. By focusing business development on segments such as automotive, consumer, industrial, instrumentation, medical and military/aerospace, providers can tap less volatile markets that still have a lot of outsourcing potential.

As the industry knows all too well, overcapacity has led to massive restructuring, with much of it occurring in high-cost regions. The result is a shift of EMS capacity from high- to low-cost regions. In all likelihood, this shift was bound to happen. The downturn just accelerated what would have been a more drawn-out process of moving production to low-cost centers over a period of several years. By having more low-cost capacity particularly in Asia now rather than later, the EMS industry gains a stronger position to compete against both OEM and ODM manufacturing.

The downturn has also caused EMS companies to target their financial performance under an assumption of no growth. That's also a healthy strategy for the long haul. If providers can achieve profitability with essentially no growth, then they'll put up even better numbers when growth does return.

So the downturn has imposed changes that will ultimately make for a healthier industry. Now the question is: Will the industry get well by resuming 5% to 10% growth in 2003? With the March quarter typically prone to seasonal weakness and no strong indications yet for June, the answer remains elusive and perhaps three to six months away. But unlike the 1990s, end market demand - starting with business spending on IT - will have a lot to say about any recovery of the EMS industry in 2003.

Whether or not the EMS industry returns to respectable growth in 2003, this year will mark a turning point in a number of areas.

For the first nine months of 2002, the dozen large EMS providers tracked by MMI collectively lost $3.5 billion, an unprecedented number in the annals of EMS (Nov. '02, p. 7). Granted, this figure includes Solectron's $2.5-billion charge after taxes for goodwill and intangibles impairment. Excluding this one-time charge, the 12 companies still lost about $1 billion for the period. This adjusted number is still staggering, and MMI is betting that things can't get any worse.

What's more, there are reasons for projecting overall improvement in bottom line performance for 2003, at least for the larger providers. As mentioned earlier, EMS management teams have their attention riveted on bottom line results, whether or not the top line improves. Secondly, the industry has completed the bulk of its restructuring, which will pay greater dividends in 2003. The industry has the potential to reap financial benefits from an increasing ratio of low- to high-cost capacity.

EMS penetration of the PCB assembly world is much higher than its overall penetration of the available market for outsourcing (Dec. '02, p. 8). While there is still PCBA work to be won largely from Japanese and European OEMs, much greater potential lies in the outsourcing of finished products. For a good example, take IBM's new outsourcing deal with Sanmina-SCI (see also p. 4). This agreement consists of build-to-order, configure-to-order, custom configuration and order fulfillment. PCBA wasn't even a part of the deal.

MMI believes the rate at which OEMs outsource system-build work will have increasing influence on future growth rates. However, finished product outsourcing is not a worry-free strategy either for EMS providers or OEMs. On the EMS side, system-build work generally carries lower margins, putting more financial pressure on a provider, which must find a way to compensate in other areas. For OEMs, outsourcing an entire product line can be a company-altering event. In that product line at least, the OEM can no longer call itself a manufacturer and is at the mercy of its EMS supply base. That's big step for most OEMs and one requiring much soul-searching.

It's a mistake to treat design services as mere extensions of a core EMS offering. Design services are not just another way to add revenue from value-added activities outside manufacturing. An important game in design services is to win the product manufacturing program by designing the product first. This strategy plays into the aforementioned need to win system build work. In 2003, design services will emerge as an increasingly important means to gain product manufacturing business while avoiding head-to-head competition on the manufacturing side. Flextronics has a big effort underway to sell OEMs on the concept that it can reduce product cost substantially by taking over product design (Oct. '02, p. 1-2).

This effort puts the onus on competitors to respond, and they can do so in several ways. One approach is to act as a CDM, or contract design manufacturer. This term will gain visibility in 2003, because it allows an EMS provider to offer design services in the same way as manufacturing services are rendered, that is, on a contract basis. Another strategy calls for entering the ODM (original design manufacturer) market, which was created by Taiwanese computer manufacturers. An ODM designs a product on its own and then sells the product as a fully outsourced solution to an OEM. Yet another scenario takes place with joint design, in which both the OEM and its outsourcing partner design the product together.

An EMS company has the option to pursue any or all of these approaches to product design. Although the EMS and ODM markets are converging (Aug. '02, p. 1-2), MMI does not foresee widespread adoption of the ODM approach within the EMS industry in 2003. Granted, there are EMS companies such as Flextronics and PEMSTAR that are pursuing ODM projects on selected products. But the ODM model of developing expertise in a few product areas runs counter to the EMS generalist approach of working in many product areas. Plus, EMS providers are typically loath to commit their resources, whether design or manufacturing, without a purchase order.

The joint design option is an interesting one to ponder because it can apply to both EMS providers and ODMs. For example, an OEM could do the product spec and system architecture and then turn the rest of the design work over to an EMS provider. Or an ODM could develop a reference design that could be customized by a joint design team. These roles can also be reversed. Joint design will be one of the more subtle, but no less important trends to watch for in 2003.

In 2003, MMI expects that EMS providers will generally avoid acquiring OEM facilities in high-cost areas unless they find a compelling reason to do so. That reason could be some capability or market presence that a provider deems absolutely essential. Otherwise, providers have closed or consolidated too many facilities in high-cost areas to be adding more such facilities now.

Trouble is, the facilities that OEMs want to get rid of are often in high-cost areas. Unfortunately, preserving jobs at these facilities is becoming less realistic since EMS providers want the work transferred to their own underutilized facilities.

There just isn't enough EMS business in the US and Western Europe to go around. Two years of weak demand and program shifts to low-cost regions have seen to that. Moreover, local and regional providers in these high-cost markets can no longer assume they'll even get early production runs. Increasingly, OEMs are bypassing the US and Western Europe to launch products directly in the low-cost regions (Dec. '02, p. 1-2). These providers, it seems to MMI, have four choices. Find a niche that is insulated from outsourcing to low-cost centers, come up with a low-cost solution of their own, sell out, or face a troubling future.

Recently passed legislation in Europe has banned lead from nonexempt products starting in July 2006. Most OEMs will want to comply, and many will turn to their EMS providers for a lead-free process. A coalition of Japanese, US and European organizations has called for lead-free soldering by the end of 2005. That earlier deadline would leave less than three years to prepare, if a company hasn't already started. So in 2003, those who have held off on lead-free soldering will get serious about conversion.

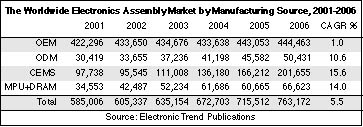

A new report from Electronic Trend Publications (San Jose, CA) presents a broader than usual picture of the original design manufacturing market, which ETP predicts will grow steadily from $30.4 billion in 2001 to $50.4 billion in 2006. These values equate to a CAGR (compound annual growth rate) of 10.6%. The ETP report, entitled The Worldwide Original Design Manufacturing Market, estimated the ODM market for 2002 at $33.7 billion, increasing to $37.2 billion this year (table).

This study views the ODM market as more than the usual Asia-based companies that design and manufacture computer or telecom products for OEM brands. Such companies are classified as one type of ODM. The report also identifies a second type of ODM - typically North American or European in origin and dedicated to a vertical industry niche such as found in the telecom, medical equipment, military/avionics, automotive, or industrial market. This second type of ODM provides subassembly products to a larger OEM or prime contractor. Still, in both categories the ODM owns the design and assumes some inventory risk.

Although the report foresees consistent growth for the ODM market from 2001 to 2006, the EMS market is expected to end up with a higher CAGR despite a down year in 2002. Over the forecast period, ETP projects a CAGR of 15.6% for the EMS market, compared with the aforementioned 10.6% for the ODM business.

According to the study, the majority of outsourced assemblies are expected to migrate to EMS partners as opposed to ODMs. There will be exceptions, however, such as notebook computers, printers, monitors and cell phones. The report states, "In these highly competitive product markets, its simply is preferable to outsource the entire design and assembly to a competent and competitive ODM supplier."

In addition to the EMS and ODM markets for outsourced work, the ETP report posits a third form of outsourcing - MPU and DRAM subassemblies. Normally, these subassemblies would be included as part of ODM revenue. But the study treats MPU and DRAM costs as a separate element within the worldwide electronics assembly market. As a result, ODM market estimates are lower than ETP's previous estimates that incorporated these MPU and DRAM numbers. According to ETP, MPU and DRAM components should be considered outsourced assemblies and, as such, represent the highest value-added element in computer products.

It's no surprise that the study foresees a declining OEM share of the assembly market over the forecast period. OEMs will represent 58% of the market in 2006, down from 72% in 2001. So by this analysis, 42% of electronics assembly value will be outsourced by 2006. All three outsourced segments will grow in market share, according to the report, but the ODM segment will have the smallest share gain from 2001 to 2006. The ODM share will increase from 5% to 7% over the period, while the EMS portion will expand from 17% to 26%. The final piece, MPU and DRAM subassemblies, will go from a 6% share to 9% (table).

At $18.9 billion in 2001, the computer segment of the ODM market should grow to $32.9 billion in 2006, according to the ETP report. The communications segment should expand from $6.2 billion to $10.1 billion over the forecast period, while the consumer side should increase from $2.2 billion to $3.1 billion. The study also predicts the military/avionics segment should represent $2.5 billion in 2006, up from $1.8 billion in 2001. The automotive, industrial and medical segments will also grow, but will remain under $1 billion.

Asia will remain by far the leading region for ODM work over the forecast period. The report forecasts a CAGR of 13.3% for Asia and estimates that its share will rise from 67% in 2001 to 75% in 2006. Europe's ODM share will also increase from 7% to 9% over the period, and ETP has assigned Europe the highest CAGR - 19.2%. North America will grow at an estimated CAGR of 4.3%, but its share will drop from 17% to 13% over the forecast period. The rest of world will see its ODM share shrink from 9% to 3%.

The Worldwide Original Design Manufacturing Market also covers 85 large ODMs. To learn more, contact saberry@electronictrendpubs.com.

Pursuing ODM capabilities...Flextronics isn't the only EMS provider engaged in the design of mobile phones. Elcoteq Network has joined Symbian's Platinum Partner Program, which will aid Elcoteq in designing mobile handsets based on the Symbian operating system.

IBM will outsource $3.6-billion worth of server and other work to Sanmina-SCI (San Jose, CA) and $120 million in asset recovery services to Solectron (Milpitas, CA). Both contracts last three years. Sanmina-SCI will acquire operations in Mexico and Scotland from IBM, while Solectron will add an IBM activity in North Carolina. The purchase price of the Sanmina-SCI transaction is less than $200 million, most of which is inventory.

Sanmina-SCI will take over manufacturing of a significant portion of IBM's low and midrange xSeries servers and IntelliStation workstations for customers in the Americas, Europe, the Middle East and Africa. The EMS company will provide build-to-order (BTO) and configure-to-order (CTO) services for these Intel-based products. In addition, Sanmina-SCI will handle order fulfillment for these products and IBM NetVista PCs going to customers in those regions and will perform custom configuration of some ThinkPad notebooks for those regions. Sanmina-SCI is already responsible for production of the NetVista PCs through a deal announced about a year ago (Jan. '02, p. 4-5). But IBM will continue to manufacture the majority of all ThinkPad notebooks in China.

Excluded from the deal are xSeries servers and IntelliStation workstations being built by Solectron in Brazil for customers in Brazil, Argentina, Paraguay and Uruguay. Also unaffected are any of IBM's Intel-based products for customers in Asia Pacific, and the majority of these products will continue to be produced at an IBM joint venture facility in Shenzhen, China.

Sanmina-SCI will acquire the IBM operations that support these products in Mexico and Scotland. In Guadalajara, Mexico, Sanmina-SCI will lease a factory of more than 400,000 ft2. In Greenock, Scotland, the EMS provider will take over an operation mainly for logistics in a space estimated at 500,000 to 600,000 ft2, but Sanmina-SCI did not say whether this acquisition would be done by facility lease or purchase. The agreement calls for the transfer of about 650 IBM employees in Greenock, 400 employees in Guadalajara and 10 employees in Raleigh, NC. All IBM employees whose work is being outsourced will be offered jobs with Sanmina-SCI.

The IBM operations will be integrated within Sanmina-SCI's volume computing division, which specializes in PCs. This division, formerly part of SCI, was a pioneer in the use of BTO and CTO for manufacturing PCs.

The server market represents a growth opportunity for Sanmina-SCI, and the company makes a big splash in that market through this deal. "It positions Sanmina-SCI in a leadership role for Intel-based server manufacturing, logistics and distribution. It diversifies our overall product mix specifically in this computing division and also strengthens our long-term relationship with IBM," said Jure Sola, Sanmina-SCI chairman and CEO, in a conference call with analysts. According to Sola, the transaction also expands Sanmina-SCI's global manufacturing capability in a key geographic region.

This contract does not include motherboard assembly, and Sanmina-SCI will buy motherboards from existing IBM suppliers. Sola said his company at present has no interest in building these motherboards. But he noted, "There's other vertical integration that I believe we can add...." Sola would not provide analysts with any details of how the company's vertical integration would apply to the project.

Subject to customary closing conditions, completion of the deal is expected in Q1 2003, according to Sanmina-SCI. An IBM statement lists an expected closing date of February 2003.

Sanmina-SCI expects the deal to be accretive to its fiscal 2003 earnings. The company projects a return on invested capital over 20% annualized.

Sola emphasized that the key to success in this contract will be to achieve high inventory turns. He said, "We expect inventory turns on this type of product to be over 25 times."

There is downside protection built into this contract, and Sola reported Sanmina-SCI is fully covered with regard to inventory.

Under a definitive agreement, Solectron will acquire IBM's Global Asset Recovery operations in Raleigh, NC, as IBM is outsourcing a significant portion of its asset recovery operations to Solectron. These operations restore end-of-lease PCs and other IT equipment for resale. As a result of this deal, Solectron will strengthen its asset-recovery capabilities and expand its long-time relationship with IBM. The transaction is expected to close in February.

Solectron will expand its postmanufacturing services by adding IBM's asset-recovery capabilities such as demanufacturing, remanufacturing, refurbishment, recycling and disposal. At the Raleigh refurbishing center, IBM processes PCs, laptops, monitors, servers, printers, point-of-sale equipment and storage products.

Under the agreement, Solectron will use the existing IBM center and acquire the related building, equipment and fixed assets. Solectron will offer jobs to about 250 IBM employees who support these operations.

The provider will integrate the IBM center into its Solectron Global Services operations. Solectron currently provides asset recovery services at four other locations.

Elcoteq Network (Espoo, Finland) is enlarging its presence in China by acquiring a controlling interest in two Chinese joint-venture EMS companies. The Finnish provider is buying IBM's 70% stake in Shenzhen GKI Electronics Company Limited and Beijing GKI Electronics Co, Ltd. Chinese authorities have approved the deal, scheduled to close on Dec. 31, 2002. The deal is described as Elcoteq's biggest so far.

The purchase price for the acquisitions and certain licensing comes to $37.3 million in cash. China Great Wall Computer Shenzhen Company Limited, an IT supplier in China, will remain as the joint venture partner in the two GKI companies. The deal is expected to have no impact on the joint ventures' operations, employees or customers.

These acquisitions will boost Elcoteq's business in China above 1.1 billion euros a year. Elcoteq estimates that the two companies will exceed 600 million euros in combined sales for 2003. Reportedly, the companies are profitable.

Elcoteq will strengthen its position in both Northern and Southern China by taking control of two plants, one in Beijing and one in Shenzhen. Together, the plants will add 15,000 m2 of space, which will increase to 28,800 m2 when the Beijing operation moves a new 20,000-m2 facility in early 2003. Counting the new facility, Elcoteq will double its floor space in mainland China from 25,000 m2. The two operations will also bring 1600 people, nearly doubling Elcoteq's work force in China to 3300. With the new plant, Elcoteq will end up with 30% of its floor space and 33% of its work force in China. The company said the acquisitions will enable it to handle more projects competitively from existing and new customers.

In addition, the deal will further Elcoteq's relationship with Nokia in China due to a substantial supply relationship that comes with the transaction. In 2000, IBM and Great Wall formed Beijing GKI Electronics to supply PCB assemblies for wireless products and systems made by Nokia ventures in China. Beijing GKI was set up to manufacture in Beijing's Xingwang industrial park, which Nokia has designated as a campus location for itself and its suppliers. The new 20,000-ft2 facility is also located in the Xingwang park.

Besides this Nokia relationship, the GKI companies also bring Elcoteq several Japanese and Western customers reportedly with technically demanding products.

What's more, Elcoteq and IBM have agreed to explore opportunities for cooperation in communications technology products and other applications. There is the potential to offer customers IBM's system design skills together with Elcoteq's manufacturing capabilities.

Elcoteq's president and CEO, Lasse Kurkilhathti, said the deal "takes us back to the growth path and balances our European and Asian businesses to nearly equal in size. We look forward to increased business with IBM in communications technology products and fruitful cooperation with the prestigious Great Wall Company as our joint-venture partner."

If the GKI operations were added to Elcoteq's results for the first nine months of 2002, Asia would have represented 46% of sales, instead of 27% as was reported, and Europe would have contributed 40%, rather than 55%.

Elcoteq entered China in 1999 and currently operates plants in Dongguan and Beijing. These facilities, which house a total of 1700 people in 25,000 m2 of space, produce mobile phone and mobile network products for several European and Asian customers.

For IBM, this deal is the latest in a series of moves in which IBM has divested itself of PCBA activities. Formed in 1995, Shenzhen GKI, like Beijing GKI, was set up to produce PCB assemblies. Most recently, IBM sold off its Endicott, NY campus, which included a PCBA operation (July '02, p. 3-4).

Meanwhile, Elcoteq will reopen its second plant in Tallinn, Estonia, at the beginning of 2003. The provider decided in the fall of 2001 to close this plant and move its production to the other Tallinn plant. Production of communications network equipment will be shifted to the second plant, which was originally designed for that purpose. The transfer involves 200 to 300 people.

Elcoteq said its main reason for reopening the second plant was to make room for manufacturing terminal, or mobile phone, products in the other Tallinn plant.

The provider currently employs 2000 people in Tallinn, up 200 from a low in 2002.

Elcoteq also finalized the sale of its industrial site in Wroclaw, Poland, to a privately owned French company after the sale was approved by Polish authorities (Aug. '02, p. 8).

More activity in China...WKK Technology Ltd. (Hong Kong) has opened its new WKK Technology Park at Changping in the Dongguan area of Southern China. The 25-acre campus includes a 125,000-ft2 plastics facility, which is a joint venture with Japan's Nissin Plastics, and two 500,000-ft2 buildings for EMS. Some operations are being moved from WKK's existing Shenzhen facility to the new park....Solectron is adding about 200,000 ft2 at its Suzhou, China site, which currently has about 600,000 ft2. Mostly for manufacturing activities, the new building is scheduled to be up and running by the end of Q3....PCI China, a wholly-owned subsidiary of PCI Limited (Singapore), has entered into a joint venture with Shanghai Gaozhi Science & Technology Development Co. Ltd. The joint venture, PCI-Gaozhi (Shanghai) Electronic Co. Ltd, will provide EMS in China for the consumer, telecom and medical instrument segments.

New programs...Tivo has chosen Solectron to provide full product life-cycle services for stand-alone and satellite set-top boxes. In addition, as sole EMS provider for IPWireless (San Bruno, CA), Solectron will supply services from NPI through fulfillment for a wireless desktop modem, PCMCIA broadband modem cards and network base stations. This work will take place in Dunfermline, Scotland. Another Solectron win comes from Trimble for GPS-related products. In yet another new program, Solectron is doing some work for Acer in the provider's Romania facility. Also, AT&T has expanded its CRM (customer relationship management) activity with Solectron. Finally, the provider has won programs from five major automotive companies for instrument clusters, window motion modules, ABS breaking modules, diesel particulate sensors and diesel engine turbo sensors....In the medical area, Jabil Circuit (St. Petersburg, FL) has announced a new relationship with Abbott Laboratories (Chicago, IL). Jabil has also added Symbol Technologies (Holtsville, NY), a supplier of mobile information systems, and Emerson as new customers....Ac-cording to Reuters, a Chinese-language paper reported that Hon Hai Precision Industry Co. of Taiwan will build about two million thin PCs for Dell this year....Japan's Sumitomo Metal Micro Devices has selected Elcoteq to manufacture LCD controller modules in Dongguan, China. SMMD, which has produced the LCD modules in Japan and the Philippines, is following end customers into China....China's TCL Mobile Communication Co. Ltd., billed as the number-three brand for mobile phones in China, has started ordering mobile-phone LCD modules from Nam Tai Electronics (Hong Kong). Nam Tai holds equity stakes in both TCL and its parent company....Sanmina-SCI's medical facility in San Jose, CA, has received FDA approval to manufacture an RF controller for the NovaSure System from Novacept (Palo Alto, CA). The system is designed to treat excessive menstrual bleeding....Auto Life Acquisition Corp. (Carlsbad, CA) has selected Corlund Electronics to manufacture all of Auto Life's requirements for its engine cleaning and transmission flushing machines. Corlund will also manufacture Auto Life's new products - a fuel injection cleaning system and a coolant flushing machine - when they are rolled out in early 2003. Production will take place at Corlund's Vista, CA facility....Metretek Contract Manufacturing (Melbourne, FL), a subsidiary of Metretek, Inc., has landed a multiyear contract to build electronic assemblies for a large domestic furniture manufacturer. The contract is expected to generate about $2.5 million in annual revenue. Metretek, Inc. is a wholly owned subsidiary of Metretek Technologies, which also designs data-collection products and data-management systems through subsidiaries....LaBarge (St. Louis, MO) will produce cables for space shuttle launches under a new $3.8-million contract from United Space Alliance, NASA's prime contractor for the space shuttle....EMS providers themselves outsource at times, although they don't go around broadcasting this activity. For instance, top-tier provider Sanmina-SCI has placed an order with CirTran Corp. (Salt Lake City, UT), a full-service contract manufacturer of PCB assemblies, cables and harnesses. CirTran said it will work with Sanmina-SCI on production for new markets requiring fast turnaround of low-volume runs.

New alliance...CirTran has also formed an offshore alliance with SVI Public Co., Ltd., an EMS company in Thailand. The two companies will work together to support mutual customers from product design through volume manufacturing. With this accord, SVI customers get a US-based manufacturing solution, important for design and prototype phases. Through SVI, CirTran customers will gain a low-cost solution as they ramp up volumes.

Deal done...Elscint Limited has completed the sale of its manufacturing, assembly, engineering and integration operations in Ma'alot, Northern Israel, to Sanmina-SCI (Dec. '02, p. 3).

ECA (Electronic Components, Assemblies & Materials Association) is planning to hold an EMS industry forum in San Jose, CA, on February 20. At this meeting, ECA hopes to address critical issues facing the industry and establish an action plan that could take place under the concept of an EMS industry organization.

Invitations to the forum will be going out to senior EMS management, and the meeting will be open to any EMS company.

"[There's] no doubt in mind that it will progress into a formal activity. It will be up to the group as to what that will be," said Robert Willis, president of ECA. According to Willis, ECA will be ready to organize EMS company attendees into whatever they choose as the best way to address industry issues.

In the spring of 2002, ECA sponsored a meeting that outlined a number of important issues facing the EMS industry. Among them are poor forecasting, a lack of information sharing among EMS providers and other parties in the supply chain, and confusion over the proper role of the EMS provider.

Based in Arlington, VA, ECA is a sector of the Electronic Industries Alliance.

Some financial news...For the quarter ended Nov. 29, 2002, Solectron reported a net loss of $70.9 million on sales of $3.137 billion. Sales were slightly above the prior quarter's $3.117 billion and slightly below the year-earlier quarter's $3.152 billion. Excluding restructuring and impairment charges and a gain from the repurchase of debt, the loss narrowed to $6.8 million, or 1 cent per diluted share. Expecting seasonal softness in the February quarter, Solectron has offered guidance of $2.8 to $3 billion for sales and a loss of 2 cents to break-even for EPS excluding unusual charges. Also, Solectron received about $48 million from Lucent to unwind a supply agreement for optical products (Oct. '02, p. 5)....For the quarter ended Nov. 30, 2002, Jabil Circuit recorded net income of $8.4 million on sales of $1.068 billion. Sales were up 8% sequentially and 21% year over year. Jabil's guidance for the February quarter calls for revenue to increase sequentially by 5% to 12% to $1.1 to $1.2 billion. The company estimates core EPS will be 15 to 17 cents in the February quarter. Core EPS, which exclude amortization of intangibles, acquisition-related charges, restructuring charges and other income, were 15 cents in the November 2002 quarter....Sanmina-SCI has increased its offering of senior secured notes to $750 million, up from an original figure of $450 million (Dec. '02, p. 6). With a coupon of 10.375% annually and a maturity date of January 15, 2010, the notes are being offered in a private placement as part of a refinancing transaction, which includes a new $275-million credit facility....Nam Tai Electronics will transfer its stock listing to the New York Stock Exchange from the Nasdaq market. Nam Tai's stock will begin trading on the NYSE under the symbol NTE on January 23. Also, the company has invested $10 million for a 25% stake in Alpha Star Investments Limited, the ultimate holding company of JCT Wireless Technology Company Limited (Hong Kong). After the transaction, Nam Tai will assume a major role in the production of wireless communication terminals and their modules for JCT, which is Nam Tai's first customer for these products....SMTC (Toronto, Canada) and its lending group have agreed to revise certain terms of its credit facility. The revised terms will establish amended financial and other covenants for the period up to June 30, 2004, based on the company's current business plan....IEC Electronics (Newark, CA) has completed a $7.3-million refinancing, which has enabled the company to repay all but $100,000 of debt owed to its prior lenders. For fiscal 2002 ended Sept. 30, 2002, IEC reported sales of $39.4 million and a net loss of $1.43 a share, of which $0.94 came from discontinued operations. Sales were down from $114.8 million in the prior year. But the company was profitable in its fiscal Q4 with an EPS of $0.24, of which $0.06 came from discontinued operations.

Company news...PEMSTAR (Rochester, MN) has been selected as a Medtronic Cardiac Surgery Speed to Market 2002 Partner of the Year. The provider credited its medical design group....Two providers recently became certified to ISO 9001:2000. They are Applied Technical Services Corp. (Bothell, WA) and CASE Assembly Solutions (Easton, MA)....SMTC Design, the design services unit of SMTC, and Formation (Moorestown, NJ), an embedded systems provider, have joined the Avnet Design Service Provider Program.

Solectron has ended its search for a new chief executive with the naming of Michael Cannon as president and CEO. He succeeds Koichi Nishimura, 64, who in September announced his intention to retire from CEO duties (Oct. '02, p. 8).

Cannon, 50, joins Solectron from Maxtor Corp., a hard disk drive supplier, where he spent six years as president and CEO. He was also elected to the Solectron board.

After 14 years with Solectron, Nishimura is also retiring as chairman, a position he originally intended to keep. "Ko's continued involvement would have been welcomed. However, Ko has always wanted to do what is best for the company. And he decided that it was best for him to retire from all three positions. He has always felt that having a former CEO as chairman is generally not a good governance practice," said William Hasler, elected as Solectron's new chairman. He made these remarks in a conference call with analysts.

Hasler, the company's lead independent director, also holds the position of co-CEO of Aphton Corp., a biotech firm.

At Maxtor, Cannon oversaw a significant increase in sales and also orchestrated the 2001 merger between Maxtor and Quantum's hard disk drive division. His career includes senior management positions at IBM and Control Data. At IBM, he led the turnaround of its hard-drive business, in part by establishing lower cost operations in Singapore, Thailand, China and Hungary.

Cannon brings to Solectron a career spent in high-tech manufacturing, engineering and operations. "I have, I believe, a lot of relevant experience as it relates to Solectron's needs in terms of global manufacturing, in terms of supply-chain logistics. Also, I have, I believe, quite a bit of experience that's relevant to Solectron in terms of interacting with large, global OEMs," said Cannon during the conference call. He added that he is already familiar with many of Solectron's customers at the senior management level.

In connection with this appointment, an additional change took place in Solectron's senior management. Saeed Zohouri, executive VP and COO, has left the company. Solectron said this change is part of the CEO transition process. Zohouri's responsibilities will be handled by Cannon.

Meanwhile, another senior executive is on his way out. Bill Mitchell, Solectron executive VP and president of its Global Services unit, is leaving the company to become president and CEO of distributor Arrow Electronics. George Moore, an executive VP of Solectron, is replacing Mitchell as head of the Global Services unit.

More people on the move...Jabil Circuit has appointed Michel Charriau as chief operating officer Europe. Most recently, Charriau was executive VP of Philips Consumer Electronics and CEO of Philips Contract Manufacturing Services (PCMS), both divisions of Royal Philips Electronics. Jabil is currently integrating six PCMS facilities purchased from Philips, with three more to be transferred to Jabil. ...Danzas AEI Intercontinental (Newark, NJ), a business unit of logistics provider Danzas Group, has promoted Henri Duhot to senior director of the Electronics Manufacturing Sector.