![]()

![]()

Cover Story

2005: The Outsourcing Engine Will Keep Turning

MMI’s annual outlook for the year ahead

World Markets

The Case for Making Set-Tops in Mexico

News

In most quarters, 2004 was thought to be a recovery year. It turned out to be more than that, as a group of 15 large providers grew at an overall rate of 24% for the first nine months of the year (Nov. ’04, p. 1). What’s more, based on the midpoints of Q4 guidance, nine US-traded providers, including five tier-one companies, are projected to grow by a collective 20% in 2004. Since end markets did not come close to this growth, the secular power of outsourcing was very much evident last year. Will outsourcing continue to push the EMS industry ahead in 2005? The answer is a qualified yes. That is, unless unforeseen softening in end markets eats into outsourcing gains.

If the Semiconductor Industry Association forecast for 2005 is any barometer, end market demand won’t aid EMS industry sales this year the way it did last year. The latest SIA forecast is calling for flat semiconductor sales in 2005. If end markets act roughly in parallel to the SIA forecast, then they won’t help EMS industry sales much in 2005. The result would be slower industry growth this year than in 2004. But obviously no one has a clear view of what will transpire this year. (For a new EMS industry forecast, see article on p. 4.)

Still, one thing you can be sure of: the industry is never stagnant. Change is the name of the EMS game so MMI will take its annual stab at fingering what new trends to look for in the coming year. The format of our outlook has changed as well. Our view for 2005 starts with a series of questions such as:

Will EMS and ODM companies start merging? So far, there is some evidence of this happening. The three tier-one providers with ODM capabilities have each made an ODM acquisition or two in order to kick start their ODM businesses. Flextronics acquired ODMs Microcell and GTRAN, which played key roles during the startup of Flextronics’ ODM business in cell phones. Foxconn (the trade name for Hon Hai Precision Industry) purchased Ambit Microsystems, a communications ODM which gave Foxconn an entree into that ODM segment. And Sanmina-SCI added Newisys, a server ODM that provided Sanmina-SCI with an ODM offering in enterprise servers.

But none of these acquisitions touched the PC computing segment, where the Taiwanese ODM business got started and where it continues to derive a major share of its revenues. The three tier-one providers have chosen ODM niches apart from the PC segment, rather than take on the Taiwanese ODMs where they are strongest. Only when EMS providers decide that they want a piece of the PC ODM space will they have a reason to acquire a major Taiwanese ODM in that space.

For now, the three tier-one companies are busy building the ODM businesses that they do have. None have given any indication, in public anyway, that they are ready to leap into the PC ODM segment.

As for the Taiwanese ODMs, their growth strategies largely center on expanding into new ODM products such as cell phones. Although acquiring an EMS company would enlarge an ODM’s manufacturing footprint, such a deal would also mean taking on lower-margin EMS business that would not appeal to ODMs used to more profitable business.

But the EMS and ODM industries are converging, with the emergence of hybrid providers on both sides. In addition to the aforementioned tier-one providers, there are tier-two and -three companies that run both EMS and ODM businesses. On the ODM side, Wistron is a prima facie example of a Taiwanese company with both EMS and ODM offerings.

This convergence will continue. In the near term, hybrid EMS companies will keep expanding their ODM design capabilities. If they can’t easily hire new skill sets, they will acquire them. At some point down the road, this convergence will likely bring a tier-one or -two EMS company together with a major ODM. But as of now, there are no signs of this occurring in 2005.

ODM versus contract design: which one will win? The answer in a word is both. The EMS industry for some time has been augmenting its design capabilities so that providers can engineer customer products from the concept stage. These full-spectrum design capabilities apply to both the ODM and contract design scenarios. In the former model, there is more risk because designs are done on spec. But the ODM sets margins and retains IP for like projects. In the latter, design projects come with firm orders so risk is reduced. But sometimes OEMs want design work thrown in at little or no cost with manufacturing programs. Both models are valid, and both will see increasing demand this year. Hybrid EMS providers will be in a position to pursue both kinds of design projects, while providers who have stayed away from the ODM business will be candidates for contract design work.

Will there be tier-one consolidation? Certainly, the past does provide a recent precedent with the merger of Sanmina and SCI. But none of the six tier-one players needs the global presence, scale or EMS capabilities that would come from acquiring another top-tier company. Still, a tier-one acquisition would offer customer diversification and an immediate boost in revenue. MMI believes that a deal of this kind would be opportunistic. That is, a company would have to decide that they were buying customers and revenue on the cheap. If one of the tier-one providers runs into financial trouble, the odds of such a deal go up.

Will there be continued consolidation in the lower ranks of the EMS industry? Yes, of course. Consolidation has been underway for years in the EMS industry. Local players want to be regional. Regional providers want to go national. National providers want intracontinental and then global reach. EMS acquisitions continue to offer a fast way to extend a company’s footprint and grow its revenue. They can also add capabilities in such areas as design or test that a company lacks.

An increase in EMS consolidation deals already occurred last year amid improving market conditions. The number of consolidation deals went up by about 50% in 2004. (The official count will appear next month.) As companies improve their financial performance, they become more inclined to make acquisitions. Barring unexpected market softness, MMI expects the deal-making momentum from last year to carry over into 2005.

Another factor may also come into play. The dollar’s decline makes acquisitions of US assets less expensive for Asian and European companies, especially those who are looking for a US presence.

Is the one-stop shop the new difference maker? Yes and no. No, because just about any provider worth its salt will describe itself as a full-service EMS provider offering solutions from design through order fulfillment. Although one can argue about the extent of some companies’ design capabilities, lots of providers have at least board layout and DFM services and can do box build and direct ship. In today’s parlance, one-stop shop has become so overused that it can no longer serve as a means to differentiate providers.

However, within this amorphous category there are capabilities that will be used more and more to set some providers apart from others:

• Launching a product simultaneously in two or more regions.

• Providing design and NPI services on three continents.

• Doing a complete product design including system architecture, software engineering and design verification.

• Providing reverse logistics and repair on three continents.

• Offering BTO and CTO services for both low- and high-volume products.

The bar has been raised for those who would offer a global end-to-end solution. A global benchmark would include front- and back-end services as well as manufacturing on the three major continents.

How far will vertical integration go? Flextronics and Foxconn are two of the leading proponents of this strategy. Foxconn got started as a manufacturer on the component level and worked its way up the vertical integration ladder. Flextronics began with EMS and now is supplying more and more components (Oct. 2004, p. 1-2). The two companies are in a class by themselves when it comes to the variety of components supplied in volume. And there is no one on the horizon in a position to match them. (The other vertically integrated tier-one provider, Sanmina-SCI, is focusing its vertical offering on higher-complexity products.)

Both Flextronics and Foxconn are looking to expand their components businesses. Flextronics wants to harness its plastics and sheet metal capabilities for new component offerings. The company said it would not rule out producing such things as cables, connectors and heat sinks – products that Foxconn already supplies. Foxconn, for its part, is looking to supply components for the automotive industry, according to an Internet source in Asia (Dec. 2004, p. 7).

Can the two companies keeping expanding the scope of their vertical integration? MMI is betting that they will continue to expand their component offerings, but in a selective manner. They need to be in component businesses that will not burden them with high capex requirements. If they can leverage existing capabilities, that’s all to the good. The success of these components businesses hinges on the ability to be a low-cost producer. The two companies won’t do anything that would drive up costs such as SG&A. Flextronics has shown that its board and enclosure SG&A costs undercut what an independent supplier could expect.

The pursuit of component business reflects a fact of life: EMS is a margin-limited business. If a company wants higher margins, it must find other sources of revenue.

Will the transition to lead-free products create problems? Unfortunately, a number of lead-free issues will turn into problems in 2005 as OEMs prepare for the July 2006 deadline set by Europe’s RoHS directive. Chief among these problems are:

• Logistics. Managing the transition from lead-containing to lead-free finished products will not be easy. Leaded and lead-free items must be kept apart throughout the supply chain. Mixing the two types of product at the component, subassembly or finished-product level will potentially cause a violation of the directive. Not only that, finished product inventories will require a careful planning to ensure that come July 1, 2006, lead-free products are in the pipeline ready for delivery, while the inventory of lead-containing products is used up.

• Design for the environment. In order to design lead-free products, you need a database of components qualified for lead-free processing. But not every supplier will have their components qualified when designs are firmed up this year. That means finding qualified replacements if they exist, loosening component specs enough to come up with a substitute, or changing the design to eliminate nonconforming components. Multiply this scenario across many products, and you have a problem of major proportions. The problem applies to both new products as well as existing products redesigned for lead-free compliance. The good news for the industry is: some of this work, particularly product redesigns, will be done by EMS providers. The bad news is: it may be too much of a good thing given the number of products involved.

• Component part numbers. Some component suppliers have decided that they will not issue new part numbers for their lead-free components, much to the chagrin of many EMS providers. As result, providers will be forced to keep track of these lead-free components by using date codes or other means. A problem with date codes is that different suppliers will have different cut-in dates for their lead-free parts. Providers may be able keep the date codes straight during manufacturing. But how do you identify these lead-free parts if they come back at some future date for a repair action?

• Reliability testing. Generic testing only goes so far. OEMs who need high reliability will want their products tested individually. Again, this requirement means more work for the EMS industry. Unfortunately, the industry won’t have much time to deal with any last-minute reliability issues that are discovered.

• A drain on resources. With regard to RoHS compliance, 2005 will be an increasingly busy year for the EMS industry. Many products will undergo lead-free conversion, NPI and preproduction this year. Some portion will start in production by the end of the year. Because so many products are on similar schedules, resources at EMS providers could become stretched in certain areas such as engineering. Providers will be handling many more product redesigns than they would normally see.

Inevitably, there will be OEMs who wake up to compliance so late that they must scramble to meet the deadline. Many of the latecomers will likely seek help from EMS providers experienced in lead-free conversion. Unfortunately, these OEMs will be calling upon providers when they are busy meeting the lead-free schedules of customers who did not wait to comply. It is not clear how this situation will play out. But it would not be out of the question to imagine an extremely busy provider referring latecomers to other providers.

Can anything slow down outsourcing to China? At this point, nothing short of a major supply chain disruption will put the brakes on outsourcing to China in 2005. Cost savings there continue to be compelling for many OEMs.

Nevertheless, the rapid growth of the Chinese economy has put strains on China’s infrastructure, while bad loans have weakened its banking system, which must continually digest large inflows of foreign currency. If China can fix these problems, there is little to prevent it from being the world’s chief destination for low-cost manufacturing, with one possible exception. Landed costs from China are based on relatively cheap oil. If oil prices continue to climb, at some point logistics costs start to impact landed costs.

How will the EMS industry grow? MMI would be surprised if there are a large number of major divestiture deals in the pipeline. The number of OEM divestitures, which peaked in 2000, has declined again in 2004, according to MMI’s preliminary estimate. (See next month’s edition for the official count.) Although a number of large OEMs still maintain substantial manufacturing operations particularly in box build and system integration, it is not apparent that many of these OEMs are ready to divest these operations. Japan probably contains the largest concentration of these OEMs, and the EMS industry has been waiting for several years for the Japanese market to open wide to outsourcing. There are still no signs of that happening. Europe is home to some major outsourcing candidates as well, but divestment is a slow process in heavily regulated Europe. What’s more, adding high-cost sites in Western Europe is not attractive for large EMS companies. Finally, there is the US, where the large EMS players again are not looking to buy OEM assets.

Although some plant divestitures are bound to take place in 2005, MMI believes that the preponderance of industry growth this year, outside of the Flextronics-Nortel deal, will come from organic and quasi-organic outsourcing. Quasi-organic outsourcing would occur when an OEM transfers manufacturing of an existing product to EMS facilities while selling some inventory and equipment to the provider. But the two types of growth often do not come with an announcement. So it becomes more difficult for the industry to demonstrate that it’s growing.

Higher growth markets such as medical, industrial controls and instrumentation are also more suited to organic outsourcing. In such cases, OEMs often do not have enough electronics manufacturing to warrant a divestiture deal.

What will guide EMS providers through 2005? MMI believes 2005 will be the year of ROIC (return on invested capital), at least for the publicly held sector of the EMS industry. Providers will continue to work on margin improvement and asset management, especially inventory, in order to increase this ratio. Because the industry is margin-limited, it is incumbent on management to show that EMS companies can earn a respectable ROIC.

As a result, ROIC will increasingly be applied as a test for pursuing new programs. Programs that exhibit low ROIC levels will find fewer takers. In the last year or so, a number of providers renegotiated and in some cases cut loose programs that were not providing adequate returns. This year will find ROIC-driven providers less willing to bargain for business if it means relaxing ROIC standards.

The beauty of using ROIC is that it allows for margin variations that occur with different types of products. For example, a lower margin product might still be acceptable if it requires less working capital.

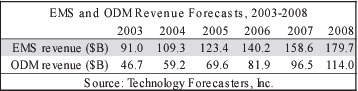

In the latest forecast from Technology Forecasters, Inc. (Alameda, CA), the EMS industry will continue to grow, but not as fast as the ODM sector. For the period 2003 to 2008, TFI is projecting a CAGR (compound annual growth rate) some five percentage points higher for the ODM side than for the EMS industry. Over that period, ODMs will enjoy a CAGR of 19.5%, compared with 14.6% projected for the EMS industry. This is the second forecast to give ODMs the edge when it comes to growth (Dec. 2004, p. 2-3).

TFI estimates that the EMS market reached $109.3 billion last year, which represented growth of 20.1%. This number is in line with the 20% sales growth that MMI calculated for nine US-traded providers based on their Q4 guidance (Nov. 2004, p. 1). For 2005, TFI expects growth to moderate, with revenue increasing by 12.9%. That rate will bring estimated EMS revenues to $123.4 billion this year. The firm foresees steady year-to-year growth for the EMS industry in subsequent years through 2008. Growth is projected to remain in the range of 13.1 to 13.6% from 2006 to 2008. In 2008, the EMS industry will attain $179.7 billion in sales, according to the TFI forecast (table).

While the EMS sector fared well in 2004, the ODM market did even better, according to TFI estimates. The firm puts ODM sales for 2004 at $59.2 billion, up 26.8% from a year earlier. For the period 2005 to 2008, TFI is forecasting year-to-year growth ranging from 17.6 to 18.1%. At the end of the forecast period in 2008, the ODM business will achieve projected sales of $114.0 billion. At that point, the ODM business will have a 38.8% share of total sales from outsourcing, based on the TFI forecast.

According to a Quarterly Forum report from TFI, “there is enough opportunity in handsets, consumer wireless local area network (WLAN) equipment, and other consumer products (such as MP3s) to sustain rapid growth in ODM over the next few years.” While the firm believes that ODM growth rates will remain very healthy, it sees current rates as unsustainable. As ODMs run out of new products suited for the ODM model, growth will slow, predicts TFI. Branding efforts by ODMs are also likely to have a moderating influence on the growth of ODM businesses, says TFI.

As for the EMS industry, the firm finds that the industry’s value proposition is still valid. The industry continues to offer lower cost structures and higher capacity utilization levels than OEM customers have. OEMs who see their core competencies as technology and innovation will gravitate to EMS outsourcing, says TFI. Those who view their core competencies as marketing and channel distribution will be attracted to ODM outsourcing.

The TFI forecast appears in a report entitled “Electronics Manufacturing Outsourcing Report: Five-Year Forecast of EMS and ODM Industries by Market Sectors and Geographies.” The report was presented at TFI’s Quarterly Forum held December 2004. For more information, email emiscoll@techforecasters.com.

It is widely believed in the industry that manufacturing of high-volume consumer-type products belongs in China. But Elcoteq’s acquisition of Thomson’s set-top box manufacturing in Juarez, Mexico (Dec. 2004, p. 4), shows that this rule does not always apply.

As a result of the acquisition, which went into effect this month, Elcoteq will continue the manufacturing of Thomson set-top boxes in Mexico. It must be assumed that Thomson could have outsourced this set-top work to other parts of the world. Why then did this set-top production stay in Mexico? The answer has much to do with managing the inventory associated with the high volume production of set-top boxes.

“Being in Mexico allows us to manage the inventory pipeline and the inventory velocity better than shipping from China. So typically products can be built or finally configured in an assembly to order model in Mexico,” said Bill Coker, director of sales and marketing at Elcoteq Americas (Irving, TX). This build/configure-to-order scheme contrasts with creating bulk inventory in China and then transporting it by ship or air. Based on landed costs, Coker maintained that Mexico is competitive with China, while proximity to the customer allows Elcoteq to be more flexible in meeting demand.

Elcoteq plans to expand the Juarez operation to accommodate new business and customers. The company intends to put more set-top box man-ufacturing and other home communications products in its Juarez site on the border. “Juarez is an ideal location for set-top box production when it’s compared with interior locations in Mexico like Monterrey or Guadalajara,” said Coker. Monterrey remains an Elcoteq center for mobile phone production.

This deal not only provides Elcoteq with diversification within the communications technology segment, but also establishes the company as a leading EMS producer in the set-top space. Coker estimates that at least 30% to 50% of the set top market is still internally produced by such companies as Scientific-Atlanta and Motorola. This internal portion “creates a huge available market for us to go service,” he said.

While Flextronics (Singapore) has been quite open about acquiring engineering capabilities in India, the company has said nothing about a US acquisition it recently made. MMI has learned that about three months ago Flextronics acquired RTRON, a Texas-based contract manufacturer specializing in cable and electromechanical assembly.

The former RTRON operation occupies a 150,000-ft2 facility in Stafford, TX, within metropolitan Houston. According to the website of a real estate services firm that had RTRON as a client, the company was a provider to the semiconductor industry. It may have served other segments as well. According to a 2001 statement from RTRON, the company was offering to support capital equipment, energy, medical and telecom operations. Regarding the latter, the RTRON operation offers a variety of optical cable assemblies.

This move could tie in with Flextronics’ strategy to expand into more component businesses (Oct. 2004, p. 1-2). As mentioned in this month’s outlook article on page 3, cables are among the components that Flextronics would not rule out adding to its vertical offering.

RTRON was established in 1998 by brothers Randy and Rodney Corporron and Cathy O’Leary. All three had been executives with K*Tec Electronics, an EMS provider that was merged into Suntron. The three left K*Tec to form RTRON.

Hon Hai acquiring ODD assets and people…Hon Hai Precision Industry (Tu-Cheng, Taiwan), which uses the trade name Foxconn, is picking up production equipment and about 200 R&D engineers associated with optical disk drives from Behavior Tech Computer (Taipei, Taiwan), according to DigiTimes.com. This transfer follows an earlier announcement that Foxconn would manufacture ODD-related products for BTC (Oct. 2004, p. 4).

NOTE AB (Norrtälje, Sweden) has signed an agreement to acquire Point Product Oy, a Finnish contract manufacturer with operations in both Finland and Estonia. The deal will give NOTE a presence in Finland and will significantly increase the provider’s capacity for low-cost production outside of Sweden.

Sales of the Point Product operations amounted to approximately SEK 90 million last year (about $13 million), or around 10 million euros, with an operating margin of about 9%. Customers come primarily from within the industrial and telecom segments.

Payment for the Finnish provider consists of a fixed amount plus a variable portion, the latter being based on future earnings. The purchase price is expected to reach around SEK 18 million (about $2.6 million) for goodwill and about SEK 10 million (about $1.4 million) for Point Product’s assets in the form of machinery and capital employed. The main part of the deal will be settled in cash, and the acquisition will take effect no later than January 2005.

According to NOTE, Point Product has based its operations on a model similar to that of NOTE. Point Product has about 40 employees in Finland and 130 in Estonia. All personnel are included in the deal. In Hyvinkää, Finland, just north of Helsinki, NOTE will take over a small Point Product operation, which handles prototypes and low volumes. NOTE will also gain a larger facility for low-cost production in the coastal city of Pärnu, Estonia. The operation in Estonia will be integrated with the NOTE group’s low-cost facilities. In Central Europe, NOTE owns a factory in Taurage, Lithuania, and utilizes a network of subcontractors in Poland. The deal also brings with it a 50% interest in a small mechanics production unit in Estonia.

Through this acquisition, NOTE also obtains a presence in Finland, the second largest EMS market in Scandinavia. The Finnish EMS market is about two-thirds the size of the Swedish market, according to NOTE. During the fall of 2004, NOTE stepped up efforts in Finnish market, and initial deliveries have begun to Finnish customers including ABB and the Nokia Research Center. NOTE says a local presence is a key prerequisite for capturing bigger contracts this year.

The acquisition is expected to contribute positively to the company’s earnings per share starting in Q2.

Originally formed in 1999 under the name EuroSupply, NOTE has acquired a number of Swedish electronics firms in recent years. For 2003, the company recorded sales of SEK 859 million (about $124 million) and profit before tax of SEK 63 million (about $9 million). Listed on the Stockholm Stock Exchange, NOTE employs about 950 people. Among the company’s customers are Volvo, Ericsson, Atlas Copco, Electrolux, Emerson Energy Systems and Parker Hannifin. (See next section for two new customers.)

In Sweden, NOTE operates five production facilities and five Gateways, while a sixth Gateway is located in the UK. The company has shifted its focus in Sweden from volume manufacturing to development, industrialization, and lower-volume, higher-complexity production. In addition to supplying low-cost production in Central Europe, NOTE offers global manufacturing though an alliance it spearheaded. According to the alliance’s website, NOTE’s partners in the alliance consist of Teikon Tecnologia Industrial (Brazil), Surface Mount Technology (Holdings) Ltd. (China), Rangsons Electronics (India), and SMC (US).

Some new programs…NOTE has also announced two new customers. Neonode Sweden AB has selected NOTE as a volume supplier for a multimedia mobile phone, the Neonode N1. The order is valued at around SEK 200 million (about $29 million), one of NOTE’s largest wins. The provider will distribute the phone directly from its factories to customers, whether orders come via the web or direct sales. Under another new program, NOTE will provide PCB modules for laser pattern generators supplied by Sweden’s Micronic Laser Systems AB for the production of photomasks. The contract includes aftermarket services….Solectron (Milpitas, CA) has won a new contract from Nortel in the enterprise data market….According to Indian news sources, TVS Electronics (Chennai, India), which runs IT and EMS businesses, will provide repair services in India for fixed wireless terminals made by China’s Huawei. Included in this agreement are call center support, parts management and field support….TXP-Texas Prototypes (Richardson, TX), a provider of prototyping EMS, has entered into a business agreement with the Republic of Korea’s Gwangju Metropolitan City, Photonics 2010 Initiative. The Korean government has granted Gwangju City a total of $750 million for development programs from 2000 to 2008 in order to build a photonics infrastructure….Three-Five Systems (Tempe, AZ) has received a US General Services Administration contract for flat panel display systems.…According to a report posted on the web, Ultra Electronics has chosen TTems (Blyth and Rogerstone, UK) to share manufacturing of sonobuoys in support of the UK’s Ministry of Defence. The contract is valued at £6 million over ten years….Silicon Graphics (Mountain View, CA) has awarded Pinnacle Data Systems (Columbus, OH) a multi-year program to serve as the primary source of board repair services for the majority of the OEM’s product line.

A fire this month consumed the manufacturing area of Mid-South Electronics’ Plant 1 in Annville, KY. At about 200,000 ft2, Plant 1 was the main facility at the Annville site, which employs about 700 people. The plant engaged in PCB assembly and plastic injection molding, as required for refrigerator components, and served several customers including Frigidaire. Mid-South considers the plant a total loss.

Plant 2, a much smaller facility in the 240,000-ft2 complex, was basically untouched. It did not contain much production.

Mid-South Electronics also operates a sister location in Gadsden, AL, which totals 246,000 ft2.

The provider has taken a team approach in dealing with the loss of the plant. One of the plans being evaluated is to see how much production can be shifted elsewhere. But nothing has been finalized.

The loss of Plant 1 is a major blow to the Annville area, where Mid-South Electronics is the largest manufacturer.

Mid-South Electronics, is a subsidiary of privately held Mid-South Industries (Gadsden, AL), an MMI Top 50 EMS provider in 2003.

The company’s website describes the Kentucky operation as a major world source for ice and water dispensing systems for residential refrigerators. Annville serves as MSI’s primary location for service to the telecom, major appliance, and business equipment markets, according to the website.

New facilities… Jabil Circuit (St. Petersburg, FL) is starting work on two new plants: one in India and another in China. In India, the company has broken ground on a second plant, a 175,000-ft2 facility in Ranjangaon, near Pune, in the state of Maharashtra. Slated to be fully operational by mid-2005, the plant will offer the full complement of Jabil services. Expandable to 400,000 ft2, the site is expected to serve the consumer, instrumentation, networking, peripherals and telecom industries. In China, Jabil has selected Wuxi, an Economic Processing Zone in Jiangsu Province, as the site for a new 515,000-ft2 facility. The plant, Jabil’s fourth in China, is scheduled to be fully operational in the fall of 2005. Again, the new facility will offer the complete range of Jabil services. The Wuxi site will be expandable to 900,000 ft2….Celestica (Toronto, Canada) plans to invest about $100 million over five years in a production site in Bors, Romania, according to Banca Comerciala RoBank, a Romanian banking firm. The firm reported that the initial investment will be $25 million followed by annual sums of $15 million. Reportedly, the entire project will consist of four production units. Celestica confirmed that there is investment in Romania. The provider already operates two Central European sites in the Czech Republic….To accommodate increased demand for systems integration services, Benchmark Electronics (Angleton, TX) will add a third manufacturing site in Thailand. The company plans to start this site in a leased facility offering 60,000 ft2 of systems integration space in the city of Ayudhaya, 30 miles north of Bangkok Airport. This new facility will sit in the same industrial park as the company’s current Ayudhaya site. Benchmark expects the facility will be fully operational by the end of Q1 2005….Simclar, Inc. (Hialeah, FL), an EMS company in the Simclar Group (Dumfermline, Scotland), has opened a fabrication facility in Matamoros, Mexico. The facility can process hard- and soft-tooled sheet metal, coat with powder and wet paint, produce injection-molded plastics, and provide overmolding for complex cable and harness manufacturing. Simclar has located the facility directly adjacent to its existing PCB and wire harness plant. The company says the new facility will give it more capacity and capability for higher-level assembly....LCD panel manufacturer J.I.C. Technology, a subsidiary of EMS provider Nam Tai Electronics (Hong Kong), has relocated to a new factory complex in the countryside of Baoan County, Shenzhen, China. Manufacturing space has increased from 152,000 ft2 to 416,000 ft2. J.I.C. also upgraded it production capability and capacity.

Partner sought for Russian facility…A Russian EMS facility is seeking a partnership opportunity. The operation could act as a turnkey supplier or take on a partner who would acquire a share in the EMS company. This company is represented by consulting firm MHM (Ayr, Scotland). Email mike@mhm.info.

Jabil Circuit and Solectron observe the same fiscal year, yet the two tier-one providers offer differing outlooks for fiscal 2005 ending in August. Jabil is maintaining its guidance calling for double-digit growth in the fiscal year. In contrast, Solectron’s has reduced its revenue outlook for fiscal 2005 and is now projecting flat sales for the year.

At the beginning of fiscal 2005, Solectron had expected revenue growth of 12 to 16%. “With a weaker than expected first half, we now see that growth pushed out to the second half of the fiscal year, which means that the full year revenue for fiscal 2005 is expected to be flat with 2004,” said Mike Cannon, Solectron’s president and CEO, during the company’s December 2004 conference call regarding Q1 fiscal 2005 results.

Fiscal Q1 revenue came in at $2.69 billion, which was about $200 million less than the low end of Solectron’s guidance. The company cited a delay in a new product ramp for a set-top box program, a longer than expected transition to a next-generation 3G handset model, lower demand for semiconductor capital equipment, and softer than expected networking revenue.

Still, Solectron raised gross margin for the third quarter in a row to 5.8%. GAAP earnings from continuing operations of 5 cents a share hit the midpoint of company guidance (for non-GAAP EPS).

For fiscal 2005, the company has also adjusted its guidance for non-GAAP EPS. The new range is from 23 to 27 cents, compared with the earlier expectation of 25 to 30 cents. But the Solectron is still confident that it will achieve ROIC for the year of 14 to 17%.

Jabil is not changing its earlier guidance for fiscal 2005. The provider is still expecting revenue to range from $7.2 to $7.4 billion, which equates to growth of 15 to 18%. Guidance also calls for core earnings growth of 18 to 22% and core EPS in a range of $1.20 to $1.24. While Q2 sales guidance reflects the seasonal decline in demand for consumer products, Jabil foresees significant growth in the second half of the fiscal year.

More financial news…Sanmina-SCI (San Jose, CA) has completed its 2004 fiscal year audit, which included previously announced reviews of accounting at one of its plants. These reviews caused a delay in the filing of the company’s SEC Form 10-K (Dec. 2004, p. 6). Based on adjustments following completion of the audit, the company added a 1 cent loss to its previously reported GAAP loss of 1 cent per share for fiscal 2004. The adjustments involved, among other things, stock-based compensation, interest expense related to an acquisition of minority interests in a subsidiary, and an increase in restructuring charges. Meanwhile, in form 10-K filed Dec. 29, 2004, Sanmina-SCI reported a material weakness in its internal controls in connection with the audit and in light of new guidance for assessing the effectiveness of internal controls. This weakness related to inadequate preparation and insufficient review of certain account reconciliations primarily relating to intercompany account balances between consolidated entities and trade payable balances; absence of documented support for, and review of, certain manual accounting entries and consolidation adjustments; and lack of qualified personnel in certain key accounting roles. The company instituted a number of corrective actions and believes these efforts have addressed the material weakness....According to Bloomberg News and Dow Jones, Foxconn International Holdings, the handset operations of Hon Hai Precision Industry (Foxconn) of Taiwan, aims to raise up to HK$3.37 billion (about $432 million) from an initial public offering in Hong Kong....Flextronics will take cash and non-cash compensation charges totaling about $7.6 million in connection with the departure of former CFO Robert Dykes.