![]()

![]()

It would be great to return to the salad days of the 1990s when annual growth rates of a youthful EMS industry routinely topped 20%. But the EMS industry is no longer young, and the chances for such industry growth have diminished as the industry has aged. To wit, market researchers, on average, foresee declining year-over-year growth rates that will fall to single digits by 2009 (Dec. 2006, p. 1-2). Industry backers may balk at such predictions, and they could well be wrong. Growth can fluctuate year to year. But MMI believes 2007 will be the year that the EMS business will likely face up to its status as a maturing industry.

Still not convinced that the EMS industry is maturing? Let us count the ways.

• Top 50 growth rates from 2002 to 2005 (2006 isn’t in yet) have averaged 11.0% (see chart). This number, which represents real data not estimates, does not signify an industry still in its high-growth phase. Since the Top 50 generated over 80% of industry revenue in 2005, the Top 50 can be used as a proxy for the entire industry.

• Geographic expansion of the large global EMS players is mostly over. There are still some areas such as Vietnam that may attract EMS companies, but the largest players are now pretty much where they want to be.

• The EMS industry has evolved such that a small group of companies account for the bulk of industry revenue. The six largest EMS providers combined for $82 billion in 2005 sales out of an EMS market estimated at $132 billion on average (Dec. 2006, p. 1). Hence, sales of the top six amounted to about 62% of total industry revenue in 2005. Similarly, top-ten sales equated to some 70% of the total. This is another characteristic of a maturing industry.

• EMS providers are margin-limited within their core manufacturing business. Yes, margins can be higher in design and postmanufacturing services, but the lion’s share of provider revenue will continue to come from manufacturing, where customers limit provider returns. Savvy customers know approximately how much profit their providers are making on customer programs. And the EMS industry has matured to the point where there are now many savvy customers.

In 2007, the EMS industry will see the term maturing or the arguably unfair label mature applied to it increasingly by outsiders. Is an industry label just a matter of semantics or a matter of concern? MMI thinks the industry should approach labeling as a serious issue because it has everything to do with how the industry is perceived. For those outside the industry, it makes a difference if the industry is entering its mature phase as opposed to continuing in its growth phase. Investors obviously treat a growth industry differently from a mature industry. Prospective employees, especially young professionals, often look for a company associated with a fast-growing industry. Mature industries may not be as appealing to young engineers and the like. Suppliers may not treat a company in a maturing industry the same way they would treat a customer in a growth industry.

But there is a silver lining. In general, mature industries also become more stable and hence predictable. Investors like predictability.

In keeping with this attribute of stability, 2007 might end up looking not much different from 2006 for the EMS industry. Obviously, it’s too early to be sure. But some initial indicators appear to be holding steady for 2007. Regarding end market demand, market research firm iSuppli is projecting that the electronic equipment market will grow by 6.7% in 2007, almost the same as the firm’s estimated increase of 6.6% in 2006. Forecasts for the semiconductor industry also call for nearly equal growth in 2007 and 2006. The Semiconductor Industry Association is predicting a 10% increase for semiconductor sales in 2007, following a 9.4% rise in 2006. These numbers are in line with iSuppli’s semiconductor forecasts of 10.6% and 9% growth in 2007 and 2006 respectively.

If we assume that 2007 end market and semiconductor growth will be roughly consistent with 2006, unknowns still remain for projecting EMS market growth in 2007. End market growth will be offset to some extent by product cost reductions mandated by customers. What effect will outsourcing have on EMS industry growth? This is a complicated question that must take into account business won in 2006 as well as in the first half or so of 2007. Individually, EMS providers can now provide the 2006 part of the answer, although of course they won’t.

Still, some light can be shed on the outsourcing mystery. During 2006, MMI did not hear any CEOs of public EMS companies talking about changes in the pipeline of outsourcing opportunities. That would seem to indicate no big swings up or down in 2007 business won in 2006. What’s more, if the EMS business begins to mirror the textbook performance of a maturing industry, then there should be less fluctuation in EMS market growth year to year than in the past.

But what happened in 2006? Forecasts of 2006 EMS revenue from four market research firms averaged $149 billion, which represented a 13.5% increase over the 2005 mean (Dec. 2006, p. 1). Actual growth in 2006 could go higher. MMI now estimates that the nine largest US-traded providers increased aggregate sales by 11.7% last year. When consolidated results of Hon Hai Precision Industry, by far the world’s largest EMS provider, are added in, the Top 50 growth rate will likely end up above 15%. That’s because Hon Hai’s consolidated sales for the first half increased 47% year over year (in NT$), and non-consolidated sales for the first nine months were up 34% (in NT$). With this 15+% outlook for the 2006 Top 50, can 2007 produce a Top 50 growth near this level?

Unfortunately, there are two answers this question. On the affirmative side, consistent market indicators and a maturing industry model would say that Top 50 growth in 2007 would come close to the 2006 outlook of 15+%. Such an outcome would mark the third straight year of Top 50 growth of about 15% or better. But growth at that level would go against the four-year historical average of 11.0% for the Top 50. It would also exceed a combined EMS market forecast of 11.8% growth from the four market research firms (Dec. 2006, p. 1).

While MMI cannot give an accurate reading of the tea leaves for 2007 growth, trend spotting is still within its power. Here are ten themes that will shape events in the coming year.

2007 will go down as a pivotal year in the history of the EMS industry. Wall Street’s patience has been stretched thin while waiting for EMS company turnarounds. Three large providers – Celestica, Sanmina-SCI and Solectron have been working on improving top- and bottom-line results for some time. If their efforts prove successful in 2007, this outcome would give the industry a major boost in credibility with Wall Street. Two successes out of three would still be a plus.

If the score is zero out of three or one out of three, then the EMS industry will be saddled with an unfortunate perception. Outsiders will then begin to see it as an industry so competitive that it fails to properly sustain important industry players.

There are structural reasons why inventory will continue to burden the EMS industry. Inventory for eight of the nine largest US-traded providers increased 33.4% during the first nine months of 2006. (As of this writing, Jabil has not reported full financial results for the fiscal year ended Aug. 31). Providers may be able to work off some of this inventory. But there are structural reasons whey inventory levels will remain to some extent elevated. One: increasing levels of box build and system integration work entail extended supply chains, which put more inventory in the pipeline. Two: more and more OEMs want to run as lean as possible. So any inventory buffers or hubs end up at their EMS providers. This is a fact of life that EMS providers cannot escape without jeopardizing customer relationships. Three: new business in nontraditional sectors – ie., medical, industrial, instrumentation and military/defense – is often low volume, high mix, for which inventory turns are much lower than in high-volume products.

India will stay in the spotlight in 2007, but will remain years behind other Asian centers in terms of manufacturing volume. Look for Vietnam to be taken more seriously as a potential low-cost center in Asia.

New facilities opening in India will give the country plenty of visibility in 2007. Large scale projects by Flextronics and the Hon Hai group are good examples. Solectron will become another player to watch in India. The provider’s joint venture Solectron Centum is spinning off its EMS division into a new EMS company managed by Solectron (Dec. 2006, p. 4). This new company will likely become a candidate for expansion in India, based on a shared 51,000 ft2 in India as listed in Solectron’s annual report. Sanmina-SCI, which has a development center in Chennai, remains the only top-six provider that has does not have a manufacturing facility up and running or announced. Odds are that Sanmina-SCI will do something about it this year.

The Chennai area has attracted handset heavyweights Nokia and Motorola along with Flextronics and the Hon Hai group. As a result, Chennai will quickly emerge as a manufacturing center for handsets and potentially other products in India. A combination of major OEMs and EMS providers in Chennai (Jabil also has manufacturing space there) will attract a supply base as Guadalajara, Mexico, did in the 1990s. Cisco’s decision to open a pilot facility in Chennai provides further evidence of this trend (see News, p. 6). Because of the scale of the new industrial parks in the Chennai area, it appears to be India’s best hope for the development of a robust supply base, currently a major drawback for manufacturing in India.

Meanwhile, new buzz about Vietnam will follow reports of Hon Hai studying the country for a possible investment of some $1 billion. Vietnam’s stock has already gone up with Intel’s decision to invest $1 billion in the country, which just joined the World Trade Organization (see News, p. 6).

New evidence indicates that full-scale convergence of the EMS and ODM sectors is not so inevitable after all. In recent years, the convergence of the EMS and ODM industries has been portrayed as a fait accompli. Even MMI had jumped on the bandwagon. The 2006 outlook predicted that the two sectors would continue to intermingle gradually (Jan. 2006, p. 3). But two recent cases show that an EMS provider can run into difficulty with the ODM model.

Item number one: Late last year, Sanmina-SCI announced that it will “realign” its ODM business to focus on joint development manufacturing services (Nov., p. 6). To MMI, this means that the company is shifting its engineering efforts from ODM projects to less risky JDM work, where revenue is typically guaranteed. Sanmina-SCI tried to develop a channel business for ODM products and found that competition was fierce.

Item number two: Jabil took a charge of about $12 million in the November quarter for discontinuing an unspecified consumer product that it had developed (Dec. 2006, p. 3). The company did not use the term ODM to describe this product. But some portion of this charge is associated with excess inventory, which is consistent with the launch of an ODM product. After price points declined dramatically, the company decided to exit this business. Price points can make or break ODM products.

MMI believes that experiences such as these will create or harden resistance to the ODM business among certain EMS providers. But others such as Elcoteq, Flextronics, Hon Hai and Venture will continue to embrace the ODM model.

As RoHS requirements spread beyond Europe, lead-free capability will join quality as a given for EMS providers in more parts of the world. The first phase of China RoHS will go into effect Mar. 1, 2007 with the requirement to mark electronic information products and identify any of six hazardous substances contained therein (Mar. 2006, p. 5-6). At some point, Chinese authorities will issue a catalog that will include product categories being regulated, the category of hazardous substances to be restricted, and the timeline for restriction, according to a translation of the China RoHS law.

California’s version of RoHS took effect Jan. 1, 2007. The California law bans the sale of certain video display devices containing any of four heavy metals including lead. When it comes to environmental issues, California often serves as a bellwether for other states. Indeed, eight states have looked at RoHS-like legislation, according to AeA (formerly the American Electronics Association). In an online report on the new US Congress, AeA concluded that “Democrats are likely to consider a federal RoHS bill….”

Unfortunately, this proliferation of RoHS requirements also creates compliance challenges. Take China. Based on a product classification list issued by Chinese officials as a guide, China RoHS contains some items that are either outside the scope of the EU’s RoHS or exempt from it. So it’s possible that a product which escapes RoHS regulation in Europe might still fall under China RoHS. Furthermore, unlike RoHS in Europe, products going into China will have to be tested by approved labs.

There will still be room for M&A activity, but blockbuster deals among large EMS competitors are probably not in the cards. M&A deals will likely occur for one of the following reasons:

• Mid-range and large providers seeking continued diversification.

• Large providers looking for additional technologies and/or skill sets.

• Regional providers striving for growth and footprint expansion.

• Providers making asset purchases as part of outsourcing agreements. This type of acquisition will involve equipment, inventory, and in some cases people. But high-cost facilities will not be acquired unless the provider does not have the skills or capacity to do the work with existing facilities.

Blockbuster deals among large competitors are unlikely to occur in 2007. Since three out of the top-six providers are attempting turnarounds, they are not inviting targets for their competitors. Integrating a business that still has challenges is harder than taking on one that has been performing well. Redundant facilities would also present a problem.

A private equity buyout is always a possibility as this is a growing trend in the business world. Viasystems serves as a precedent. The odds for a buyout probably go up if turnarounds are further delayed.

Look for providers to increasingly use product design as the hook that lands end-to-end manufacturing contracts. Outsourcing product design can be presented as the proverbial win-win for both OEM and EMS provider. The OEM can reap the following rewards:

– Save design resources for other projects.

– Minimize design handoffs to save time.

– Assure design for manufacturability and design for testability.

– Tap the provider’s engineering expertise in a product domain.

– Save design expense by utilizing a provider’s low-cost design centers.

The EMS provider can realize these benefits:

– Gain the inside track for a manufacturing contract by participating in product design.

– Be in a position to assume AVL control, allowing the provider to specify its suppliers.

– Utilize the design project to build domain expertise.

– Deepen the customer relationship.

– Gain the opportunity to do product upgrades as well.

But convincing an OEM to give up product design can be a tough sell where product design is considered a core competency. In such cases, outsourcing board design to the EMS provider will become more and more popular. Board design has become a commodity skill that OEMs will increasingly do without. This form of collaborative design still puts the EMS provider in a position to take on other design work down the road.

OEMs will pay more and more attention to their total delivered cost, which means greater emphasis on logistics. In a global scenario, EMS providers will have more say about what gets manufactured where in order to achieve this cost goal. Look for increasing use of a mix-and-match model where subassemblies are produced in a low-cost center and final product is assembled and configured near consuming markets. Reasons for doing it this way include transportation costs of bulky finished products, pipeline inventory costs, and customs duties. Binary decision making – do it here or in a low-cost country – is being replaced by providers’ ability to manufacture in multiple high- and low-cost geographies. Logistics capabilities for merging subassemblies and products for particular markets will become increasingly important. Look for more emphasis on logistics in 2007.

This trend also means that providers can and probably will get more creative in offering manufacturing alternatives in their quotes. Today, quoting is not just about price but also manufacturing locations.

Earlier reports of the demise of the EMS industry middle were premature. But a real threat has appeared. The threat to mid-range providers is coming from large providers with business units dedicated to such markets as medical, industrial, military/defense and instrumentation that are the stock-and-trade of mid-range and smaller providers. Two recent deals are telltale signs of this trend – Benchmark’s acquisition of Pemstar and Kimball’s planned purchase of Reptron. Both deals involve a large company acquiring a smaller company’s customers in such nontraditional markets.

In the past, predictions were made that the mid-range segment of the EMS industry would disappear. These predictions did not prove true because they were typically based on large providers undercutting prices. To the extent that large providers achieved volume purchasing, which often does not include expensive silicon, such purchasing did not put smaller providers out of business. These companies were adept at providing the flexibility necessary for high-mix, low-volume business often required by nontraditional markets. Large providers could not match this high-mix capability without units dedicated to high-mix business segments. Now that such units are established, they have had enough time to win business, some of which would have otherwise gone to mid-range providers.

Capacity additions in China can no longer be taken for granted. Providers’ main concern for expanding in China will not be land acquisition, construction or equipment purchases. The issue will be finding enough qualified workers, especially technical staff and management, to staff new factory space.

Labor shortages in Southern China are nothing new (April 2005, p. 8). And yet in the past, EMS providers did not report difficulty in staffing their factories in China, at least within the pages of MMI. Now however, a Flextronics executive has gone public about a shortage of qualified professionals in China. A January article in the Economist reported that Peter Tan, president and managing director of Flextronics Asia, “finds it especially hard to hire and retain technical staff, ranging from finance directors to managers versed in international production techniques such as ‘six sigma’ and ‘lean manufacturing.’”

China is not in danger of losing its crown as king of low-cost manufacturing. The country’s installed EMS base is too large, and its materials supply base remains robust and highly competitive. Nevertheless, rising labor and other costs, the possibility of further currency appreciation, and now staffing problems are adding up.

A new survey reveals that some OEMs are rethinking or have reversed their decisions to outsource a program. Of the responding OEMs with outsourced manufacturing or design, 27% indicated that they were currently thinking about bringing a product program back in-house, while 7% said they had already done so.

“We suspect that what might be driving it is a lack of performance on the part of some contract manufacturers that aren’t able to invest in robust systems and applications,” said Mark Zetter, president and founder of VentureOutsource.com (San Jose, CA), which conducted the online survey.

More than 500 participants from some 24 countries contributed to the findings of the survey, entitled Eyes on Electronics Outsourcing Industry Survey 2006. Besides OEMs, the survey also included other players in the electronics outsourcing industry.

Among other topics explored by the survey was the amount of mark-up that goes into a bill of materials when an EMS provider handles purchasing for the BOM. OEMs that don’t outsource or have not yet done so were asked to estimate the average percentage increase they felt an EMS provider might add to the OEM’s BOM when the provider purchases materials and components for the OEM. The survey found that 33% of respondents estimated 3% to 5% was added, and 16.2% judged that the increase was less than 3%. So in nearly half of these cases, which lacked actual outsourcing data, the maximum estimated mark-up was 5%. Another 8.9% figured that 6% to 8% would be added to the BOM. By comparison, survey results for OEMs that do outsource show that for the majority of these OEM respondents the added cost numbers are much higher when taken as a weighted average.

Another question looked at how the supply base perceives growth of the ODM (original design manufacturer) sector versus growth of the EMS market. VentureOutsource.com asked materials, components and equipment manufacturers; distributors; other suppliers and vendors; and related parties if they felt that the ODM market would continue to grow faster than the EMS market. Of the respondents, 64.2% answered yes. A majority of supply base respondents agree with forecasters who on average project higher growth rates for the ODM sector than for the EMS industry (Dec. 2006, p. 1). Interestingly, an assumption can be made that some of these respondents probably do business with both ODMs and EMS providers.

The survey also delved into outsourcing providers’ understanding of their customers’ product market cycles. EMS providers, ODMs, prototype houses and related parties were asked how well they feel they understand their OEM customers’ different product market cycles. On a scale of 1 to 6 with 6 indicating the highest degree of understanding, a majority of respondents rated their understanding at a level of 4 or 5. Those who assessed their understanding at a value of 4 represented 32.8% of respondents, while those who chose a value of 5 made up 21.9%.

Other VentureOutsource.com survey results for OEMs that do outsource indicate that a majority of these OEM respondents rated their providers’ understanding at lower levels. This difference could indicate a disconnect in the industry with respect to understanding product market cycles.

For more on the online survey, visit www.VentureOutsource.com.

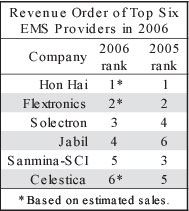

The same two companies will occupy first and second position when top-six providers are ranked by calendar 2006 revenue, but below them will be a new order of the largest industry players.

For 2006, Hon Hai Precision Industry remains in firm control as number one in sales. Its continued high growth in 2006 puts even more distance between Hon Hai and the rest of the industry. With estimated 2006 (calendar) sales of $17.49 billion, Flextronics retains its spot as the second largest EMS company by revenue. For the remaining four slots in the 2006 standings, however, two providers move up in the order and two drop down (see table).

It is a bit surprising that Solectron, with quasi-calendar year growth of 8.7%, climbs up one rung to the number-three spot. Solectron’s sales from December 2005 to November 2006 came in at $11.10 billion, slightly above Jabil’s $11.08 billion for the same period. MMI’s earlier estimates for 2006 had incorrectly put Jabil ahead of Solectron (Nov. 2006, p. 2). Jabil’s sales did run ahead of Solectron’s for the August and November quarters but not enough to overtake Solectron for the year. Still, Jabil, one of the two fastest growing top-six providers in 2006, did advance two positions in the order to number four.

Taking the final two positions are Sanmina-SCI and Celestica at number five and six respectively. Both moved down in the order compared with their 2005 positions (table). Sanmina-SCI’s 4.1% revenue decrease in 2006 caused it to drop down two slots. The company’s recent decision to form a separable personal and business computing unit would result in a smaller company and potentially a further reduction in rank, if this unit is sold off (Nov. 2006, p. 6). Celestica’s estimated growth rate of 3.7% in 2006 ensures that it remained the only top-six provider with sales under $10 billion.

Note: MMI arrived at estimated 2006 sales for Flextronics and Celestica by adding the midpoint of Q4 sales guidance to nine-month revenue. Consolidated sales for Hon Hai have not been projected yet, but based on first-half results revenue growth will likely exceed 30%.

Taiwan’s Hon Hai group plans to add to its massive installed base in China (Dec. 2006, p. 6), yet the world’s largest EMS provider is reportedly eyeing Vietnam for investment as well. What’s more, Hon Hai is expanding its efforts in India.

According to two online news services based in Taiwan, Hon Hai has sent a contingent to Vietnam to study the viability of a manufacturing site there. Two other sources, Bloomberg (posted on the Taipei Times website) and The Associated Press, reported that Hon Hai expects to manufacture in Vietnam within a year. But sources differ somewhat in their descriptions of this investment. Two sources say Hon Hai plans to invest $1 billion in Vietnam, while two others report that the group may make an investment of that magnitude (in one case the investment is described as over $1 billion.)

As a new member of the World Trade Organization, Vietnam is becoming a more favorable place for such investment. In addition, Vietnam’s average wage is about $60 a month, compared with increasing pay levels of $90 a month in some coastal regions of China, the Taipei Times reported.

Meanwhile, Hon Hai, under its trade name Foxconn, will partner with Cisco in India. Cisco has announced plans to launch a manufacturing pilot facility in Chennai, India. In line with the company’s outsourced manufacturing model, Cisco has selected one of its global manufacturing partners, Foxconn, to work with Cisco on the facility. This facility initially will manufacture certain products for the domestic Indian market. Reportedly, Hon Hai is already investing $110 million in the Chennai area, where it will develop a special economic zone with Motorola (March 2006, p. 6).

While Hon Hai may end up being the first top-six provider to manufacture in Vietnam, it is not the first EMS company to locate a manufacturing plant there. Sparton (Jackson, MI), for one, is an early adopter of offering low-cost manufacturing from Vietnam. Another EMS provider with a plant in Vietnam is CEI Contract Manufacturing Limited (Singapore).

In December, Hon Hai acquired a 64.59% interest in Altus Technology (Chu-Nan, Taiwan), a supplier of camera modules for mobile applications. The stock purchase amounted to NT$1.197 billion ($36.4 million). Founded in 2003, Altus was primarily funded by the Hon Hai group.

Deals done…This month, a wholly owned Jabil subsidiary successfully completed a previously announced tender offer for outstanding shares of Taiwan Green Point Enterprises (Taichung, Taiwan), a supplier of plastics for cell phones and other products (Nov. 2006, p. 1-2). As of Jan. 12, over 97.6% of Green Point’s shares were acquired at cost of about $871 million. The purchase was financed under Jabil’s $1.0-billion bridge credit agreement. Green Point will be merged into the Jabil subsidiary, subject to certain closing conditions, which are expected to be met in April….Benchmark Electronics (Angleton, TX) has completed its acquisition of Pemstar (Rochester, MN) through an exchange of shares. The deal was reported earlier (Oct. 2006, p. 6-7).

New business…NCR (Dayton, OH) has awarded Solectron (Milpitas, CA) a five-year contract to manufacture ATMs and payment solutions in the Americas and self-checkout systems globally. As part of a global realignment, NCR will transfer its Americas manufacturing to Solectron’s sites in Columbia, SC; Guadalajara, Mexico; and Jaguariuna, Brazil, by the end of 2007. Solectron has been producing and assembling data warehouse servers as well as providing systems integration for NCR’s Teradata Division for seven years….Redback Networks (San Jose, CA), which develops networking solutions for IP-based services and communications, has entered into a one-year manufacturing agreement with Jabil (St. Petersburg, FL). Under the agreement, Jabil will manufacture certain Redback products.…Mintera (Acton, MA), whose products enable optical transport at 40 gigabits per sec, has established a manufacturing relationship with Sanmina-SCI (San Jose, CA), which will oversee the manufacture of a 40 Gbps DWDM transport subsystem at its Allen, TX, location. Also, Sanmina-SCI serves as one of three partners in a system that provides an end-to-end solution for improved communications within coal mines. The system uses the networking capabilities of Rajant (Malvern, PA) and Sanmina-SCI. …LaBarge (St. Louis, MO) is building a variety of cable assemblies for US Marine Corps applications under a $1.3-million contract from Applied Marine Technology, a supplier in the homeland security sector.…Sparton (Jackson, MI) has landed a contract for the manufacture of sonobuoys for the US Navy. The contract is valued at about $13.8 million. Sparton is the only US-owned designer and manufacturer of the submarine detection devices.

Equity-based partnership…CEI Contract Manufacturing Limited (Singapore), an EMS provider that is publicly traded in Singapore, has entered into an agreement to acquire a 10% stake in the enlarged share capital of Kinergy (Singapore), which intends to carry out an initial pubic offer. Kinergy is a high-mix, low-volume EMS provider as well as a manufacturer of proprietary equipment for customers who are mainly in the semiconductor industry. The equity purchase will allow the two companies to realize the synergies in their capabilities and to expand their market share jointly. CEI will bring its strength in board assemblies to the partnership, while Kinergy will contribute its strength in precision mechanical engineering and assemblies.

Some financial results…For the quarter ended Dec. 30, 2006, Sanmina-SCI posted non-GAAP net income of $34.7 million, up from a net loss of $2.1 million in the prior quarter but below net income of $39.6 million in the year-earlier quarter. Non-GAAP EPS for the December quarter amounted to 7 cents, which was in the middle of the guidance range. GAAP net income for the quarter increased year over year to $28.2 million from $17.4 million. Revenue totaled $2.78 billion, up 2.3% from the prior quarter but down 2.9% from the year-ago quarter. Sanmina-SCI saw sequential growth in the following segments: multimedia and consumer electronics, medical, defense and aerospace, automotive, and personal computing systems. Non-GAAP gross margin for the December quarter stood at 6.1%, representing an increase of 130 basis points sequentially and 10 basis points year over year. The company’s core EMS business, accounting for $1.94 billion in the quarter, produced a non-GAAP gross margin of 7.9%, while the Personal Computing division, with $837.5 million in sales, came in at 2.0% gross margin. Non-GAAP operating margin was 2.5% in the December quarter versus 1.2% in the prior quarter and 2.7% in the year-earlier period. “Demand in the quarter was not as strong as we have seen historically, but we experienced nice growth from a number of our core markets and a majority of our key customers,” stated Jure Sola, chairman and CEO. For the March 2007 quarter, Sanmina-SCI expects revenue to be seasonally down in the range of $2.65 billion to $2.75 billion. Guidance also calls for non-GAAP EPS of 5 cents to 7 cents and non-GAAP gross margin of 6.2% to 6.4%. Earlier in the month, Sanmina-SCI filed its Form 10-K for the fiscal year ended Sept. 30, 2006. Within the 10-K were restated historical results correcting errors related to equity grants (Dec. 2006, p. 2)….Plexus (Neenah, WI) reported sales of $380.8 million for the December 2006 quarter, slightly below the low end of guidance for the quarter. Although Plexus achieved better than expected revenue performance from the medical sector, the company’s other sectors contributed lower than expected sales. Sales for the quarter declined 4% quarter over quarter. Still, they increased 16% year over year, with growth in all end markets except for wireless infrastructure, which was essentially flat. Non-GAAP EPS was 33 cents at the midpoint of guidance. Non-GAAP gross margin of 10.4% was up by 90 basis points year over year, but down about 90 basis points from the prior quarter. Non-GAAP operating margin of 5.1% was 80 basis points higher than a year earlier, but dropped by 110 basis points from the previous quarter. Looking to the March quarter, or Plexus’ fiscal Q2, the company said it is experiencing softness with a number of customers across all of its market sectors. Also, there is continued uncertainty regarding follow-on orders for a large defense contract. “We are in for a lousy Q2, resulting in a material impact to our growth goals for the fiscal year,” said Dean Foate, president and CEO, during a conference call. Plexus expects March quarter sales of $345 million to $355 million and non-GAAP EPS of 15 cents to 19 cents. Given this fiscal Q2 outlook, questions about longer-term economic conditions, and uncertainty about the defense contract, Plexus has revised its fiscal 2007 growth target to 8% to 12% from a previous range of 15% to 18% (Nov. 2006, p. 6). The company expects growth to resume in all sectors in the June quarter (fiscal Q3) and projects continued growth into the September quarter. “But given the steepness of the recent end market pullback, we are approaching the later quarters with a measure of caution,” said Foate.

Some company news…Bernama, the Malaysia National News Agency, reported that RM3.5 million ($1 million) worth of components belonging to Solectron were stolen from a transit warehouse in Penang on Christmas Day. This theft follows a November 2006 robbery of an air cargo warehouse in Penang, where components were also taken, according to the news service….Elcoteq’s board of directors will propose during its March general meeting that the company’s domicile and head office be transferred to Luxembourg. Elcoteq is currently headquartered in Espoo, Finland.

US expansion…That’s not a misprint. According to Business First of Louisville, Solectron’s Louisville, KY, operation is relocating to a 500,000-ft2 leased facility, more than twice the size of the building it replaces. The company’s Form 10-K lists the Louisville operation as a repair and refurbish activity, which does not lend itself to offshoring.

Another factory in Thailand… Construction has begun on a new factory in Fabrinet’s Pinehurst manufacturing complex near Bangkok, Thailand. The company’s latest factory, completed in November 2005, is near capacity. At about 300,000 ft2, the new facility will accommodate fast-growing demand for Fabrinet’s optical components, module manufacturing and system assembly services as well as anticipated growth in capital equipment, automotive and medical markets. Fabrinet will be able to customize factory assembly lines to support Class 100,000 to Class 100 clean rooms for opto-electronic manufacturing and “dry rooms” to meet the ultra-low humidity requirements of medical devices.

More restructuring…Jabil has closed its facility in Brugge, Belgium, according to X-Line Asset Management’s website for surplus equipment....Sparton (Jackson, MI) will close manufacturing operations at its Deming, NM, facility no later than March 31. The company said it can no longer offer competitive cable wire harness solutions to its customers. Sparton offered this service to select transportation customers for many years.

People on the move…Curtis Campbell has resigned as VP of sales for Top 50 EMS provider Flash Electronics (Fremont, CA) to become president of another provider, Isis Surface Mounting (San Jose, CA).