![]()

Cover Story

Restructuring Reshapes Industry

Market Data

Researchers Expect Another Down Year

Worldwide EMS Market Estimates 2001-2006

News

IBM To Sell Endicott Site To Local Group

Lexmark Deal Puts MSL in Mexico

Sanmina-SCI Acquires Memory Module Firm

Flextronics To Add Network Services Unit

The immediate effects of industry restructuring are obvious. But the job losses and the downsizing or closure of plants are taking place primarily in high-cost regions. When the dust settles in a year or so, the EMS industry will emerge in a different form from the one that preceded the downturn.

A much larger share of manufacturing capacity will end up in low-cost regions, and for at least two tier-one players the restructuring process will leave 60% or more of global capacity in these regions.

The long-term implications of this shift in capacity mix are beginning to surface. For one thing, EMS facilities being closed in the US and Western Europe will probably stay that way for good. The US's role as a center of EMS production will grow increasingly limited to products that cannot be manufactured outside the US for technical, logistics or security reasons.

Downsized facilities in the US and Western Europe will typically find their missions changed. A number of these facilities will see more NPI work as they become product launch sites feeding volume production facilities in low-cost locations. There are also examples of facilities being converted to repair centers.

But restructuring will have effects that ripple beyond the EMS industry. Companies that supply the industry will need to reexamine how they will support an industry with a much larger share of production in low-cost regions, especially Asia.

Take Solectron. When the provider started restructuring roughly 30% of its capacity was in low-cost areas and 70% was in high-cost regions. When Solectron completes the process in four to five quarters, that mix will shift to 60% low-cost and 40% high-cost. Then there's Celestica, which recently announced further restructuring. These actions will increase Celestica's capacity in low-cost geographies from about 55% to 65%.

Shifts in capacity mix can come about in two ways. One is the loss of capacity caused by closures and downsizing in the high-cost regions. The other effect results from providers adding people and floor space in Asia. For example, Flextronics will add 10,000 people in Asia when it closes its Casio and NatSteel Broadway acquisitions. These deals will increase the provider's work force in Asia by some 37%. Flextronics is also enlarging its Asian floor space, and a major increase will come from the construction of a new industrial park in Shanghai, China.

Meanwhile, restructuring charges continue to pile up. Additional charges recently announced include about $150 million in the June quarter for Flextronics, $313 million in the May quarter and about $150 million in subsequent quarters for Solectron, and $300 to $375 million spread over the September and December quarters for Celestica. These charges total about $913 to $988 million.

Despite the size of these and earlier charges, details of actions taken are hard to come by. Providers are right to withhold such information pending notification of affected employees. But often the details are never released. There is a feeling in the industry that if a provider discloses the details, this company alone will face negative publicity.

There are some exceptions, though, such as Flextronics' facility in Brno, the Czech Republic, where production will be moved to Hungary. (See also News on p. 8.) A Flextronics spokesperson said it didn't make sense to keep the manufacturing side of this modem facility open since it serves one main customer. About 1000 people will lose their jobs, while a small group in design and development will remain. So restructuring has not been confined to high-cost areas.

But high-cost regions have borne the brunt of it. The capacity shift to low-cost regions will have consequences, some of which still remain unclear. But the effects will likely be far reaching. Here are some possible impacts worth considering:

Whatever the answers, the downturn has led to a reshaping of the industry. Restructuring is bringing immediate changes to the industry as well as long-term effects. Pay attention to both.

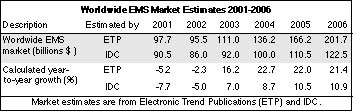

Two market research firms have recently reached the same conclusion: the worldwide EMS market will decline again in 2002, for the second year in a row. But they differ markedly when it comes to forecasting how fast the EMS market will grow once it recovers. Electronic Trend Publications, or ETP (San Jose, CA), sees the market returning to predownturn levels, while IDC (Framingham, MA) takes a more conservative view of the future.

ETP's latest report on the global EMS market, just released, projects the market will slip 2.3% from $97.7 billion in 2001 to $95.5 this year. This slippage follows an estimated decline of 5.2% from 2000 to 2001. But the report expects market growth to snap back to 16.2% in 2003, followed by increases of more 20% in the next three years. Based on IDC's forecast, the market will hit $111.0 billion in 2003, rising to $201.7 billion in 2006 (table).

According to ETP, once the telecom market recovers, estimated at sometime in late 2003 or early 2004, outsourcing by OEMs, particularly Japanese companies, in such segments as consumer products will drive strong growth rates for the remainder of the forecast period.

It comes as no surprise that ETP is predicting Asia will experience the strongest EMS growth of any region over the period 2001 to 2006, with Asia's market share growing from 20% to 26%. This gain will come at the expense of North America, and ETP expects the North American slice of the market to shrink from 51% in 2001 to 45% in 2006.

Together, the communications equipment and computer/office segments will maintain their lion's share of the EMS market from 2001 to 2006. ETP projects their combined share will start the period at 74% and end up at 73%. But the computer/office segment will add 5% to its share, which will exit the period at 37%, while communications' share will lose 6%, ending at 36% of the market. So the ETP forecast has the two segments reaching parity in terms of EMS revenue by 2006. ETP expects some of the highest growth rates to occur within the transportation sectors - automotive and aerospace.

ETP's new report is entitled The Worldwide Contract Electronics Manufacturing Services Market, Ninth Edition. For more information, contact saberry@electronictrendpubs.com.

IDC has also issued a new EMS market report, in which the firm has again lowered its 2002 forecast for the EMS market (May, p. 3). IDC has reduced its previous 2002 estimate of $92.0 billion to a current forecast of $86.0 billion. IDC's earlier forecast of slight growth this year has been replaced with prediction of a declining EMS market for the second year in a row. After shrinking by 7.7% in 2001, the market will contract by 5.0%, or $4.5 billion, this year, according to the IDC report.

The EMS industry will begin to grow again in 2003 but will not return to the growth levels seen before the economic downturn, notes IDC. The firm is predicting a 7.0% increase for 2003, with growth topping out at 10.9% in 2006 (table). Given these modest growth rates, the market won't hit $100 billion until 2004 and will end up at $122.5 billion in 2006. IDC calculates a compound annual growth rate (CAGR) of 6.2% from 2002 to 2006.

IDC believes that increased penetration of the European and Japanese markets is essential to the long-term growth of the EMS industry. The firm expects Japanese OEMs will begin to add significant revenue to the EMS industry by the end of 2003 or the beginning of 2004.

In 2002, the telecom and networking segments of the EMS market will decline by $3.0 billion and $1.5 billion respectively, predicts IDC. These segments will begin to generate growth for the EMS industry in 2004, according to the new report. It also foresees the computers segment shrinking and the servers and storage business holding steady in 2002. The peripherals and "other" segments will contract this year as well.

The one bright spot in the current year is the consumer sector, which IDC expects to grow by $2.0 billion. This segment has a forecasted CAGR of 13.6% from 2002 to 2006, the highest rate among IDC's segments. The firm expects the consumer segment to pick up market share over the forecast period and exit 2006 with a leading share of 21%.

The new IDC report is entitled Year of Restructuring: EMS Industry Forecast and Analysis, 2001-2006. Contact jnagle@idc.com.

The number of EMS deals closed in the first half of 2002 was down by 27% compared with the same period last year. MMI counted 27 EMS transactions closed in the first six months of 2002 versus 37 deals done during the first half of 2001.

Unless there is a flurry of M&A activity in the second half of 2002, the year will finish with substantially fewer deals than recorded in 2001. If the current level of deal-making continues for the rest of the rest year, 2002 will register about 54 transactions, or about 21 fewer than the 75 deals tallied last year (Feb., p. 1-5). In that event, 2002 would mark the second successive year of declining M&A activity. The number of EMS transactions tracked by MMI peaked at 111 in 2000.

Fewer purchases of OEM manufacturing assets have contributed to this year's reduction in deals done. For the first half of the year, MMI counted ten acquisitions of OEM manufacturing assets including a tier-one automotive supplier, compared with 13 such deals in the year-earlier period. EMS providers in general have become more selective in taking on OEM facilities in high-cost centers.

But one can speculate about other factors that may have hindered deal-making this year. They include lower stock prices, fewer players due to consolidation, lower cash levels in some cases, a reduced need for footprint expansion among major players, and excess capacity.

On the other hand, the downturn did produce more distressed sales. In the first six months, assets of six failed providers were bought, based on reports in MMI.

Still, the downturn did not prevent some providers from acquiring capabilities, such as design engineering or depot repair, to enhance or extend offerings beyond core manufacturing services. In the first half, nine such deals went through, including five from Flextronics. Because these deals often do not carry high price tags, they appeal to providers even in tough times.

Editors note: Transaction data come from deals identified by MMI in a given year. Not all deals are disclosed, and some come to light well after the fact.

In an effort to preserve jobs, IBM has agreed to sell its 4.1 million-ft2 Endicott, NY campus, including an EMS business, to a local investor group. This group formed Endicott Interconnect Technologies to acquire IBM's Interconnect Products (ICP) operations at the Endicott site.

Within IBM's Microelectronics business, ICP manufactures plastic chip carriers, bare printed circuit boards, and backplane and printed circuit assemblies. ICP supplies both IBM and external customers, including EMS clients that utilize the site's ECAT (electronic card assembly and test) services. As part of this deal, Endicott Interconnect Technologies has obtained an agreement to supply IBM for four years.

The new company will take on nearly 2000 IBM employees, or about half of the site population. IBM will lease back 1.4 million ft2 for its remaining business units at the site.

ICP's ECAT operation produces board assemblies for IBM high-end servers as well as external customers. These customers include Sun, which contracts for server motherboards, and Nintendo, for which the site builds board assemblies for video game consoles.

The new owners will invest $100 million, which includes the purchase price and improvements. IBM did not disclose the price. The Binghamton Press & Sun-Bulletin reported a price of $65 million, which has not been confirmed.

Local investors from the Broome County, NY area make up the new ownership. Principal backers consist of David and William Maines of Maines Paper and Food Service and James Matthews, owner of The MATCO Electronics Group. Recall that MATCO Electronics no longer exists as an EMS provider; its assets have been sold off (March, p. 5). William Maines serves as president of Endicott Interconnect Technologies.

The sale results from the restructuring of IBM Microelectronics, which is now focusing on a high-end foundry business, ASICs and standard products, and new technology services. IBM also pointed out that ECAT is not a strategic area for the company, which has been divesting ECAT operations for some time.

An IBM site executive said the investors group's proposal, which focused on preserving local jobs, was IBM's best option. Reportedly, one top-tier provider offered to move work offshore. In general, large providers have grown reluctant to take on OEM facilities in high-cost regions.

New York State officials, including Governor George Pataki, were involved in deal negotiations. Endicott Interconnect Technologies is eligible to apply for state grants totalling $5 million.

MSL (Concord, MA) has made good on its longstanding goal to manufacture in Mexico. Another EMS provider, Electronic Product Integration Corp. (Southfield, MI), is also starting up in Mexico, while IEC Electronics (Newark, NY) withdraws from the region.

MSL has acquired a PCB assembly operation in Reynosa, Mexico, from printer OEM Lexmark International. That operation, which went under the name Lexmark Electronics, resides in a facility of about 150,000 ft2 with about 240 employees.

Although cost pressures have led some OEMs to move work from Mexico to Asia and China in particular, MSL remains a backer of Mexico. "Mexico continues to be a low-cost manufacturing opportunity for customers of ours that want to continue to manufacture close to other facilities they may have in North America," said Bob Bradshaw, MSL's CEO and president.

He added, "I still believe - and the customers I talk with still believe - that there's a requirement to manufacture and to fulfill to end customer demand in North America. And certainly Mexico provides low-cost manufacturing capability to meet those objectives."

Lexmark becomes a new customer of MSL, which has entered into an agreement to supply Lexmark from the Reynosa facility. The agreement also gives MSL time to bring other customers into the facility.

The sale of the Reynosa facility is consistent with Lexmark's strategy to contract out most of its manufacturing. The bulk of its manufacturing is already outsourced to Asia.

The facility had been for sale since last fall.

Meanwhile, IEC Electronics is closing its Mexican facility, also in Reynosa. The company is selling the facility's assets - equipment, furniture, fixtures and inventory - to another EMS provider, Electronic Product Integration Corp. (EPI), which is opening a plant in Juarez, Mexico. The deal also calls for the transfer of IEC's customer base in Reynosa to the new EPI operation in Juarez.

"We firmly believe selling the assets of our Mexican facility is a step in the right direction towards restoring financial stability and economic viability to this company. Without the continuing losses in Mexico, we expect to see improvement to our bottom line in the fourth quarter," stated W. Barry Gilbert, IEC's chairman and acting CEO.

According to privately-held EPI, the equipment bought from IEC will allow EPI to jump start its Juarez facility. The company expects production in the Juarez facility to begin after the assets have been transferred in mid to late August. EPI is also planning to use some of the purchased equipment at its Norwalk, OH facility, which operates as EPIC Technologies.

EPI's president, John Sammut, described this asset purchase as "the next step in our strategy to broaden our EMS capabilities with complete system integration in Mexico that will enable EPI to compete for a broader range of assembly services."

Started in 1999, EPI plays in the high-mix, low- to medium-volume side of the market through its EPIC facility in Ohio (May, p. 2). Manufacturing services primarily consist of complex PCBA. EPI was formed by TMW Enterprises, which is controlled by Thomas Wheeler, and the Crawford Group.

Benchmark Electronics (Angleton, TX) and Sun Capital Partners (Boca Raton, FL), a private investment firm specializing in leveraged buyouts and turnarounds, have emerged as the successful bidders in the bankruptcy court auction of assets of ACT Manufacturing (Hudson, MA). The company filed under Chapter 11 in December 2001.

Benchmark is acquiring the Thailand and UK operations of ACT for a price of $45.2 million in cash. The transaction includes the assumption of about $15 million in net debt under an interest-bearing debt facility. Based on recent information, Benchmark expects annual revenues from this acquisition to run between $180 and $200 million. On that basis, the transaction is expected to be slightly accretive to Benchmark's 2002 earnings, before any one-time charges associated with the deal. Subject to certain closing conditions, the deal is expected to go through this month.

The Thailand operation will allow Benchmark to expand its Asian presence into a high-volume, low-cost site in the region. Benchmark has been manufacturing in Singapore and has sought a low-cost Asian location for some time (Sept. '00, p. 4). The deal will also bring Benchmark several new customers in the medical, telecom and industrial control sectors.

In Thailand, Benchmark is gaining a 240,000-ft2 facility located in Ayudhaya near Bangkok. The facility comes with expertise in RF and wireless. Benchmark is also buying the ACT operation in Leicester, England, with a 55,000-ft2 facility. ACT originally acquired this UK facility in 2001 from the Fisher-Rosemount Systems division of Emerson.

ACT's US assets have gone to an affiliate of Sun Capital Partners. Through the affiliate, Sun Capital has bought ACT operations in Hudson, MA; San Jose, CA; Lawrenceville, GA; and Corinth, MS. In these US operations, there remains "a core set of customers with a decent level of revenues," said M. Steven Liff, VP of Sun Capital.

These operations now constitute a new company, ACT Technology, Inc. The new entity will provide EMS to the networking, telecom, high-end computer, industrial and medical segments. According to Liff, the new company plans to "refocus on customers, match expenses to revenue, fix the cost structure of the business, continue to grow the customer base, and possibly look for strategic acquisitions."

Sun Capital is working with the ACT management team to determine how many employees will be needed and who will run the business.

Conspicuously absent from these deals is ACT's 230,000-ft2 operation in Angers, France, which ACT acquired from the French company Bull in 2000. The Angers operation specializes in complex and large PCBA and system assembly and integration. According to a spokesperson for ACT, no decision has been made yet on the French operation.

In addition, ACT is winding down its operation in Hermosillo, Mexico, and pursuing the closure of its cable operation in Dublin, Ireland, in keeping with Irish law.

Sanmina-SCI (San Jose, CA) has acquired Viking Components (Rancho Santa Margarita, CA), a supplier of memory modules and some other products. In addition, the EMS company is combining this acquisition with the company's InterWorks subsidiary to form Sanmina-SCI Modular Solutions Division.

With the new division, Sanmina-SCI is positioning itself as a leading manufacturer of modules and subsystems based on Flash, DRAM, SRAM and DSP technologies for OEMs and end-users in telecom, networking, network storage, computing and other embedded markets.

Founded in 1988, privately-held Viking designs, manufactures and distributes products including computer system memory, flash memory and readers, and modems. Viking supplies resellers, distributors and OEMs. The company has ISO-certified facilities at its Rancho Santa Margarita, CA headquarters and in Dublin, Ireland.

"This new division formalizes our expanding capabilities in supplying custom and standard modules and modular subsystems," stated Randy Furr, Sanmina-SCI's president and COO. He added that the combined infrastructure of the two operations increases Sanmina-SCI's ability to provide customers with a global solution.

Sanmina-SCI is not the first provider to adopt a strategy of offering modular, or building-block, solutions for OEMs' products. Solectron has utilized a building-block approach through its Technology Solutions unit. Similar to Sanmina-SCI, Solectron made acquisitions in the memory module space - namely SMART Modular Technologies in 1999 and Centennial Technologies last year - which support a building-block strategy.

As for the Viking deal, customers were an important aspect. "We selected Viking because of its proven expertise and longstanding partnerships with leading OEM customers in many of our core markets," stated Furr.

According to a September 2001 article in the Orange County Register, Viking had to restructure last year in the wake of falling memory prices. The newspaper reported that the company moved away from low-margin products.

To oversee the Modular Solutions Division, Sanmina-SCI has hired Ralph Kaplan. Most recently, Kaplan served as president of High Connection Density, a supplier of memory and connector products. Before that, he was VP and GM of memory products at SMART Modular Technologies. Glenn McCusker, founder and CEO of Viking Components, will be joining the senior management team at Sanmina-SCI.

The other part of the new division, InterWorks, was acquired by Sanmina-SCI in 2000 as a supplier of DSP modules and memory products.

Flextronics (Singapore) will be acquiring Elisa Instalia, the network installation and maintenance arm of Finnish telecom carrier Elisa Communications. Following Flextronics' acquisition of Orbiant Group in Sweden last year (Nov., '01, p. 7), this deal furthers the position of Flextronics as a network services provider in the Nordic region.

Also, Elisa Communications, reportedly the second largest telecom operator in Finland, has made Flextronics a long-term partner to construct and maintain fixed and mobile networks.

According to Dow Jones, the purchase price is 37.2 million euros in cash. The transaction is expected to be completed on August 30. Elisa Instalia will become part of Flextronics Network Services (Stockholm, Sweden).

Elcoteq (Espoo, Finland) has signed a memorandum of understanding to acquire design activities from Benefon (Salo, Finland), a mobile telematics OEM. The Finnish EMS provider plans to transfer three-fourths of the capacity of the Benefon R&D Center into Elcoteq Design Center Oy, a new wholly-owned subsidiary of Elcoteq.

Benefon will become a customer of the new design unit, which will gain access to Benefon's intellectual property rights relating to the design work in question. The OEM's R&D group will continue to be responsible for ongoing telematics development, but will work closely with Elcoteq Design Center, from which Benefon will contract for a major portion of the design unit's initial capacity. This deal also offers Elcoteq an opportunity in global procurement and manufacturing.

According to Elcoteq, its Design Center unit will enable the company to offer technology, product development and ODM services to Elcoteq customers. The new unit will provide development services based on wireless terminal platforms and acquire technologies for these products. This deal supports Elcoteq's redefined strategy (May, p. 5).

A preliminary price was set at about 11 million euros for the R&D capacity. The parties expect the deal to be closed in July.

Some 90 design and engineering professionals now employed or contracted by Benefon will join the Elcoteq Design Center. Most of them are located in Salo, Finland, which will become the main location for the design unit. Some 30 people are located in Turku and Forssa, Finland, and a smaller number in St. Petersburg, Russia. The design unit will continue to operate in Benefon's R&D locations, but later on will move to its own facilities.

Elcoteq plans to appoint Markku Leinonen, an Elcoteq veteran, to head the Design Center. Jorma Nieminen, founder and president of Benefon, has agreed to make himself available to the new Elcoteq unit for at least one year.

Benefon's mobile telematics instruments provide full voice and telematics communication as well as precise location of the user.

New programs at Solectron... Solectron (Milpitas, CA) recently announced expanded relationships with a number of OEMs. The company will provide NPI, enclosure services and PCBA for a new high-end Apple project. IBM has chosen Solectron to handle PCB and system assembly services for a mid-range server product. ADC Telecommunications has awarded Solectron a two-year contract to supply NPI, PCBA, system build and integration, burn-in, upgrade and repair services for a cable modem termination system. Solectron will provide NPI through fulfillment for McDATA's latest network switching product and perform a series of integrated services for Alcatel's sonet metro optical system. Handspring has selected the provider to handle all North American and Asian repair and refurbishment for new products. Solectron also revealed three new customers. Under a one-year contract, Solectron will supply Dot Hill Systems (Carlsbad, CA) with NPI, complete product manufacturing, test and product distribution for a new line of high-availability data storage products. Another new customer is SkyBitz, which provides global location tracking systems. Solectron also landed appliance manufacturer Maytag as a new customer in what Solectron describes as Maytag's first outsourcing relationship with an EMS company.

Other new programs...NICE Systems (Ra'anana, Israel) has engaged Flextronics to provide turnkey manufacturing from order receipt to product shipment for NICE's voice recording products. NICE will complete the handover of production for its voice recording line during the second half of 2002....Lifestream Technologies (Post Falls, ID) has chosen Sanmina-SCI as the primary manufacturer for a smart-card enabled home cholesterol monitor....nStor Technologies (San Diego, CA) has contracted production of its NexStor 4000 series of data storage products to the Electronics Manufacturing group of Varian (Palo Alto, CA)....Raytheon has awarded XeTel (Austin, TX) a contract for volume production of circuit card assemblies for the next-generation Sidewinder missile. Raytheon expects to produce more than 15,000 missiles between US and international customers....LaBarge (St. Louis, MO) has landed a $9-million contract from Northrup Grumman's Electronic Systems sector to supply subsystems for a military airborne radar system. The provider was previously named to the system's production team (Mar., p. 8)....Integrex (Bothell, WA) will produce a mobile docking station for SonoSite (Bothell, WA), a supplier of hand-carried ultrasound systems....Chartered Electro-Optics Pte Ltd, an electro-optics subsidiary within the Singapore Technologies Group, has selected CEI Contract Manufacturing Limited (Singapore) to supply PCBA-related services for a new project. Chartered Electro-Optics designs and manufacturers products such as thermal imagers and laser systems. A company owned by Singapore Technologies holds a stake in CEI....The Value Added Division of DDi Corp. (Anaheim, CA) will manufacture the InstantOffice product line for Vertical Networks (Sunnyvale, CA). DDi will supply these integrated communications products out of its newly expanded 61,000-ft2 facility in San Jose, CA. Although DDi is known as a PCB and backplane supplier, in this case the company will manufacture five products, each consisting of a chassis, backplane, system components and software....Celestica (Toronto, Canada) is one of ten members of a consortium to develop and test a Virtual Input Pen that will serve as an input device for mobile and fixed handsets. The European Commission will fund 50% of the 24-month project, with a total budget of about 4.4 million euros.

When it comes to cell-phone outsourcing, Nokia has been a holdout for internal manufacturing. According to a recent news report, Nokia will continue to disappoint EMS providers who want to see Nokia raise its level of mobile-phone outsourcing.

Reuters reported the president of Nokia's mobile phones division as saying that Nokia did not expect to increase mobile-phone outsourcing from a current level of about 15 to 20% of production.

XeTel (Austin, TX) has engaged an investment bank, Lincoln Partners LLC (Chicago, IL), to help in reviewing strategic alternatives, including the sale or merger of XeTel, in whole or in part. The provider has issued a positive sales outlook for the June quarter, while XeTel's auditor has expressed doubt about its ability to continue as a going concern.

"The reality of this economy is that we will need to improve our equity position in the future. Hence, we have enlisted Lincoln Partners to assist us in the many alternatives available to us," said Angelo DeCaro, XeTel's president and CEO, during its latest conference call.

These alternatives range from "an equity infusion that may or may not result in a change in control of the company. It could be a merger of two or three smaller companies rolled up with an equity infusion to manage those [two or] three, all the way to the extreme of just an outright sale of the company," said DeCaro.

Sales for XeTel's fiscal year ended March 2002 amounted to $79.8 million, down 58.6% from $192.9 million in the prior year. For fiscal 2002, the company reported a net loss of $23.6 million, including $6.2 million of inventory write-downs and customer settlement costs. Ericsson was XeTel's largest customer at 22% of fiscal 2002 sales, and telecom accounted for the largest share of sales at 41%.

For the March quarter, Xetel reported at net loss of $8.7 million on sales of $12.0 million. That loss included inventory write-down and bad debt reserves totaling more than $3 million. Sales were flat compared to the previous quarter's sales of $12.3 million.

But XeTel expects revenue to increase sequentially by at least 50% in the June quarter, and the company has set a goal of returning to at least break-even in the September quarter.

Meanwhile in XeTel's recently filed form 10K, its auditor, PricewaterhouseCoopers, warned, "Without improvement in profitability or additional financing, the company will lack sufficient working capital to fund operations for the entire fiscal year ending March 29, 2003. These matters raise substantial doubt about its ability to continue as a going concern."

XeTel has made a short-term arrangement for working capital. In April, the company set up a new asset-based credit facility with Silicon Valley Bank. That facility allows for borrowings up to $4.3 million and matures on July 22.

In form 10K, XeTel disclosed that its ability to continue as a going concern depends on its ability to return to profitable operations and positive cash flow, to obtain new financing to pay obligations as they become due, and to maintain adequate liquidity.

But long-term debt is not one of XeTel's concerns. The company eliminated its long-term debt as of the end of the March quarter.

Several of XeTel's customers have switched to consignment to ease the company's cash flow, while others have agreed to prepayments or other such arrangements.

XeTel is the second EMS provider to announce a relationship with Lincoln Partners in recent months. The first was IEC Electronics (April, p. 7). Jack Calderon, former CEO of EFTC, leads the EMS practice at Lincoln Partners.

New names...Singapore-based provider Venture Manufacturing (Singapore) Ltd has changed its name to Venture Corporation Limited....Comtel Holdings, which has three operating locations in Southern California, has taken the name of one of its acquisitions - Corlund Electronics. The Corlund name was chosen because of Corlund's 20-year history in the EMS industry and its name recognition in the region. Sales for the renamed provider were up 42% in 2001 to $72 million, and the forecast for this year is additional growth of 20 to 25%. According to Corlund's CEO, Lyle Jensen, its focus on a vertical EMS model with emphasis in the medical, RF and instrumentation markets has served the company well during the downturn. Besides offering typical EMS capabilities of NPI, PCBA and box build, Corlund also provides precision machining and sheet metal fabrication, cable harnesses, and a dedicated depot repair center. The company is moving its headquarters from Tustin to Vista, CA.

Some financial results...For the fiscal year ended April 30, SigmaTron International (Elk Grove, IL) reported sales of $84.8 million, up 5% from the prior fiscal year. Net income for fiscal 2002 came in at $1.5 million, compared with a net loss of $1.2 million a year earlier. The provider has started to investigate opening an operation in China....Surface Mount Technology Ltd. (Hong Kong) increased its sales to HK$1.005 billion in the fiscal year ended March 31, compared with HK$882.5 million in the previous fiscal year. Net profit amounted to HK$36.1 million versus HK$66.5 million in the prior year....For the fiscal year ended March 31, the China-based contract manufacturing business of VTech (Hong Kong) recorded a 27% decline in sales to $92.8 million. VTech, which sells electronic learning and telecom products, said EMS profits were stable.

New facilities in China...Solectron is adding 252,000 ft2 of manufacturing and warehouse space in Suzhou, China....Surface Mount Technology Ltd. expects that a new 100,000-ft2 factory in Dongguan, China, will be operational in August. The provider is also setting up a new plant in Suzhou, and operations there are scheduled to begin in September.

Lawsuits...A number of law firms have announced securities class action lawsuits alleging that Flextronics and top executives failed to disclose that the company's business and operations were being adversely affected in certain ways.

More restructuring...Jabil Circuit (St. Petersburg, FL) plans to consolidate its Liverpool, UK plant into its Coventry, UK plant at an estimated cost of $25 to $28 million, for which Marconi has agreed to reimburse Jabil. Jabil acquired the two plants from Marconi....PEMSTAR (Rochester, MN) has moved to consolidate its engineering and manufacturing centers in San Jose, combined its Thailand facilities, and consolidated its Boston manufacturing and engineering units.