![]()

![]()

Cover Story

ODMs Boost Outsourcing Market in 2003

World Markets

Opportunities Seen for European EMS

Too Much of a Good Thing in Asia?

News

TeliaSonera Buying Flextronics Operation, Expands Relationship

TFS To Buy Out Partner in Malaysia

Canadian Provider Makes Acquisition

MC Assembly Starts Up in Mexico

Q1 results for 18 EMS providers

Last Word

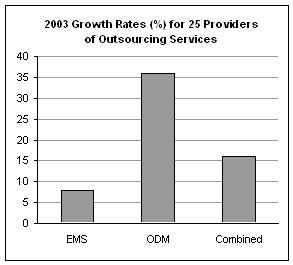

Outsourcing and the EMS industry are often considered one and the same. So one would be tempted to assume that the overall market for outsourcing resumed moderate, single-digit growth last year in parallel with the EMS industry. However, recent analysis by MMI suggests that the outsourcing business, comprised of both EMS providers and ODMs, grew substantially faster than the EMS industry alone.

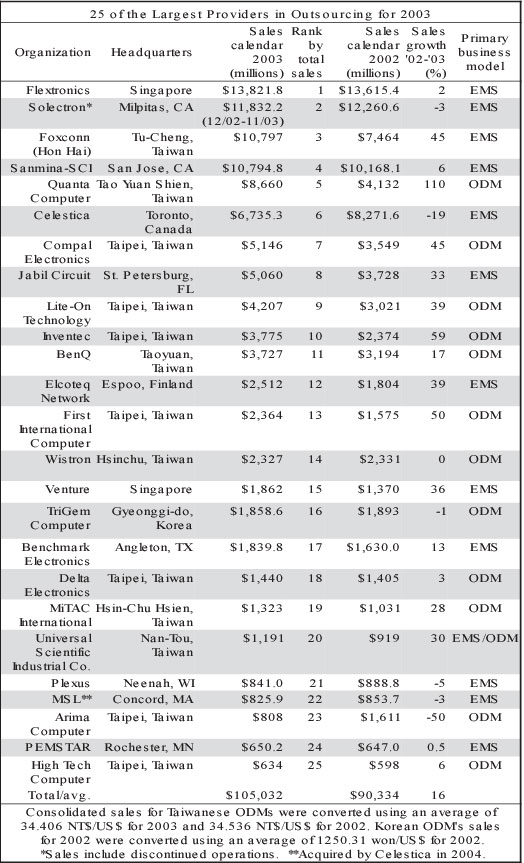

For the first time, MMI has compiled a list of 25 of the largest companies in the outsourcing space (see table below). Last year, these EMS providers and ODMs accounted for sales of $105.0 billion, up by a healthy 16% over 2002. That’s about double the rate of the MMI Top 50™ EMS providers, which increased at an adjusted rate of about 7.9% overall in 2003.

Why did outsourcing sales from this list of 25 companies expand at twice the rate of the Top 50? Even though ODMs represented a minority share of the 2003 outsourcing revenue, they grew fast enough to boost outsourcing sales for the group. Aggregate sales for the 12 ODMs on the list of 25 climbed by an impressive 36% in 2003 (see chart). For at least half the ODMs in this group, 2003 wasn’t a recovery year; it was a boom year. Four ODMs posted growth rates of 45% or better. In contrast, the 13 EMS providers on the list combined for an 8% growth rate in 2003, in line with the Top 50.

High ODM growth rates are a reflection of the product areas in which ODMs specialize. Last year, ODMs benefited from the continued demand for laptop computers, an area they dominate. LCD monitors were hot, and ODMs are major suppliers of displays. What’s more, ODMs have expanded into areas outside the computer field, and some of these new areas such as cell phones augmented sales. ODMs also profited from their ability to manufacture in China during a period in which massive amounts of work were being moved there. OEMs are increasingly inclined to choose predesigned ODM solutions for commodity products.

The growth of ODM outsourcing has meant that ODMs have been taking market share away from the EMS industry. Gone are the days when ODMs were considered too regional and too specialized to be competition for the EMS industry. In 2003, the 12 ODMs on the MMI list combined for $36.3 billion in revenue, or 35% of the total outsourcing sales for the 25 companies. The 13 EMS providers on the list generated collective sales of $68.8 billion, or 65% of the total.

Since the EMS and ODM shares are calculated from a base of $105.0 billion in 2003 sales, these percentages give one an approximation for the EMS/ODM split in the total outsourcing market. Assuming about $95 billion for the EMS market in 2003 and a 65% share for EMS, one comes up with a total outsourcing market size of about $146 billion for 2003. If the total available market in 2003 was $600 to $700 billion, then the outsourcing penetration rate was in the range of 21 to 24%, based on this analysis.

But this analysis is not without uncertainty. For one thing, ODMs sometimes sell products under their own brands. Take Korea’s TriGem Computer. It is a major supplier of PCs to the Korean market. Own-brand sales should not count toward ODM sales in this analysis. Problem is, ODMs do not break out their own-brand sales in their financial reporting.

Although some amount of own-brand sales has crept into this analysis, the list does exclude motherboard manufacturers such as Asustek Computer, where own-brand sales can be significant. Still, if one were able to obtain just the ODM/OEM portion of Asustek’s sales, that portion would likely qualify for this list. While ODM sales may have been inflated somewhat by own-brand sales, on the other side of the ledger the ODM side of this analysis does not count ODM sales contributions from the large motherboard suppliers.

Also note that Universal Scientific Industrial Co. has been treated here as an EMS provider even though the ODM percentage of its sales is increasing.

This analysis became possible after April 30, the deadline for Taiwan-listed companies to report consolidated sales. Consolidated sales in NT$ were converted to US$ using average annual exchange rates for 2003 and 2002 as supplied by the US Federal Reserve system.

It turns out that consolidated sales for Foxconn (Hon Hai Precision Industry) were $297 million higher than estimated by MMI. As a result, Foxconn just edged out Sanmina-SCI for the position as third largest provider in the outsourcing space. MMI also made a minor correction in Foxconn’s 2002 sales previously listed in the March issue.

Based on this new list of outsourcing providers, EMS companies hold down the first four spots in the 2003 hierarchy as in the MMI Top 50. But the fifth spot now goes to an ODM, Quanta Computer. ODMs also occupy the seventh, ninth and tenth positions.

Although Asia gets all the attention, Europe also presents growth potential for EMS providers and ODMs. MHM (Ayr, Scotland), an information services firm, recently singled out ten growth opportunities in Europe encompassing EMS and ODM work.

First and foremost is Eastern Europe, a $10.6-billion opportunity from 2003 to 2006, according to MHM. Naturally, work is expected to be moved from Western to Eastern Europe. But in addition, brand name divestments will arise in Eastern Europe, as will the opportunity to assemble components sourced from China, says MHM. The firm also foresees suppliers adding plants in Eastern Europe as they move farther east over the forecast period.

Within Eastern Europe, ODMs will find a $1.96-billion opportunity from 2003 to 2006, predicts MHM. The firm says top-ten players as well as smaller design houses can participate.

Since a significant amount of in-house manufacturing remains within European OEMs in the communications sector, this sector presents a major source of new business potential. MHM estimates that communications will be worth $4.4 billion in new EMS business over the forecast period. The firm points out that Ericsson has 90% of its manufacturing in Sweden, for example. OEMs with unwanted capacity include Siemens and Alcatel, according to MHM. The firm reports that seven plant divestitures are required within the European Union at present. A major opportunity also involves the design and manufacture of subassemblies in China.

Other segments offer growth potential as well. According to MHM, the consumer EMS business in Europe represents a $2.6-billion opportunity over the forecast period. The firm identifies Philips, Siemens, Thomson, Telfal and Miele in connection with this opportunity.

In the European automotive market, MHM projects $990 million worth of new EMS business from 2003 to 2006. Automotive suppliers such as SVDO, TRW, Valeo, Bosch, Delphi and Kostal are listed as potential customers.

Growth potential also lies in two more segments. The first one, industrial, instrumentation and control, comprises an EMS opportunity with an estimated value of $648 million over the forecast period. This opportunity will go to mid-tier EMS providers with additional outsourcing coming from Agilent, Actaris, Siemens and ABB, according to MHM. The final sector, medical products, represents a $404-million opportunity for mid- and top-tier companies. Medical OEMs in Europe consist of Siemens, Philips, GE and a plethora of smaller, newer companies.

Acquisitions provide still more opportunities to grow in Europe. Mentioned earlier, divestments by EU brand names offer an opportunity that MHM puts at $1.3 to $2.5 billion over the forecast period. The firm cautions that these deals should be done sparingly. Acquisitions of competitors present another source of revenue, valued at $50 to $750 million. MHM lists Zollner, Videoton and Scanfil as examples of attractive domestic players.

Finally, MHM finds an opportunity worth $10 million to $1 billion or more from spinning off divisions of industry companies. The firm believes that industry consolidation went too far and that shareholders could benefit from spinning off non-synergistic units or technologies as demand picks up.

Note that due to overlapping categories in the above analysis, there is double counting in some cases.

MHM estimates that the European market for EMS and ODM work grew 10% in 2003, with major European EMS providers accounting for about $20 billion in revenue. The firm is projecting compound average annual growth of 12% for EMS plus ODM sales in Europe for the period 2003 to 2006.

More information about EMS and ODM opportunities in Europe is available through MHM’s new Information Service. E-mail mike@mhm.info.

As demand picks up in the EMS industry, low-cost Asian sites are seeing more than their fair share of new business. That’s a good thing for EMS providers because higher capacity utilization helps their margins. But an industry consultant warns that busy Asian plants in some cases may not have the resources to ramp new programs as fast as OEMs would like.

“For instance, if the OEM’s program is not a good fit technically, i.e. requires new processes or higher levels of process control, then time to quality production might require considerably more time than scheduled,” said Robert Freid, president of Contract Manufacturing Consultants (Bellevue, WA). “OEMs should take this into consideration when deciding among suppliers.”

Freid believes that smaller programs are more likely to face this problem since major global accounts have the leverage to get resources allocated to them.

TeliaSonera Sweden is acquiring the product portfolio and operation for customer-placed equipment from Flextronics Network Services, a unit of Flextronics (Singapore). This deal chiefly relates to office exchanges and LAN equipment. But the transaction does not include onsite installation and maintenance services that Flextronics provides to TeliaSonera, a leading telecom company in the Nordic and Baltic regions. Indeed, TeliaSonera and Flextronics have signed a five-year supply agreement to expand the scope of that relationship.

The Flextronics operation that TeliaSonera is acquiring involves some 130 Flextronics employees, who will be offered jobs at TeliaSonera Sweden. This activity includes product management, sales support, delivery and technical support.

TeliaSonera says it is making this acquisition to integrate the product portfolio with the rest of TeliaSonera’s product offering. In the past, TeliaSonera has accounted for about 80% of Flextronics’ revenue from this operation.

Under the new five-year agreement, Flextronics Network Services will become the main supplier of onsite installation and maintenance services for TeliaSonera’s fixed network customers. The new agreement expands the relationship between the two parties, both geographically and by volume. Until now, TeliaSonera had bought delivery, installation and maintenance services in select product and geographical areas from Flextronics Network Services.

This relationship stems from Flextronics’ 2001 acquisition of a network installation and maintenance organization along with 5000 employees from the former Swedish telecom company Telia. In 2002, Telia merged with Sonera, a Finnish telecom company.

The original supply agreement with Telia was due to expire at the end of the year.

Three-Five Systems, or TFS (Tempe, AZ), intends to gain 100% ownership of TFS Electronics Manufacturing Services, its Malaysian joint venture with Unico Systems, by buying out Unico’s minority interest. TFS has agreed to purchase Unico’s 40% ownership position in the Penang, Malaysia, operation for 423,000 shares of TFS’s common stock. The transaction is effective immediately subject to certain procedural approvals in Malaysia.

“Our establishment of the TFS-Malaysia joint venture in 2003 was a key step in the transformation of TFS into a global EMS company. It allowed us to establish a strong presence in a key growth area in Asia,” stated Jack Saltich, president and CEO of TFS.

Last year, the TFS joint venture acquired Unico Technology, a privately held EMS company based in Penang (May 2003, p. 4-5). Unico came with an established customer base including Intel.

TFS said the purchase will integrate the Penang operation’s capabilities into TFS’s global manufacturing structure.

Dr. Sam Quah, who served as president of the joint venture, will remain with TFS as president of the company’s Penang, Malaysia, operation.

According to TFS, the dilution of the shares issued for this transaction should be offset by the additional income earned as a result of 100% ownership. TFS’s forecast for 2004 sales will not change since the joint venture was already fully consolidated.

Adeptron Technologies (Markham, Ontario, Canada) has acquired certain operating assets of another Canadian EMS provider, Ottawa-based Prestec Electronics Ltd., from an agent acting on behalf of Prestec’s senior secured creditor. Adeptron bought inventory, capital assets and customer relationships; the purchase price was CDN$2.25 million in cash. Adeptron also hired Prestec’s former work force of about 115 employees.

Purchasing the Ottawa operation has expanded Adeptron’s range of service offerings by adding expertise and equipment in cable and harness assembly, as well as in mid-plane and back-plane assembly and box build. The operation also includes two class-10,000 clean rooms, supporting both optical and medical subassemblies.

According to Adeptron, it has added to its revenue base and gross margins by earning the business of many former Prestec customers. For the period from Feb. 4 to March 31, former Prestec customers accounted for about CDN$1.8 million in Adeptron revenue.

For the March quarter, Adeptron’s sales rose 73% year over year to CDN$5.95 million. The company incurred a net loss of CDN$1.13 million, including one-time expenses of about CDN$350,000 primarily related to the retention of key personnel in the Ottawa operation. US-dollar exchange rate effects and sales mix reduced gross margins.

In connection with the acquisition, the company has decided that it will take actions to reduce its work force.

Adeptron is listed on the Toronto Stock Exchange.

UQM Technologies (Frederick, CO), a developer of alternative energy technologies, has sold the assets of its EMS subsidiary, UQM Electronics (St. Charles, MO), to a new company, CD&M – Electronics.

From the sale, UQM Technologies received $0.9 million in cash and 15% ownership in privately-held CD&M. The purchase price included manufacturing equipment and inventory. The buyer has also entered into a sublease with UQM for the remaining term of the lease on the St. Charles, MO, manufacturing facility, which contains 30,000 ft2 of manufacturing space and 20,000 ft2 for expansion.

CD&M now offers custom design and other engineering services, PCB assembly, box build, and cable and harness assembly. The company positions itself as a contract manufacturer for segments including automotive, Internet, gaming, medical, photographic services, highway construction and printing and graphics.

The primary shareholder in CD&M is Bill Alexander, who owns an electronic calibration service called TICMS in the St. Louis area.

UQM expects to report an operating loss from its discontinued EMS business of $2.6 million for the fiscal year ended March 31, 2004. The company also anticipates a loss on disposal of $0.8 million.

CD&M is restarting operations of the facility after UQM shut it down completely. In January, UQM formalized a plan to sell or close its EMS business. This decision was made six days after UQM lost a lawsuit that it filed against an Ingersoll Rand subsidiary, a former customer of UQM’s EMS operation. The suit sought payment for inventory purchased on behalf of the customer and lost profits on a cancelled production order.

New programs…Flextronics’ Product Introduction Center in San Jose, CA, will assemble fuel cells for MTI MicroFuel Cells (Albany, NY), a subsidiary of Mechanical Technology Inc. MTI Micro’s initial direct methanol fuel cell system is intended for use in industrial handheld electronic OEM devices. In parallel with this initial product ramp, MTI Micro and Flextronics’ design center in Dallas, TX, will work together under a US Department of Energy contract recently awarded to MTI Micro. The cost-shared development contract will provide $3 million in DOE funding to be matched by MTI Micro….Elcoteq Network (Espoo, Finland) has started production at its plant in Shenzhen, China, for Huawei, a major Chinese supplier of communications equipment….IBM, Motorola, Hitachi Global Storage and Fluke were among PEMSTAR (Rochester, MN) customers initiating new projects during the March quarter. Also, PEMSTAR co-designed, developed and is manufacturing an integrated cell phone and personal organizer created for the visually impaired. Developed for Netherlands-based ALVA B.V., this product, the ALVA MPO 5500, has won three awards for product design. According to PEMSTAR, its ODM platform reduced costs and risks in the R&D stage of the product and, at the same time, shortened time to market....Supercomputer OEM Cray (Seattle, WA) has selected Vanguard EMS (Beaverton, OR) to manufacture and test electronic assemblies for the Cray XD1 high-performance computing system....Lockheed Martin has awarded LaBarge (St. Louis, MO) a $1-million contract to produce card assemblies for ground-based radar.

This month, MC Assembly (Melbourne, FL) started production in Zacatecas, Mexico, which gives the MMI Top 50 EMS provider a low-cost offering in not one, but two geographies. In December 2003, MC Assembly began shipping product from a joint-venture facility in Wuxi, China.

At present, the provider is operating from a temporary facility of 15,000 ft2 in Zacatecas, which is about 3 ½ hours from Guadalajara. Next door to the temporary facility, a new 54,000-ft2 plant is being built and is due to be ready in about three months. MC Assembly is starting out in Mexico with two SMT lines and plans to add a third. Current staffing in Mexico stands at about 40 employees, and the company expects to increase that work force to 50 or 60 people within the next 30 days or so. The provider expects that mostly industrial products will be produced in the Mexican operation.

MC Assembly looked at a lot of locations in Mexico, including such well-known ones as Guadalajara, Chihuahua and Monterrey as well as the border towns. Zacatecas came out on top. “The labor rate was a little less expensive there, but yet the area had a pretty large pool of employees. The population is pretty dense in and around that area,” said Tom Wienckoski, president of MC Assembly.

As a medium-volume, medium-to-high mix provider, MC Assembly wants to stay out of the high-volume arena. “But we feel that there’s a pretty good market these days for companies that need a low-cost supplier on some percentage of their products,” said Wienckoski. In such cases, “most of their products aren’t applicable for the low-cost regions because of design, volumes, changes, schedules, whatever the case may be,” he added.

For the most part, programs going to Mexico and China will consist of new business rather than existing work transferred from Florida, according to Wienckoski.

MC Assembly is projecting that its domestic sales for 2004, excluding China and Mexico, will come in at around $200 million. That’s up from $142 million in 2003. Domestic operations are comprised of three manufacturing facilities and a materials/logistics center in Florida. The company employs just over 1100 people.

When the Mexico facility is completed, MC Assembly will have about 250,000 ft2 in Florida, 40,000 ft2 in China and the aforementioned 54,000 ft2 in Mexico.

Sparton (Jackson, MI) intends to open a facility of about 55,000 ft2 in Ho Chi Minh City, Viet Nam, and as a result will become the first US-owned EMS provider in Vietnam. Sparton’s board has approved an expenditure of up to $7 million for this project, including land, building and initial operating expenses. Construction will start next month, and the company plans to open the facility, subject to the rainy season, in January or February 2005. The operation will start out with about 75 people.

Why did Sparton choose Vietnam when China is so popular now? For one thing, Vietnam’s population has the highest percentage of well-educated people compared with other Asian countries that Sparton studied. “In Ho Chi Minh City, a city of 10 million people, it’s very easy to hire someone who has a masters degree in electrical engineering, a Ph.D. degree in electrical engineering,” said David Hockenbrocht, president and CEO of Sparton. In addition, the Vietnamese would rather work for an American company, he observed.

Sparton also found Vietnam’s legal system an advantage. As a former French colony, Vietnam has patterned its legal system after the French. So the government, while communist, “has very great respect for individual rights, private ownership, private capital investment and intellectual property,” said Hockenbrocht.

Ease of doing business in Vietnam was another factor in Sparton’s decision. “We discovered that the Vietnamese government had done everything to make it attractive in all regards for Western capital to go to Vietnam,” he said.

When considering Vietnam, OEMs typically want to know if the wage base there is less than in China. “If you compared Ho Chi Minh City or Hanoi to Beijing or Guangzhou, you would find it to be less for a comparable technically trained or executive-level person,” said Hockenbrocht.

But Vietnam does not have a materials infrastructure. So Sparton will use its international procurement office, opened in Singapore in December, to purchase materials for the Vietnam operation.

The Vietnam site will be Sparton’s seventh manufacturing location, but its first outside North America. Sparton focuses on high mix, low-to-medium volume in highly regulated businesses.

“Most of the business that we will be receiving in Vietnam over the next two or three years is new business that we do not already have, some from existing customers and some from new customers,” said Hockenbrocht.

Expanding in Thailand…Benchmark Electronics (Angleton, TX) plans to open its second manufacturing site in Thailand and have it fully operational by Q3. Located in Nakorn Rachasima (Korat), Thailand, the site offers 125,000 ft2 of manufacturing space with an additional 55,000 ft2 available for future expansion. The provider originally acquired the facility as part of ACT Manufacturing assets that Benchmark purchased in 2002. In addition, Benchmark reports it has been expanding its engineering design team in Asia in response to increased demand for engineering services….SMTEK International (Moorpark, CA) has begun construction to double capacity at its manufacturing facility in Ayutthaya, Thailand. The company has also signed an agreement to purchase the facility. This additional capacity is expected to be operational in October. SMTEK’s Thai subsidiary has obtained a $1.7-million credit line to finance the real estate purchase, expansion costs, and working capital needs there.

Entering Eastern Europe…PEM-STAR has taken majority ownership in a joint-venture start-up of a production facility in Brasov, Romania. Production is expected to begin in the June quarter. The provider said it made a very small investment to start that facility.

Adding capacity in Mexico…EPIC Technologies recently added two SMT lines to its 70,000-ft2 facility in Juarez, Mexico. The operation is up to seven SMT lines, has been on a 24/7 schedule since January, and has grown to over 600 people. EPIC (Rochester Hills, MI) is the parent company.

Integrated Microelectronics, Inc., or IMI (Laguna, Philippines), has entered into a strategic alliance with Pensar Electronic Solutions (Appleton, WI). The alliance will expand IMI’s reach in the North American OEM market, while providing Pensar with a high-volume solution in Asia.

Pensar, which specializes in low- to medium-volume, high-mix manufacturing, will be able to move high-volume work to IMI as the need arises. IMI has already started its first qualification run for a customer that started with Pensar.

Pensar’s position in industrial electronics aligns with IMI’s strength in the industrial segment. Both companies also engage in the medical market, but IMI’s exposure has been limited to Japanese companies. Pensar will give IMI a gateway to the US medical market for noninvasive products.

IMI believes in making alliances. “Especially for the size of IMI, I think it’s a good method and strategy,” said Arthur Tan, president and CEO of IMI. “There will always be a lot of companies who need to use a localized NPI center. We’ll never be able to put one in all the geographical areas. Forging these alliances also enables those NPI centers to remain in the loop with their customer base and not lose it to the other CMs in Asia.”

Other IMI alliances include one with ISIS Surface Mounting (San Jose, CA) and another with Hansa-tech (Cambridge, UK). The ISIS alliance is coming to an end in light of Elcoteq acquiring a 20% stake in ISIS (Nov. 2003, p. 4-5). IMI is in negotiations with a Southern California operation to serve as its new partner on the West Coast. Also, IMI is exploring the possibility of an alliance in the US Southeast.

IMI structures its alliances as a win-win for both sides. When a program is moved from a partner to IMI, there are several ways for the partner to participate. One option is to have the partner handle program management. “Even if the customer doesn’t pay for the project management side of it, IMI will still have that expense any way. So we’ll go ahead and share that with Pensar,” said Tan.

This year, IMI is projecting sales growth of 17 to 20% and bottom-line growth of 50%. In 2003, IMI reported sales of $94.0 million.

Pensar regained its independence last year when Pensar management bought back the operation from SMTC, which has acquired it in 2000.

AeTec, a privately-held EMS provider based in Tempe, AZ, brought in record Q1 bookings that were up over 300% from the year-earlier quarter. The company attributed much of this growth to several new contracts totaling over $7 million in new business from Roper Scientific (Tuscon, AZ), a maker of high-performance digital imaging and spectroscopy systems. Roper has contracted AeTec to build the electronics for Roper’s scientific cameras.

Moreover, a surge of new contracts is fueling annual growth, and AeTec is projecting that 2004 sales will increase by 215% over last year. The provider also expects to expand its work force of about 90 employees by over 15%.

AeTec will gain new business from a major OEM that has decided to transfer internal manufacturing to the provider. “We have been selected. It’s just a matter of the details,” said Dan Stuber, AeTec president and CEO.

The company attributes this explosive growth to its ability to better address the needs of its customers. “We focus on becoming part of their organization, not just a transactional service provider,” said Stuber.

Offering both domestic and offshore manufacturing, AeTec operates about 50,000 ft2 of manufacturing facilities between its Tempe and Costa Rica locations. “Unlike most competitors that have offshore factories, we don’t require that the product volume is high before we take it offshore,” said Stuber. All that AeTec requires is a stable product, somewhat predictable volume, and an annual purchase order.

Corrected report…Last month’s news section on page 6 contained an inaccurate report of the number of people to be employed in Jabil’s new EMS facility in Memphis,TN. Based on information received after the April deadline, the new facility, which replaces an existing plant, will increase staffing by 200 people or so.

After longtime immersion in the EMS industry, one tends to think of manufacturing as an either/or proposition. An OEM either manufactures in house or outsources production. But two professors recently highlighted a third option – pooling manufacturing resources among OEMs.

At first, this writer was puzzled when introduced to the concept of pooling. Why in the world would OEMs want to pool production capacity? Cooperating with a competitor would seem to violate a basic tenet of the electronics industry.

Yet these two professors, Erica Plambeck from the Stanford Graduate School of Business and Terry Taylor from Columbia University, argue that pooling resources among OEMs is sometimes a better strategy than outsourcing. What’s more, after analyzing the results of OEM outsourcing, the researchers conclude that pooling capacity encourages OEMs to innovate. Pooling reduces production expenses, and the savings, they believe, give OEMs incentive to invest more in innovation. Such innovation includes product variations that OEMs otherwise might not undertake. According to a statement released earlier in the year, the researchers plan to publish these and other findings in a series of papers.

Proponents of outsourcing would point out that contract manufacturing also reduces the OEM’s production costs, thereby promoting investment in the development of new products. And these benefits are achieved without getting in bed with a competitor.

Although the concept of pooling may seem foreign to the EMS community, pooling does take place. Think about joint ventures such as the well-publicized arrangement between 3Com and Huawei Technologies, a Chinese maker of communications equipment. Through the venture, 3Com gains access to Huawei’s enterprise networking business assets, including production in China. The venture provides 3Com with a high-end extension to its product line. So here is an OEM, 3Com, that utilizes both outsourcing and pooling.

Also consider the Sony Ericsson joint venture in mobile phones and a similar venture announced by Alcatel and TCL. Consumer electronics is another area where pooling can be applied. Pooling occurs in the ODM business as well when ODMs sell products under their own brand name.

Note that pooling and EMS are not mutually exclusive. Sony Ericsson, for example, utilizes outsourcing, and the Alcatel-TCL venture is expected to engage in the practice.

While pooling does not conform to the classic outsourcing model, it is a reality. How big a reality becomes the next question. Professors Plambeck and Taylor assert that the OEM-to-OEM outsourcing market exceeded the contract manufacturing market in 2002. They say OEM-to-OEM pooling amounted to about $115 billion in 2002. If this number is anywhere close, it makes for a powerful statement, because pooling would then take a chunk of the total outsourcing market off the table for EMS providers.

In some cases, it makes sense to pool manufacturing resources, such as when OEMs have complementary product lines. For EMS providers, pooling can be a hindrance or a help.