![]()

Vol. 10, No. 11: November 2000

Cover story

No. 1 Solectron Bids for No. 6 NatSteel Electronics

Emerging Players

A Second Wave of Up-and-Comers

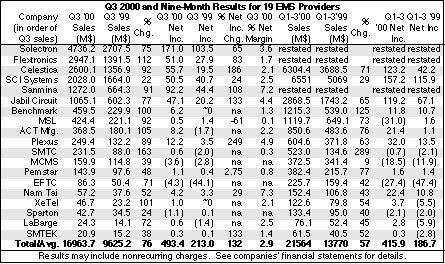

Market Data

Enclosure Side

Electromechanical Space Attracting Variety of Buyers

SCI Acquires Second Enclosure Supplier

NEL Buys Piece of Enclosure Company

Another Consolidator: Trend Technologies

Another buyer in the enclosure space

Flextronics in Deal with Siemens

Varian Expands Contract Mfg. Business

On Oct. 31, Solectron, the world's largest EMS provider, said it will make a cash offer for Singapore's NatSteel Electronics Ltd. (NEL), the sixth largest provider overall and the largest based in Asia.

Solectron is offering $4.53 per share for NEL, which has about 534 million diluted shares outstanding. That price equates to a potential deal value of some $2.4 billion.

The deal underscores the importance of Asia as an emerging growth market for outsourcing. The offer also highlights a recent trend of investing in Asian capacity. In last few months a growing number of EMS providers have decided to either acquire EMS operations in Asia or put up their own plants there (Oct, p. 11-12; Aug., p. 5-6, p. 8-9).

"The trend of original equipment manufacturers to outsource their manufacturing and supply-chain needs is now emerging in the Asia/Pacific region," states Koichi Nishimura, Solectron chairman, president and CEO. "By acquiring NatSteel Electronics, we at Solectron would further strengthen our presence in this region, expand our capacity and solidify our leadership role in bringing the benefits of outsourcing to companies in Asia."

This announcement follows on the heels of Sony's move to divest facilities in Japan and Taiwan to Solectron (Oct. p. 5-6). In a conference call with analysts in Singapore, Nishimura said he thinks that with NEL's high-volume capability the Sony partnership "may be a real opportunity for all three of us" along with some of the Japanese OEMs.

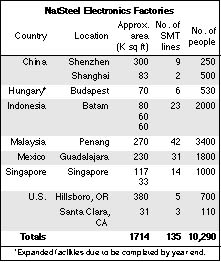

To bolster Solectron's presence in Asia, the company will gain NEL facilities in Shanghai and Shenzhen, China; three buildings on the island of Batam in Indonesia; a factory in Penang, Malaysia; and two facilities in Singapore. In Asia, NEL has one million ft2 of factory space, 90 SMT lines and 7150 employees in EMS (see table below). Within China in particular, NEL's newly opened Shenzhen facility (Oct. , p. 11) will give Solectron a presence in the country's industrialized southern region.

Elsewhere, NEL operates in the US with two sites as well as in Mexico and Hungary. NEL lists total factory space at 1.7 million ft2, which presumably does not include an expansion project underway in Hungary.

This deal also signifies something else: Consolidation is reaching all levels of the EMS industry. Small and midsize CMs are no longer the only players being targeted for acquisition. But it stands to reason that as the tier-one providers grow ever larger, so too does the size of their appetite for acquisitions. NEL is the highest ranked provider to be acquired so far.

Solectron's offer for NEL came about because NEL's largest shareholder, NatSteel Ltd., decided to entertain bids for its 33% interest in NEL. Competing against one or more unnamed parties, Solectron won the bidding contest for NatSteel Ltd.'s shares of NEL. Furthermore, Solectron has received commitments from NatSteel Ltd. and other major shareholders to tender shares representing 43% of NEL's common stock. These other shareholders consist of key members of NEL's management team and Temasek Capital.

Solectron's offer is contingent on shareholders tendering more than 50% of NEL's shares on a fully diluted basis. Other conditions include NatSteel Ltd. shareholders' approval of the sale of NEL shares to Solectron and the completion of regulatory reviews and approvals. Solectron hopes to complete the offer by the end of December.

The offering price of $4.53 or S$7.95 represents a 74% premium over NEL's closing share price on Oct. 27, the last closing date before the offer was announced. Compared with a pre-speculation closing price on Oct. 19, the offer amounts to a 156% or 157% premium, depending on the source.

NatSteel Ltd. says the proposed sale of its NEL stake is in line with its restructuring goals, one of which is to focus management resources on core steel and industrial businesses. Another objective is to maximize value to shareholders by unlocking the value of constituent businesses. One of those businesses is NatSteel Broadway, a plastics and metal supplier that also does EMS work.

Solectron says it was attracted to NEL by its strong management team, led by CEO Chester Lin, and by its complementary business strategy. According to both companies, that management team will remain in place.

"Chester and his team at NatSteel Electronics have an excellent track record in this industry, and their end-to-end supply-chain business strategy is very consistent with our strategy at Solectron," states Nishimura.

Since early 1999, NEL has been transforming itself from an Asia-based PCB assembler to a global supply-chain service provider. That has meant, of course, bringing in box-build work. For example, NEL now does high-level system assembly for communication switch products in an Oregon facility acquired from NEC (Feb., p. 11). The company has outfitted at least five other plants with box-build capability. CEO Chester Lin told US analysts that he expects box build to be 10% of NEL's business this year. He said the box build share would probably increase to around 35% in 2001.

NEL has also used other means to expand on the box-build side. Last year, the company formed a joint venture with Pacific City International (PCI), an IT distributor in China, to serve that market with a model for build to order (BTO) and configure to order (CTO). (See Dec. '99, p. 5.) Then there is the LiteOn Enclosure joint venture that NEL has formed with the LiteOn Group of Taiwan. This joint venture will give NEL global enclosure capabilities for fulfilling box-build orders (see article on p. 8). NEL expects the venture to help bring in new box-build customers.

Building and perhaps designing enclosures is one thing. Product development is quite another. On the development end of the design-to-market supply chain, NEL has gained capabilities as well. The company has formed ODM (original design manufacturer) partnerships with a number of companies. Often cemented with an equity stake, these partnerships provide NEC with product development expertise that it would not otherwise have. The most recent of these has been struck with ST Electronics Ltd, a developer of complex electronic systems. Other ODM partners include Shuttle, Eumitcom and Accton (July '99, p. 5; Oct. '99, p. 3; Dec. '99, p. 5). In addition, NEL has obtained engineering capability through its stake in U.S. Robotics, the analog modem business that 3Com spun off. What's more, NEL is planning a Q4 alliance with a large medical concern for medical test equipment R&D.

NEL's ODM alliances will "enhance our ability to provide some level of ODM design solution that is also going to enhance our total service offering," said Solectron CFO Susan Wang in the conference call with US analysts.

NEL has also sought access to technology on the chip level. The company has made two investments in chip development efforts including US-based Metron Communications. Metron is working on communication chip sets for wireless Internet access.

On the distribution and fulfillment side of the supply chain, NEL has been active as well. Other than the joint venture with Chinese distributor PCI, perhaps the most visible effort in this area has been NEL's ownership stake in ECS Holdings, which controls three IT distributors in Asia (Nov. '98, p. 9-10).

Wang said the PCI and ECS affiliations would give Solectron another opportunity to supply the distribution channel with products on a BTO and CTO basis. The company tried that with Ingram Micro, but the Ingram Micro alliance has not generated any programs worth disclosing.

Interestingly, Solectron also values NEL for its traditional strength in high-velocity, low-cost production. "I would venture to say that their competitive position in this high-velocity market has been superior even to Solectron, which has up to now focused more at the medium-mix, medium-volume [and] high-mix, low-volume end of the market...," said Wang. She also pointed out, "The high-velocity, high-volume value proposition that Solectron has today is limited in capacity."

In addition, Wang said NEL's supplier network in Asia will add to Solectron's supply chain capability.

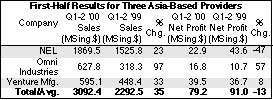

NEL increased its sales in the first half of the year, as did two other Asia-based CMs (see table, below). Of the company's S$1.87 billion (about $1.07 billion) in first-half sales, 53% came from Apple. NEL is well known as a supplier of motherboards for Apple's iMac PC. Hewlett-Packard represented the second largest portion of NEL's sales at 18%. IBM and the distribution company ECS were next at 8% apiece, followed by NEC and Compaq with 4% and 3% respectively. Other OEM customers include U.S. Robotics, Accton, 3Com, Intel, Osram/Siemens and Metricom.

In the first-half of 2000, NEL derived 65% of sales from motherboards plus 15% from PC peripherals. Disk drives contributed 7% of sales as did the combined category of office equipment and others. Although communications only amounted to 6% of first-half sales, NEL has taken steps to expand its communications business. The NEC facility acquisition mentioned earlier serves as one example. Another is U.S. Robotics, which NEL as part owner is supplying with modem products. According to NEL's Chester Lin, the company projects that communications will account for about 35% of sales next year.

For 1999, NEL's sales totaled S$3.23 billion ($1.9 billion).

Last month, NEL lowered its sales target for the current year by about 15% from its original expectation of about S$5 billion in sales. NEL cited a slowdown in PC manufacturing demand mitigated by new business from alliances and acquisitions. However, the company expects profitability for the second half of 2000 to be close to its original forecast, which called for profitability to be no less than that achieved for the same period last year.

"The PC business seems to be a little bit soft, and as a result NEL [stock] has been batted down a bit in the marketplace. We believe this is a short-term cyclical situation," Solectron's Wang told US analysts. She said business opportunities for both companies are such that it "would be quite possible" to use any excess NEL capacity that results from a softening in PC demand.

Meanwhile, NEL's Lin estimated that NEL's capacity utilization now stands at about 85% to 90% overall.

Based on this deal and the divestiture agreement with Sony, Solectron expects sales for fiscal 2001 to exceed $23 billion, up from previous guidance that sales would top $20 billion. The provider has also updated guidance for EPS. Solectron now anticipates diluted EPS ranging from 99 cents to $1.02 and cash EPS, excluding goodwill amortization and other intangible costs, of $1.22 to $1.25. Previous guidance called for diluted EPS of $1.12 to $1.15 and cash EPS of $1.18 to $1.21.

In connection with the NEL acquisition, Solectron intends to raise about $2.5 billion from concurrent public offerings of its common stock and Liquid Yield Option notes. The company says this financing will replenish cash reserves that will be used for the acquisition.

As speculation in Singapore swirls around possible acquisitions of other Asian contract manufacturers, PCI Ltd. has emerged as one potential takeover target. PCI's largest shareholder, Chuan Hup Holdings Ltd., has engaged ING Barings South East Asia Ltd. to act as financial adviser for a review of Chuan Hup's interest in PCI. Chuan Hup holds 32.9% of PCI's issued shares.

With a specialty in LCDs and LCD modules, PCI manufactures semi-finished and finished products such as cordless telephones, point of sales terminals, portable bar code readers and modem cards. Major customers include Siemens, Motorola, Xerox, Tecom, Roche, Qualcomm, Lucent, Philips and Robert Bosch. For fiscal 2000 ended June 30, PCI reported sales of S$185.0 million, of which S$149.4 million came from EMS.

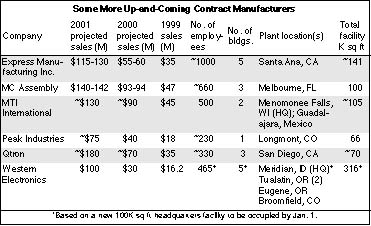

Last month, MMI came up with seven contract manufactures that are on track to reach $100 million this year. After the article appeared, the newsletter was contacted by four other companies that believe they too should be considered up-and-comers. And they certainly have a point. Although none of them will hit $100 million this year, they are all growing at high rates. So in the interest of providing OEMs with still more choices, MMI presents a group of what could be considered a second wave of up-and-comers. This group also includes two additional fast growers, Express Manufacturing and Qtron, that were only mentioned briefly last month.

All six of these privately held companies generated less than $50 million in sales last year. Yet four of them project 2001 sales ranging from $115 million to about $180 million. Two others, with 1999 sales of less than $20 million, forecast that their 2000 sales with hit either $100 million or a $100-million run rate next year (see table below). How are these companies able to grow so fast? Each one has its own formula.

Express Manufacturing, Inc. EMI considers itself to be the largest consignment house in the US. If all of EMI's current business were converted to turnkey, the company would have $600 million in revenue, says EMI. But over the last two years or so, EMI has been working to change its business model from consignment to largely turnkey (July, '99, p. 7-8). In 1999, only 4% of sales came from turnkey work. This year, EMI expects turnkey sales to account for about 35 to 40% of revenue. The boost in turnkey sales comes from new customers, which have awarded five major turnkey programs to EMI (Oct., p. 5). For 2001, the CM projects that about 70 to 75% of sales will be turnkey. Since making the move to turnkey, EMI's reach has gone well beyond its traditional base in Southern California.

Because EMI is new to turnkey, people have questioned its supply-chain capability. "They think our supplier relationships are all new," says Luke Kensen, EMI's director of business development. But he adds, "We've had relationships with suppliers from day one." EMI has worked with distributors who have referred clients to EMI for manufacturing. "So the supply chain and our buying power are very much in place," declares Kensen.

EMI prides itself on its ability to serve customers as a long-term sup-plier. Most of its large customers have been with EMI for 14 years or more.

Customers include such names as Gateway 2000, Pairgain Technologies and Xerox. But EMI also caters to lesser known OEMs. Among them is Advanced Energy Inc. of Fort Collins, CO.

MC Assembly. This medium-volume, medium-mix provider does a lot of high-end board assembly including BGAs, microBGAs, fine pitch down to 15 mils and double-sided active SMT. As a result, next year's capital equipment budget, estimated at $7 to $7.5 million, will not only cover SMT lines but also such items as a 3D laminography system and optical inspection equipment. "We will continue to invest in technology," says Tom Wienckoski, MC Assembly's president and cofounder.

He positions the company as providing customer service and flexibility, while offering tier-one capabilities. If at the end of a week a customer suddenly needs 500 boards by Tuesday, "we'll work Saturday, Sunday - whatever it takes to get the job done," says Wienckoski. He asserts that a $15-million-a-year customer would not receive this attention from a top-tier provider.

"Most of our growth is coming from existing business," reports Wienckoski. MC Assembly supports 14 to 15 customers, with two to three new accounts added per year. "As they grow, we take advantage of the opportunities," he says.

Customers include International Gaming Technology (Reno, NV), Pliant Systems (Research Triangle Park, NC) and Nortel (Boca Raton, FL). Wienckoski estimates about 45 to 50% of sales come from telecom/datacom, followed by the industrial market at 25% of sales and medical at 20%.

MC assembly is "very, very healthy financially," says Wienckoski. "We're in a good position to grow with our customers. All we have to do is add people and equipment."

The company also expects to lease another 103,000 ft2 in Melbourne, FL. After moving out of one of its existing buildings, the provider will have a total of 183,000 ft2 next year.

MTI International. Primarily Midwest-based, MTI sees its growth coming from telecom customers, which represent over 60% of its business. Medical and industrial make up the balance.

"We tend to ride customers growing very rapidly or have the opportunity to grow very rapidly," says Greg Martinek, MTI's president and CEO. He adds, "The idea is greater penetration in existing customers versus adding several new customers." Each year, MTI does add new customers, but is selective.

Martinek does not try to set MTI apart from other providers. "I don't think we have the ability to differentiate in our industry. What we sell is a commodity," he says.

"Quality, service and technology are givens," adds Martinek. "I think the only way...to differentiate yourself is how you execute for your customers."

Still, MTI has some uncommon attributes. For one thing, it maintains a hybrid circuit business, which until 1996 was its primary line of work. Hybrids are formed from ceramic substrates that are deposited with thick- or thin-film conductors. Though the hybrid business now amounts to less than 15% of MTI's sales, Martinek says "it opens doors for us where possibly we would be just another contract assembler."

Another difference is MTI's facility in Guadalajara, Mexico. It is unusual for a provider of MTI's size to have a facility in Mexico, especially in Guadalajara where the largest providers have congregated.

Yet another unusual trait is MTI's status as certified minority-owned business.

Peak Industries. From its beginning in 1996, Peak has focused on electromechanical assembly and finished product manufacturing. Indeed, 95% of Peak's revenues come from box-build activities. To act as a one-stop CM, Peak has expanded its supply base and added PCB assembly and test as well as system test.

"Peak Industries is the first of a new breed of CM that has made complex electromechanical assembly its core business. We didn't expand out of a competence in enclosures, cables or PCAs. We build products, much like an OEM would, with special focus on supply chain management, quality systems and fulfillment services," says Mark Hopkins, Peak's president, CEO and founder. "Our PCA capability has been tuned to support the needs of a box-build project whose volume and complexity make it a good fit for US-based production. There is currently a tremendous demand for this manufacturing service model."

To illustrate the product complexity that is Peak's forte, consider the following examples. Peak manufactures a robot used in DNA sequencers, a protein analyzer, a cell phone test system and a blood coagulation analyzer.

The company serves the medical, telecom, instrumentation and computer/networking segments. Customers include Agilent, Applied Biosystems, HP, KLA Tencor and US Surgical. In addition, Peak has begun shipments for Carrier Access and 3Com.

In Longmont, CO, Peak just occupied a 20,000-ft2 expansion of its facility, now at 66,000 ft2. What's more, the company plans to complete construction of an adjacent 45,000-ft2 facility in August, 2001.

Peak has grown at a compound annual rate of 110% over the past four years. The company projects that it will reach a $100-million run rate by Q4 2001.

Qtron. This San-Diego, CA-based CM is forecasting that its business will more than double next year to about $180 million. As a result, Qtron will nearly triple its manufacturing space in 2001. The company has just announced that it will relocate from three buildings totaling about 70,000 ft2 to a campus setting of about 200,000 ft2, also in San Diego. Qtron is taking two buildings with an option on a third, which would bring to the total to about 270,000 ft2. The provider expects to complete its move to the new facilities by about the middle of next year.

"I believe we're the leading guy in San Diego, most definitely by size, revenue, technology, capability, people," declares Lynn Brock, Qtron's president and CEO. He says the new facilities will take Qtron to the level of a national player.

Qtron's growth reflects a strategy that emphasizes RF. "We started out with a strategy about a year and half ago to focus on RF, RF wireless and that kind of technology," says Brock. "We are booking business all the way to Vancouver, British Columbia, with up-and-coming companies that utilize that technology."

The company's San Diego location has given Qtron an advantage for pursuing RF type business. "San Diego is an emerging hub for start-ups in the wireless world," observes Brock. Unlike their forbearers, these start-ups outsource manufacturing.

About 70% of Qtron's business stems from RF/RF wireless type products.

Qtron is seeing more than 100% sequential growth in its Q4 revenue. So the company is working 24-7, has added three SMT lines in the last two months and purchased two flying probe testers. Brock reports that Qtron's original investors "are continuing to support us and give us what we need for growth."

Western Electronics. WE is a full-service provider whose internal capabilities extend beyond the typical offerings of PCBA, board test, repair, box build, final test and drop shipping. They also include molded cabling, wire harnesses, finishing and EMI/RFI shielding. In fact, WE is one of the rare providers that can create shielding by vacuum metallization. This capability combined with painting, powder-coating and other finishing services set WE apart from others in the industry.

Products manufactured by WE include video projection equipment, global positioning devices, print servers, networking devices, medical equipment, ESD detection devices, label printing equipment and digital recorders.

Unlike the preceding up-and-comers, WE has used acquisitions to add capabilities. Earlier this year, WE acquired finishing capabilities when it picked up Strategic Finishing of Tualatin, OR, in the Portland area. Then in September, WE purchased SurMounTek, a quick-turn CM in Broomfield, CO. Increasing WE's PCBA capacity, this acquisition also improved its ability to provide design-for-test (DFT) services during prototyping. In addition, WE is looking to acquire a sheet-metal fabrication house to support future growth.

Currently based in Garden City, ID, WE is constructing a 100,000-ft2 headquarters facility in Meridian, ID. The company plans to consolidate its Garden City and Nampa operations into the new facility, which is expected to be finished by Christmas. Initially, the new site will employ 200 people, up from the present Idaho work force of 130. What's more, WE recently opened a 60,000-ft2 facility in Tualatin for final assembly and test.

WE has introduced a concept called F.A.S.T. Centers (Final Assembly, Sales and Technical Support). If an opportunity warrants it, WE will set up a center near a partner's location to perform final assembly and test. These centers can also incorporate other services such as DFM, DFT and prototyping.

Last year, a group led by DBSI purchased the assets and liabilities of Western Electronics. DBSI became majority owner.

Editor's note: The above companies are not intended to represent a complete list of fast-growing CMs.

As the worldwide EMS market continues on a trajectory of unabated growth, two firms continue present differing estimates of market size.

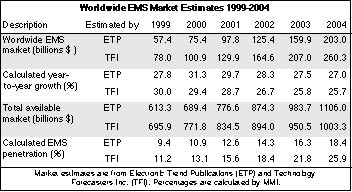

According to a new report from Electronic Trend Publications (ETP San Jose, CA), the worldwide market for electronics manufacturing services is on track to reach $75.4 billion in sales this year, up 31.3% from $57.4 billion in 1999. Entitled The Worldwide Contract Electronics Manufacturing Services Market, 7th Edition, the report forecasts an EMS market size of $203.0 billion in 2004 (see table, below). This figure translates into a compound annual growth rate of 28.7% over the period 1999-2004.

"This industry shows no signs of letting up its frenetic pace of growth," states Randall Sherman, principal analyst for the report. "OEMs across the entire spectrum of electronic products are moving to the contract manufacturing model." ETP predicts the EMS industry, barring a major economic downturn, will maintain high growth through 2004.

Another long-time source of EMS market research, Technology Forecasters Inc., (TFI Alameda, CA), also forecasts rapid expansion for the EMS industry. But as has been the case in the past, TFI's projections for EMS market size are higher than those of ETP (Nov., '99, p. 2; Oct. '99, p. 4). TFI puts this year's market at $100.9 billion, which represents some 29.4% growth over TFI's 1999 market estimate of $78.0 billion (see table). The firm updated its market numbers in August and will be including more detail in its new Quarterly Forum for Electronics Manufacturing Outsourcing and Supply Chain.

The differences in market size estimates may have something to do with the definitions used by both companies. "For Japanese OEMs, we are counting subsidiaries and keiretsu members as contract manufacturers, because the decision still was to delegate manufacturing to another company, albeit closely related, for lower-cost assembly," says Pamela Gordon, president of TFI. In contrast, ETP considers assembly by keiretsu members as OEM production.

Despite any differences in methodology, the annual growth rates projected by each firm are not far apart. For the years 1999 through 2004, ETP's annual rates range from 27.0% to 31.3%, while TFI's span from 25.7% to 30.0% (table). What's more, rates for two firms differ by no more than 2.2% in any given year. Both firms also predict a gradual decline in growth rates. For ETP, this decline is expected to begin in 2001, while TFI's projections show it starting a year earlier.

The total available assembly market, of course, is not growing nearly as fast as the EMS segment. Another ETP report, The Worldwide Electronics Assembly Market, projects that the overall assembly market will expand at a compound annual rate of 12.5%, reaching $1106 billion in 2004 from $613 billion in 1999 (table). TFI has also forecasted values for the total available market. TFI's TAM, which represents cost of goods sold, starts out somewhat higher at $696 billion for 1999 and ends up at $1003 billion in 2004.

Dividing EMS market value by total available market size, one can calculate the EMS industry's market penetration. For 2000, calculated penetration values from ETP and TFI data are 10.9% and 13.1% respectively (table). These values are below some penetration estimates that have been cited.

But analysis in the ETP assembly market report shows that the outsourced share of the TAM is actually higher. This report introduces the concept of OEM-to-OEM outsourcing, by which computer OEMs, for example, source standard board-level products such as CPU modules or boards, memory modules, and graphics and networking cards. ETP estimates that in 1999 OEM-to-OEM outsourcing exceeded the value of outsourced work done by EMS providers. When these two outsourcing segments are combined, ETP finds that 25% of the worldwide assembly market was outsourced in 1999. The ETP assembly report further estimates that the outsourced share will expand to 38% in 2004.

Within the EMS market segment, box assembly revenue will grow faster than PCB assembly sales over the period 1999 to 2004, according to ETP's EMS report. The compound annual growth rate for box build is projected at 34.9% versus 25.7% for PCBA. For 1999, ETP estimates $17.0 billion in revenue, or 29.7% of the EMS market, came from box build. Five years later in 2004, box build sales are expected to hit $76.1 billion, or 37.5% of the market.

According to ETP's EMS market study, communications equipment will become the leading market segment for EMS, both in total revenue and in growth rate. The study projects that the communications share of the EMS market will increase from 34% in 1999 to 49% in 2004.

For more information, contact Electronic Trend Publications at (408) 369-7000 and Technology Forecasters at (510) 747-1900. Or see www.electronictrendpubs.com and www.techforecasters.com.

Technology Forecasters Inc. (TFI) reports that since August merger and acquisition activity within the EMS industry has been moving in a new direction. In the past two years, TFI data show that takeovers of divested OEM facili-ties equalled (1998) or exceeded (1999) acquisitions of EMS competitors. MMI data essentially agree, although the newsletter gave OEM divestitures a slight edge in 1998 (Feb., p. 1). Now in the last three months, TFI's data-base has shown an emerging trend: EMS companies are buying competitors more often than OEM facilities. TFI finds that EMS providers have made 30 acquisitions of competitors through October of this year compared with 22 OEM divestitures.

TFI has created the report Mergers and Acquisitions in Contract Manufacturing: Trends and Best Practices to help executives through the M&A process.

People talk about consolidation in the EMS industry. But it's also happening in the enclosure space on the electromechanical side of outsourcing. Except that the companies buying up enclosure suppliers don't all have the same pedigree. You might say that buyers come from three distinct lines: competitors within the enclosure business, traditional EMS companies, and board and backplane suppliers extending their value-added assembly services.

In the first case, an acquirer strives for greater scale and a broader footprint as an enclosure supplier to OEMs and EMS companies in the supply chain. Under the second scenario, an EMS company buys an enclosure supplier to integrate enclosure capabilities within a box-build offering (see also Aug., p. 1-3). The third type of buyer, with a core competence in board fabrication and backplanes, integrates an enclosure operation to augment the company's value-add. All three types of buyers appear below.

SCI Systems (Huntsville, AL) has purchased CMS Hartzell (Lexington, KY), a supplier of enclosures, from Linsalata Capital Partners (Cleveland, OH), a private equity firm. Providing SCI with the ability to build more enclosures in-house, this is SCI's second enclosure deal after its 1999 acquisition of TAG Manufacturing (Oct. '99, p. 2). The new deal also shows that outsourcing is increasingly bringing together EMS providers and mechanical suppliers of enclosures. (Aug., p. 1).

Financial details were not released. U.S. Bancorp Piper Jaffray (Minneapolis, MN) acted as Linsalata Capital Partners' advisor in this sale.

Serving the outsourced enclosure needs of leading OEMs, CMS Hartzell offers engineering and manufacturing capabilities in sheet metal fabrication, plastic injection molding and die casting. The company operates eight plants spread among Kentucky, California, Wisconsin, Minnesota, Texas and Mexico and employs over 2000 people. CMS Hartzell also maintains affiliate relationships in Scotland and China to provide market presence in Europe and Asia.

While a 1999 sales figure is unavailable for CMS Hartzell, 2000 revenue is projected as approximately $250 million.

"This strategic acquisition broadens our current enclosure capabilities, customer base and geographic footprint while adding critical capacity to support a number of growth opportunities. We are very pleased with CMS Hartzell's impressive customer set, which we believe offers us the potential over time to expand our subassembly, subsystem integration and final system assembly activities. CMS Hartzell's healthy growth rate is supported by an excellent reputation for superior customer service," states Gene Sapp, chairman and CEO of SCI.

Notable customers of the enclosure company include Cisco, Compaq, Lexmark and Sun.

Dan Kubes, who directs the EMS investment banking practice at U.S. Bancorp Piper Jaffray, points out, "SCI has a current supplier relationship with Cisco. The acquisition will further deepen and enhance that relationship with Cisco and will allow the combined entity to expand their broad service offerings to Cisco and other major technology OEMs."

Cisco, it turns out, was also a customer of SCI's first enclosure acquisition, TAG Manufacturing. SCI was recently added to Cisco's approved vendor list for PCBAs.

Kubes reports that CMS Hartzell attracted strong interest among both financial and strategic buyers. "The strong level of interest for CMS Hartzell generated by U.S. Bancorp Piper Jaffray is certainly indicative of a broader trend of the continuing convergence between the large CMs and the major electromechanical enclosure players," he notes.

According to Kubes, "The financial performance of CMS Hartzell will be accretive to SCI's P and L." Bear Stearns (New York, NY) reports that CMS Hartzell's EBITDA margins "are in the low- to mid-teens, compared to SCI's in the 6% range."

CMS Hartzell was created by the 1998 merger of Continental Metal Specialty, a metal stamping and assembly house, and Hartzell Manufacturing, a plastics company. Linsalata owned both companies at the time of the merger.

At present, the ability to manufacture enclosures serves as one way to differentiate the large CMs.

Recently, NatSteel Electronics Ltd. (NEL Singapore) signed definitive agreements to purchase about a 25% interest in Taiwan's LiteOn Enclosure, which provides metal and plastic enclosure products and final assembly. As a result, LiteOn joins NEL as an associate company.

What's more, this move may ultimately benefit Solectron, which just made a takeover bid for NEL (see article on p. 1). With NEL, Solectron would add enclosure capabilities as some of its competitors have done.

Formerly a majority-owned subsidiary of Taiwan's LiteOn Group, LiteOn Enclosure becomes a joint venture between NEL and the LiteOn Group.

NEL is also selling its metal stamping subsidiary in Guadalajara, Mexico, to the joint venture. The parties are also considering an injection of assets in Hungary to quickly start the venture's plastic operations there. LiteOn Enclosure also operates in Shenzhen, China, and Taipei.

LiteOn Enclosure and NEL are committed to use each other's services. This joint venture will equip NEL with plastic and metal enclosure capabilities in Asia, North America and Europe where NEL's plants are starting to fulfill their box assembly orders. The venture reflects NEL's strategy to transform itself from an Asia-based PCB assembly house to a global provider of supply chain services from design to market.

Since September, Trend Technologies (San Jose, CA), an enclosure supplier to both OEMs and CMs, has announced or closed three acquisitions in the enclosure space.

In the latest deal, Trend this month signed an agreement to purchase G.Form Kft. (Budapest, Hungary), which engages in plastic injection molding and mold making. Operating at two locations in Hungary, G.Form has 90 employees and 13 molding machines.

"Manufacturers of electronic products have been establishing facilities in Central and Eastern Europe, especially in Hungary," states Bert Vermeulen, Trend's European business manager. "This acquisition helps us to supply these OEMs and contract electronic manufacturers with mechanical components and subassemblies locally from Hungary."

Earlier in October, Trend announced a deal of larger proportions. The company entered into an agreement to purchase Cowden Metal Specialties (Chino, CA), a precision sheet-metal manufacturing company.

This deal will give Trend a presence in Southeast Asia as well as more facilities in North America. The Cowden deal will add three facilities in California; a plant in Guadalajara, Mexico; and facilities in Johor Bahru, Malaysia, and Singapore. As a result, Trend's facility space will almost double, exceeding two million ft2.

With Cowden and G.Form, Trend will manufacture in 16 facilities worldwide and maintain over 600 metal stamping and molding machines. Trend's sales for 2000 are projected at nearly $600 million.

In the first deal of this series, Trend acquired Data Packaging Ltd. (DPL), an injection molder located in Mullingar, Ireland, near Dublin. DPL strengthens Trend's plastics capabilities in Ireland, while giving DPL customers the chance to utilize the metal capabilities of Trend Dublin.

Before the DPL acquisition, Trend's sales for 2000 were estimated at over $400 million

Another buyer in the enclosure space...Sweden's AB Segerström & Svensson, an enclosure supplier, has acquired Lewis C. Grant, a British manufacturer of enclosures. Datacom and telecom are the primary enclosure markets for both companies. Segerström aims to be a top-three supplier of enclosure systems. This deal will increase the Swedish company's sales to Motorola.

Publicly traded DDi Corp. (Anaheim, CA), a provider of interconnect services including raw PCBs and backplanes, has acquired Texas-based Golden Manufacturing, a privately held supplier of metal enclosures and value-added assembly services to communications OEMs and others.

So DDi serves as an example of a third type of buyer, a company that integrates enclosure capability with a core backplane offering. This deal allows DDi to build both the enclosure and the backplane that goes into it.

"Golden is especially appealing to us because we will be able to backward integrate into our assembly services the in-house production of metal enclosures, a key material in the assembly of backpanels, card cages and wire harnesses," states Bruce McMaster, DDi's president and CEO. By integrating Golden into DDI's Texas facility, DDi says it is improving turnaround times for its value-added preproduction and high-growth assembly lines of business.

According to a new agreement with Siemens Mobile, Flextronics International (Singapore) will acquire part of the production activities at Siemens' site in L'Aquila, Italy.

Employing about 1000 people, these activities focus on telecom infrastructure products and have a history of manufacturing products related to GSM network systems, especially base stations.

"We build on the existing cooperation with Siemens, and this deal strengthens it even further," states Ronny Nilsson, president of Flextronics International, Western Europe. "We will develop the business in Italy and will be able to serve not only Siemens, but also other customers."

Flextronics manufactures cell phones for Siemens under earlier agreements (April, p. 3; Aug., p. 9-10).

Varian Inc. (Palo Alto, CA) has purchased Imagine Manufacturing Solutions, a CM in Rocklin, CA, for Varian's Electronics Manufacturing segment. The price was $6.7 million in cash.

For the last 12 months, Imagine had sales of about $16 million, and its work force totals 130. The purchase includes most of the assets, certain liabilities and the assumption of a lease on a 31,000-ft2 building. Imagine manufactures products for companies in the commercial video, networking, semiconductor yield and test, and medical equipment markets. The CM was originally part of Jones Intercable and had operated under the name Jones Futurex.

The acquisition provides Varian Electronics Manufacturing with access to the Silicon Valley market, while the Varian unit avoids paying the high costs of operating in the Valley. "It gives us an entryway into Silicon Valley without actually having to be there," explains Wilson Rudd, VP of Varian's Electronics Manufacturing business.

This is the second acquisition this year for the contract manufacturing business. In January, it took over Executone's manufacturing operation in Poway, CA (Feb., p. 10).

For the fiscal year ended September 2000, Varian Electronics Manufacturing generated external sales of $164 million, up 71% from a year earlier. The Varian operation, a high-mix business, ships close to 2000 different products in an average month.

More deals done...Viasystems Group (St. Louis, MO) has completed its acquisition of Laughlin-Wilt Group, a CM based in Beaverton, OR (Oct., p. 8-9). LWG's cofounders - Joe Laughlin, president and CEO, and Jay Wilt, executive VP and COO - will continue with the company in their present roles....Benchmark Electronics (Angleton, TX) has acquired the MSI Division of Outreach Technologies. Located in Manassas, VA, the MSI operation comes with a facility of about 40,000 ft2. Benchmark paid $4.5 million, subject to adjustment for working capital....Last month, Finmek Group (Padova, Italy) acquired Seima Elettronica, a former Magneti Marelli company in Tolmezzo, Italy. Employing 160 people in 4500 m2, Seima Elettronica provides assembly and testing of boards and subsystems in medium to high volumes. Its specialty is automotive. Meanwhile, Finmek wants to go public on the Italian Stock Exchange in the first half of 2001....Nam Tai Electronics (Hong Kong) has closed on its purchase of the J.I.C. Group of companies (Hong Kong), which produce LCD panels and transformers in China (Oct., p. 10). The price was $32.7 million, based on net income of not less than $3.8 million for the 12 months ending Mar. 31, 2001.

New programs...Alcatel Canada, formerly Newbridge Networks, has selected SMTC Corp. (Toronto, Canada) as the primary manufacturer for a selection of high-complexity PCB assemblies. Now in full production, the contract is valued at about $350 to $400 million over the next three years. Alcatel Canada is outsourcing its higher volume DSL board assemblies as a complement to its internal manufacturing capacity....Brix Networks (Billerica, MA) has chosen Pemstar (Rochester, MN) as its global contract manufacturer. Brix develops products and services that verify Internet-based service level agreements. Pemstar has also identified Condux as another new customer....Metro-Optix (Santa Clara, CA, and Allen, TX) , a provider of optical networking equipment, has selected ACT Manufacturing (Hudson, MA) as a strategic partner to manufacture a variety of complex PCB assemblies for the customer's core product. ACT has been working on new product introduction with Metro-Optix, which is developing Internet infrastructure for metropolitan networks....AirPrime (Santa Clara, CA), a provider of CDMA-based wireless access solutions, has made Flextronics the manufacturer of choice for its OEM wireless access products....Key Tronic Corp. (Spokane, WA) has landed a three-year contract to manufacture several versions of a point-of-sale printer for Axiohm Transaction Solutions. Production could begin as early as this month in Juarez, Mexico....Network Computing Devices (Mountain View, CA), a supplier of information appliances, has announced an expanded manufacturing alliance with SCI Systems (Huntsville, AL). This expanded relationship will involve SCI's design and product development services. NCD recently issued to SCI a promissory note convertible into 3.3 million shares of NCD stock....IBM China and China Great Wall Shenzhen Co. have formed a joint venture to provide advanced PCB assemblies to Nokia joint ventures for current and future wireless products and systems. The new company is called Beijing GKI Electronics Co. Ltd....UMM Electronics (Indianapolis, IN), a member of the Leach Technology Group (Westport, CT), will provide product development and manufacturing services for the Portable Organ Preservation System in partnership with another Leach company and TransMedics (Malden, MA).

New facilities...Celestica (Toronto, Canada) has opened an office in Tokyo, Japan, which has been set up as a Japanese subsidiary. The new subsidiary, says Celestica, shows its commitment to building strategic relationships with Japanese partners, both in Japan and globally. Celestica reports it already has a number of Japanese customers including NEC (July, p. 6-7)....Flextronics plans to construct two buildings of about 103,000-ft2 each at Pease International Tradeport, formerly Pease Air Force Base, in Portsmouth, NH. The New Hampshire operations that Flextronics acquired from Cabletron will be moved to the new site (Jan., p. 8-9)....Also in New England, SMTC has announced a 150,000-ft2 facility in Franklin, MA, which will double its overall manufacturing in the region. The new plant will consolidate two Boston area operations in sheet metal, enclosures and systems integration as well as expand service offerings to New England customers....Yet another CM is adding space in New England. Benchmark Electronics has leased about 40,000 ft2 in Mansfield, MA....Universal Scientific Industrial Co. (Nan-Tou, Taiwan), the ninth largest CM in the MMI Top 50 for 1999, has opened a 36,000-ft2 facility in Morgan Hill, CA, within Silicon Valley. The facility is offering services from design and prototyping to launch for high-volume production. USI's parent company is Advanced Semiconductor Engineering, an IC packaging house. Because of that, USI says the Morgan Hill operation must have the capability to place the latest IC packages....Citing a need for added capacity in the Southwestern US, Sparton Corp. (Jackson, MI) plans to construct a facility in Hobbs, NM. The Hobbs facility, Sparton's seventh plant, will be linked to current facilities in Rio Rancho and Deming, NM.

People on the move...SCI has named COO Bob Bradshaw as president. He joined the company in December 1999 after serving as president of Solectron's Eastern Region. Before that job, Bradshaw spent 20 years at IBM....At Solectron, Walt Wilson has chosen to step down from his position as senior VP of business integration and information technology and relinquish his title of corporate officer. Wilson will assume a new role coordinating certain strategic projects. Solectron says the decision is Wilson's alone. His business integration duties will be assigned to Sajjad Malik, who has been appointed VP of enterprise integration. IT responsibilities are handled by Bud Mathaisel, corporate VP and CIO....Mark Holman, a former Solectron executive, has been named the first president and CEO of e2open, one of two new exchanges backed by consortia. Holman had been corporate VP of strategic marketing, planning and corporate development at Solectron....Jack Calderon, chairman of EFTC (Phoenix, AZ) has ended his employment status with the company. Calderon will resign as chairman effective January 31, 2001 and will serve on the board of directors until April 1, 2001. But he will continue in a consulting capacity. Earlier, Calderon gave up his chief executive duties to James Bass, who was brought in as the new president and CEO (July, p. 8). This year, EFTC underwent a recapitalization by Thayer Capital Partners and BLUM Capital Partners, and a new management team was brought in. Also at EFTC, Rodney Gunther has been promoted to VP and GM of Southwest Commercial Operations in Phoenix, AZ....Manufacturers' Services Ltd. (Concord, MA) has promoted Bert Notini to CFO. Having arrived in April from Wang Global, Notini had been MSL's executive VP of business development and general counsel. MSL has also promoted Alan Cormier to VP and general counsel and John Boucher to VP of global supply chain management....Sparton has promoted David Hockenbrocht to president and CEO from president and COO. He replaces John Smith who stepped down after 50 years with the company. ...MCMS (Nampa, ID) has hired Tony Nicholls as COO. He had served as VP of operations for Plexus....Group Technologies (Tampa, FL), a subsidiary of Sypris Solutions, has appointed Richard Warren to the newly created position of director of supply chain management. He comes from Lear Corp., formally United Technologies, where he was materials and purchasing manager....EPI (Hillsboro, OR), the contract manufacturing division of Epson Portland Inc., has named Jim Sloan as sales and marketing manager for business development and Kimball McKeehan as business development manufacturing manager. Sloan has spent the past 11 years dealing directly with contract manufacturing and has represented U.S. and Asia-based companies with manufacturing facilities. McKeehan, a veteran of HP, came to EPI from a biomedical company....Laughlin-Wilt Group has hired Bill Winther as VP of operations for LWG's Northwest business. He had been president of the Centralab Division of Philips....CTI Technology (Springfield, MA) has hired Jennifer Estabrook as VP, general counsel and secretary. She comes from The Stanley Works....Tim Benincasa, former president of CM EPIC Technologies (Norwalk, OH), has formed Goodhouse Electronics Marketing (GEM), an EMS rep firm. Located in Sandusky, OH, the new firm sells contract assembly, sheet metal fabrication, plastic injection molding, and wire and cable services. GEM represents Electronic Product Integration (EPI), an EMS provider based in Farmington Hills, MI....Bruce Spivack, Ph.D. has joined the management consulting team at Technology Forecasters, Inc. (Alameda, CA). His duties will include managing TFI's new Quarterly Forum for Electronics Manufacturing Outsourcing and Supply Chain. Spivak has nearly 15 years of consulting experience in manufacturing.

ACT Manufacturing (Hudson, MA) has put into place a new organization structure. Under this scheme, the provider has appointed three people to the newly created position of executive VP. Jack O'Rear, who came to ACT through its acquisition of CMC Industries, has become executive VP of operations for the Americas. Blaise Scioli, a long-time senior manager at ACT, has assumed the title of executive VP of global marketing and business development. He will also continue to oversee ACT's Cable and Electromechanical Assembly Division. Robert Zinn has been made executive VP of European and Asian Pacific operations. Zinn came to ACT with its acquisition of GSS/Array, where Zinn had served as president and CEO. The new organization also includes the naming of two senior VPs of operations in the Americas. Gary Barnier is responsible for ACT's facilities in Massachusetts and California, while Mike Driste oversees plants in Georgia, Mississippi and Mexico. In addition, the company recently appointed Jim Menges as senior VP of operations for Asia.

Supply-chain alliance...Celestica has entered into a strategic alliance with Partminer, which provides marketplace technology and procurement services.