![]()

![]()

Cover Story

Design

JDM Model for Defense/Aerospace Outsourcing

Market Data

News

Flextronics Keeps Adding Skills in India

JDS Selling Transceiver Operations to Fabrinet

Last Word

After nine months of results are in, 2004 is shaping up as a very good year for the EMS industry. A group of 15 large EMS providers including the tier-one companies has exceeded 20% growth for the period and is on pace to surpass industry forecasts for the year. Because these providers account for the majority of industry revenue, the EMS industry should also perform better than was expected for 2004.

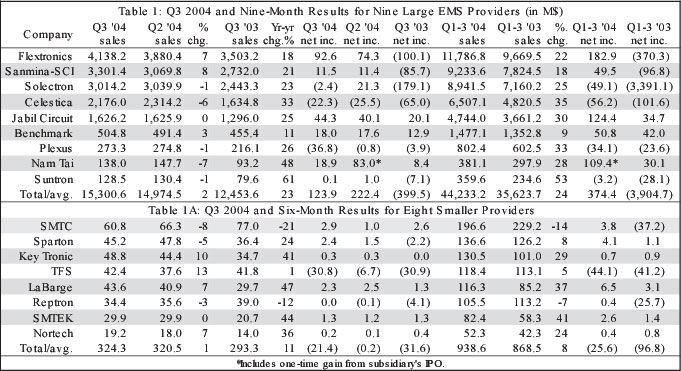

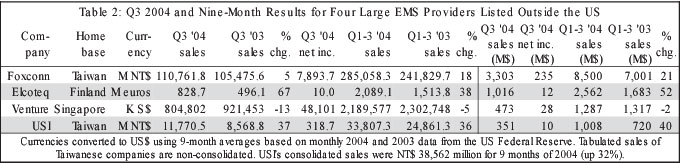

Nine large providers with US-traded stock combined for a growth rate of 24% for the first nine months of the year (Table 1). This growth rate did not change when revenue was added from six other large providers, four of which are based outside the US (Table 2). (The remaining two consisted of a large EMS division, Kimball Electronics Group in Table 5, and PEMSTAR, whose results are estimated in Table 4 because of an accounting investigation.) These 15 large providers totaled $58.6 billion in revenue for the first three quarters of the year.

Having put up 24% growth for the first nine months, this group of 15 providers will easily top industry growth forecasts made before the start of the year (Dec. 2003, p. 2). An average of three forecasts called for EMS growth of 9.0% in 2004 and a five-year CAGR of 10.7%. If the EMS market for 2003 was about $94.9 billion – the average of the three forecasts – then the 2004 market will easily exceed $103.4 billion, the predicted average for 2004. The nine-month growth for these large providers is high enough to ensure this outcome.

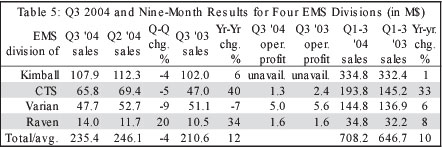

But the rest of the EMS market, mostly smaller players, probably did not grow at an overall rate of 24% if MMI’s data is any indication. Eight smaller providers, all US-traded, increased revenue in the aggregate by 8% for the first nine months (Table 1A). When sales from three EMS divisions in Table 5 are added, the growth rate rose to 11%, still well below that of the large providers.

What will full-year EMS growth rates look like? Using the midpoint of Q4 guidance for the nine US-traded providers in Table 1, MMI calculated 20% estimated sales growth for these providers in 2004. Absent specific guidance from the two Taiwanese providers in Table 2, a similar estimate cannot be done for the four providers based outside the US. But since nine-month sales (non-consolidated for Taiwanese companies) increased by 25% when converted into US dollars, these non-US-based providers probably won’t have much effect on the 20% growth estimated for the US-traded providers.

But estimating annual growth for the smaller players is merely a guess because MMI’s sample size is not large enough to represent their numbers with accuracy. Indeed, this is the problem with estimating EMS industry growth for any year. Still, the 13-point gap between large- and small-provider growth rates for the first nine months probably indicates that the smaller players generally are not keeping up with their larger competitors.

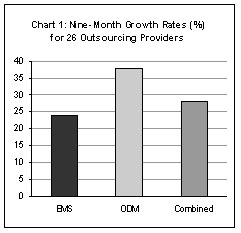

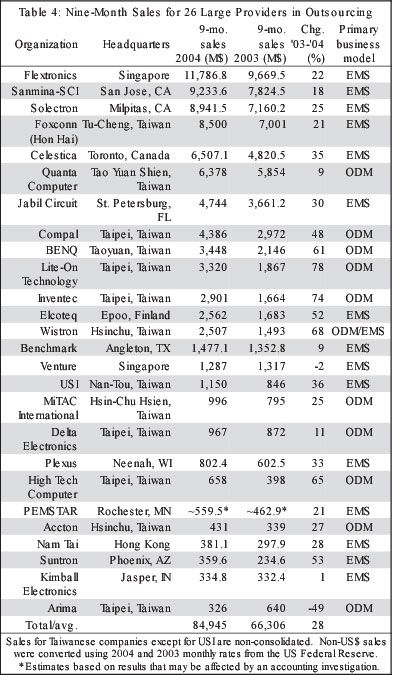

Lest anyone doubt the staying power of outsourcing, 26 large providers of outsourcing services together posted a sales gain of 28% for the first nine months of the year (Table 4). Made up of EMS providers and ODMs, this group accounted for combined sales of $84.9 billion in the first three quarters of 2004. Likewise, this growth rate is well above a 2004 forecast for the combined EMS and ODM markets. Earlier this year, Electronic Trend Publications (San Jose, CA) predicted that the combined markets would grow by 12.5% in 2004 (July, p. 3).

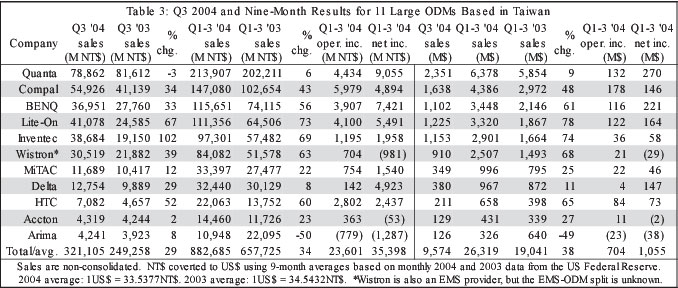

The group of 26 outsourcing providers received a boost from its 11 ODM members, which collectively increased nine-month sales by 38% in US dollars (34% in NT dollars – Table 3). As shown in Chart 1, the growth of these large ODMs outpaced that of large EMS providers in the group by 14 percentage points. This should not come as a surprise; it is generally accepted that the ODM business is growing faster than the EMS industry.

But the gap between ODM and EMS growth rates among large players appears to be narrowing from last year. Within a group of 25 of the largest outsourcing providers listed for 2003, 12 ODMs together grew sales by 36% last year, compared with 8% for the EMS providers in that group (May, p. 1).

An interesting fact emerges from the results of the 11 ODMs covered here. Total net income for the group exceeded combined operating income (Table 3). Some ODMs benefited from significant amounts of non-operating income. In the first nine months, operating profit margin for this ODM group amounted to 2.7%, which is below what is typically expected for an ODM business.

Note that Taiwan’s major motherboard suppliers were not included in this group of ODMs.

Interest in the outsourcing of design activities is growing among defense and aerospace prime contractors and their second- and third-tier suppliers. But defense and aerospace customers in general will confine their design outsourcing to activities that take place after electrical design, according to Sypris Electronics (Tampa, FL), an EMS provider specializing in defense, aerospace and homeland security.

When a customer hands off a completed electrical design to an EMS provider who then finishes the design work and takes the product design into production, that provider is acting as a joint design manufacturer, or JDM. The JDM model may be old hat on the EMS industry’s commercial side, where providers routinely turn customers’ electrical designs (schematics) into board layouts. But based on Sypris’ experience, this model is only now making a dent in the defense and aerospace sector, where the pace of outsourcing has been slower than in the commercial world.

With defense and aerospace customers placing more importance on design services, Sypris recently announced its JDM services offering. The announcement capped an effort that began about a year ago. For JDM work, Sypris has assembled a staff of more than 100 design engineers spanning systems engineering, hardware design and software development.

While Sypris has the engineering expertise to design an encryption device from the requirements stage – and is working on one such project and another similar to it – this is the exception rather than the rule. Turnkey product design of defense and aerospace products requires more expertise than an EMS provider would typically have. “To do this, a JDM/EMS company would need to have expert systems engineers in the applicable field or technology such as radio frequency, infrared, electro-optics, signal processing, communications security, and/or others. No JDM/EMS company can possibly maintain a staff to span the systems engineering design expertise necessary to address the full range of defense and aerospace electronic product requirements of its customer base,” wrote Jeff Kaylor, Sypris’principal applications specialist, in a paper published in the Proceedings of the SMTA International Conference held in September.

In contrast, JDM, which starts at schematic capture, requires engineering skills that are more widely available. In a JDM program, design work would include selecting parts not specified by the customer, board layout and design verification.

This model is beginning to strike a chord within the defense and aerospace community. For instance, from December 2003 to August 2004, Sypris received 13 different inquiries from customers regarding JDM work. Of those inquiries, three or four turned into business for Sypris. But not all of the proposed work was attractive to Sypris. The company actually declined to bid on some requests, which involved legacy products supported by certain databases and design tools that Sypris would not commit to.

Defense and aerospace companies have been slow to farm out design activities just as they been reluctant to outsource in general, much to the dismay of those who expected big things from the sector. “There were some people several years ago who were forecasting a very rapid double-digit kind of compound annual growth rate of defense and aerospace outsourcing. And it didn’t happen,” said Kaylor in an interview with MMI. He explained that companies in the sector have wrestled with a number of issues, which have kept them from wholesale adoption of outsourcing. Risk management, lower absorption of fixed costs, internal politics and union issues can all act as impediments, he said.

Despite the impediments, Sypris is now seeing greater interest in outsourcing from corporate levels down to individual operating sites. Likewise, EMS growth rates in defense work are forecasted to increase. Last year, Electronic Trend Publications predicted a 7.2 % CAGR (6-year) for the defense segment of the EMS business. This year, ETP issued a five-year forecast for an 8.8 % CAGR in the defense segment. Yet this improved rate is not good enough for Sypris, and the provider expects to surpass it.

However, Sypris’ growth plans do not include an ODM strategy, now increasingly popular on the commercial side of the EMS industry. “I find it difficult to envision that in the defense and aerospace market that the ODM concept will ever catch on to the extent that it has in the computer and the cell-phone marketplace,” said Kaylor. An ODM capability for the defense and aerospace market would involve so many different systems engineering disciplines that it would be virtually possible to staff for them, he explained.

With the introduction of the new JDM offering, Sypris is presenting itself as the first JDM provider dedicated to the defense and aerospace sector. Nevertheless, providing engineering services to the defense market is not a new activity. Two examples come to mind. Sanmina-SCI has over four decades of experience providing engineering and design services to the defense/aerospace sector in support of its own product development and as a value-added service to its customers, according to the company’s website. This history in the sector comes from the former SCI Systems, which was founded as an aerospace supplier and was eventually acquired by Sanmina-SCI through a merger. Secondly, PEMSTAR Pacific Consultants, a unit of PEMSTAR, has a record of providing turnkey product designs to both commercial and government customers.

Sypris Electronics is a subsidiary of publicly-held Sypris Solutions.

A new report forecasts continued robust growth for electronics manufacturing in China, but it also warns about risks arising from the country’s economic growth. Electronics Manufacturing in China, Third Edition, published by Electronic Trend Publications (San Jose, CA), predicts that the COGS (cost of goods sold) value of electronic products manufactured in China will grow at a 17.2% CAGR from 2003 to 2008. However, the report cautions that the rising cost of raw materials such as oil, steel and water could make China less attractive for foreign investment and could precipitate a meltdown in the banking system and in foreign exchange.

According to ETP, by 2008 China will account for nearly a third of worldwide COGS for electronic products. In 2008, China’s share of global COGS is expected to reach 30.9% of a total estimated at $875.4 billion. ETP projects that this year China will take a 20.2% share of $718.5 billion in total COGS, up from an 18.9% share of $648.2 billion in 2003.

The study predicts that China’s COGS will amount to $145.0 billion in 2004, representing an increase of 18.6% from $122.2 billion estimated for 2003. In 2008, electronic products made in China will represent $270.3 billion in COGS.

ETP projects that computer segment, which had 30% of China’s COGS in 2003, will enjoy the highest growth from 2003 to 2008 with a CAGR pegged at 20.7%. The second fastest growing piece should be automotive at 16.9% CAGR, followed by communications at 16.6%, according to the report.

As one might expect, computer and communications products represent the majority of COGS value in China. The study estimates that communications and computer products accounted for 34% and 30% of China’s COGS respectively in 2003. By 2008, the two segments will have a combined share projected at nearly 68%.

For more information, go to www.electronictrendpubs.com.

Publicly held CTS Corporation (Elkhart, IN), which operates component and EMS businesses, has reached a definitive agreement to acquire SMTEK International (Moorpark, CA), a Nasdaq-listed EMS provider.

CTS will buy the outstanding shares of SMTEK at a price between $14.20 and $15.00 per share, corresponding to an equity value in the range of $44.3 and $46.8 million. The final price per share depends on a formula that includes the price of CTS stock over 20 trading days. Payment will be 75% in cash and 25% in CTS common stock. In addition, CTS will assume and pay off all debt obligations of SMTEK, currently at about $15 million.

SMTEK, a high-mix, turnkey provider, had sales of $102.4 million in the last reported 12 months and operating earnings of $4.0 million. Its four facilities are located in Moorpark and Santa Clara, CA; Marlborough, MA; and Bangkok, Thailand. The company primarily serves medical, industrial, security, aerospace and defense, and communications markets. Customers include Medtronic, Occam Networks, L-3 Communications, Raytheon, Philips Medical Systems, Hass Automation, Fujikura and Pentair.

CTS gave three reasons for making this deal: strengthening its position as a high-mix provider; accelerating its expansion into industrial, medical and other such growth markets; and obtaining a West Coast operating presence, which CTS currently does not have.

“The combination brings CTS an expanded geographic and market footprint and significantly broadens the engineering capabilities we can bring to our customers. For SMTEK customers, the combined company provides greater financial strength, broader geographic point of delivery capability, and expanded expertise in box build and direct-ship logistics,” stated Don Schwanz, chairman and CEO of CTS.

Box build accounts for about 80% of CTS’s EMS revenue, and PCB operations make up about 20%. In contrast, SMTEK derives about 80% of its sales from PCB assembly and some 20% from box build.

In the last reported 12 months, CTS generated sales of $520.8 million, of which $258.7 million came from its EMS business. When the transaction is completed, the combined EMS operation will have estimated revenue in excess of $360 million.

Subject to approval by SMTEK shareholders and other customary conditions, the deal is expected to close in Q1 2005. Thomas Wheeler and certain related trusts control about 33% of SMTEK’s common stock. He has agreed to vote in favor of the acquisition.

CTS expects the transaction to be accretive by $0.02 to $0.03 per share in the first year.

Flextronics (Singapore) has entered into an agreement to acquire Emuzed (Fremont, CA), a provider of mobile multimedia technology and solutions with R&D centers in Bangalore and Chennai, India. This is but the latest in a series of acquisitions that Flextronics has made to gain engineering capabilities in India (Oct., p. 6-7; Sept, p. 3; June, p. 1-2).

“Emuzed is a dominant supplier of multimedia technologies, products and services to mobile and consumer electronics industries…Adding their convergence technologies capabilities into our software design services offering will strengthen our existing offering to customers,” stated Ash Bhardwaj, Flextronics’ president of design and ODM services.

Founded in 2001, Emuzed employs around 200 people in Bangalore.

Meanwhile, Nortel Networks has completed the transfer of certain optical design operations and related assets in Ottawa, Canada, and Monks-town, Northern Ireland, to Flextronics. This closing is the first stage of a larger outsourcing pact announced by the two companies earlier this year (July, p. 1-2).

Optical components supplier JDS Uniphase (San Jose, CA) has agreed to consolidate its datacom transceiver manufacturing with Fabrinet (Pathumthani, Thailand), an MMI Top 50 EMS provider. This supply agreement includes the sale of JDS’s Bintan, Indonesia, and Singapore manufacturing operations and provides JDS with long-term sourcing guarantees for the datacom transceivers currently manufactured at these facilities.

About 450 JDS employees associated with manufacturing will transfer to Fabrinet. JDS will retain its Singapore design and development team. Terms of the agreement were not disclosed.

Fabrinet has provided high-volume manufacturing services to JDS since 2000 and began manufacturing datacom transceivers for the company in 2002.

The provider specializes in the engineering and manufacture of complex optical, mechanical, and electronic components, modules, and subassemblies.

More new programs…Under an agreement with Ukranian Mobile Communications, Flextronics Network Services, a business unit of Flextronics, will become the main contractor for the rollout, expansion and maintenance of UMC’s GSM network throughout Ukraine. Flextronics will handle nearly 70% of the construction for UMC’s GSM network, involving roughly 1800 GSM sites….Solectron (Milpitas, CA) will manufacture the Personal Internet Communicator, a new consumer device developed and designed by AMD. The PIC was developed to provide affordable computing and Internet access in high-growth markets starting with India, Mexico and the Caribbean region. Under this global agreement, Solectron is supplying complete product manufacturing and assembly, testing and product distribution for several markets in Asia/Pacific and the Americas….The Medical Division of Sanmina-SCI (San Jose, CA) will manufacture a hemodialysis system for Renal Solutions (Warrendale, PA)….Elcoteq Network (Espoo, Finland) has signed an ODM agreement with Siemens, whereby Elcoteq will deliver a mobile phone model. Production will start during Q4. Elcoteq has also landed other new handset products customers and programs, in some of which the end customer has also outsourced product design. The provider projects that altogether these new accounts will generate at least 350 million euros in sales during 2005. In addition, Orthogon Systems (Devon, UK) has contracted Elcoteq to manufacture wireless broadband radio links at Elcoteq’s Offenburg plant in Germany….Among the eight new customers signed by PEMSTAR (Rochester, MN) in the September quarter is Motion Computing (Austin, TX), a supplier of tablet PCs and accessories….OnScreen Technologies (Safety Harbor, FL) has contracted SMTC (Markham, Ontario, Canada) to manufacture a line of rapid dispatch emergency signs based on OnScreen’s LED video display technology….COLT Technologies (Salt Lake City, UT), a developer of wireless agricultural technologies, has selected Electronic-Coop (San Juan, Puerto Rico) to assemble components for COLT’s wireless health monitoring system for livestock. This one-year contract accompanies a blanket purchase order for 10 million pieces....L-3 Communications Security and Detection Systems has awarded LaBarge (St. Louis, MO) a $6-million contract to continue to perform turnkey manufacturing services for three explosives detection systems used at airports to automatically scan checked baggage (June, p. 6). Also, LaBarge has finalized a $4.1-million contract with Northrop Grumman’s Electronic Systems sector. Under the contract, LaBarge will supply electronic subsystems for a military airborne radar system supporting defense projects in Australia and Turkey.

Strategic alliances involving Japan…SIIX (Osaka, Japan), an MMI Top 50 provider, and MFS Technology (S) Pte Ltd (MFSS), a subsidiary of flex circuit maker MFS Technology Ltd (Singapore), have signed a memorandum of understanding. The two companies intend to form a strategic alliance, whereby SIIX will direct all of its requirements and inquiries for flex circuits to MFSS for quotation and supply. SIIX will also represent MFSS in the Japanese market for new flex circuit accounts. The Japanese provider currently buys flex circuits from MFSS for requirements outside Japan for non-Japanese accounts and for its own consumption. MFSS plans to qualify SIIX as another source for contract assembly and will direct its non-customer assigned component requirements and inquiries to SIIX. Each company intends to purchase S$3 million worth of the other’s stock….EMS provider Integrated Microelectronics Inc. (Laguna, Philippines) and EAZIX, its design service and ODM arm, have partnered with a Japanese software development company, Embedded Linux Technology, to help Japanese OEMs bring their products to market. EAZIX provides services such as embedded software development, hardware design, prototyping, and design for manufacturing. IMI takes care of volume manufacturing. ELT handles project management and provides local technical support for the OEMs.

New owners of EMS provider Nexus Custom Electronics (Brandon, VT) are preparing to take the company public. “We are going to file a registration statement with the SEC in the next 60 days,” said Joseph Donohue, co-chairman of Nexus. Donohue and his partner Robert Farrell recently acquired Nexus through Sagamore Holdings, a new company they formed to make the purchase (Sept., p. 5). Donohue expects that Nexus will be public by spring 2005.

The two partners plan to basically grow Nexus through acquisition. In the next two to four years, “we’d like to get Nexus up to 150 million dollars through acquisition,” said Donohue. Once Nexus is public, a $30-million credit line kicks in from one of its investors. This line will provide a source of funds for making acquisitions.

“We’re definitely in a buying mode,” said Donohue.

Meanwhile, Celerity Systems (Knoxville, TN) has signed an agreement to acquire an interest in Sagamore Holdings. Celerity will provide Sagamore with consulting services, including management advice, in exchange for 7.5 million shares of Sagamore’s common stock. After the payment of certain fees, Celerity expects to retain five million shares, representing 5% of Sagamore’s common stock. Celerity focuses on providing capital formation, management advice and investments in developing companies.

New facilities in Mexico…Suntron (Phoenix, AZ) has leased a new 80,000-ft2 facility in Tijuana, Mexico. The facility will give Suntron more space for its Tijuana operation, which just landed its first military contract from a new aerospace and defense customer under a four-year agreement....NuVisions Manufacturing (Springfield, MA) has opened a new plant in Tijuana for PCB and electromechanical assembly. The plant is designed to provide the company with a lower cost alternative to address the growing demands of Nu Visions’ low- to medium-volume customer base.

Some financial news…Flextronics is privately offering 6.25% senior subordinated notes with a principal value of $500 million and a due date of 2014. The company intends to use the net proceeds of the offering to repay outstanding debt under its revolving credit facilities and for general purposes, including working capital requirements, acquisitions and capital expenditures….PEMSTAR is conducting an investigation of certain accounting discrepancies related to its Guadalajara, Mexico, facility. The company said it believes this issue will not materially affect current fiscal year results, but may impact previously reported fiscal periods. PEMSTAR estimated the amount at issue at $6 million or less. The accounting review has caused PEMSTAR to delay filing SEC Form 10Q for the September quarter….Hon Hai Precision Industry (Tu-Cheng, Taiwan), also known as Foxconn, has stated that a number of press reports were wrong about the timing and amount of its IPO plan for its overseas subsidiary. So it appears that the IPO amount reported here last month on page 5 is incorrect....Elcoteq has obtained a 230-million-euro revolving credit facility.

Loss of a customer…Suntron has reported that Applied Materials, one of Suntron’s principal customers, has decided to move substantially all of its current Suntron business to other contract manufacturers. Suntron has had an ongoing dispute with Applied regarding payment for excess and obsolete materials. Applied Materials accounted for 25% of Suntron’s Q3 sales. The provider expects that this transition will not adversely impact Suntron’s results until Q1 2005.

People on the move…Celestica (Toronto, Canada) has appointed John Boucher as its new chief supply chain and procurement officer. He replaces Robert Shanks, who left the company for personal reasons after a short time in this position (Sept., p. 7). Boucher joined Celestica in March from MSL, which was acquired by Celestica. At MSL, he was the corporate VP of global supply chain management. Also, Celestica has named Robert Hemmant global lean architect.

In the past, if someone were to propose an electronics industry code of conduct for OEM supply chains, that person might be met with disbelief, or even derision. After all, the dominant pattern of outsourcing in recent years has been to transfer production from high-cost sites in the developed world to low-cost areas in the developing world, where local regulations sometimes permit practices that wouldn’t be tolerated in the US or Western Europe. Nevertheless, HP, Dell and IBM recently released the Electronics Industry Code of Conduct with the help of five tier-one providers (Oct., p. 5-6). Adherents to the code are expected to police themselves and require that their first-tier suppliers implement the code. Although the code creates a burden for EMS providers, MMI believes that it’s good thing for the EMS industry…that is, if it’s enforced.

By promoting socially responsible business practices throughout the globe, these OEMs and their EMS providers can show that they’re not exploiting workers in the developing world. Basic human rights alone justify the code. But the electronics industry also gains positive PR, which should not be underestimated.

Here’s why. MMI used to think that nothing could derail the secular trend in outsourcing. But what if human rights groups threaten to boycott certain electronic products based on their belief, whether legitimate or not, that these products or parts contained therein were made under “sweat shop” conditions in the third world? OEMs may be sold on the concept of outsourcing, but they’ll think twice if groups of customers start objecting to their outsourcing practices. This is not a farfetched scenario. It has already happened in the retail industry.

But it won’t be enough just to proclaim that a company has adopted the code. EMS providers must not only apply the code to themselves, but also ensure compliance among their component and other first-tier suppliers. Tier-one EMS providers have large supply bases, and it remains to be seen how they will enforce the code. Will they do it in stages, starting with their key suppliers? How long will it take to audit all these suppliers? What will cause punitive measures to be invoked?

Although the code provides standards for conduct, it does not offer guidelines for enforcement, other than to specify a corrective action process. That leaves OEMs and their providers to come up with their own processes for enforcement. Still, this shortcoming may not amount to much if the code and its enforcement are adopted as standard language in supply agreements.

Effective enforcement is essential if the code is to be taken seriously both within the electronics industry and without. Outsiders will be monitoring this process. Make no mistake about it. At least one human rights group – the Catholic Agency for Overseas Development – is already waiting to see how the code will be enforced. PR will go negative if it is concluded that the code is mere window dressing.