![]()

![]()

Until recently, Russia had remained an outermost blip on most radar screens in the EMS industry. Despite the country’s large population and adoption of a market economy, Russia managed to attract from the global EMS industry just one manufacturing operation, and a small one at that, since 1997. But today, several developments are making a case that Russia should be taken more seriously as a potential location for EMS.

First, and perhaps foremost, Elcoteq (Espoo, Finland), the only EMS provider to enter Russia, just enlarged its Russian footprint significantly. Last month, the company officially launched in St. Petersburg a new 14,700-m2 facility, which is about five times larger than the Elcoteq’s original plant there. Currently staffed with about 290 workers, the new St. Petersburg factory is expected to employ about 1,500 people at full capacity. Elcoteq told MMI that it plans to reach this employee count by the end of 2006.

So far, the company has spent about 25 million euros on the new plant. This investment includes land, plant construction and utilities, and some equipment.

Secondly, Elcoteq is not the only global provider with designs on Russia, if a report from Russia is true. A Foxconn official in Russia told Vedomosti, a Russian business newspaper, that Foxconn will start production in Russia in 2008 as part of a planned investment of up to $2 billion in the country, according to a Russian news website, MosNews.com.

Finally, Russia has been dubbed one of the four major emerging markets in the world. The other three – Brazil, China and India – have already been penetrated by global providers. Like the other three, Russia has enjoyed a fast growing market in wireless telecom. As of Q2, Russia had about 100 million cellular subscribers, which amounted to annual growth of 94%, according to data supplied by Elcoteq. (Penetration was a surprising 69%.) Russia also ranks among the five countries with the highest growth in GSM traffic.

With an average annual growth rate of 6.5% from 1998 to 2004, Russia’s economy has also drawn investment from other quarters, particularly the automotive industry.

For Elcoteq, the attraction of Russia is twofold. “We see this as both an emerging market as well as a low-labor-cost country, which is very close to the Western European markets,” said Jan Lindholm, Elcoteq’s director of group marketing. Both of these aspects supplied motivation for building the new plant, and the plant’s dual mission encompasses both.

One function of the plant is to manufacture products for Western OEMs who want to supply the emerging Russian market. With some products, local content is desirable. “For the telecom operators where the Russian government is a partner, the label manufactured in Russia has an added value,” said Lindholm.

The other mission is to operate as part of Elcoteq’s low-cost network of sites supplying Western Europe. Indeed, blue collar labor rates in Russia are about 60% of blue collar rates in the traditional Eastern European centers for manufacturing, according to Lindholm. China’s rates are lower at around 40% of the Eastern European level. Still, with the St. Petersburg plant “you almost have Chinese cost level about 100 miles from the European border,” he said.

Products manufactured by the St. Petersburg operation include handset accessories, modems, and boards for WLAN and other network customers. The operation has also been doing systems integration for a major OEM. Although Elcoteq is not currently manufacturing cell phones in Russia, the company intends to add them to the new plant’s portfolio. According to Lindholm, Elcoteq is negotiating with existing customers to start manufacturing mobile phones in St. Petersburg. The communications-focused company is not only seeking high-volume handset and accessories business for the plant; Elcoteq is also targeting network equipment programs such as system integration and base-station plug-in units as well as business that is in line with current production.

St. Petersburg offers Elcoteq several advantages. For one thing, the city is about 250 miles from customer locations in Helsinki, Finland; Tallinn, Estonia; and Stockholm, Sweden. As the former RF capital of Soviet Russia, St. Petersburg also has a concentration of microwave and other RF expertise. Some 23 technical universities in St. Petersburg feed its pool of technical talent. To illustrate the high level of education there, 41% of Elcoteq’s employees in the city have master’s degrees, and 88% have attended professional schools or college. What’s more, Elcoteq has engaged two universities and three colleges to provide facilities and personnel for training employees.

Elcoteq and other Western companies are popular places to work, said Lindholm, because the young, educated workers are eager to learn. The company has found that people in St. Petersburg, Russian’s traditional gateway to the West, are open to new ideas.

But operating in Russia is not without challenges. Companies must contend with the country’s bureaucracy, a vestige of many years of Communist rule. Elcoteq has been working with Russian officials for some eight years to overcome this obstacle. For example, Elcoteq is one of two companies (the other is dairy firm) granted “green corridor” status by Russian authorities. This means Elcoteq does not have to declare the St. Petersburg plant’s outbound products at the border so trucks carrying these goods avoid customs delays. Under the green corridor arrangement, Elcoteq can do customs declarations at the plant.

The green corridor is part of a special logistics process that Elcoteq set up for the St. Petersburg operation. This process extends to inbound components as well. Under a temporary license, the company brings components by truck from a hub in Finland to the Russian plant without paying any duties or taxes. Exported goods are trucked back to the hub in Finland. Elcoteq does not pay duties or taxes when moving goods in or out of Russia.

Developing countries like Russia present another challenge. They typically do not possess the infrastructure or supply base that one takes for granted in the developed world. In Russia, Elcoteq is limited to sourcing things such as packing material. So the company is encouraging suppliers to manufacture locally in Russia items such as sheet metal, die cast parts and plastics, which have higher transportation costs.

When it comes to Russia, corruption often surfaces as a concern. Even Russian President Vladimir Putin recently acknowledged that corruption continues to be a serious problem in Russia, as reported by RIA Novosti news service. Like many Western companies, Elcoteq has a strict policy against “backhanders,” or payoffs. “We have had our share of these issues, but when those who demand special favors actually see that we are not giving them, then sooner or later they give up,” said Lindholm. He added, “I wouldn’t say that we have any major problems with corruption more than you have in the other developing countries.”

Now that Elcoteq has upped its investment in Russia, it is natural to ask if global competitors will see Russia as their next move in Eastern Europe. “This is such an interesting market that I expect others to come in,” said Lindholm. Aside from the aforementioned report on Foxconn, no tier-one provider has disclosed whether it plans to enter Russia.

Nevertheless, MMI recently came across one EMS executive in Europe who shared his view of Russia. In a June interview, Michel Charriau, Jabil Circuit’s senior adviser – Europe, told MMI that in his opinion it was time to start exploring Russia as Jabil’s next step in Eastern Europe. He stressed this was his personal view, not a company position. In countries such as Russia, “you cannot move very fast. You better move carefully and learn your way. If it’s a long process, the earlier you start the process, the better [off] you are,” said Charriau.

Elcoteq believes that its eight years of experience in Russia give the company a head start on the competition.

Providers who do take the plunge into Russia will find an electronics market estimated at $1 billion, of which 20 to 25% comes from Russian companies, RIA Novosti reported citing an official from Russia’s Federal Industries Agency. Outsourcing from Russian companies is in its early stages. “The question whether to make or buy is like where the Western markets were 10 to 15 years ago,” said Lindholm. Elcoteq wants to provide its global network to Russian companies, but so far it has one domestic Russian customer, which exports only to countries that were part of the Soviet Union.

While Russia will afford providers labor rates that are among the lowest in Europe, they are probably not the very lowest. OEMs looking for rock-bottom rates may find lower blue collar costs in places such as Ukraine and Romania. But Lindholm argued that once you take the productivity in St. Petersburg into account, product costs will end up in the same range.

As always, OEMs will have the final say as to whether Russia emerges as a major EMS center in Eastern Europe. EMS providers do not put up plants on spec. If OEMs are just looking for the lowest labor costs in Europe, then Russia will have competition from other countries in Eastern Europe. But if OEMs need to deliver product to Russia and Western Europe, a Russian EMS site would kill two birds with one stone, as the saying goes.

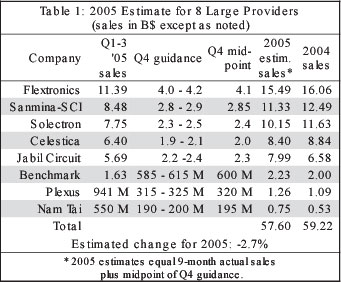

2005 will end up a lackluster year for the US-traded sector of the EMS industry. Nine-month sales for the nine largest US-listed providers declined overall by 2.3%. What’s more, evidence is building that the US-traded sector will see a dip in collective sales once results are tallied for 2005. Full-year estimates based on Q4 guidance for eight of the nine companies show a 2.7% decrease in aggregate sales for the eight providers (Table 1).

To arrive at 2005 estimates, MMI added the midpoint of Q4 guidance for each company to its sales for the first nine months. (One large provider, PEMSTAR, was left out because Q4 guidance and reported Q4 2004 revenue are not comparable.) Even if one took the high end of the guidance range in each case, collective sales for 2005 would still fall short of the 2004 total by 1.9%.

These 2005 estimates reveal an interesting divide. The four largest providers are all projected to have down years. This finding holds true at the high-end of Q4 guidance as well as at the midpoint. In contrast, estimated 2005 sales for the four smaller providers in this analysis (Table 1) point to an up year for all of them. When it comes to sales growth in 2005, apparently bigger is not better for US-traded companies.

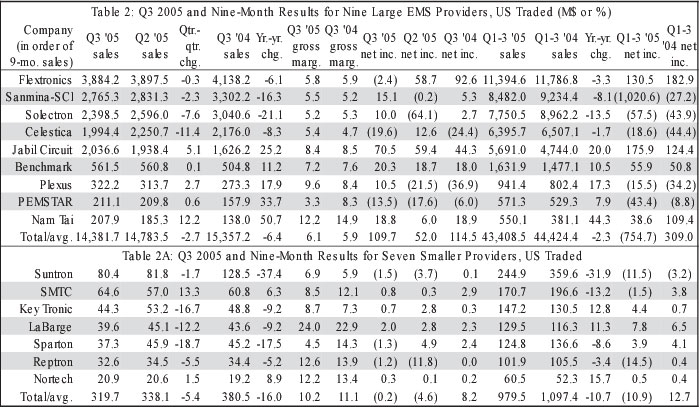

For the first nine months of 2005, the nine largest US-traded providers accounted for sales of $43.41 billion, down 2.3% from $44.42 billion in the year-ago period (Table 2). As a group, these companies accounted for a three-quarter net loss of $754.7 million in 2005, compared with net income of $309.0 million a year earlier. However, without Sanmina-SCI’s nine-month loss of $1.02 billion, which included one-time charges of $979 million in Q1, the group would have earned net income of $265.9 million.

Q3 sales for the group of nine decreased 2.7% sequentially and 6.4% year over year (Table 2). Net income for the quarter was down 4.2% from a year earlier, but was up 111.0% from the prior quarter. Overall gross margin for Q3 improved to 6.1% from 5.9% in the year-ago quarter.

Seven smaller US-traded providers did not provide any net offset to the collective sales decline reported by the nine large providers for the first nine months of 2005. In fact, aggregate sales for the smaller companies dipped by a greater percentage. Nine-month sales for these seven smaller providers totaled $979.5 million, a drop of 10.7% from the year-earlier period (Table 2A). Together, these smaller companies produced a net loss of $10.9 million in the first nine months of 2005, after combining for net income of $12.7 in the same period last year.

These smaller providers do have at least one advantage over the large US-traded players. As a group, the smaller companies enjoy a higher gross margin overall. For Q3 2005, they combined for a gross margin of 10.2%, below the year-earlier level of 11.1%, but still well above the large providers’ margin of 6.1%. Despite a double-digit gross margin for Q3, the small provider group as a whole was unable to break into the black.

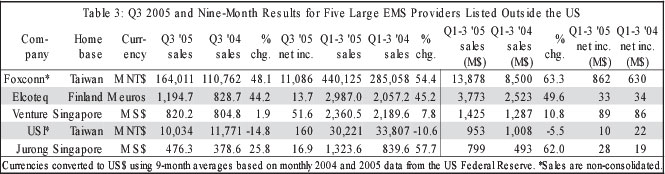

Still, 2005 sales in the US-traded sector of the EMS industry do not necessarily reflect growth of the industry at large. For the first nine months, sales growth at five large providers listed outside the US was well above what their US-traded peers achieved (Table 3). In three out of five cases, sales growth for the period exceeded 40%. When converted into US dollars, these increases also received a boost from the currency effect of a weaker US dollar. (Sales were converted into US dollars by using nine-month average exchange rates for 2004 and 2005 based on monthly data from the US Federal Reserve.) Together, the five non-US listed providers accounted for a nine-month sales increase of 50.8% in US dollars. This gain largely stems from the results of one company, Taiwan’s Foxconn (the trade name for Hon Hai Precision Industry), whose non-consolidated sales for the period climbed 63.3% in US dollars (54.4% in Taiwan dollars).

Combined net income for the five non-US providers, however, did not keep apace with sales growth in the first nine months. Their net income rose 29.0% in US dollars, more than 20 percentage points below sales growth.

This non-US sales growth pushed combined growth for the large EMS providers in MMI’s analysis into double-digits. Aggregate sales for the 14 large publicly traded providers grew by 10.3% in the first nine months. Their revenue for the period totaled $64.24 billion, easily a majority of EMS industry sales at somewhere around 70%. So despite the anemic performance of the US-traded sector, a large portion of the industry will likely end the year with respectable growth – double digits if the nine-month growth rate holds up in Q4.

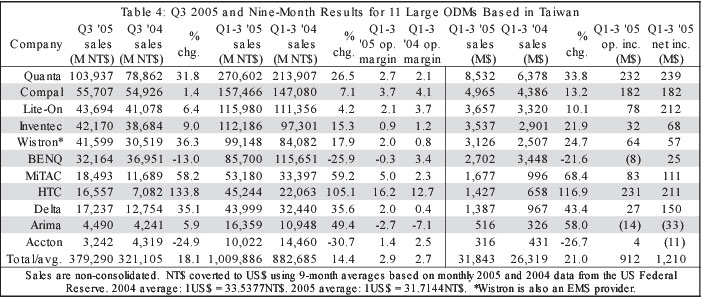

But the outsourcing picture brightens even more when ODM contributions are added. For the first nine months, 11 of the largest Taiwanese ODMs produced collective sales growth of 14.4% in Taiwan dollars, or 21.0% in US dollars (Table 4). Year-over-year growth picked up in Q3, as the ODM group’s sales for Q3 increased by 18.1% over the year-earlier quarter.

Operating margin for the group, while nothing to boast about, did improve overall. Nine-month margin increased to a combined 2.9% in 2005 from 2.7% in 2004. Interestingly, the ODM group earned more net income (US$1.21 billion) in the first nine months of 2005 than operating income (US$921 million). For ODMs, non-operating income can be significant.

Combining ODM sales with revenue from the EMS group yields a nine-month total of $96.08 billion, which grew 13.6% over the year-ago period. This combined growth rate for 14 large EMS providers and 11 large ODMs shows that outsourcing remains alive and well despite lackluster sales to date in the US-traded sector of the EMS industry.

Celestica (Toronto, Canada) has acquired Displaytronix (Oxnard, CA), a provider of flat-panel display repair services, in a move to add capability to Celestica’s after-market services offering. The deal also trains a spotlight on Celestica’s After-Market Services unit, carved out just over a year ago as a separate business within the company. Financial details were not released.

Serving the LCD and plasma display market, Displaytronix provides repair services for flat-panel display devices such as notebook computers, flat-panel monitors, high-definition TVs and handhelds. The privately held company operates with about 13,000 ft2 and just over 60 employees in its California facility. Both OEMs and ODMs receive in- and out-of-warranty support from Displaytronix. One customer is Siemens, who uses Displaytronix as the preferred partner for Siemens’ worldwide LCD repair requirements.

Although Celestica picked up repair capabilities in past acquisitions, this is the company’s first stand-alone acquisition of a repair business. The deal will allow Celestica to do its own LCD remanufacturing, rather than rely on LCD subcontractors as it had been doing in order to fulfill contracts for PC repair. By bringing LCD work in house, “we can ensure higher quality standards. We can take more control of the supply chain and add more value to our customer,” said Bert Pendergast, VP, After-Market Services, Celestica. “So it was a capability play, if you will, so that we’re more full serviced to our customer. And we’ll continue that as a business.”

Utilizing the newly acquired capability, Celestica plans to set up an LCD remanufacturing center in each of the three major world markets. The first LCD center will go into a North American site in Mexico. A center in the Czech Republic will serve as the European solution for LCD remanufacturing, and LCD capability will also be deployed to a low-cost region in Asia. These centers will handle bulk remanufacturing of LCDs, which can then be shipped to country-specific sites performing whole-unit repair.

The After-Market Services unit operates 14 repair sites worldwide, employing some 3500 people. Celestica’s after-market business extends well beyond the PCBA repair activities of its past. Today, the unit repairs products such as notebooks, set-top boxes, cell phones, handhelds and printers. Celestica is offering after-market services as part of an integrated solution to its largest accounts with the idea of feeding fault data back into design. The after-market unit is also free to sell its services to non-EMS customers. Services include returns management, repair, remanufacturing, refurbishment, rekitting, recovery, and recycling.

According to Celestica’s Pendergast, the latest estimates put total demand for after-market services at about $18 billion, of which less than 50% is outsourced. The outsourced portion is largely populated by many small repair companies – “hundreds and hundreds and hundreds,” said Pendergast – which specialize in one product in a single region. He said customers are telling Celestica that they would rather sign a global contract than rely on the current system of small repair vendors. Managing these small vendors creates SG&A expense, and consolidating parts from various vendors drives up logistics costs. In contrast, a global contract providing local repair requires a single vendor manager. And Celestica takes responsibility for repair of the product and its components. “They’re relying on us either to do it all ourselves, or then we have subcontractor relationships where we don’t have the technology in house to do it for them,” said Pendergast. This need for a global contract becomes a market opportunity for Celestica and other providers with a global footprint for repair.

Global providers such as Jabil Circuit and Solectron have emphasized post-manufacturing services in recent years, and as a result, have gained visibility in this area. Is Celestica behind them in terms of branding an after-market services business? “That’s a fair comment. Talk to me in 12 months. We hope to be the industry leader,” said Pendergast.

Flextronics makes a mechanicals deal…Flextronics (Singapore) acquired a Brazilian enclosure operation in Q3.

Venture withdraws from a deal on the mechanicals side…Univac Precision Engineering, a subsidiary of 2004 top-ten provider Venture (Singapore), will not carry out the proposed acquisition of SEB Corporation (Singapore). (See Sept., p. 3.) Negotiations failed to produce a definitive agreement that would allow Univac to purchase the remaining shares of SEB. But Univac did put up $110,000 to take a 52% interest in a new subsidiary, Hartec Asia (Singapore), established to provide products and services involving nano technology.

Jurong in a mechanicals alliance…Through a subsidiary, EMS provider Jurong Technologies Industrial (Singapore) has entered into a memorandum of understanding with China Precision Technology (CPT), a Chinese supplier of metal and plastic components, for the purpose of forming an alliance between the two parties. Under the MOU, each company will act as the preferred subcontractor to the other and its respective customer base. Also, the MOU contemplates that CPT and Jurong in collaboration with other partners will jointly carry out product development for ODM plasma display panels and LCD products as well as other products such as Bluetooth headsets, global positioning systems and antenna modules for telecom products.

Vansco Electronics LP (Winnipeg, Manitoba, Canada), which focuses on the heavy equipment market, gained an EMS foothold in Europe with its acquisition of Mitron Oy assets in Finland. The Canadian company bought the assets of Mitron’s Automotive Electronics, Forest Systems and Bus Sign businesses, all of which are located primarily in Forssa, Finland.

These divisions together employ about 95 people in R&D, administration and production. Vansco expects to offer jobs to all of them and plans to grow the work force as it brings in additional business. The acquired operations design and manufacture electronic products for forestry, bus and mobile equipment manufacturers. Production runs are characterized by low to medium volumes and high mix.

This is Vansco’s second acquisition in 2005. Earlier, the company purchased Preco Electronics’ EMS operation in Morton, IL (June, p. 6-7).

Vansco has grown to more than 1,000 employees and over C$200 million ($171 million) in sales.

Jaltek acquires design house…UK EMS provider Jaltek Systems (Luton, England) has acquired Abra Cad, a contract design house with whom Jaltek had a four-year alliance. In addition, Jaltek recently announced an alliance with NOTE AB, a provider based in Sweden. Under this arrangement, Jaltek will offer NPI and low-volume assembly in England, while NOTE operations in Lithuania and Estonia will handle higher volumes.

New programs…Under a new contract, Sanmina-SCI (San Jose, CA) will provide manufacturing capacity for QuVIS (Topeka, KS), a supplier of high-fidelity motion imaging technol-ogy….Photo-Me International (Bookham, England) has selected Solectron (Milpitas) to manufacture PMI’s new generation of digital photo minilabs….According to an online report by Scotland’s The Herald newspaper, HP is outsourcing work from its Erskine, Scotland, plant to a Foxconn site in Pardubice, Czech Republic. Also, InFocus (Wilsonville, OR), a maker of digital projectors and display products, has revealed that Foxconn (the trade name for Taiwan’s Hon Hai Precision Industry) is the other beneficiary of InFocus’ previously announced decision to end its relationship with Flextronics (Aug., p. 6). InFocus said it will complete its contract manufacturing transition from Flextronics to Foxconn and South Mountain Technologies, InFocus’ joint venture with China’s TCL, in Q4. Funai Electric, InFocus’ existing contract manufacturer, will stay in the OEM’s supply base….PEMSTAR (Rochester, MN) has landed new programs with SpectraLink (Boulder, CO), a company in the workplace Wi-Fi telephony space, and with FinePoint Innovations (Phoenix, AZ), a supplier of pen input components and a subsidiary of InPlay Technologies.…Nam Tai Electronics (Tortola, British Virgin Islands) has won a new order from Sony Computer Entertainment Europe to build new USB buzzers for a series of interactive quiz games on Sony’s PlayStation 2....Raytheon-Network Centric Systems has awarded Sparton (Jackson, MI) a $2-million contract to produce PCB assemblies for an airborne interrogator system, selected by the US Air Force and the UK Royal Air Force.…Nortech Systems (Wayzata, MN) has received an order from GE Rail to supply components for a video camera system….SmarTire Systems (Richmond, BC, Canada) has entered into a manufacturing agreement with Vansco Electronics, which will produce SmarTire’s tire transmitter products in Vansco’s recently acquired Morton, IL, facility. This contract expands the companies’ current relationship. In addition, SmarTire’s EMS agreement with a Korean company, Hyundai Autonet Company, ended with the acquisition of that company by Hyundai.….In Q3, DRS Technologies (Parsippany, NJ) booked $60 million in EMS contracts, primarily associated with the US Army’s Bradley vehicles, international F/A-18 aircraft, and US Navy display systems.…EMS provider Irvine Electronics (Irvine, CA) has secured a multimillion-dollar contract from DRS to supply PCB assemblies for the US military’s Driver’s Vision Enhancer program.…LaBarge (St. Louis, MO) has won a $2.2-million contract from BAE Systems to produce Ethernet switch units for Bradley combat vehicles. Also, Boeing has awarded LaBarge an additional $2.2-million contract to continue to supply wire harness assemblies for US Air Force training jets….Winland Electronics (Mankato, MN) recently added a new medical customer, Cardiac Science (Bothell, WA).

Facility investments…In Shanghai, China, Flextronics recently set up a factory focused on the mechanical portion of notebook production. Flextronics Software Systems, of which Flextronics owns 88%, has launched its first software development center in China; the new center is located in the city of Beijing….Construction of Jurong Technologies’ new facility in Suzhou, China, is underway, and the facility is expected to be ready near the end of Q1 2006. Also, the company has set up a new joint-venture facility in Bangkok, Thailand, to support customers in the hard disk drive industry. Finally, Jurong plans to open a new plant in Jaguariuna, Brazil, with a production area of 50,000 ft2.…Minnetronix, which specializes in contract design and manufacturing for medical devices, will add 24,500 ft2 to its Saint Paul, MN, facility to meet increasing demand for its services. The addition, expected to be in operation by July 2006, will more than double the company’s current space. With 90 employees, Minnetronix serves clients including St. Jude Medical, Possis, Medtronic, CardioFocus, Orqis Medical, Terumo, Arrow International and the Cleveland Clinic.…According to reports from India, Avalon Technologies, a subsidiary of EMS provider Sienna Corporation (Fremont, CA), has opened its fourth plant at the Madras Export Processing Zone in Chennai, India.

Some financial news…Foxconn subsidiaries have taken a combined 11.57% stake in Taiwan’s CyberTAN Technology, a home networking equipment manufacturer offering ODM/OEM services….Fitch Ratings has revised its rating outlook on Flextronics to negative from stable. This outlook reflects Flextronics’ expectations for lower organic growth, Fitch’s belief that the company will be challenged to meet near-term operating margin targets, and the potential use of high cash balances for shareholder-friendly transactions and/or acquisitions….Solectron’s board has authorized the company to repurchase up to $250 million worth of its common stock over a 12-month period starting in the February 2006 quarter….Nam Tai Electronics intends to privatize two Hong Kong-listed subsidiaries, Nam Tai Electronic & Electrical Products and J.I.C. Technology Company in which it holds a 69.50% and 71.63% interest respectively. The total cost of privatizing both is estimated at about $75 million. …Sparton declared a 5% stock dividend at its annual meeting last month.…The Electronic Contract Assemblies segment of Kimball International (Jasper, IN) generated September quarter sales of $108.0 million, which were flat compared with sales of $107.9 million in the year-earlier quarter. Segment income from continuing operations in the September quarter decreased $2.0 million from the same period last year….The EMS segment of CTS Corporation (Elkhart, IN) saw its Q3 sales increase 35% year over year to $89.1 million, primarily from the SMTEK acquisition. Segment operating earnings for Q3 were $2.1 million, up from $1.3 million in the year-earlier quarter.

People on the move…Elcoteq (Espoo, Finland) has appointed Anssi Korhonen senior VP, product development services. His most recent position at Elcoteq was head of the terminal products business….Western Elec-tronics (Meridian, ID) has named Robert Subia president and COO....Suntron (Phoenix, AZ) has restructured its board of directors. Added to the board are Scott Rued, managing partner of Thayer Capital Partners, and Kurt Grindstaff, a financial consultant. Gone from the board are Chairman Jeffrey Goettman, James Van Horne, Jesse Hermann and Enrique Zambrano....Libra Industries (Mentor, OH) has named Patrick Leber its new materials manager.

As the article on page 3 points out, the US-traded sector of the EMS industry will likely end 2005 with a sales decline. How can this be? After all, the downturn is well behind the industry now. And there’s a lot of product still to be outsourced. You can argue whether outsourcing penetration is above 20% or below it, but whatever the real number is, it’s low. Low enough to propel growth well into the foreseeable future. The question of what happened to the sector this year becomes even more perplexing when you consider that the sector grew by about 20% in 2004.

Then again, maybe part of the answer actually lies in that 2004 number, which exceeded forecasts for the industry. Sector growth in 2005 will obviously come in below industry expectations. But over two years, growth will average out in the high single digits, which isn’t far from forecasted CAGR for the EMS industry. The variation from 2004 to 2005 shows that outsourcing still exhibits a degree of “lumpiness” from year to year. Some of this unevenness might be caused by a few major events acting in one direction or the other. For example, two major cell-phone customers of Flextronics, Alcatel and Siemens, divested their handset businesses to other companies. These actions cost Flextronics over a billion dollars in revenue for its fiscal year ending in March 2006.

Also realize that a substantial portion of 2005 revenue originated with program wins in 2004. As the industry knows, it can take six to nine months or even longer to turn on revenue from a contract win. So an analysis of 2005 should also focus on what was happening in 2004. It’s hard to know for sure whether there was a lull in outsourcing last year. Few contract wins are ever spelled out in any detail. But only one mega win, Flextronics’ pact with Nortel, was announced in 2004.

Another plausible reason for the sales decline is competition from outside the US-traded sector of the EMS industry. This threat comes in not one or two, but three forms. There are, of course, the EMS providers based in Asia and to some extent Europe. Taiwan’s Foxconn, which maintains high growth in spite of its size, is a prime example. Another group siphoning off outsourcing dollars consists of ODMs, no longer strangers to the EMS industry. Now, a third wave of competitors is emerging – Asian manufacturers that combine EMS with other businesses. Asustek, which has announced plans to separate its manufacturing and branded-product businesses, is a case in point. A number of Chinese companies also fall into this category (June, p. 3-4).

Despite a disappointing 2005 for the US-traded sector, one can come up with reasons for the sales decline. One hopes that US-traded companies are already close to having enough wins to bring them back to respectable growth in 2006. Otherwise, there will be concerns about the US-traded sector winning its fair share.