Cover Story

Outsourcing Pipeline Opening Up

Market Data

Researchers Update EMS Forecasts

Market Makers

Q&A with Bill Mitchell of Solectron Global Services

News

Distributor Warns Against Buy-Back Scheme

Outsourcing Poll Proves Positive

From the early stages of the downturn, tier-one providers have spoken of a large pipeline of major outsourcing deals being proposed. But throughout the spring and summer, there was little evidence of that pipeline. The outsourcing of two Lucent operations to Celestica and Flextronics' agreement with 3Com were about the only major news during that period. Observers began to wonder why so little had appeared from the pipeline, given its purported size. Still, providers pointed out that these deals are complicated, requiring lots of time to iron out. For a number of deals, that waiting period is now over, as the pipeline has recently shown signs that it is beginning to flow.

Bear Stearns analyst Thomas Hopkins counted up 14 deals announced from September to mid October and estimated their annual value at $3.3 billion. Some of the biggest deals have gone to two tier-one providers, Flextronics and SCI Systems.

#On Oct. 2, Flextronics said it will buy from Xerox office manufacturing operations in Toronto, Canada; Resende, Brazil; Aguascalientes, Mexico; and Penang, Malaysia. Some 3650 Xerox employees in these operations are expected to join Flextronics. In addition, Xerox intends to sell to Flextronics an office manufacturing operation in Venray, The Netherlands, after consultations with European works councils. The deal is worth about $1 billion in estimated annual revenue to Flextronics, which will receive a five-year manufacturing contract. The provider will pay about $220 million, which includes a modest premium over book value. The agreement represents about 50% of Xerox's overall manufacturing operations.

In discussions with Flextronics, Xerox agreed to discontinue operations that did not have a future at Flextronics. So Xerox will close its PCB assembly factory in El Segundo, CA, and its customer replaceable unit plant in Utica, NY, and move the work at both locations to Flextronics operations in Mexico.

Flextronics will pick up somewhere around 1.4 million ft2, largely for final assembly type work. According to the company, asset transfers will most likely take place between November 2001 and February 2002.

What's more, Flextronics intends to build a lot of the PCB assemblies now being produced at Xerox's site in Mitcheldean, England. The transfer of this work would also follow works council consultations.

Five days before the Xerox deal went public, Flextronics announced another, albeit smaller, program. The provider is taking over the manufacture of Hewlett-Packard's large-format printers in Singapore along with about 250 HP employees. Flextronics is occupying about 70,000 ft2 within HP's campus there.

#Then there's SCI, which has just landed two deals with combined first-year revenues estimated at about $1.1 billion. In the largest of the two, SCI has entered into an agreement to acquire IBM's Yasu, Japan operations for card design and product/test engineering and EMS. SCI estimates that first-year revenue of the multiyear agreement will exceed $700 million. The provider will support IBM's Storage Technology and Personal Computer Divisions, including mobile computing products. SCI will design and manufacture electronic cards for IBM and its customers as an IBM-preferred supplier. Revealed on Oct. 1, this deal marks the second divestiture of a Japanese operation to a tier-one provider after Solectron's acquisition of a Sony operation.

Under the other deal, announced on Sept. 20, Nortel intends to outsource its remaining PCB assembly activities to SCI. The provider will acquire those activities, which are located in Nortel's Systems Houses in St. Laurent, Quebec, Canada, and Monkstown, Northern Ireland. The deal includes the sale of equipment and inventory. In addition, Nortel will extend its master supply agreement with SCI, which covers existing PCBA services. These multiyear agreements will generate first-year revenue estimated to be in the range of $400 million.

The North American part of the deal is expected to close in Q3 or early in Q4, and the European portion in Q4.

Also, SCI has revealed that in an agreement signed earlier this year, it assumed supply chain management, box build, configuration, system test, and order fulfillment for certain of Nortel's Enterprise products. SCI will handle these activities, previously performed by Nortel's Systems House in Billerica, MA, from SCI's Canadian operations.

#On Oct. 3, Nortel disclosed yet another outsourcing agreement. The company has agreed to divest to C-MAC Industries the majority of Nortel's manufacturing activities for system integration, configuration and testing of its DMS circuit-switching products. C-MAC will buy most of the DMS-related manufacturing activities currently performed in Nortel's Systems House in Research Triangle Park, NC. Nortel also intends to divest to C-MAC similar activities within its Systems House in Monkstown, Northern Ireland.

These operations will be transferred to C-MAC's operations in Creedmoor, NC, and Carrickfergus, Northern Ireland. C-MAC will provide fully configured DMS switching products to Nortel distribution centers and customer sites worldwide.

The deal, which includes the sale of equipment and inventory, is expected to close in Q4. Ultimately, the deal will benefit Solectron, if its proposed merger with C-MAC goes through (Aug., p. 1-2).

#But Solectron has also landed a high-profile deal of its own. On Oct. 15, the company announced that its Global Services business unit will handle all repair and refurbishment for the Microsoft Xbox video game console in North America. (See related article on p. 4.) Solectron will also do production monitoring and quality assurance for production of the Xbox. As the world knows, Flextronics is manufacturing that product for Microsoft.

#Last month, Jabil Circuit said it has signed a three-year agreement with Intel to assume production of certain peripheral products. As part of this deal, Jabil will purchase a 150,000-ft2 facility in Penang, Malaysia, from Intel, which obtained the operation as part of its acquisition of Xircom. The operation will add about 900 people, and Jabil will buy assets including inventory and buildings. Closing is expected in Jabil's fiscal Q1 2002.

Other programs won by Jabil in recent months include designation as a principal worldwide supplier for Agilent Technologies and a set-top box contract from Hughes.

The pipeline may also include work for Taiwanese companies that do EMS or ODM work. DigiTimes.com, a source of electronic industry news in Asia, is reporting that Sony is expected to outsource 18 to 20 million units of its PlayStation 2 game console to two Taiwanese companies - Asustek and Hon Hai Precision Industry Co., better known by its Foxconn trade name. (See also June, p. 3). According to this source, Sony will give 7 to 8 million units to Asustek and the remainder to Foxconn. Note that MMI has not confirmed this report, and it differs from information published in the online edition of the Taipei Times.

How big is the pipeline? Veteran EMS analyst Alex Blanton of Ingalls & Snyder estimates that outsourcing being negotiated by the top tier is worth at least $20 to $30 billion a year. He expects outsourcing from Alcatel, Hitachi, Lucent, Motorola, Nortel, NEC, Siemens and Sony.

Bear Stearns' Thomas Hopkins has some of those names on his list of pipeline OEMs. He singles out Aiwa/Sony, Alcatel, Hitachi, Philips, Siemens, and Toshiba. Earlier in the year, Bear Stearns had forecasted $20 billion in outsourcing over the next 12 months, some of which has already come to fruition.

With end markets still in a slump, the pipeline has the potential to pull the EMS industry out of the doldrums. A flow of deals has started. Now it will be up to OEMs in all three world markets to keep it going.

Two market research firms have released their latest forecasts for the global EMS market. Shackled by the downturn, the EMS business will grow less than 5% this year, according to one firm, or dip into slight decline, predicts another.

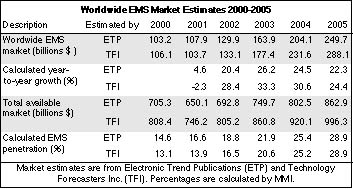

A new market report from Electronic Trend Publications (ETP, San Jose, CA) estimates that the EMS market worldwide will reach $107.9 billion in 2001, up just 4.6% from $103.2 billion in 2000. The other firm, Technology Forecasters, Inc. (TFI, Alameda, CA), forecasts a 2.3% dip from $106.1 billion last year to $103.7 billion for 2001.

The ETP study, entitled The Worldwide Contract Electronics Manufacturing Services Market, Eight Edition, still paints an optimistic picture for the longer term, with CAGR (compound annual growth rate) forecasted at about 19% over the next five years through 2005. Still, the report expects growth to be nonlinear, as indicated by first half results of this year. This year's anemic growth will be followed by a strong recovery in 2002 and 2003. Subsequent growth will be strong but at somewhat lower rates, the study predicts.

Next year, the EMS market will hit $129.9 billion and grow by 20%, according to the ETP report. The market will then rise to $163.9 billion in 2003, representing a 26% increase, and reach $249.7 billion in 2005 (see table). As for TFI, the company predicts that by 2005, total EMS revenue will reach $288.1 billion.

"It is believed that many of the newly implemented outsourcing programs by lagging OEMs such as Alcatel, Lucent, Motorola, Nokia, and Siemens will hit their full potential in the latter part of the forecast period after 2002," the ETP report notes. Also, the study finds that many assembly opportunities in the transportation and industrial/medical sectors will soon begin to materialize.

What's more, TFI reports that nearly all of its OEM clients "are aggressively increasing their outsourcing strategy."

As one would expect, the ETP study projects box build, at a 22.7% CAGR, growing faster than PCB assembly, at a 17.8% CAGR over the 2000-2005 forecast period. So box build will account for 34% of all industry revenue by 2005, compared with 30% share in 2000.

Turning to world markets, North America will see its market share decline to 53% in 2005 from 58% in 2000, according to the ETP report. It also forecasts that Asia's share of the EMS business will increase from 17% in 2000 to 23% in 2005. Europe's slice of the market will dip slightly from 23% to 22% over the forecast period. Though the rest of world's share will remain unchanged at 2% in 2005, the study expects that ROW regions such as Australia, Israel and India will experience higher than average growth as a result of new demand for local capability within these countries.

With regard to end markets, the ETP study predicts that the computer/office and communications segments will expand at similar rates, but lose some market share. From 2000 to 2005, the computer/office share will decline from 43% of the EMS market to 40%, and the communications portion will contract from 42% to 39%. Each segment will maintain roughly equal shares.

Some of the highest growth rates are expected within two of the smaller pieces of the EMS pie - automotive and military/avionics. Take automotive. The ETP report estimates that the automotive slice will grow from 1% of the EMS market last year to 4% in 2005. Military/avionics will expand from 2% in 2000 to 5% in 2005. ETP has the consumer and industrial/medical segments holding steady at 5% and 7% respectively.

To assess the performance of EMS providers, the ETP study assigned a rating based on the weighted values of various financial metrics. For the fourth time in a row, Jabil Circuit earned the highest rating.

According to ETP data, EMS penetration of the total available market stood at 14.6% in 2000 and will rise to 28.9% by 2005. TFI data yields an EMS penetration rate of 13.1% in 2000, also increasing to 28.9% by 2005.

But the EMS market does not capture all the outsourcing done by OEMs, as MMI has pointed out (Aug., p. 8). In addition, there is OEM-to-OEM outsourcing, led by computer OEMs who often use other OEMs to supply items such as motherboards, memory modules, disk drives, power supplies and monitors. The ETP report shows "OEM-to-OEM outsourcing is still larger than the CEMS market. Thus, total outsourcing is already 30% and will grow to 45-50% by 2005," says Steve Berry, ETP's publisher.

Another overlooked area is outsourcing to original design manufacturers, or ODMs. Although TFI's EMS numbers do not include ODM revenue, TFI has broadened its forecasts of total outsourcing to include the ODM space. The firm will hold a discussion of the ODM market in its next Quarterly Forum for Electronics Manufacturing Outsourcing and Supply Chain.

For information on the web, go to www.electronictrendpubs.com for ETP and www.techforecasters.com for TFI.

Solectron recently made a move to add a new capability for its postmanufacturing services arm, Solectron Global Services. This new capability, called customer relationship management, or CRM, may well be a first for the EMS industry. At least Solectron believes it is.

The company intends to acquire Stream International, billed as one of the world's ten largest providers of CRM services. Stream brings 22 contact centers in North America, Asia and Europe and about 10,000 employees. For 2000, Stream generated sales of $323 million, up 37% from a year earlier. The companies expect to complete the deal by the end of this month.

What does CRM have to do with Solectron Global Services and its offerings for the after-sales market? To find out, MMI interviewed Bill Mitchell, executive VP and president, Solectron Global Services. Mitchell came to Solectron about 2 1/2 years ago with its acquisition of Sequel, a repair services company, where he served as CEO. That acquisition led to the formation of Solectron Global Services, which Mitchell has directed from the start.

MMI took this interview opportunity not only to explore CRM, but also to learn more about Global Services and its market.

MMI: As a service offering, CRM is not often mentioned in the EMS industry. Why is CRM so important to your business?

Bill Mitchell: Let me take you back a little bit. We started Solectron Global Services a little more than two years ago, in July of 1999 to be exact. It's part of the overall vision that Ko Nishimura has had of a supply chain facilitation company that would design, build and service products throughout the product life cycle and give a complete end-to-end solution. When we formed Global Services, we laid out a strategic road map that had three dimensions to it. One dimension was: You had to be able to provide service around the world - hence, the need for a global footprint. Second, you had to be able to provide it for a wide variety of marketplaces and customers ranging from wireless to networking to computing to telecommunications and so on. And you had to have a complete set of capabilities.

At that point, Solectron had capabilities to fundamentally do repair. But repair is only one of the services that are required to maintain products in the field from the time they are manufactured until the time they're removed from service. So we put on our road map then what we think is one of the key pieces of this strategy, and that piece is call center, or CRM, capability. It's one of linking mechanisms throughout the whole product life cycle.

Think about almost any product, a notebook computer for example, and what you need to do with it from the time it's manufactured and installed. There's repair, maintenance and upgrading - all of those things that go on until ultimately that computer reaches its end of life. You might tear it down for parts or recycle it or refurbish it and upgrade it for use in a different application. So over the life of a product, there are, in fact, a whole series of different events. Within each one of those events, a series of things happen. Almost universally, they start with a call of some kind, whether it's a voice call, an email call, a scheduled maintenance event, an upgrade event or whatever says we need to do something with that product in the field. That call flows through a CRM capability, sometimes internally, sometimes externally, sometimes by email, sometimes by voice, sometimes by fax, sometimes by chat room. Sometimes people send in cocktail napkins and other kinds of things. But there's a communications link that goes in there.

For us to provide a full set of end-to-end capabilities along the product life cycle and then a full set of event capabilities from the beginning of a service event to the end of the service event, we must go through a CRM capability. So it's always been very high on our list of things that we wanted to have in house, because it's the information highway. And information is very valuable in this space.

MMI: Do you expect that other providers with after-sales offerings will move into CRM as Solectron has?

Bill Mitchell: I think we have a leadership position in this space. As of now, we haven't seen anybody come in after us. Would somebody come in behind us and try to follow us? I wouldn't be surprised.

We have a very strong first-mover advantage.

MMI: Compared with an EMS company, Stream obviously employs a lot more people to achieve the same level of sales. Yet one analyst reports that its EBIT margin is in the high single digits, nearly double Solectron's normal operating margin. What can you say about Stream's profitability?

Bill Mitchell: It does have a different revenue and profitability model. As you well recognize, with the bulk of Solectron's business there's a very large component of materials. Of course, we have no materials component in the Stream business model. It's a call center model so its ability to provide advanced CRM types of services is based on the intellectual capital of the people and the systems that we can bring to it. So it's just a different model. It is more labor intensive than other parts of Solectron.

One of the reasons we were attracted to Stream was that it does have a proven record of profitability. We continue to state that this will be accretive right from day zero. This is an accretive acquisition, and we're very, very pleased with it. We did look through the [CRM] industry, and Stream has a very strong record of both growth and profitability.

MMI: It appears that the addition of Stream will almost double your sales, based on your fiscal Q4 run rate and Stream's fiscal 2000 sales. What is the growth strategy for Global Services? Is it to grow primarily by acquisition?

Bill Mitchell: It's both. Like Solectron, it's been a combination of growing organically and by acquisition. In Global Services, we've made a number of acquisitions over the last few years, and Stream is clearly the largest. These have been aimed at filling in spots on our road map that I mentioned earlier. But they are also leverageable, because longer term we would expect about half of our growth to come by acquisition and about half of it to come by organic growth.

We've shown some very strong organic growth over the last year just in the face of what you well understand are not very attractive market conditions. In fact, virtually all of the growth between our [fiscal] 2000 and 2001 figures is organic, in the 60% range.

We look for those acquisitions that we can leverage with other capabilities we have in order to increase the rate of growth. We think Stream is a real winner there.

MMI: Would it be fair to say that of the three business units at Solectron, Global Services had the highest growth for fiscal 2001?

Bill Mitchell: On a percentage basis, that's right. We had the highest growth percentage within Solectron Corporation.

MMI: Global Services accounted for about 2.4% of Q4 sales. What is the goal for Global Services as a percentage of Solectron's sales, and when do you expect to achieve that target?

Bill Mitchell: We've been tasked to become as rapidly as possible 10% or more of Solectron's revenues and, we hope, a larger percentage of Solectron's overall profitability. When I ask my boss how long I have to do that, he says, "How about within a year or two."

To get to 10% of revenues, we need very dramatic growth rates. In fact, on the back of an envelope you can get to growth rates over 100% per annum very easily. We're on track to do that so we expect to become 10% of Solectron in a relatively short period. That's obviously contingent on a whole bunch of things that none of us have control over - market conditions, world events, etc.

Note that our business in fact has held and has strengthened first of all in the face of an economic downturn and then secondly in the face of the events of September 11. If you think about it, there's a rationale for this. The after-market deals with the installed base, while the front end, new build and new purchases, can be very volatile and clearly is in a very volatile period right now. When that gets volatile or turns down, people become a lot more interested in maintaining what they have, upgrading what they have, looking for additional services. When you're going into the cost reduction mode, you look for outsourcing opportunities. So our business tends to be somewhat countercyclical to that of the more traditional front-end manufacturing business. That is one of the reasons why personally I think it's good place to be and why Ko [Nishimura] believes it's a very strong place for Solectron to have a presence going into the future.

MMI: How large is the market opportunity for Global Services? According to Solectron, CRM alone was a $44-billion market in 2000?

Bill Mitchell: We participate in a number of studies. Dataquest and IDC, in particular, look at the marketplace, and the after-market in total is probably on the order of about $550 billion a year. It's growing at about 10%. It's a huge market. Now it's not as tightly bounded as the classic manufacturing market, where you can count up the cost of goods sold and get a pretty good idea of the total available market and how rapidly it's growing. The piece that we can access is probably on the order of about $200 billion. There's another large piece of it - $350+ billion - which is really infrastructure outsourcing, consulting, hosting, all of those types of activities, where we really don't participate. Where we do participate, though, are in hardware and software services, both of which CRM cuts across. That's about a $200-billion marketplace, of which CRM would be, say, a $40- to $45-billion piece. Other pieces that we would participate in would be hardware maintenance; logistics management; inventory and spare parts planning and management; and on-site services, which would include installation, moves, additions and changes. So we participate in a whole series of segments that make up a large and growing marketplace. We like it because it includes customers that we know from other parts of Solectron.

We think there's a real opportunity for a market leader to emerge in the after-market part of the business, as Solectron and a few others have emerged as leaders in the manufacturing and premanufacturing parts of the business.

MMI: Of that $200-billion TAM, how much of it has already been outsourced?

Bill Mitchell: That's a great question, and it's one for which we don't have a really good answer. As I said, that $200 billion out of $550 billion isn't as hard a number as you can get by adding up cost of goods sold, which is a pretty sold number. Our best guess is that it depends on the segment. Within that marketplace, CRM is probably 15% to 20% outsourced, and those are very rough numbers. Hardware services is probably that or maybe a little bit more, but the level of penetration is still low. Clearly, there's still a very substantial amount of outsourcing that is available, but it's a squishy number.

MMI: OEMs have outsourced repair and refurbishment for a long time because early on they saw that as not being a core competence perhaps even before they saw in many cases that manufacturing wouldn't be a core competence. So the outsourcing of the back end, if you will, has been going on for some time.

Bill Mitchell: That's true. But companies kept inside a lot of the spares planning, inventory planning, logistics management capabilities, some internal repair, a lot of engineering change capabilities, vendor management, CRM capabilities. A lot was still kept inside.

Here's what I think has changed. Five years ago, companies were asking for board repair. Now some people are saying, "I want you to be my after-market service chain. I want to have a single point of contact or a few points of contact that can manage all of the activities required to maintain my products in the field."

Typically, many of those activities were in different parts of the organization. Again, that's why the market number is a little bit squishy. So for example, call centers might be in a sales and marketing or customer service organization. The logistics part of the business might be in a logistics and warehousing organization, and sometimes repair sat in the manufacturing organization, and so on. So you'd find that there were different pockets and greater or lesser degrees of outsourcing.

One example absolutely struck me. Five years ago, I was dealing with a large OEM on a notebook outsourcing program. At one meeting, 18 different organizations from five separate business units were represented. All were involved in doing an advanced model for notebook repair.

For that notebook OEM, we cut their cycle time from about 14 days to a day-plus - 36 hours. So there was a huge benefit in terms of customer satisfaction. In doing that, we saved them well in excess of $50 million a year. Not because we had cheaper hands, but because we were able to optimize the system.

MMI: What other postmanufacturing capabilities will you be expanding further? Two possibilities from your capabilities grid, as shown on the Solectron web site, are logistics and field services.

Bill Mitchell: Let me take both of those - first of all, logistics. We have good working relationships with the major logistics carriers in the world. We have zero intention of getting into that business. It's an asset-intensive business. As I talk to my friends in those companies, I say, "We have no intention of having trucks and planes and things that you have." Do we need to ally with them and work with them? Absolutely. We do because the management of the whole logistics network and how products move is one of the important cost elements as well as an important service element.

If a product is in the box and being moved, they're far better at it. When the product comes out of the box and technical things start happening, then we're better off doing it.

Will we have capabilities in that area to optimize logistics networks? Absolutely. Will we be working with the major carriers, who will actually do the physical kinds of things, that's absolutely true too.

Field service is another area. It's one that we will certainly continue to evaluate. We have a modest field service capability now that we picked up from another acquisition.

MMI: Will acquisition be the primary means for further expanding your capabilities?

Bill Mitchell: That could be. Some of them we may want build internally, and there's always the make or buy decision. Clearly, we looked at CRM capability and said there's no way that we're going to be able to build the kinds of capabilities that we have with Stream in the time frame that's required. We might look at some other things and find we probably have some of the basic capabilities in house and can expand them and replicate them.

So we have built some capabilities. For example, we think we have the state of the art in terms of optical service capabilities. That's all stuff we've built internally.

MMI: What do you think about network installation services, which one of Solectron's competitors is pursuing, as a service offering?

Bill Mitchell: That one is very much also a make or buy decision as to whether you want to do it yourself or ally with somebody who does that as a business. It requires some very specific and very special capabilities. We have some of those in house. We have not made a big deal about it. But with some of the things we do in the telecommunications world, we actually have a fair amount of that capability.

It's a capability that we would look at to see whether we can leverage it in other places.

America II Electronics (St. Petersburg, FL), an independent distributor, is cautioning EMS providers not to try to take inventory off the books by using a buy-back scheme that violates accounting rules.

Under this scheme, a provider would sell excess parts to a distributor to get the inventory off the books. The provider would then buy back the parts when needed, with the distributor making a small profit for its trouble. Typically, extended terms are offered so that no cash changes hands. America II reports that some providers have discussed this scheme with the company.

According to America II, this scheme is an accounting no-no. Based on statement no. 49 of the Financial Accounting Standards Board, "the buy-back scenario should be viewed as a financial arrangement. This arrangement means no sale has transpired. If no sale has occurred, then the reporting of those assets cannot be taken," says J.P. Androff, worldwide director of Contract Manufacturing Services at America II.

"Even though this violates accounting practices, the bigger issue is the scrutiny that the SEC will give to creative write-offs of inventory," he added.

The company contrasts this scheme with the legitimate sale of excess inventory where America II will take the parts under consignment and resell them within the secondary market.

A new outsourcing survey from SG Cowen Securities (Boston, MA) shows the outsourcing trend is still intact. The firm's Fifth Annual Electronics Manufacturing Outsourcing Survey found that 71% of 84 respondents expect to increase outsourcing between now and 2003. But when results were weighted according to COGS (cost of goods sold), the vote for more outsourcing was 99%.

The poll also shows that the downturn has in some cases made OEMs more inclined to outsource. Some 43% of participants on a COGS-weighted basis indicated that during the downturn their mindset has been to outsource more. That compares to 28% who favored bringing manufacturing in-house during the slowdown.

The downturn is also causing a number of OEMs to speed up efforts to reduce the number of their EMS providers. SG Cowen found that a weighted 71% of respondents intend to shrink their EMS supply base by 2003. The survey asked those who are cutting out providers whether the downturn has accelerated this initiative. A weighted 42% of those OEMs answered in the affirmative. An average of 2.6 EMS suppliers was considered strategic by survey respondents.

Poll results show how popular it is to use EMS sites in low-cost geographies. A weighted 71% of respondents have moved a larger percentage of their outsourced production offshore to low-cost geographies over the past 12 to 18 months.

The survey also found that 49% of respondents utilize their EMS providers in the R&D phase, and that number is expected to rise to 64% in 2003.

ODMs were covered in the survey as well. A weighted 72% of respondents said they use ODMs, while 57% expect to increase their outsourcing to ODMs in the future.

The SG Cowen survey encompasses 84 representatives from OEMs with a total COGS of $340 billion. It is the second such poll done this year (May, p. 4).

Flextronics (Singapore) has acquired Instrumentation Engineering (IE), a systems test equipment developer and manufacturer. According to Flextronics, this deal significantly enhances its capacity and capabilities in the functional test market. IE has experience in designing and building custom test systems for optical and wireless network equipment.

The firm has locations in New Jersey, Pennsylvania and New Hampshire as well as Milan, Italy. Of IE's 200-plus employees, 125 are engineers. IE will become a wholly owned subsidiary of Flextronics Design and will keep its name.

A U.S. Bankruptcy Court in California has accepted Sanmina's offer for assets of E-M-Solutions (Fremont, CA), an enclosure manufacturer that filed for Chapter 11. Sanmina (San Jose, CA) bested Teradyne (Boston, MA), which had entered into an agreement earlier to acquire assets of the enclosure company (Aug., p. 7).

Sanmina will pay up to $110.65 million in cash, $20.0 million of which is subject to reduction based on a post-closing audit. The company intends to buy assets that include certain manufacturing operations in the U.S. as well as the stock of E-M-Solutions' subsidiaries incorporated in Mexico and Northern Ireland. Not part of this transaction are facilities in Gretna, VA; Longmont, CO, and Monterrey, Mexico. Separate negotiations are underway for the sale of these facilities.

For Sanmina's fiscal 2002, the deal is expected to generate sales between $200 and $300 million, and it is expected to be accretive before any infrequent charges. Among E-M-Solutions' customers are EMC, LTX and Sun.

More deals done...Celestica (Toronto, Canada) has completed its acquisition of Singapore-based Omni Industries Ltd. (June, p. 1-2). Celestica will issue to Omni shareholders about 9.2 million subordinate voting shares and will pay about $475 million in cash....Solectron (Milpitas, CA) has concluded its acquisition of Iphotonics (Glen Burnie, MD), a provider of core optical manufacturing services (Sept., p. 2)....PEMSTAR (Rochester, MN) has closed on its acquisition of Pacific Consultants LLC (Mountain View, CA), a contract product development firm (Sept., p. 3-4)....VisionTek (Gurnee, IL) has taken a majority interest in Wavedge Technologies (Dallas, TX), an engineering firm specializing in circuit design, PCB layout, CAD services, prototype analysis and production release support.

New alliance...Manufacturers' Services Ltd. (Concord, MA) has formed an alliance with Venture Technologies (North Billerica, MA), a product design company. Venture's engineering expertise will complement MSL's design and NPI capabilities in the Northeast U.S.

Some new programs...Solectron will manufacture certain key product lines for Sierra Wireless (Vancouver, Canada), a supplier of wireless data communications products. According to Reuters, Solectron will also assemble Handspring's Trio, a handheld computer with a built-in cell phone....Flextronics has landed a contract from Movaz Networks (Atlanta, GA) for the manufacture of its RAY optical product line....Under a new supply agreement, PEMSTAR will provide MTS Systems (Eden Prairie, MN) with manufacturing services for its electronic assemblies. In addition, PEMSTAR has signed an agreement to purchase MTS operations in Chaska, MN. The transaction is expected to close in November. The Chaska operations will continue to supply MTS and will serve key PEMSTAR customers in the Minneapolis-St. Paul area. MTS is a supplier of computer-based testing and simulation systems for mechanical behavior and instrumentation products for process automation. Also, PEMSTAR will furnish Given Imaging (Yoqneam, Israel) with production lines and related services for its M2A capsule, which when swallowed delivers color images of the gastrointestinal tract....Nortel has selected CirTran Corp., a contract manufacturer in Salt Lake City, UT, to provide EMS for Nortel's CallPilot, a unified messaging tool. In addition, CirTran has received two contracts from InterMotive Products, which designs fleet durability solutions for cars and trucks.