![]()

![]()

Cost reduction is at the heart of most outsourcing decisions. If it were not for the benefit of cost reduction, outsourcing would surely not be the trend it is today. After 25 years of outsourcing, one might think that product cost reduction has become a straightforward process for OEMs who put manufacturing in the hands of EMS providers. Far from it. In fact, cost reduction introduces some essential paradoxes:

• Product cost reduction is a given in outsourcing, but OEMs often do not take it for granted.

• In turnkey programs, it is not uncommon for the OEM, not the EMS provider, to control the majority of cost savings.

• OEMs and their EMS providers are encouraged to build trust in their relationships. Yet when it comes to cost reduction, skepticism can sometimes be a healthy attitude.

• OEMs have reasons not to demand guaranteed cost reductions.

• Despite years of experience in outsourcing, OEMs may differ in their approach to cost reduction.

• Cost reductions achieved in the past do not mean that these savings will necessarily continue.

Unraveling these seeming contradictions will shed light on the complex nature of cost reduction today for it is a topic that has largely remained in the shadows. EMS providers are leery of discussing it because to do so might reveal information sensitive to customers. Or give one customer the feeling that its cost savings don’t measure up to what some other clients are achieving. OEMs, for their part, generally avoid talking publicly about their outsourcing, much less the cost reduction aspects of it. Nevertheless, MMI was able to find three OEMs willing to go on the record about cost reduction. What they said should explain the paradoxes and give the EMS industry a good sample of the latest OEM thinking on cost reduction.

OEMs expect cost reductions as a natural result of outsourcing. But there are OEMs who are not content to sit idly by while their providers pass along cost savings. Take Teradyne. The maker of automatic test equipment needs its own process to manage cost reduction for two reasons. One is a product life cycle that can span seven years, with a seven-year after life. “We have a long product life so you must have mechanisms in place to control the cost over a longer period of time,” says Scott Cameron, who is responsible for outsourcing at Teradyne. The other reason is that Teradyne’s products follow Moore’s Law, which calls for continual increases in IC transistor density. That means Teradyne should pay less and less for the same semiconductor functions. “If we don’t have a process that ensures that stuff is happening, we’re going to lose,” says Cameron.

In Teradyne’s process for managing cost reduction, a team of commodity managers monitors the material costs that drive the company’s spend. They look at parts – both purchased internally by the company and externally by EMS providers – accounting for about 90% of Teradyne’s spend. Quarterly, this team does a rolling four-quarter forecast of costs at the part number level, which include cost-down rates and how those rates will be achieved. This data is then combined at the assembly level and further rolled up to the product. Teradyne applies the same sort of forecasting to labor and test, which are broken down into sub-elements. Each quarter, the company compares actual cost reductions at the part number, assembly and test levels to what was projected. That way, Teradyne can address any costs that are out of line.

Also, by utilizing actual costs, the company can re-price quarterly the assemblies or products sourced from its EMS providers. Teradyne won’t do business with providers unless they share actual costs with the company. With actual costs in hand, Teradyne can be sure that it is receiving the cost savings to which it is entitled. Teradyne’s cost reduction process was developed with this in mind.

“EMS providers in general will let you know when they’re paying too much and ask you to reimburse. And they’ll keep quiet when they’re paying too little and keep the profit. That’s one of the ways they make money,” says Cameron. He adds that if you don’t have the right processes in place, “you’re in jeopardy of only hearing about the bad news and not the good news.”

Although providers today may deny engaging in this practice, it is historically true that an unknown number of EMS providers were able to capture extra cost savings through a well-known device called purchase price variance, or PPV. MMI learned of this device over five years ago from a former quote manager at an EMS company. PPV occurs when a component price drops below the value quoted to the OEM customer. If the provider does not immediately transfer the new price to its customer, the provider enjoys some additional profit until prices are adjusted, say at the end of a quarter.

“I’ve always talked bluntly with all the contract manufacturers I work with, and all of them have refuted that,” says Matt Douglas, a VP in filter operations at Andrew Corporation, which sells communications equipment, services and systems. “They say, ‘Oh no, we don’t do that. We pass it straight through.’ Do I believe it 100 percent? No. I’ve always maintained a little bit of skepticism.”

Like Teradyne, Andrew also uses its own people to manage cost reduction on the materials side. “The best way in my view of assuring the product cost reductions that you’re expecting is to have your internal people at the OEM focus on the material, the BOM value. And we focus on making sure that we have the absolute lowest possible BOM value,” says Douglas.

Andrew retains responsibility for reducing the cost of high-dollar-value components, representing at least 80% of the dollar value of the material in an Andrew product. Starting with the highest cost parts, Andrew’s people examine their options. Can they second source a part to introduce competition that will lead to a lower cost? Or should they simply negotiate with the existing supplier to get the job done? They also look at the possibility of consolidating component volume with other programs in order to get better pricing based on a higher quantity.

“The dollar value of reduction from a contract manufacturer is generally less than what we go and get ourselves by negotiation with raw materials suppliers,” says Douglas. This statement makes sense since typically more than 80% of the cost of Andrew’s products lies in material, and Andrew is controlling the pricing of at least 80% of the material’s value.

Andrew still monitors prices of the remaining parts, for which contract manufactures handle supplier negotiations as well as procurement. These parts might represent 80% of the items on a BOM, but only 20% of its value. A software program used by Andrew compares prices of these parts quarter to quarter and flags any significant increases.

Andrew’s cost reduction process also accounts for PPV. If a provider finishes a quarter with material on hand that was bought for Andrew at a price above the next quarter’s rate, the company pays the provider what is called a buy down. On the other hand, any material that the provider purchased at a level below the quarter’s starting price will result in a credit against the buy down.

Based on five years of experience working with contract manufacturers, Douglas says, “I’ve never really put much stock in their ability to reduce our material cost.” Still, he points out, “They do a very good job of managing our manufacturing value add cost.”

Andrew checks on that aspect of cost reduction as well. The company looks at three factors in the manufacture of an outsourced product: manual assembly time, SMT assembly time and test time. Douglas says his company expects time reductions on a quarterly basis as providers come up the learning curve.

Although the EMS business is now largely turnkey, Andrew and Teradyne show that there are OEMs using internal staffs to manage cost reduction on the materials side by focusing on high-dollar-value parts.

Kodak is another OEM that has targeted component cost as an important source of cost reduction. The company recently outsourced digital camera manufacturing to Flextronics (Aug., p. 3). “One of the key things that I expect that we’re going to be doing over the coming weeks and months is work with in this case Flextronics specifically to identify opportunities to reduce component cost via either platforming or other mechanisms,” says Dennis Olbrich, worldwide operations director, Digital Capture and Devices at Kodak. By platforming, he means replacing a component with a more commonly used part that brings economies of scale and lower pricing. Olbrich expects that both Kodak and Flextronics will be involved in this effort.

“Obviously, since we’ve been manufacturing these products, we have a very strong knowledge of the component costs. And so we’re starting from a little different point than most companies would be in this relationship,” says Olbrich.

If EMS providers are to play a greater role on the materials side of cost reduction, some say they must be given more control over the AVL (approved vendor list). It is only then, the argument goes, that providers have the necessary leverage to negotiate with suppliers. “Most of the EMS providers do well where they can move the spend without customer approval,” says Teradyne’s Cameron. According to Cameron, suppliers are more likely to negotiate with providers that have the ability to move the business.

But giving AVL control to EMS providers is far from a slam dunk. “It’s probably the most hotly contested topic in the outsourcing industry,” says Andrew’s Douglas.

“We have contemplated doing that. We have not done that,” he adds. In Andrew’s view, the people who design the product have the best leverage with material suppliers. “So we have better leverage than the contract manufacturer, even though they’re a much larger company in some cases and they spend more money. We have better leverage because the point where you get the best material pricing is when the raw material supplier is being decided on whether they’re going to be designed into the product or not, qualified onto the product or not,” says Douglas. Still, Andrew is discussing the possibility of turning price negotiation over to an EMS provider once the design is complete and Andrew has specified the suppliers.

If EMS providers have a negotiating advantage over OEMs, it lies with a provider’s ability to aggregate component purchases over multiple programs. But not everyone is willing to give the EMS industry high marks for combining component buys. “I find that most EMS providers are still not good at aggregating and using their spend,” says Cameron. However, he does qualify this remark by adding that they do well with commodity items such as low-dollar passive components. Cameron questions how providers that run disparate ERP systems can know what they’re buying across the organization.

Cameron offers a prescription whereby EMS providers can improve cost reduction on the materials side. His prescription contains three elements. One, providers should know what they’re buying or about to buy enterprise wide. Two, they must be able to aggregate it and influence the terms of sale with that spend. Three, OEMs can help their providers in this regard by giving them more control over the AVL.

Still, Douglas is skeptical about an OEM turning over all control of material costs to an EMS provider. He does not see the motivations of the two sides aligned 100%. “The OEM wants lower material values, but for the contract manufacturer, quite honestly, it’s in their interests to have higher material values because most product pricing is based on a material markup of some sort. So if there’s a higher material [value], typically the manufacturing cost is higher.”

In order to give AVL control to an EMS provider, the OEM must be able to see what the provider is paying for the OEM’s parts. In other words, the OEM must have full visibility of the provider’s costs in what is called an open-book relationship. When the two sides elect not to share such financial information, their relationship becomes closed-book. These two types of relationships create another area of disagreement in the outsourcing community.

Teradyne is a solid backer of open-book pricing. For Teradyne, openness is a key to understanding its cost drivers. As mentioned earlier, a provider must openly share cost information with Teradyne as a condition of doing business. “The OEM will be much more successful in establishing this level of openness [with a provider] early in the engagement….Otherwise, they’re much less likely to do it,” says Cameron.

A key ingredient in an open relationship is establishing a high level of trust and respect between the two parties such as the relationship that Teradyne has with its EMS provider.

Open-book arrangements come with an obligation for OEMs. “If you have open book, you very much have to respect the confidentiality of that and not abuse the information in a way that puts the supplier in a position where it’s very hard for them to make money,” he says.

According to Cameron, an open-book approach can minimize the friction that occurs between OEMs and their providers during the cost reduction process. For example, an EMS provider that takes business with a low or negative margin will be hard pressed to deliver cost reductions in the future. But in the closed-book scenario, the customer will still expect reductions. That is a recipe for frustration. With open book, each side knows the other’s financial position going in.

In addition, Kodak supports more transparency with suppliers as a general principle. The company believes that the more visibility that it has working with a supplier, the more advantages that tend to result. “So more visibility both ways tends to be the philosophy that we try to achieve,” says Olbrich.

Andrew has engaged in both kinds of relationships, but prefers to agree on a pricing formula and then stick with it, regardless of volume, through a closed-book approach. The company believes in sharing the risk. “If volume is up, the contract manufacturer benefits from that. If volume is down, the contract manufacturer is disadvantaged and may lose money in a quarter,” says Douglas. Though the CM’s fixed costs would be underabsorbed in that case, the CM would be unable pass on additional charges that would otherwise be recognized under open-book pricing. “So I’d say generally our approach is not to dig into the contract manufacturer’s cost situation because at the end of the day that’s the whole reason for me wanting to use them – to make my job easier. I don’t want to go run the factory,” he says.

Perhaps the most direct approach to reducing the costs of outsourced products is to merely write cost reduction guarantees into a contract. Easier said than done, as the saying goes. “More often than not, that’s a very difficult thing to ask unless you have a program that is highly attractive to a contract manufacturer in terms of size or strategic importance,” says Robert Freid, president of Contract Manufacturing Consultants (Bellevue, WA). “I have seen it done, but it’s not something in common practice.”

“I suspect there are a lot more targets going into contracts in the last two or three years, as companies are striving to identify every possible advantage,” he adds.

Adopting targets “tends to be the more typical way that it works – absolutely” says Kodak’s Olbrich. “It has to be a fairly stable environment and predictable before people are willing to give guarantees.”

Cameron of Teradyne believes guarantees are problematic because if a provider cannot reach a guaranteed reduction of say 10% without losing money, they likely won’t live up to the guarantee. Yet if they do better than 10%, “they’re likely to deliver the 10% and keep the rest,” he says.

Relying on cost reduction targets, Teradyne fixes rates on such things as material markup and labor and then strives to lower the variable component of each cost. “So we might hold the labor rates firm, and we’ll ask the EMS provider to drive efficiencies in labor, take fewer hours as well as increase yields,” says Cameron.

Andrew uses a mixed approach for cost reduction. The company specifies guaranteed reductions for a portion of product cost and target reductions for another portion.

It is standard practice in OEM outsourcing to offer EMS providers incentives for reducing product cost. Mark Zetter, president of consulting firm Venture Outsource (San Jose, CA), offers a general guideline for an incentive program. In the first three to six months – this period can vary – the EMS provider keeps all of the cost reduction, according to his guideline. During the subsequent six months, the OEM and its provider share product cost savings 50-50. Then after nine or 12 months, the OEM receives 100% of the cost reduction.

How are the savings achieved? According to Cameron, there are four basic categories of cost reduction:

• Take cost out by negotiating with component suppliers.

• Look for alternative processes and materials and better ways to accomplish the same thing.

• Move manufacturing nodes to a low-cost region.

• Source materials in a low-cost region.

Kodak has identified three primary sources of cost reduction for its digital camera outsourcing program with Flextronics. First is the additional scale that Flextronics brings in electronic components. “We believe that there is some opportunity to leverage Flextronics’ strength in that field,” says Olbrich. Second, Kodak is hoping to reduce costs further in the electrical and mechanical designs for cameras by taking advantage of Flextronics’ strong design capabilities in fields adjacent to digital cameras. Third, Kodak will get some cost advantages by utilizing the provider’s logistics systems, which are tailored for consumer digital products. The company looks for reduction in total delivered cost.

While cost reduction rates, of course, can vary, a rule of thumb is to expect a reduction of 3 to 5% on an annual basis, according to Zetter. “I’m talking about your average contract manufacturing company, your average OEM that is sourcing the contract manufacturer,” he explains.

But it might not have been wise to expect that 3 to 5% take-down rates would be easy to come by in 2006. Teradyne’s Cameron says this year has been a tough one for cost reduction.

Likewise, Andrew’s Douglas sees 2006 as challenging for his industry, which expects to reduce product cost every year by somewhere between 10 and 20%. Expectations “generally iron out around 15%,” says Douglas. “It’s a very challenging thing to reduce your product cost by 15% annually when the raw materials that go into your product are increasing in some cases 60%.” Copper prices increased that much through September, according to Douglas. Aluminum and silver went up by more than 20% in that year-to-date period, he reports.

Does price inflation of these raw materials prices put component suppliers in a big squeeze? “Absolutely,” Douglas responds.

In Cameron’s view, inflationary pressure will mostly affect non-electronic commodities such as metal and cabling.

If one can’t reduce material pricing sufficiently, one can reduce material content, i.e., the number of components, through redesign. Product redesign can provide a means to outflank the current challenges of cost reduction. But there’s a catch. “Design resources are expensive, and it takes a lot of time to qualify those types of design changes,” says Douglas. Moreover, design engineers at OEMs such as Andrew are always working on the next generation of products.

With OEM design resources at a premium, perhaps there is a greater role here for the EMS industry. More and more EMS providers have the ability to redesign products for cost reduction. If product costs prove to be resistant to reduction, OEMs can utilize an EMS provider to reduce material content through redesign where product life permits. This OEM approach would seem preferable to squeezing EMS providers and component suppliers for reductions that they might not be in a position to give.

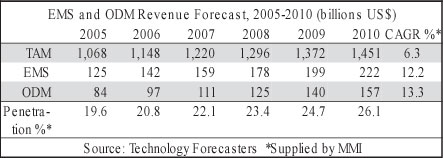

A new five-year forecast for the EMS and ODM industries calls for the two sectors to grow at close to the same compound annual growth rate (CAGR). This forecast implies that the ODM industry will no longer enjoy growth rates significantly above those of the EMS industry.

According to the latest projections from Technology Forecasters Inc., or TFI (Alameda, CA), the EMS industry’s revenue will increase from $125 billion in 2005 to $222 billion in 2010, corresponding to a CAGR of 12.2%. The five-year growth rate for the ODM side is just over one percentage point higher in the TFI forecast. ODM revenue will grow at a CAGR of 13.3%, starting at $84 billion in 2005 and ending at $157 billion in 2010 (see table).

TFI expects EMS sales to reach $142 billion this year, an increase of 13.6% over 2005, while ODM revenue should grow by 15.5% to $97 billion in 2006. In this latest forecast, the firm raised its expectations for 2006 from its forecast of a year ago, which projected EMS and ODM sales of $132 billion and $95 billion respectively for the current year (Oct. 2005, p. 3).

For 2007, TFI foresees a slightly lower growth rate of 12.0% for the EMS industry, which will generate $159 billion in sales. ODM growth will also dip a little bit to 14.4%, as ODM revenue will rise to an estimated $111 billion next year.

Combined revenue for outsourcing providers (EMS + ODM) should hit $239 billion this year, predicts TFI, and the outsourcing total represents an increase of 14.4% from 2005. MMI’s roll-up of first-half 2006 sales from 31 large providers yielded a somewhat higher growth rate of 17.8% (Sept. p. 1). For the period 2005 to 2010, TFI projects that the outsourcing business will grow at a compound rate of 12.6%, reaching $379 billion by the end of the period.

In the new five-year forecast, outsourced business will not come anywhere close to capturing a majority share of the total available market of electronics production. Though the penetration rate of outsourcing will increase over the forecast period, by 2010 outsourcing will only account for just over a quarter of the TAM (table). If accurate, this 2010 projection is a long way from full penetration of the TAM.

TFI pegs the 2005 TAM at $1.07 trillion, rising to $1.45 trillion in 2010. These start and end points correspond to a five-year CAGR of 6.3% for the TAM. This rate is half the aforementioned outsourcing CAGR of 12.6%.

The new forecast appears in “Electronics Manufacturing Outsourcing Report: Five Year Forecast of EMS and ODM Industries by Market Sector and Geography,” which is available to members of TFI’s Quarterly Forum. For more information, email jread@techforecasters.com.

With labor rates about one third of those in Hungary and Poland, Ukraine in recent years has been considered a potential source of low cost assembly for OEMs in Europe. This year, Ukraine is starting to realize its potential as two major EMS providers are building manufacturing facilities there.

Earlier this year, Flextronics announced that it was erecting an industrial park in Ukraine (Feb., p. 7). Now Jabil Circuit has begun construction of a greenfield facility in the country. Ukraine’s standing in the EMS industry has risen since both Flextronics and Jabil have voted for it with their investment capital.

Flextronics has not released any details about its new park, but Jabil has been more forthcoming. Jabil is building a 26,000 m2 facility in Uzhgorod, Ukraine, within the Special Economic Zone Zarkappatya. The facility will be operational by spring 2007, and current operations at a smaller, leased facility in Uzhgorod will be relocated to the new plant. Jabil, which employs about 900 people in Uzhgorod, expects to add 1,500 employees over the next 12 to 18 months.

“We’re excited about the area. We think it’s really going to bring a level of competitiveness that will be comparable to landing products from China into the European marketplace,” said John Lovato, Jabil’s president for Europe, in an interview with MMI. According to Jabil, Ukraine can compete given its educated and available labor force, competitive labor costs, proximity to the European market, natural resources for developing a strong supplier base, and government support.

But the Ukrainian government hasn’t always cooperated. In April of 2005, the government revoked special economic zone privileges in an effort to stop illicit use of SEZs (June ’05, p. 2). Authorities reaudited legitimate businesses, and Jabil was granted SEZ status in July of this year, pending approval through a new budget law. Lovato said Jabil is confident that its SEZ status will be ratified in the government’s new budget by the end of the year.

Jabil plans to develop in the SEZ Zarkappatya an industrial park integrating suppliers and partners. The industrial park approach, a strategy pioneered by Flextronics, can be applied in underdeveloped areas to build up a local supply base.

According to Lovato, Jabil will be using Ukraine for “cost- and margin-sensitive products with very high volume.”

The company has been manufacturing in Ukraine since 2004, and start-up volumes over the last two years have come from Jabil operations in Western and lately Eastern Europe. “We expect that to be complemented with new products as we have projected new market share growth there,” said Lovato. The Ukraine operation currently serves two customers.

In a classic example of EMS industry consolidation, publicly held Benchmark Electronics (Angleton, TX) has signed a definitive agreement to acquire Pemstar (Rochester, MN), another US-traded EMS provider, through a stock-for-stock transaction.

Under the agreement, Benchmark will exchange 0.16 share of its common stock for each outstanding share of Pemstar. Based on Benchmark’s closing price on Oct. 16, the transaction values Pemstar at $4.63 per common share, which is a 27% premium over the stock’s closing price on that day. As a result, the deal is worth about $300 million including the assumption of Pemstar debt.

According to Benchmark, the acquisition brings it a combination of skill and scale. Pemstar’s engineering capability adds depth and breadth as well as geographic presence to Benchmark’s engineering team, said Cary Fu, Benchmark’s president and CEO, during a conference call with analysts. He also pointed to the complementary nature of Pemstar’s customer base and the opportunities to expand those customer relationships. In addition, the deal will expand Benchmark’s presence in end markets it has not served traditionally, including those that are in the early stage of outsourcing. Fu gave two examples of these markets: semiconductor equipment and military and aerospace.

Pemstar’s footprint offers Benchmark yet another benefit. Benchmark plans to utilize Pemstar facilities, particularly in areas of the world where capacity is constrained. With 11 manufacturing locations worldwide, Pemstar operates in three low-cost countries: China, Thailand and Romania. “We are in the position to increase the Pemstar facility utilization level at the same time to avoid cost expansion, which we had to otherwise undertake to meet strong demand from our customer base,” said Fu.

“Benchmark’s proven track record, strong balance sheet, and reputation as a global leader in electronics manufacturing services make the deal an attractive one for Pemstar’s customers, shareholders and employees,” stated Al Berning, Pemstar’s chairman and CEO, in a press release.

During the conference call he said, “While we believe in our ability to be successful as a stand-alone entity, there is no denying the benefits that come with scale and scope in an industry such as EMS.”

The transaction, which is subject to approval of Pemstar’s shareholders, antitrust approvals and other closing conditions, is expected to close in Q1 2007, subject to the timing of regulatory reviews.

Benchmark anticipates that the acquisition will be accretive in calendar year 2007, excluding any integration, restructuring and amortization costs related to the acquisition. The company believes that the deal will result in cost synergies of about $20 million a year over the longer term.

In explaining why Benchmark decided to make the deal now, Gayla Delly, Benchmark’s CFO, said that in recent periods Pemstar “has successfully addressed many of the issues that had weighed on its performance.” The company has restructured its footprint and rationalized its customer base. “The result has been improved margins and a resumption of revenue growth, both [of] which we are confident are sustainable,” she said.

Founded in 1994 by a group of eight IBM managers, Pemstar employs about 3,500 people. Fiscal 2006 revenue totaled $871 million, and sales from Motorola and IBM represented over 10% of the total. Other large customers listed in Pemstar’s Form 10K for fiscal 2006 (ended March) are Applied Materials, Fluke, Hitachi Global Storage and Honeywell. Some $250 to $300 million of revenue on an annual basis is generated by Pemstar’s Tianjin, China, operation, for which Pemstar is seeking strategic alternatives. This site, one of Pemstar’s two locations in China, is associated with a turnkey cell phone customer, believed to be Motorola.

Besides offering a range of EMS capabilities typical of a large provider, Pemstar can design and build custom test and automation equipment. This is a capability that Benchmark does not have but views as significant.

More acquisitions…Veritek Manufacturing Services (Escondido, CA), a privately held EMS provider, has completed the purchase of DDi’s assembly business for about $12 million in cash. The assembly business brought in sales of $15.6 million for the first six months of 2006. DDi (Anaheim, CA) divested this business to focus on its core PCB business. …TES (Langon-sur-Vilaine, France), a provider of design and manufacturing services, has acquired a plant in Penang, Malaysia, from AV Industries. A year ago, TES partnered with AVI in order to begin Penang operations within the AVI facility. The acquisition gives TES its first factory in Asia….Publicly held TXP Corporation (Richardson, TX), a provider of pre-manufacturing services, has signed a letter of intent to acquire the assets and intellectual property for Siemens’ Optical Network Terminal technology.

New business…Enablence Technologies (Ottawa, Canada), a developer of fiber-to-the-home modems, has entered into an agreement by which Sanmina-SCI (San Jose, CA) will manufacture Enablence’s triplexer and diplexer product lines….Under a memorandum of understanding, CTS Corporation through its Electronics Manufacturing Solutions unit (Moorpark, CA) will provide full turnkey EMS for a broadband-over-power-line access node developed by Ambient Corporation (Newton, MA). CTS will supply the services, including PCB assembly, box build integration and direct-ship logistics, from its New Hampshire facility....LaBarge (St. Louis, MO) has received $15 million in follow-on orders to continue providing wiring harnesses for a very light jet made by Eclipse Aviation, based in Albuquerque, NM (April, p. 5). Also, LaBarge has secured new orders totaling $4.3 million from Modular Mining Systems (Tucson, AZ) for electronic assemblies used in mine information management systems. LaBarge’s Pittsburgh, PA, facility will manufacture an integrated solution of PCBs and box-level assemblies.

Celestica (Toronto, Canada) has sold its Vimercate, Italy, operations to Bartolini Progetti and entered into alliance with the firm to provide certain EMS, after-market, NPI and support services on a subcontract basis. Bartolini Progetti is an Italy-based logistics and after-market services provider. The agreement is in line with Celestica’s strategy to shift the majority of its production to lower-cost regions.

This arrangement will provide Celestica with continuing capacity and service capability in Italy for ongoing customer support.

About 850 people employed by Celestica in Vimercate will continue their employment under the Italian company.

Also in Europe, Celestica is closing its facility in Telford, UK, reports the Shropshire Star, a British newspaper.

More restructuring…Under the first phase of a new restructuring plan, Solectron (Milpitas, CA) will reduce its work force by about 1,400 employees in high-cost geographies and will close or consolidate about 700,000 ft2 of facilities in Western Europe and North America. The company expects this restructuring will be completed within the next 12 months. Estimated charges for this phase will total about $50 to $60 million. Regarding a second phase of this restructuring plan, Solectron will continue to assess the profitability objectives and customer requirements for certain sites. The company will announce a second phase of restructuring only after the complete plan has been vetted internally and with customers. Solectron expects that a second phase should be completed within 24 months.

A special committee of Sanmina-SCI’s board has reported the findings of the committee’s investigation into the company’s stock option practices dating back to Jan. 1, 1997 (Sept., p. 7-8). The committee found that most stock option grants between 1997 and 2006 were not correctly dated or accounted for. This investigation singled out the actions of a former and current member of management involved in the authorization, recording and reporting of stock option grants. The unidentified current management employee has resigned.

Sanmina-SCI also disclosed that it has received a federal grand jury subpoena for documents relating to the company’s past practices for granting stock options.

It would be nice to ignore Hon Hai Precision Industry. Then one wouldn’t have to worry about its dominant size or market share gains.

Certainly, it’s tempting to classify Hon Hai as something other than an EMS provider. After all, Hon Hai didn’t evolve like other EMS providers. It started out as a component company. Hon Hai doesn’t look like other providers. Among its operations is a substantial motherboard business, something that the EMS industry in general has avoided. Hon Hai sells branded products on the board and components level; branded products are an anathema to most other EMS companies. Also, Hon Hai operates as a group of affiliated companies. Again, this is not a model typically espoused by the rest of the industry.

What’s more, Hon Hai almost invites one to ignore it. The company is not as easy to track as public companies are in other parts of the world. Hon Hai almost never announces program wins and says little about its operations and performance. Hon Hai’s elusive behavior could almost fool one into thinking it’s not there or placing it in the ODM category where it doesn’t belong, as some have done.

But Hon Hai is now the EMS industry’s 900-lb gorilla, albeit a somewhat stealthy one. Measured by first-half 2006 sales, Hon Hai is more than twice the size of its nearest competitor. Industry players ignore Hon Hai at their peril.

If Hon Hai continues to grow at 30% or better, it will be likely be atop the industry in a dominant position for years to come. That could be bad news for the rest of the industry.

Throughout Hon Hai’s history as it moved up from component to systems supplier, the company strived to be the low-cost producer. This approach won the company customers and market share. MMI doesn’t see Hon Hai departing from this basic philosophy for two reasons. First, the company is still run by its founder, Terry Guo. Second, Hon Hai is in a position to use its size and buying power to negotiate lower prices from its suppliers.

If Hon Hai continues to keep its quoted prices down, as MMI believes it will, Hon Hai will restrict margins for everyone else it competes with. In the past, this pricing effect was limited primarily to the PC industry, in which the EMS industry did not have a large presence. But Hon Hai has branched out into consumer products such as cell phones, game consoles and iPods and into other segments including communications and automotive. As Hon Hai expands into other areas, it competes with more and more companies. And those companies begin to feel the pricing pressure created by Hon Hai. This is not a recipe for expanding margins, which is a goal for a number of EMS companies.

The Hon Hai effect won’t go away. But if a company runs up against Hon Hai, better to do so with eyes wide open.