![]()

Cover story

Optical Business Puts CMs in a Different World

Market Makers

Q&A with Benchmark's Don Nigbor

Market Data

News

Sanmina and Viasystems To Acquire Lucent Facilities

Flextronics Hatches More Deals

Last Word

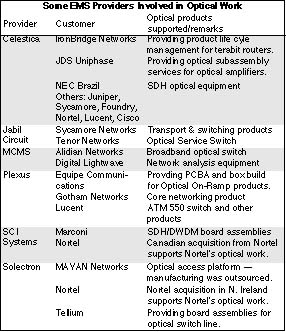

Stoked by the need for more Internet bandwidth, optical networking hardware has been a red-hot market this year. And it's showing no signs of cooling off. Sycamore Networks (Chelmsford, MA), a well-known developer of optical networking gear, expects this hardware market to reach $40 billion by 2004, based on data from RHK, a California research firm. A key driver of this high-growth market is dense wave division multiplexing (DWDM), which increases the capacity of a fiber optic network by putting information on different wavelengths within a single fiber. As the demand for optical networking hardware has surged, so too has outsourcing in that space.

Take Celestica. "Celestica's optical networking business is growing very fast off a small base just 18 months ago," says Dan Shea, senior VP and chief technology officer at Celestica. "Now, with 14 customers, we expect revenues generated from the optical networking side of the business to reach more than US$1.5 billion for fiscal 2001." He reports Celestica is doing optical work in North America, Europe and Asia, with at least nine sites involved in optical assembly and test. The company's new site in Portsmouth, NH, serves as its center of competence for optical networking technologies.

But Celestica is not the only EMS provider to announce new customers in optical networking (see table). Nor is Celestica the only one with a double-digit customer base on the optical side. "There are probably a dozen of our customers that are either on the [long-distance] core or on the edge of the core," says Bob Kronser, VP of sales and marketing at Plexus. He points out, "Anyone who puts something on the core, takes something off the core, or is involved strictly with the core...is utilizing optical technology."

Outsourcing is coming both from new optical networking players, which have multiplied in the last two years, and from established companies. New players such as Sycamore want to outsource from day one. Established firms like JDS Uniphase, a supplier of optical components and modules, and Nortel are increasing their use of outsourcing.

But to enter the world of optical product outsourcing, one finds that the rules of EMS don't always apply. For one thing, outsourcing can occur at three or four levels of integration. Optical components, board assemblies and the system form three basic levels. Then one can subdivide board assemblies as to whether or not they are being supplied to the OEM with optical components.

Tellium (Oceanport, NJ), an optical switch company, provides a recent example at the board level. The company will use Solectron to provide NPI and manufacturing services for Tellium boards. Under the contract, Tellium has the option to move final product assembly and testing to Solectron. On the other hand, IronBridge Networks (Lexington, MA), a developer of a terabit router, has contracted Celestica to provide product life cycle management through the system level and extending into logistics and after-sales services. Celestica will manage the supply chain, manufacture and assemble compo-nents and test integrated systems. In optical net-working, system-level outsourcing may not be as commonplace as contract manufacturing on the board level, but the Iron-Bridge example shows that it is possible to out-source an entire optical system today.

Outsourcing is also taking place at the optical component level. MCMS is building optical trans-ceivers for operation at 2.5-10 gigabits per second. Although this work occurs at the lowest level of integration, it is far from easy. "At the component level in terms of the assembly of trans-ceiver products, the difficulty associated with some of the tasks in that is greater than when you're at the next higher level of integration," says Rich Latta, MCMS' director of engineering. Besides SMT assembly, this work involves mounting and calibration of a laser source and final packaging.

To vie for optical business, a contract manufacturer must have the requisite capabilities. Trouble is, not everyone in the OEM community is willing to discuss them. Nevertheless, based on information provided mostly by MCMS and Plexus, some basic requirements can be listed. They are board assembly of optical components, fiber handling, fiber alignment and termination at a source or detector, fiber termination at a connector, fiber splicing, increased cleanliness and optical signal testing and analysis.

Putting optical components on a board may not require any special processes, yet meeting this requirement is not necessarily straightforward. From a board assembly view, optical components with fiber pigtails are not equivalent to SMT or through-hole components. "Pigtailed components do not fit in well with the standard SMT-oriented factory. They are typically incompatible with SMT or insertion equipment and are heat sensitive, making wave soldering difficult and mass reflow impossible," says Bill Barthel, Plexus' manager of manufacturing technology development.

Moreover, working with fiber demands that a provider add capabilities. For example, a minimum bend radius must be observed when handling the fiber. It must be polished for terminations. What's more, a single-mode fiber 8 microns in diameter typically requires a 0.5-micron tolerance for alignment to a source. According to Plexus' Barthel, automated solutions for this precision alignment are not readily available. For splicing, there is equipment to be evaluated and purchased, but an operator is still involved.

So manufacturing for a program including optics requires people trained in fiber optics work. They don't exist in a typical EMS facility. One way to obtain them is by acquisition. Solec-tron, for instance, has offered jobs to about 220 people that came from Nortel's optical manufacturing group in Northern Ireland. The company intends to leverage the product knowledge it acquired from Nortel for an optical space that Solectron describes as exploding. Or take SCI. The company's recent acquisition of EOG, a Mid-Atlantic CM, added a work force versed in optical networking activities. But if people with optical skills cannot be acquired, they must be trained. According to Latta of MCMS, there are companies that provide training.

Cleanliness is another requirement, but one that doesn't always come to light. "If you're mounting optical modules onto printed circuit card assemblies, then the SMT environment is fine," says Latta. "If you're terminating cables, then a cleaner environment may be required."

For the initiated, optical cable processes may be rather ho-hum. But optical signal testing is another matter. Requirements "are changing very rapidly right now," says Kronser of Plexus. And there is a good deal of secrecy surrounding optical testing because it ties into product design.

"Today, we're looking at the optical signal and evaluating the quality of the optical signal - not just whether it's there or not, but more of a parametric measurement of the optical signal," observes Kronser.

"It's very different from the electrical verification we've done," notes Jay Vilhauer, a manager in the Test DesignCenter of Plexus. "We're literally using laser sources, optical power meters and spectrum analyzers to really look at the waveforms coming off these products before they go into further higher level assembly."

"Many of these types of test have only been done during design verification. Now there's an element of necessity that forces some of these tests to be implemented in production," says Vilhauer. He adds, "There's really an explosion of test requirements at the production level for fiber optics."

In partnership with an EMS provider, one OEM has developed automatic test stations for its optical products. These stations are used after boards have been electrically tested and optical components have been added.

Materials management for optical devices is another capability that an EMS provider cannot take for granted. Indeed, the OEM customer may have the supplier relationships and the purchasing power on the optical side.

As attractive as the optical business is, it's a new world with its own rules. A number of providers, including both tier-one and tier-two companies, have learned those rules. Other CMs are likely to follow.

The watchword at Benchmark Electronics has been and continues to be technology. Benchmark has been known for its ability to build large, complex products both at the board and system level. But last year the company underwent a major change. It acquired global capabilities and expanded into the high-volume world through its acquisition of Avex Electronics, which had done server- and PC-level work. The move added lower-complexity products to Benchmark's portfolio. But the company believes it gains an advantage from applying its technical expertise across a broader product mix.

Any time a business changes strategy there is risk. Nevertheless, this new strategy is winning business. For example, ViaSat has selected Benchmark's Huntsville, AL operation, acquired in the Avex deal, as the contract manufacturer for ViaSat's Satellite Networks division. Benchmark will build board assemblies for ViaSat satellite communications products being made at ViaSat's new facility near Atlanta, GA. The scope of work will also include box build and order fulfillment for selected products. Another program win involves assembly services for a clinic system from Medtronic.

Revenue is going up as well. For the first six months of the year, sales climbed 144% year over year to $755.7 million. Analysts are projecting revenues over $2 billion next year.

Is Benchmark now large enough and global enough to be considered a tier-one player? That is one of the questions MMI put to Benchmark's president and CEO, Don Nigbor, in a recent interview. The interview sought a better understanding of where Benchmark is today and where it is heading. Questions covered a range of topics such as ranking, program size, system integration, Avex, geographic expansion, markets, customers, margins, personnel, divestitures, front-end services and shortages. Here is what Don Nigbor had to say.

MMI: Some would say that one to two billion dollars in annual sales is no longer enough to put a company in the top tier. Where does Benchmark stand with respect to the top tier?

Don Nigbor: We feel that we already have top-tier capability in the sense that we can do multicontinent launches for customers. We're doing that today. Being able to do multicontinent launches is characteristic of a top-tier firm. We also have the size to respond to our customers. So we still maintain our flexibility while offering a complete range of services.

MMI: At Benchmark's size, how large are your programs?

Don Nigbor: We're typically seeing two to three hundred-million-dollar programs. Benchmark is probably one of the best players in that market. Although we are going to do programs larger than that, we're probably not going to be the largest company in the industry. That's because we're not doing extremely high volume.

We do have programs where we build three to four million units. So we have high-volume capability. But given our strength in high tech, high mix, we want to go to some of the customers that need both services. It's the philosophy of the one-stop shop.

MMI: For the first six months of 2000, Benchmark's business in system integration and box build was flat compared to a year earlier. Yet Benchmark is adding space in Ireland and Huntsville due to system integration requirements. What is happening with the system integration business?

Don Nigbor: We have really strong capabilities in system integration. That's being widely accepted by our customers. We're receiving a lot of interest in our large-system integration capability, also in our server-level capability and our desktop capability. So we're seeing that the percent of business at the system level is going to accelerate rapidly next year, and we're preparing for it. That's why we're doing expansions in several locations in Europe and the U.S. - Ireland and Huntsville particularly. We will see the percent of system revenue go from the 10 to 15 percent range to greater than 25 percent.

MMI: When Benchmark acquired Avex, Benchmark took over an EMS company with underutilized capacity and operating losses. How is the Avex business performing these days?

Don Nigbor: With Avex, what we wanted to do was increase global and geographic presence. It really was a perfect match between Benchmark and Avex. From a geographic standpoint, there was no overlap.

There was underutilized capacity at Avex, and the challenge going in was to fill in capacity. We're now seeing a lot of new opportunities to bring business in. The electronics market is as strong as I've seen it in my 30 years in the industry.

We're expanding a number of our sites. That includes taking about 140,000 additional square feet in Huntsville, primarily for system integration capability to complement the capacity of the board lines there. We've seen a really strong reception by our customers in Huntsville for system integration.

It's really the same story of filling capacity. On the sales side of the business, the challenge is to bring in new programs. That activity slows down during a transition. Our sales force across the company has really pitched in to fill the available capacity with new customers.

MMI: Wasn't the Lockheed operation in Hudson, NH, something of a turnaround situation as well?

Don Nigbor: There were some similarities. The operation when we acquired it was a little bit underutilized. The company was in transition. They weren't booking new business.

We have been growing in New England. The facility has expanded by 25%. We took over the entire building there, and we're looking at another site.

The acquisition provided us with great people and great technology. We're seeing the same thing in Avex.

MMI: Although Avex gave Benchmark global capabilities, in Asia Benchmark only operates in Singapore, not considered a low-cost location. What can you say about expanding in Asia?

Don Nigbor: We're seeing a strong reception for our capabilities in Singapore. It's attractive for high tech and large systems.

We're looking at expanding into low-cost, high-volume areas - China and Malaysia. We are working on it. We have been telling the analysts for six to nine months that we're projecting early '01.

MMI: Benchmark's two main segments might be described as enterprise computer and peripherals and telecom. Do you agree?

Don Nigbor: We use the term high end or enterprise, and that includes storage as well as peripherals. We define high end to be server and above.

MMI: That high end segment plus telecom accounted for 69% of sales last year based on your filing.

Don Nigbor: Yes, they're very strong. Telecom is almost 40%, and enterprise applications is around 30%.

MMI: Are those today's numbers?

Don Nigbor: The numbers are historically correct, and they've remained the same this year. Throughout our history, those have been our two largest markets.

MMI: Again in the filings, Lucent and EMC were listed as your largest customers, together representing 34 percent of sales last year. Are they still your largest customers?

Don Nigbor: Yes. Right now, our three largest customers would be Lucent, EMC and Sun.

MMI: All three of them would be ten percent or more of your sales for the current fiscal year?

Don Nigbor: Currently, they all would be greater than ten percent.

MMI: Do you expect any more customers to break that ten percent threshold in the near future?

Don Nigbor: We have customers that potentially could be larger than ten percent. Since Benchmark is experiencing strong internal growth, our customers would have to grow faster in order to become a larger percent of our business.

MMI: Your one-stop solution of offering high-complexity services along with high-volume services brings up a question. A financial analyst might say that adding this higher volume, lower margin business from Avex will grow your revenue, but it will also drop your gross margins. How do you respond?

Don Nigbor: Typically, our gross margin had been one of the highest in the industry. With the mix of the higher volume, we're probably running at about the norm for the industry. As we get larger, I think that the analysts could expect that we would be approaching the norm. As we get a balance of revenue that is more representative of the industry, naturally our results will probably represent that norm too.

We think that we can improve profitability from where we are today, and we have been improving the profitability by getting better utilization of the facilities we've acquired. But we probably won't be quite as profitable as we've been in the past. At one point, we were over ten percent gross margin. We don't think we'll be back in that space. On the other hand, we'll still be one of the strongest companies in the industry - still very solid and a very strong performer. But we'll be closer to the norm for the industry.

MMI: Benchmark, like some other contract manufacturers, has operated with a lean management structure. At least, that's our perception. Is management bandwidth an issue now with the growth that you're seeing?

Don Nigbor: One of the things we did was to put an acquisition strategy together in 1993-1994. As part of that strategy, we wanted to add technology, geographic presence and management talent. We were very fortunate in our acquisitions to bring in some very strong people who have many years in either the OEM space or the EMS space. Over the last number of years, we've been able to take those people and expand their scope. We've tried to make them feel part of Benchmark. We've given them more responsibility, and we've been able to grow these people. So a very substantial part of the senior management team of Benchmark today has come through the acquisition route. We really used it as a recruiting tool as much as a revenue and technology building tool.

We also recruit on the outside, and we've been successful there building, for example, our corporate organization and staffing that with very senior people. But a lot of the real strength of Benchmark comes from the fact that we did acquire what I would call mature manufacturing operations with good people. And we've been able to not only grow those operations, but grow the people too.

MMI: Outside of Avex, Benchmark has not participated in any of the large divestitures or megacontracts recently. Can you comment?

Don Nigbor: We have a full-time staff of people who are looking at divestitures and how they would fit into the future of Benchmark. We see that as one of the growth opportunities for the company. There are a lot of these situations coming up today where companies are divesting of their complete manufacturing assets. We're evaluating those and seeing what the opportunities are.

At the same time, we would want to do an acquisition that was synergistic with our goals to be a very flexible company, a very high-technology company and a very responsive company. So we would not want to lose our mission. At the end of the day, to be successful in the EMS business you must realize that the customer really cares about the kind of service they're getting. They're not necessarily concerned about some of the other factors that many people in the industry are focused on. The customer at the end of the day wants good service. They want good delivery. And they want good quality. Those are the things that are most important to them.

I think as an EMS company, you can't become too focused on acquisitions and drop the ball on service.

We've been very successful in winning what we consider very significant programs for a company of our size. We're seeing the company grow very nicely going forward. So we're very happy with the kind of programs we're winning today. Most of them are with strong companies that are leaders in their industry.

MMI: Does Benchmark plan to expand its service offerings either on the front end or in back-end services such as repair and warranty support?

Don Nigbor: On the back-end side, we are doing, for example, warranty and field support for a number of customers today. We're seeing the back end grow where customers want us to do more system integration and logistics. We offer complete back-end support.

We're also seeing interest in the front end. That side has been growing with the demand for engineering services. We plan on having more locations to offer these services even though we have a number of those locations today. Some are separate from our manufacturing sites. But all of our manufacturing sites do offer front-end support including prototyping.

We're talking about having more new-product-introduction capability remote from the plants. We already have remote sites in Minneapolis and Dallas. We have engineers remotely deployed in the Boston area and in California. And we're looking to grow our front-end capabilities in those areas.

MMI: Where are those engineers stationed?

Don Nigbor: Within a customer site.

MMI: What is Benchmark's position on vertical integration?

Don Nigbor: We are looking at ways that we should be vertically integrated. It's something that the acquisition team is evaluating.

But at the end of the day, you could end up with more of an association of companies. We wouldn't want to vertically integrate and lose flexibility. Just adding revenue to the top line is not a good justification for vertical integration.

MMI: Not only is the EMS industry facing component shortages, labor is tight as well. Will these resource constraints begin to take their toll?

Don Nigbor: There are component shortages today, and this has happened numerous times in the history of the industry. Benchmark has always had a very strong materials management philosophy, and we're managing our way through the shortages, we think, very well given the market conditions.

Materials shortages do make life more difficult because they keep you from running your company as efficiently as you'd like to run it. You may be getting the components, for example, but you're not getting them exactly on the day you want to receive them.

Labor is also tight. But we've been able to grow our sites. We're adding space. We're also going to look at ways to maybe expand regionally around some of our existing major facilities. We may put in some satellite facilities to expand our labor pool. And so we think we can manage the labor problem as well. We're projecting to do an acquisition in the Far East, which will help us add more capacity to the company. I think we have a multipronged strategy to address the conditions in the market.

MMI: Will tight labor affect the industry as a whole?

Don Nigbor: I think the industry will manage around it. The industry has been growing strongly in Mexico and the Far East, where there are very large labor pools.

According to a new report from Frost & Sullivan (www.frost.com), the medical sector of the EMS market amounted to $227.7 million last year. The firm predicts this sector will reach $1.3 billion by 2006. The new report, North American EMS Market for the Medical Industry, describes the growth of the medical sector as "huge."

Medical OEMs had been slow to adopt outsourcing because of a lack of confidence in EMS providers, says Frost & Sullivan. FDA (Food and Drug Administration) regulation of the U.S. medical industry presents a new set of challenges to EMS providers.

"Meeting the quality control standards demanded by the FDA is the number-one concern when medical OEMs select EMS firms," states Frost & Sullivan analyst Adam Fries. "Since medical OEMs have been slow to outsource, many EMS organizations have attained minimal experience. EMS firms that have medical manufacturing know-how can leverage this experience into increased market share."

The study points out that large medical OEMs have begun to embrace the benefits of outsourcing as a competitive strategy, and EMS providers are aggressively targeting these organizations.

Data from MMI indicate that Frost & Sullivan's estimate of the 1999 medical sector is conservative. In 1999, 19 EMS companies from the MMI Top 50 accounted for $890.7 million in medical revenue. By far, the provider in that group with the most medical sales was SCI Systems, with about $433 million, or 49% of the group's medical revenue. Coming in second was Plexus, which showed about $153 million in medical sales. Medical sales data was calculated from market mix percentages provided by Top 50 companies (April, p. 5).

Even $890.7 million doesn't completely cover medical work done by the EMS industry last year. Another three Top 50 companies, including Solectron, reported doing business in the medical sector without giving a sales percentage for the sector. In addition, there are some smaller companies providing EMS for medical companies.

A few such as Colorado MEDtech, a NASDAQ-listed company, specialize in the medical field. The provider offers a OneSource OutSource approach to medical product companies. What's more, Colorado MEDtech's medical business extends beyond contract manufacturing to areas such as software development, disposables, automation equipment and branded ultrasonic products. Sales for fiscal 2000 ended June 30 totaled $74.0 million versus $75.7 million in the prior year. Another public company in this category is ZEVEX International.

Medical contract manufacturing is not limited to the U.S. either. For example, an Israeli company, Elscint Industrial Solutions, manufactures high-end medical products such as imaging systems on an outsourced basis. Elscint's Medical Division builds CT scanners and scanner assemblies for Marconi Medical Systems, nuclear imaging systems for a GE Medical joint venture, mammography systems for Philips Medical Systems and ElscinTEC Systems, and a laser system for ESC-Sharplan Medical Systems. Other medical customers include UltraGuide, BioMediCom, Odin Medical Technologies and TxSonics. Elscint Industrial Solutions is a subsidiary of Elscint Ltd., a member of the Europe-Israel Group with holdings ranging from real estate to hi-tech. The Elscint subsidiary also has a division that manufactures equipment for the semiconductor industry.

According to a new poll conducted by SG Cowen Securities (Boston, MA), 75% of respondents expect to increase outsourcing between now and 2002. SG Cowen's Fourth Annual Electronics Outsourcing Survey included participants from 79 companies with total 1999 revenues of $340 billion and COGS of $220 billion.

What's more, 42% of respondents said they had manufacturing facilities that could be divested without interrupting other functions. Of those respondents with facilities that could be divested, 41% plan on selling these assets within the next 12 months. This pool rises to 48% for those who plan to sell within 24 months.

According to the poll, by 2002, demand for design services is expected to increase by 40%, while the call for direct delivery and depot repair is projected to grow by 102% and 92% respectively.

OEMs in the survey average about 8.7 EMS suppliers, which is expected to decrease to 7.5 by 2002. But OEMs with a small number of suppliers expect to increase the number that they work with.

Of the respondents, 37% require their CMs to be at minimum sales level, which averaged $524 million.

Surprisingly, the survey reports that participants currently outsource 54% of their cost of goods. This figure is well above typical estimates of no more than 20%. SG Cowen says its results may be biased, as the companies that chose to respond to the survey probably utilize outsourcing more widely than others do.

A similar poll was conducted by Bear, Stearns & Co. (June, p. 9).

SCI Systems (Huntsville, AL) will acquire ERG's telecom manufacturing businesses in Perth, Western Australia, and Belgium. This is SCI's third telecom deal announced in recent weeks (Aug., p. 6). This purchase will take effect in October when more than 200 of ERG's manufacturing staff will transfer to SCI.

The company will assume ERG's contract to manufacture Nokia Networks GSM base stations at the Perth facility, as well as assuming the manufacturing contract between ERG's telecom and transit businesses.

SCI also furthered its telecom growth through two new programs from Ericsson. The provider will manufacture Ericsson's PipeRider line of cable modems as well as sub units for GSM base stations.

Viasystems Group (St. Louis, MO) has signed an agreement to acquire Lucent's Rouen Global Provisioning Center in Rouen, France. The center handles production and logistics for radio telecom and transmission products. The two companies have entered into a 30-month supply agreement.

Meanwhile Sanmina (San Jose, CA) has entered into an agreement to acquire the Lucent's San Jose system integration and fulfillment operation. The operation will manufacture messaging systems sold by Lucent and enterprise messaging systems sold by Avaya, the former Enterprise Networks Group that will be spun off from Lucent this month. Sanmina expects to take on 141 employees at closing, scheduled for September.

The San Jose site does final assembly, system-level test, configuration and direct order fulfillment.

Flextronics International (Singapore) has announced another acquisition for its Flextronics Enclosures unit. Joining the unit is Lighting Metal Specialties, with high-volume operations in Chicago, Texas and Ireland. Flextronics' merger with Chatham Technologies, also part of the Enclosures unit, has been completed (Aug., p. 1).

What's more, in a stock-for-stock deal Flextronics has signed a definitive agreement to acquire Li Xin Industries, a plastics company with operations in Singapore, Malaysia and Northern China.

Finally, during the summer Flextronics announced an agreement to take over the hardware division of Italdata S.p.A., which produced nearly 350,000 PCs last year. Located in Avellino, Italy, Italdata is 50.2% owned by Siemens and 49.8% owned by Telecom Italia. The division employs 264 people. Italdata had been looking for a partner after concluding its relationship with Fujitsu Siemens Computers.

New facilities...Celestica (Toronto, Canada) has broken ground on a 200,000-ft2 facility in Rochester, MN, to house the company's Rochester operations acquired from IBM....Manufacturers' Services Ltd. (Concord, MA) is adding a second operation in Spain. Located in Tarragona, the 76,000-ft2 facility is expected to be fully operational by Q4....Able Electronics (Mountain View, CA) has opened a 26,527-ft2 operation in Tijuana, Mexico. The CM was relaunched in November 1999 when Jabil Circuit sold off the former Silicon Valley operation of GET Manufacturing (Dec. '99, p. 5).

Deal done...ACT Manufacturing (Hudson, MA) has completed the purchase of Bull Electronics Angers for a price of about $56.6 million, plus a working capital adjustment estimated at about $50 million (July, p. 6).

Corrections: Last month's news (p. 10) failed to report that Jabil's $1.5-billion shelf registration covers the sale of stock and warrants as well as debt securities....Also last month, Gerry DeBiasi of Chatham Technologies, now part of Flextronics, was misquoted on p. 2. The quote should have read: "I guarantee it will cost a lost less to ship the boards for that base station versus shipping the base station enclosure to the boards."

Component shortages continue to plague the industry, but they are not the only scarce resource in this period of outsourcing plenty. The supply of labor, particularly in professional and technical fields, can also pose a major challenge. And this condition may well outlast the component shortages that have received so much attention this year.

Of course, labor availability depends on where you are in the world and whom you're trying hire. But in high-tech manufacturing centers such as the Bay Area in California and Eastern Massachusetts, the problem can be acute. Labor "is definitely an issue with everybody around here," says Mark Hashem, director of operations for Plexus NPI Plus - New England. When there's not enough people to support the business, providers are left with a dilemma. "The question is whom do you want to support. So you start being more selective than maybe you want to be," says Hashem.

Not only can tight labor affect the ability to support customers, it can also influence where programs are placed. Take the Bay Area. "I think that OEMs should be cautious about placing new programs in the Bay Area because of the tighter labor market affecting engineering, program managers and technicians," says Robert Freid, president of Contract Manufacturing Consultants.

For some time, the Bay Area has been a notoriously difficult place to find technical professionals such as test engineers. CMs often compete with OEMs to hire these prized people. Program managers have also been a scarce commodity there. Since program management is a skill acquired from working in a CM, program managers cannot be found within OEMs or other industries. So CMs in the Bay Area have been known to raid each other for program managers. Scarcity also crops up on the direct labor side. Freid reports that debug technicians are highly sought after.

One could argue that the EMS industry is a victim of its own success. The industry's high growth rate creates a continuing demand for certain skills. Satisfying that demand becomes more difficult in the tight labor market of today's U.S. economy.

Indeed, the dearth of U.S. labor with EMS skills may well persist longer than the component shortages do. Suppliers can add capacity to produce more components, but one cannot put up an academy to instantly mint engineers or a training facility to turn out experienced program managers. Granted, employees from OEM divestitures will alleviate the problem somewhat. But CMs still need to support organic growth, which shows no signs of letting up.

Is it time to panic? No. The EMS industry is resourceful: It has been through tight labor markets before. Only now the stakes are higher. So look for EMS management teams to become more creative in their handling of the labor issue.

Labor can no longer be taken for granted. And it will play a greater role in decisions about new plant sites, program placement, employee training, and even customer screening.