World Markets

Market Focus

Flextronics and Solectron Step on the Gas in Automotive

Design

ODM Group Shows Overall Growth

News

3Com To Outsource All Manufacturing

New Gateway Model Relies On Outsourcing

Last Word

Jabil Circuit must be doing more than a few things right. The company finished its fiscal Q4 ended Aug. 31 with growth of 31% in Q4 revenue and 36% in core earnings versus the year-earlier quarter. What’s more, Jabil’s guidance for fiscal 2004 calls for projected sales growth of about 20% to $5.6 to $5.8 billion and core earnings growth above 25%.

What’s behind these numbers? Of course, there’s no substitute for good execution. But Jabil is following a course that should be instructive for the EMS industry at large as it enters the next 12 months of what may be an improving business climate. Although the not-invented-here syndrome may prevent some providers from considering what Jabil is doing, good companies are constantly looking for ways to improve. Jabil provides a cornucopia of food for thought. Here are some items on Jabil’s strategy menu.

Continue to diversify. As evidence of Jabil’s efforts to diversify, the instrumentation and medical segment is projected to grow from 6% of sales in fiscal 2003 to 11% in fiscal 2004. “That segment has grown purely organically 75% [a year] over the last couple fiscal years,” said CFO Chris Lewis during Jabil’s earnings conference call held this month.

Jabil’s efforts to plumb new markets have taken it to the defense industry (considered part of Jabil’s instrumentation and medical segment). The company recently added two defense industry accounts and achieved aerospace certification for two US sites.

Rely on organic sources for growth. With the economic picture still cloudy and new divestitures unappealing, Jabil will largely depend on organic sources for growth in fiscal 2004. “Of the $1 billion in additional revenue we expect, over 70% will come from completely organic sources unrelated to any acquisitions made in the past 24 months, and this growth is well diversified. Growth organic relationships exceed growth acquisition relationships by a ratio of ten to one,” said Tim Main, Jabil’s president and CEO, in the conference call. Although Jabil’s consumer business has benefited greatly by its Philips acquisition, the provider has also won fast-growing organic programs in the consumer segment. They include a major relationship in the mobile communications area.

Have your footprint ready for the next cycle. Jabil has transformed its footprint such that about 70% of its capacity is located in low-cost regions. The company does not expect any restructuring charges that will affect results in fiscal 2004. Still, Jabil has not given up on the US, which is expected to represent just over 10% of revenue produced in fiscal 2004. The company plans to shift some portion of US production into defense and medical work.

Continue to invest in design. Jabil recently added several design-based programs that are large in scale. The company now offers global design services in China, Europe and the Americas. Jabil’s engineering staff has increased in the last six months.

Do well by your customers. A significant portion of recent new wins has come from Jabil’s existing customers.

These points are by no means novel or complete. But put them together, and you have a good start on a recipe for EMS.

As a low-cost center for EMS work, Mexico has been hurt by a powerful one-two punch: the loss of demand from the high-tech downturn and the emergence of China. Indeed, Mexico has had to endure its share of restructuring. One recent example: Solectron designated for auction a 250,000-ft2 plant in Monterrey and surplus assets in Guadalajara. Nevertheless, amid the downsizing new EMS business is also flowing into Mexico.

High-volume consumer products like cell phones are supposed to be a natural fit for manufacturing in China, yet Elcoteq (Espoo, Finland) is ramping up production for a mobile-phone customer as fast as possible in Monterrey, Mexico. The provider received orders in July, installed equipment in August, got the first line up and approved in September and expects to reach high volumes by the end of the month. “It’s probably one of the steepest ramps Elcoteq has ever gone through,” said Bill Coker, director of sales and marketing at Elcoteq Americas (Irving, TX).

Elcoteq had to quickly come up with four production lines for this program. Three were purchased, and one was reassigned from within the company. “Our goal is to produce a phone every 21 seconds off those lines,” said Coker.

The cell phones coming off those lines are for the American market. According to Coker, the mobile-phone customer determined that it was cheaper to build in Mexico for North America than in China for North America. This customer looked at “what is the real landed cost and the cost of flexibility,” he said. Coker noted that this customer, which looks at building phones with more of a BTO/CTO model, “likes to do final configuration and distribution in the US or close by.”

The growing Mexican market for cell phones provides another reason for building handsets in Mexico. To protect its market, Mexico charges a tariff of 18% on imported mobile phones. Elcoteq is seeing Asian companies such as ODMs or Korean manufacturers wanting to build handsets in the Mexican market to avoid paying that duty. “So we think that trend will fuel more mobile phone growth for Mexico,” said Coker.

Electronic Product Integration Corp., or EPI (Rochester Hills, MI), has also shown that Mexico does not always lose business to China. Two customers have shifted work from China to the company’s EPIC Technologies operation in Juarez, Mexico. One of them is Flowserve, a company in the flow control industry. Flow-serve started with one assembly in the Juarez plant and has since moved work from China to the Mexican plant. The other client is an unnamed automotive customer.

Why did these customers take this step? “What these customers found was they weren’t getting the level of flexibility they needed out of China,” explained Todd Baggett, director of business development at EPIC.

The Juarez operation offers customers complete finished goods kanban. “That’s something they really can’t get out of China,” said Baggett. EPIC typically ships within one to two days upon receipt of a pull signal.

A logistics center across the border in El Paso, TX, provides the Mexican facility with raw material and finished goods warehousing and distribution services. EPIC’s Norwalk, OH operation uses the same finished goods replenishment methods and level load signaling.

Despite holding finished goods in kanban locations, EPIC is still turning its inventory well above industry norms in Mexico. This result is made possible because component suppliers have agreed to support kanban and inventory consignment. To achieve the necessary flexibility, EPIC uses a bin management tool that sizes component inventory bins in relation to historical consumption patterns and the desired level of customer service. “Component suppliers have recognized this tool as a strategic differentiator for EPIC and have gone the extra mile to help ensure its success, thus ensuring their own,” said Baggett.

The Mexican operation is also winning business that might otherwise have gone to China. For instance, the Juarez facility just won a contract from A.O. Smith for a motor controller product. According to Baggett, this customer did all the math in comparing Mexico to China and decided to stay in North America with EPIC. But even Baggett admits that certain products will end up in China where product cost savings are the overriding factor.

Reflecting the influx of new business, employment in the Juarez operation more than doubled during its first year completed this summer. The 70,000-ft2 facility now employs 260 people. What’s more, EPIC is now looking for a second facility in Mexico.

Most of EPIC’s growth is targeted for Mexico. “We’re going to see this fiscal [calendar] year 50% year-on-year growth. We’re expecting the same next year as a company,” said Baggett.

EPI got started in Mexico last year when it acquired Mexican assets and business from another EMS company, IEC Electronics, which closed a facility in Reynosa (July ’02, p. 4).

SigmaTron International (Elk Grove Village, IL), on the other hand, offers a somewhat different slant on Mexico. The company has started construction of a new facility in Wujiang, China (see News, p. 6) and expects to move some of its business in Mexico to the China facility when it is ready. Still, SigmaTron believes that Mexico will remain an important part of its future and will continue to grow.

Mexican operations are split between two plants located six miles apart in Acuna. SigmaTron recently leased a 27,000-ft2 building next to a plant it owns there. The company plans to consolidate Mexican operations into one location over the next 12 months in an effort to lower overhead costs and increase efficiencies.

SigmaTron’s Mexican subsidiary has been in operation since 1969.

The foregoing shows that there are cases when Mexico wins over China. The need for flexibility can tip the scales toward Mexico, even for high-volume products.

It’s no coincidence that both Flextronics and Solectron have been increasing the number of their plants that are automotive certified. Both have zeroed in on automotive electronics as a large market opportunity that can bring both growth and diversity to their businesses. With the possible exception of Foxconn, tier-one providers are all pursuing automotive business in one way or another.

But you can’t get in the door of an automotive account without the necessary certification. These days, the certification to obtain is ISO/TS 16949, which was developed by ISO and a task force partly made up of automotive manufacturers. This standard will replace the existing QS 9000 standard for automotive supplier quality by 2006.

Reflecting stepped-up efforts in the automotive market, five Solectron sites recently earned TS 16949 certification. These sites are located in Canada, Germany, Mexico, Romania and Singapore. As of mid August, Solectron had expanded to 17 the number of its facilities certified to TS 16949 and/or QS 9000. Obtaining TS certifications was an important goal for Solectron’s automotive unit launched last year. “I feel that we’ve made a significant amount of progress in that our global footprint now has the TS certifications to be able to support the automotive customers. We did not have that in place when we made our launch,” said Chris Lafferty, director of automotive business development at Solectron.

Flextronics has also been mindful of the need for certification, and the company reports all of its automotive plants today are either QS or TS certified. Three plant certifications are currently underway. For automotive work, Flextronics uses regional facilities in Europe; low cost sites in Mexico, China, Malaysia and Hungary; and Brazil when local requirements warrant it.

The top two providers are not the only ones adding plant certifications. For example, Sanmina-SCI, via its website, states that several of its plants are becoming TS 16949 qualified. The move to TS certification extends beyond the top tier. For instance, EPIC Technologies is preparing its Juarez, Mexico plant for TS certification (see previous article).

While the automotive opportunity has spurred these certification efforts, getting a quantitative handle on it is not easy. Estimates of the automotive electronics market vary. One market research firm, Strategy Analytics, puts the 2002 market for automotive electronics controllers at $30.5 billion worldwide. Another firm, Freedonia Group, describes automotive electronics as a $75-billion global industry. Given such variation, it is also difficult to come up with an EMS penetration ratio for the automotive segment. Still, Flextronics, which has done its own bottoms-up assessment of automotive electronics, believes that the tier-one automotive suppliers are underpenetrated by the EMS industry.

The two market research firms, however, agree on one thing – the growth rate of the automotive electronics market. And that growth, of course, will be driven by the increasing electronic content within vehicles. Strategy Analytics forecasts annual growth of 7.5% from 2002 to 2007, while Freedonia projects 7.1% through 2007. This steady growth offers a refreshing contrast to the uncertainty of other market segments. And the growth rate may be even higher, based on Solectron’s numbers. “The electronic content is growing faster than 10% per year,” said Solectron’s Lafferty.

Obviously, the tier-one automotive suppliers hold the keys to outsourcing of automotive electronics. According to a 2002 study by Technology Forecasters, tier-one suppliers were 21% outsourced last year (Dec. ’02, p. 5). Solectron, for one, bears good news from the tier-one group. “We have seen a good level of activity in the tier-one automotive supply base to engage and work with the EMS providers,” reported Lafferty.

But he pointed out, “Things move at a different pace in the automotive electronics side than, for example, in the cell phone marketplace or wireless infrastructure.” So Solectron has seen more outsourcing activity, but it has taken place over the last 12 to 24 months. For example, Delphi Automotive during that period awarded Solectron what was described as a sizable program (March ’02, p. 7). Solectron also serves tier-two suppliers and in some cases, tier-three companies.

Flextronics’ customers are the tier-one suppliers. “Several of the largest who have typically been internally focused around their manufacturing are beginning to look at outsourcing on a larger scale than they may have in the past or in some cases, even for the first time,” said Joe Minville, senior director, business development for global automotive markets at Flextronics.

The company’s recent efforts in automotive extend beyond plant certifications to the design side. This part of Flextronics’ automotive thrust makes sense given the provider’s well-documented strategy to pursue design-and-build business. Flextronics wants to capitalize on the desire to use consumer electronics devices such as mobile phones, PDAs and MP3 players within the car and to interface them with the car seamlessly. As the automotive industry looks at how to do that, Flextronics can offer its strength in consumer and commercial applications.

So Flextronics’ work in entertainment systems, tire pressure monitoring systems, telematics and other wireless technologies has drawn interest from the automotive companies, according to Minville. “From a design perspective, we want to leverage our strength in those areas to help our customers with new designs and new products that they might want to get in the car to allow them to enhance this portability, if you will, of their devices into the vehicle,” he said.

Solectron also wants to participate in the front end of automotive programs and has set up regional capabilities for product development.

But an automotive product can take three years to go from concept to production. That’s a long time to wait for revenue. So Solectron looks to mix in automotive programs that are closer to production. Presumably, other providers follow this approach is as well.

Once you’ve landed an automotive program, it can last five years or more in production. Such stability appeals to providers looking for a more dependable revenue stream. But automotive customers can be demanding. They impose quality and delivery requirements that providers may not be used to seeing from other clients.

Despite recent efforts in automotive, neither Flextronics nor Solectron can be considered newcomers to the segment. It is not widely known that Flextronics has manufactured automotive products for eight-plus years. Solectron’s origins in automotive can be traced at least as far back as its 2000-2001 acquisitions of Sony facilities and NatSteel Electronics. Solectron’s automotive capabilities expanded with the acquisition of C-MAC Industries in 2001. Both Solectron and Flextronics manufacture a broad range of automotive products. Of course, the tier-one EMS provider with the longest history in automotive is Jabil Circuit, which was founded as an automotive contract manufacturer.

Will these efforts by Flextronics and Solectron pay off? Although automotive electronics is a large and growing opportunity, the tier-one automotive suppliers must outsource more if EMS providers are to gain lots of new business in the segment. Not all tier-one suppliers are major electronics manufacturers. “So if you look at the electronic capabilities within some tier ones, they really do need to and in many cases are already outsourcing that electronics,” said Solectron’s Lafferty. “Even some of the premier tier ones that have electronics capabilities can’t do it all. They’re focusing on more of a system integrator position, for example, where they would have an entire cockpit and may not have the wherewithal to handle all of the electronics.”

Ultimately, the pressure to outsource may come from car companies themselves looking for ways to cut costs. “The OEMs are definitely struggling to be profitable, and the old recipe of just selling more cars to get more profit isn’t working. So it just feels like we’re on the brink of a sea change, if you will, in the way the supply chain has run today. But I don’t know how it will actually turn out,” said Flextronics’ Minville.

Back to Table of Contents

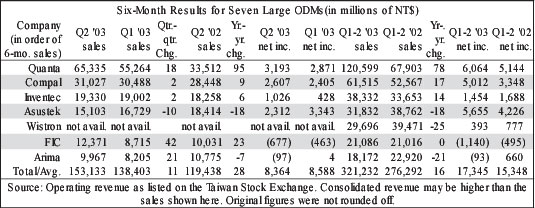

Seven large ODMs combined for overall growth of 16% in the first half of 2003 versus the same period a year earlier (table, p. 5). Compare that result with an aggregate decline of 4% in the first half for nine of the largest EMS providers (Aug., p. 7). If these two groups are representative of their respective markets, then the ODM market appears to have done better in the first half than the EMS business did.

Furthermore, five out of seven ODMs were profitable in the first six months, while just three out of nine EMS providers reported positive net income. First-half net income for the ODM group nearly kept pace with sales growth in the period as net income increased by 13% from the first six months of 2002.

For Q2, six out of seven ODMs showed a combined sales growth of 11% over Q1 2003. On a year-over-year basis, Q2 sales for the six rose by 28%. One ODM, Wistron, was not included because Q2 results for company were unavailable.

Together, the seven ODMs accounted for sales of NT$321.23 billion, or about $9.4 billion, in the first half. First-half results varied widely from a 78% sales increase year over year by Quanta Computer to a drop of 25% by Wistron. Indeed, Quanta, the largest ODM in the group, had by far the highest growth rate in the first half.

Note that results were obtained from operating revenue data listed on the Taiwan Stock Exchange. Not all of the revenue reported is necessarily ODM because ODMs sometimes sell products directly under their brand name to end users.

This analysis excluded three other large ODMs – BenQ, Lite-On Technology and MiTAC International – because operating revenue from the Taiwan Exchange did not agree with consolidated results or other data listed by the companies.

3Com (Marlborough, MA), a provider of networking products, plans to complete the outsourcing of its manufacturing and realign its product development and supply chain activities. The company will use Flextronics (Singapore) and Jabil Circuit (St. Petersburg, FL) for the remainder of its outsourcing.

Over the next six months, 3Com will complete the outsourcing of all of its direct manufacturing, distribution and related activities through the two EMS companies. Flextronics will also assume responsibility for 3Com’s global distribution from its regional hubs.

These actions will result in the closure of 3Com’s Dublin, Ireland facility, which is expected to occur by the end of February 2004. The production being outsourced to Flextronics and Jabil will essentially be the load at the Dublin facility. That load mostly consists of stackable switches, low-end hubs and some voice products.

Worldwide, about 1000 3Com employees in manufacturing, product development and supply chain operations are affected. A majority of the employees are associated with manufacturing and supply chain activities.

This is another example of an OEM deciding to close – as opposed to selling – a manufacturing operation in a high-cost region. A 3Com spokesperson would not comment when asked if the company had considered selling the Irish plant or had offered it for sale. Presumably, either Flextronics or Jabil could have acquired the plant if they had wanted it.

3Com is realigning its product development with the establishment of a Taiwan Design Center, which will be responsible for the continued design and manufacture of low-end, standardized volume products. The center will be staffed by 3Com employees and ODM partner employees. The networking company expects this center to be operational in the November quarter and fully staffed by the end of the May 2004 quarter.

So 3Com’s outsourcing strategy also includes an ODM component for low-end products with the necessary volumes. Company CEO Bruce Claflin said 3Com will focus its internal engineering on high value-add product areas such as voice-over-IP, ASICs, XRN architecture and security.

According to a report in the Taipei Times, 3Com is already using two Taiwanese ODMs – Accton Technology and D-Link – for production of switches.

3Com also sources switches and routers from Huawei, a large Chinese manufacture of networking equipment.

For Flextronics, this outsourced work will extend its relationship with 3Com. In 2001, 3Com entered into an EMS contract with Flextronics for 3Com’s high-volume server, desktop and mobile connectivity products (July ’01, p. 7). According to the 3Com spokesperson, the relationship with Jabil is new. However, 3Com had been listed as a Jabil customer in the past (March ’99, p. 2).

3Com said outsourcing to Jabil and Flextronics is a key part of these restructuring initiatives to lower 3Com’s cost structure.

Gateway (Poway, CA), which is transforming itself from a PC company to a branded integrator, has announced a new fulfillment model based on using strategic partners, collaborative planning and consolidation of in-house resources. The company will engage multiple manufacturing and service partners in the US and overseas for its PCs and consumer electronics.

As an initial part of this plan, Gateway will close its Hampton, VA manufacturing site on Sept. 30 with a reported loss of 450 jobs. The company will also reduce staffing at its locations in North Sioux City and Sioux Falls, SD as certain activities shift to partners and other facilities. Here is yet another case of an OEM closing a facility in a high-cost region.

Once fully implemented, the new fulfillment model is expected to result in annualized savings of $115 to $130 million.

Gateway chairman and CEO Ted Waitt said Gateway is completely redesigning product sourcing, logistics, service and support to create a more efficient infrastructure.

The Wall Street Journal reported that the company has been in discussions with Celestica, Solectron and Taiwan’s Wistron.

Average analyst consensus estimates project 2003 sales of about $3.5 billion for Gateway.

Some new programs…Jabil Circuit has won new customers including VeriFone, GE, Harris, Microsoft and Honeywell….Elcoteq Americas (Irving, TX), a unit of Elcoteq Network (Espoo, Finland), will manufacture wireless LAN (Wi-Fi) systems for Strix Systems (Westlake Village, CA). Production will take place in Elcoteq’s Monterrey, Mexico plant…. Raytheon Company’s Space and Airborne Systems (El Segundo, CA) has awarded LaBarge (St. Louis, MO) an additional contract in excess of $10 million to continue to produce backplane assemblies for the F/A-22 Raptor, a new stealth fighter developed for the US Air Force. LaBarge had previously won a $3.2-million contract to manufacture these assemblies.

New facilities…PEMSTAR (Rochester, MN) has opened a Product & Technology Development Center in the company’s Singapore facility. The Development Center will provide engineering design and support for high-volume production at PEMSTAR manufacturing sites worldwide and will develop key technology building blocks for markets served by the company. In addition, the new center will work jointly with the existing Equipment Group to support operations in Bangkok, Thailand, and Tianjin, China…. Nam Tai Electronics (Hong Kong) has started construction of a new factory adjacent to its main manufacturing campus in Shenzhen, China (Feb., p. 8). The $40-million project will add about 250,000 ft2. This new factory will include a 65,000-ft2 clean room to produce high-end components such as LCD modules, RF modules and CMOS sensors for cell phones. Processes required for these components include chip on film, chip on glass and ball grid array. The new plant will probably begin production in Q2 2005….During the fiscal quarter ended in July, SigmaTron International (Elk Grove Village, IL) broke ground for a new facility in Wujiang, China, and production is slated to start there during the April 2004 quarter (March, p. 8).

Techdyne (Hialeah, FL), a publicly held contract manufacturer, has taken the name of the Scottish EMS company that owns a controlling interest in it. Thus, Techdyne, which is 71% owned by the Simclar Group (Dunfermline, Scotland), has changed its name to Simclar, Inc. As a result, the company’s Nasdaq trading symbol has changed to SIMC.

“Simclar is known throughout Europe and Asia as a quality contract manufacturer. We believe the name change from Techdyne, Inc. to Simclar, Inc. will avail Techdyne of name recognition and additional market exposure,” stated Sam Russell, chairman of Simclar Group. He also said the name change will help in selling customers on higher levels of product integration.

For Q2, Techdyne, now Simclar, Inc., reported revenue of $7.7 million, down 5% from $8.1 million in the year-earlier period. Net income amounted to $240,823, compared with $221,650 in Q2 2002.

The company recently expanded into Mexico with its acquisition of AG Technologies (July, p. 5).

CirTran (Salt Lake City, UT), a contract manufacturer of PCB assemblies, cables and harnesses, has engaged a Southern California M&A firm, MET Advisors, to help CirTran in its search for acquisition candidates. The CM’s targets include small to midsize companies that can integrate well with the company while providing diversification of revenues. CirTran is also working with other M&A consultants.

The company’s goal is to identify, close and fund at least one acquisition by year end as part of its overall growth strategy.

For the first six months of 2003, OTC-listed CirTran reported a net loss of $1.2 million on sales of $686,536, compared with a net loss of $725,305 on sales of $1.6 million in the year-earlier period. As of June 30, the company had an accumulated deficit of $16.4 million and a total stockholders’ deficit of $4.7 million.

But CirTran says it is about to close $1 to $2 million in financing from an investment firm to settle old judgments and take care of tax problems. The company also expects that some shareholder debt loans will convert to equity. As a result, the $4.7 million in negative equity is expected to turn into a positive $6 or $7 million, according to Trevor Saliba, senior VP of worldwide business development at CirTran.

In addition, he reports that CirTran has a pipeline probably close to $10 million in promised business from five to six new clients.

Last November, the company secured a $5-million equity line of credit from Cornell Capital Partners LP.

CirTran maintains 40,000 ft2 of manufacturing and office space in Salt Lake. A subsidiary, Racore Technology, develops high-performance LAN products. Racore recently received an initial order for fiberoptic Ethernet NIC (network interface card) products from the US Air Force. These products are manufactured by CirTran.

Some financial news…Through a recent tender offer, Flextronics retired 9 7/8% senior subordinated notes with an aggregate principal amount of $492.3 million, representing 98.5% of the total principal outstanding (Aug., p. 6). Flextronics paid $582.6 million, including accrued and unpaid interest, for the notes due 2010….Benchmark Electronics (Angleton, TX) reports that 100% of its 6% convertible subordinated notes due 2006 were converted into Benchmark’s common stock at $40.20 per share (Aug., p. 6). The principal amount outstanding was $80.2 million….Nam Tai Electronics has asked the SEC to withdraw Nam Tai’s registration filing for a proposed offering of 9 million common shares (Aug., p. 6). The company has just raised $5.07 million in cash from the disposal of its convertible bond notes in TCL International Holdings. With the addition of this money, cash on hand totaled about $77 million despite capital expenditures. Nam Tai believes that its cash on hand, plus cash flow from operations, together with other income and banking facilities should suffice to support internal growth and expansion for the next two years....SMTEK International (Moorpark, CA) has announced the private placement of 250,000 shares of its Series A preferred stock for $500,000. The buyer is an independent investor who is also a customer. The proceeds will be used for general purposes. Dividend yield of the preferred shares is 9%....For the fiscal Q1 ended July 31, SigmaTron International posted sales of $22.1 million, up 15% from $19.2 million in the year-earlier period. Net income for the quarter climbed 112% to $1.3 million versus $616,201 in the prior Q1…Nasdaq has notified Reptron Electronics (Tampa, FL) that it has failed to comply with criteria for minimum shareholders’ equity, minimum market value, and minimum net income from continuing operations. Therefore, Reptron’s common stock is subject to delisting from the Nasdaq SmallCap Market. Trying to keep its Nasdaq listing, Reptron has requested a hearing before a Nasdaq panel.

EMS company growth in Asia and Europe...For the first half of 2003, Taiwan's Hon Hai, also known by its Foxconn trade name, reported sales of NT$121.8 billion, or about $3.6 billion, up 21% from the year-earlier period. Net income for the first six months increased 26% year over year to NT$10.1 billion....Venture (Singapore) posted first-half sales of S$1.38 billion, or about $793 million, a 53% increase over the same period in 2002. First-half net profit rose 35% year over year to S$101.0 million. ...First-half sales for Elcoteq Network (Espoo, Finland) went up 23% to 1.02 billion euros. Pretax profit was 3.5 million euros in the period.

New software purchased…New Visions Manufacturing, an EMS company in Springfield, MA, has bought NPI engineering software from Valor Computerized Systems (Yavne, Israel). The initial order for Valor’s Trilogy 5000 solution is valued at $250,000….EMS provider Nextek (Madison, AL) has purchased NPI and MES software modules from Aegis Industrial Software (Horsham, PA).

People on the move…Thomas Sabol has resigned as executive VP and COO of Plexus (Neenah, WI). Sabol joined the company seven years ago as CFO. “He has been especially effective in leading the company’s restructuring efforts as we responded to changing industry conditions. The company is now posed to return to growth and profitability, and Tom has taken this opportunity to pursue other career interests,” stated Dean Foate, Plexus president and CEO. Sabol’s responsibilities will be assumed by other executives in a leaner organization….Frank Burke has resigned as CFO of SMTC (Toronto, Canada). Burke will remain with the company through a transitional period, which allows for a successor to be named. During Burke’s tenure that began in October 2001, the company improved its cost structure and reduced its debt. “I believe that I have completed the tasks that I had set out and that this is an appropriate time for me to make this change,” said Burke….Ajay Shah has resigned as a member of Solectron’s board of directors. The company said he gave up this position in order to devote more time to his business interests and investments. Before joining the board as a nonemployee director in January 2002, Shah served as a Solectron executive VP. He came to Solectron when in 1999 it acquired SMART Modular Technologies, a supplier of memory, embedded products and other devices. Shah was chairman, CEO and cofounder of SMART Modular. Observers wonder if his resignation portends any other changes at Solectron.

After nearly three years of painfully weak end markets, there are some nascent signs that a recovery may be underway. It’s probably too early to be sure about that, but one can certainly start preparing for an upturn, whether it is starting now or next year. Providers might say that restructuring has already prepared them to benefit from improving customer demand. In one sense, this is true. But OEMs and their EMS providers have been playing by one set of rules through the downturn. When market conditions improve, those rules will change.

During this extended period of overcapacity, large providers, in some cases, have taken on programs that they might have passed on a few years earlier. During the boom times, these programs would have been too small. But empty lines become a powerful motivation. These contracts also add to the number of new program wins that a provider can claim. What’s more, some of these smaller programs give providers new customers in markets targeted for diversification.

When demand picks up, will large providers still want to keep their small customers, especially those who expect the royal treatment of a major account? Some observers say the small accounts acquired during the downturn will be jettisoned once factories begin to fill up. But it’s probably not as simple as that. Large providers have always designated certain small customers as strategic, meaning that these companies stand a good chance of being big customers some day. Nevertheless, the practice of dropping customers, which has been going on in the industry since its early days, will probably increase once recovery is in full swing.

Larger customers will also find the rules changing. During these tough times, they have expected and received cost reductions from their EMS suppliers. Much of the cost savings has come from shifting customer production to low-cost regions, particularly China. Once production has been moved, there is much less potential for cost reduction. So these OEMs will find that they can no longer expect the cost reductions that were quoted during the downturn. This emerging trend has led Flextronics, to name the most conspicuous example, to offer customers ODM solutions that afford much greater cost reductions than can be obtained by EMS alone.

As factories begin to fill up, EMS providers will be paying close attention to the customers that are using up that capacity. Customers that are yielding below-par returns will find their providers less willing to carry them and even less inclined to invest in any capacity on their behalf. OEMs that squeezed their suppliers during the downturn and got away with it may well discover that providers’ resources will be allocated elsewhere unless contracts are revisited.

When end markets pick up, customers will lose leverage in their relationships with EMS providers. This is nothing new. It just seems that way because the rules of the game have favored OEMs during the downturn.