![]()

Cover story

Market Makers

Supply Chain

Collaboration at Hub of Private Networks

News

PartnerTech Gains Polish Presence

Korea Computer Enters EMS Market in US

In January, MMI predicted that the EMS industry would grow nicely this year despite any slowdown. The power of outsourcing would overcome any loss in end market demand. But the rapidity and severity of the current downturn, especially in communications, has been overwhelming. Virtually no one, MMI included, saw it coming. But come it did, leaving growth prospects for the current year in doubt, if not in shambles. Although this downturn is no fun, it is leaving its mark. In particular, the downturn has shaken some widely held beliefs about the EMS industry.

· The first is: The industry will grow 20% or more year in and year out. It is unlikely that a 20%+ growth rate will be seen this year. But even if the industry posts no growth - and that remains to be seen - the longer term growth potential is still intact. That's because last year's growth was at least 44%, probably a record. When both years are taken together, one will find that the two-year average will probably be in line with long-term industry forecasts. Still, this downturn has taught the industry that despite the benefits of outsourcing, growth is not necessarily a given.

· Another assumption says as the EMS industry grows CMs will continue adding plants. But restructuring, once reserved for OEMs, is now in the industry's lexicon (Mar., p. 5-6). All of the top-four CMs have announced restructuring plans. These go well beyond the normal ebb and flow of jobs in the industry. The latest announcement comes from Celestica, which will undergo facility consolidations and a work force reduction of up to 3000 jobs globally. For example, the company is consolidating from three design labs for power to two and from three UK repair facilities to one.

Other details of these plans are starting to come out. Solectron is closing its plant in Suwanee, GA. Some 750 full-time employees and 325 temporary workers will lose their jobs. The 370,000-ft2 plant will undergo a transition period of four to six months. These cuts come in addition to the CM's previously announced reduction of 8200 jobs. The plant was originally set up in 1999 to consolidate Georgia operations acquired from NCR and Mitsubishi.

Flextronics intends to close down its 110,000-ft2 plant in Binghamton, NY, during the first week of June. Reportedly, 600 people work at the plant, which was obtained in the company's acquisition of the Dii Group. In addition, Bloomberg News is reporting that Flextronics will shift most of its production in Singapore to Malaysia and China. Earlier, Michael Marks, Flextronics chairman and CEO, told analysts that the company would cut a number of enclosure facilities in higher cost areas.

SCI Systems is closing plants in Arab, AL; Graham, NC; and Mexico City, Mexico, and is downsizing its San Jose, CA, operation from full-service manufacturing to new product introduction. In addition, SCI is combining operations in Fountain and Colorado Springs, CO, at the Fountain site.

Plant closings are not limited to the top tier. SMTC will shutter its 125,500-ft2 facility in the Denver, CO area. Production there will be moved to other SMTC facilities including the CM's Chihuahua, Mexico site. SMTC says it selected the Denver facility because it needed to be upgraded and was not in the best location to serve customers. The facility was formerly operated by Hi-Tech Manufacturing, which merged with SMTC.

· Industry doctrine also says M&A activity is supposed to keep increasing. But MMI counts 15 deals announced in Q1, compared with 29 in the year-earlier quarter. The Q1 drop in deal-making runs counter to the past seven years of consecutive growth in industry M&A (Feb., p. 1).

Why the decrease? MMI can speculate that there are at least two reasons: economic uncertainty and excess capacity, both resulting from the downturn. A CM with excess capacity will need a compelling reason to buy another CM. Still, one cannot rule out bargain hunters pursuing deals going forward. But in some cases, there will be the temptation to let a CM founder and wait for its customers to abandon ship. Sanmina tells of one such case in the next article.

But the downturn spells good news for CMs looking at asset divestiture deals. OEMs had been in the driver's seat, but the downturn has reduced their leverage. OEM facilities in higher cost locations are not as appealing as they once were.

"We've seen a lot of places that nobody has picked up on. I think everyone is getting choosier," said Eugene Polistuk, Celestica's chairman and CEO, during its Q1 conference call. "It's a perfect environment. Opportunities are up. Prices are dropping. And everyone is being very selective. So it's a sweet time from the point of view of asset divestitures from the OEMs."

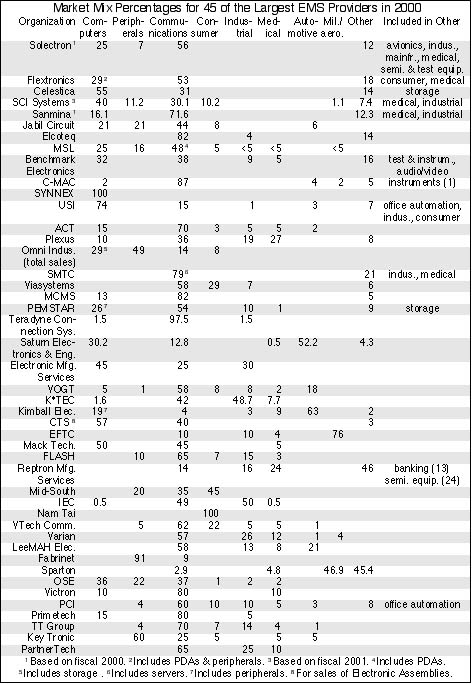

· People put their faith in communications. But the go-go segment

of recent years has suddenly lost its power as an engine of high growth.

Yet the EMS industry has become increasingly dependent on this segment.

Out of 45 MMI Top 50 CMs that supplied market mix data, at least 26 companies

relied on communications for 40% or more of their sales in 2000 (see table).

On the other hand, niches with slower growth but more stability are looking pretty good at the moment. Take Morey Corp., a $50-million CM in metro Chicago, IL. The privately held CM derives 60% of its business from industrial and avionics customers. Its niche centers on ruggedized electronics for trucking, construction equipment and agricultural equipment.

"We're growing nicely. We're in a very specific niche, and the niche we're in seems to be insulated from the overall trends we're seeing in the electronics manufacturing industry," says Ross Clark, Morey's director of marketing.

Last month, Morey started shipping a display for Pierce Fire Trucks. Also, the CM has won a program to manufacture an electronic transmission control for Transmission Technology Corp. In both cases, Morey managed product design.

These downturn effects offer the industry an important lesson. Take nothing for granted and expect the unexpected.

When it comes to profitability in the EMS business, Sanmina takes a back seat to no one. Even competitors cannot help but be impressed by Sanmina's operating margin of 15.0%, excluding one-time charges, for the March 2001 quarter. How does this vertically integrated CM do it? Randy Furr, Sanmina's president and COO, says its margins result from a combination of three factors: its technology - for example, the ability to produce 50- to 60-layer boards; the capture of margins from intracompany sales at close to $1 billion; and, most important, the way Sanmina's business is managed. The third reason "is the one that people just can't buy into because it's too much of a motherhood statement," says Furr.

Believe him or not, Sanmina's management team has done more than a few things right. The company has notched 30 mergers and acquisitions over the last six years. Its annual growth rate has averaged 40% for the past five years. As a result, Sanmina has steadily climbed up the EMS ranks. Last year, it was among the six largest EMS providers (Mar., p. 2).

But today, Sanmina, like the EMS industry at large, has seen a rapid downturn in end-market demand. Where will Sanmina's future growth come from? Is vertical integration an advantage in a downturn? How will the downturn affect operations? Will consolidation increase? These are some of the questions that MMI posed to Sanmina's Randy Furr in the following interview.

MMI: Over the long term, it is generally accepted the system build business will grow faster than PCB assembly business. How important is this trend to Sanmina's outlook for the future?

Randy Furr: There are four broad groups of businesses that we try to tie together as a strategic advantage for our customers. Those four broad groups are circuit fabrication, cable assembly, enclosures, and more traditional EMS services. EMS services can be broken down into other subareas as well. Clearly, if you look at the far end, things such as cables, circuit fabrication and some enclosures, the majority of those kinds of services have been outsourced by the OEMs for a number of years now. So the market growth opportunities in those individual areas more closely parallel the overall growth of the electronics industry. Of course, our focus is at the very high end part of that industry, a portion we think is growing at the high end of the overall growth of the electronics industry. But the point is that the benefits of the trend toward outsourcing have been pretty much realized in those areas.

When you get into the traditional EMS areas - clearly, backplane assembly, some printed circuit board assembly - some of those areas have been outsourced. Although there's still a fair amount of that done internally by our customer base. More of that in Europe is done internally than here in the US, but still a fair amount is done internally.

When it comes to end-system assembly and integration, clearly there are still a lot of growth opportunities in that area. Sometimes it's referred to as box build. A lot of people often think PCs when they talk about box build. Sanmina has no involvement in the PC industry other than doing some high-end type servers and some quick-turn prototype work, which is pretty small. When we talk about system assembly, or box build, we're talking about high-end type systems of the kind that would end up in a telephone company central office, as opposed to your desktop. And as more of the OEMs move to outsource higher levels of their overall system manufacturing and move towards a global order fulfillment model, I think the key to our growth or a portion of our growth will be tied to those decisions to move towards this global order fulfillment model by the major communications companies. So clearly it's an important element for Sanmina going forward.

MMI: In fiscal 2000, communications represented 72% of sales, while 12% came from medical and industrial customers and 16% was attributed to the high-end computer segment. Does Sanmina expect to maintain this market mix in the future?

Randy Furr: It turns out this way not necessarily because it is targeted, or we want it that way. It turns out that way because if you look at where Sanmina is strong from a competitive point of view, it is strong in the design and manufacture of very high-end, complex systems. And if you look at where the bulk of those high-end systems are used, it happens that the largest market opportunities for Sanmina are by far in the communications market segment.

I do not see that mix changing significantly over the near term, because again communications are where the bulk of these very high-end, more complex type systems are used.

MMI: Who are your top-five customers? Is Nortel still the only 10% customer?

Randy Furr: We don't publicly disclose them. But first of all, Nortel is the only company over 10%. It varies from quarter to quarter between 9 and 11% historically so it barely makes that list. But it does often. Our top customers, not in any order, are Lucent, Cisco, Nortel, Alcatel, Motorola, Tellabs. Among those, the top five can vary because by the time you get down to fourth, fifth and sixth, you're talking about a 2 1/2, 3% kind of customer.

MMI: Besides adding enclosure capability, the acquisition of Segerström & Svensson expands Sanmina's footprint and gives Sanmina a presence in Brazil and Hungary. Does Sanmina plan to expand service offerings in either of those countries?

Randy Furr: Brazil is a country like China that has some rather stringent penalties for our customers if they do not have a substantial portion of in-country content. So I believe all of our top customers that want to market and sell their products into Brazil have looked to a Sanmina to provide manufacturing services in Brazil.

We've been to Brazil many times. We've had some false starts down there, more of our choosing than anything else, simply because of the economy and how really slow the market has been to develop. Segerström now offers us wholly owned subsidiaries that were really acquired from Western OEM divestitures that give us, I think, a very good operation and a good base to build on. We plan on expanding the customer base in Brazil beyond Ericsson, which has been the primary customer down there, to serve our other top customers, all of whom, I believe, have asked us to provide some form of services down in Brazil. So clearly, that will give us some expansion opportunities.

It's a little early for me to talk about Hungary. It is our first operation in Eastern Europe. We have a team that is spending some time over there. They're going to come back with a report to me on the operation. During the due diligence, we had some people go over there just to do some preliminary type work, but not necessarily to develop a longer-term strategy. I do see Eastern Europe as key long term to Sanmina. All the reports I've had on the Hungary operation have been very positive, and I certainly believe at this point you'll see Sanmina expand in Hungary as well. I think it'll just take a couple of weeks before we fine tune that strategy.

MMI: Back to Brazil, our impression is that Segerström is building enclosures and possibly putting some electromechanical work into them. Would you see Sanmina doing full system build down in Brazil?

Randy Furr: Absolutely. There are two sites down there. One is an enclosure site, and the other is an integration site. So we're already doing some subsystem-level assembly down there. I certainly see us expanding that very quickly into a full system-build type operation.

MMI: Is Sanmina through making acquisitions in the enclosure space?

Randy Furr: I do not think so. From a strategic point of view, we need enclosure capabilities in China. That is a little bit of a gap we have today. We have a number of alternatives. I will certainly be surprised if we exit this calendar year without enclosure capabilities in China. And I know we have a game plan that does involve acquisition or acquisitions. I'll be surprised if we don't get that taken care of later this year. They're not terribly large. They're not as large as Segerström. But from a strategic point of view, they still are key for us going forward.

In addition, there are a large number of buying opportunities in the enclosure area. Our corporate development people are busing looking at all those opportunities today. I don't know if any of those will come to a point where we will do additional deals. But I know there are number of opportunities that we're looking at, and some very well could happen. So I certainly don't want to say we're through making enclosure acquisitions.

MMI: Given Sanmina's focus on the high-end portion of the EMS market, one can understand why Sanmina has not entered Mexico to any great extent. Reportedly, communications products on the infrastructure side are showing up there. Does Sanmina have any plans for Mexico?

Randy Furr: We do have one plant in Mexico.

MMI: Did it come from the Comptronix acquisition?

Randy Furr: Well, no. Back in '96 I think it was, we acquired a plant in Mexico through Comptronix. Sanmina was so focused on building products for the higher-end portion of the industry...we just didn't have any product that we could put in Mexico to utilize the plant. We actually ended up closing that plant.

About nine months ago, we opened a plant down in Mexico where 100% of the services are cable and wiring harness assembly. We are one of the larger cable and wiring harness companies around. That particular service, as you can imagine, is labor intensive, as opposed printed circuit board assembly, circuit fabrication or metal fabrication, where you have a lot of equipment. The cable business is still a very labor intensive business. It's not automated that much. So it made sense for us to open a plant in Mexico, but strictly limited to cables.

It's not uncommon today for us to build low- to medium-volume products that have one or two high-volume cables or printed circuit board assemblies in them. I do think over the long term you will see Sanmina in Mexico doing some assembly. But right now it's not something that we're looking at in the near term. So I think for the present, our operations in Mexico probably will be limited to this cable operation.

MMI: What can you say about Sanmina's optical capabilities? Can you offer examples of how these capabilities are being used?

Randy Furr: About five months ago, we signed off on an optical assembly strategy. And that involved adding a few key people. It involved fine tuning a technology roadmap. It all ties to together from optical cables through optical backplanes, optical assembly and also extends into some new areas of putting together optical modules. These are not components, but what I refer to as modules that go into systems.

We have spent a fair amount of capital over this five-month period, and our team is very close to making some announcements in the optical area as to our capabilities. We want to have those capabilities fully demonstrated. We don't want to just throw out a press announcement that somebody will question. So we do have some customers in this area, and we're doing some optical modules and optical assembly today. I would expect within 30 days to see some announcement in that area.

Our optical strategy at Sanmina is closely coupled with all of our services. Take an example of an optical switch company. We can offer them a full end-to-end solution through our various service offerings.

MMI: Is it Sanmina's intention to supply virtually all of its PCB, backplane and enclosure needs internally? Will Sanmina continue to sell PCBs, backplanes and enclosures as separate items?

Randy Furr: Our intention is not to necessarily supply all bare boards, all backplanes and enclosures internally. In each of those areas, there are examples that do not make sense for us to internally source. We presently outsource very high-volume, low-technology boards, and the same goes for some of the enclosures and backplanes. We do in-source, though, by far the vast majority. I would estimate that we in-source approximately 80 to 85% of PCBs and backplanes. We probably in-source about 40% of our enclosures and outsource 60%. It is our goal where it does make sense - the higher end, lower to medium volume, high-complexity type work - to in-source. Again, where we get involved in the much larger volumes, lower technology, we'll continue to outsource in each of those areas.

We do offer all of our services on what Jure [Sola], our CEO, refers to as a la carte. I've been told we're somewhat unique in this area. In other words, if you just want to buy bare boards from Sanmina, we'll just sell you bare boards. Or you can just buy enclosures, cables or printed circuit board assemblies. We ship a large number of the products we manufacture to Solectron, Celestica, SCI and companies of that type. We buy a fair amount of products from those companies as well. We do not see that changing. If you have a requirement for one of these kinds of products we're good at doing, we want to be that supplier of choice. We don't care who you are. And that will not change. We in no way tie in any kind of requirement that we'll provide you with high-end boards only if you buy assembly services from us. We want our customers to be satisfied with their supply base overall. We certainly would prefer being that supplier, but it doesn't always work that way. We recognize that, and we just want to participate where we can and where it makes sense.

MMI: Do you ever anticipate in the future that the contract manufacturing customers that you cited would eventually see a conflict of interest in that their supplier is also a competitor in some cases and be less willing to buy from you?

Randy Furr: Well, we do have that situation. I guess there are six companies [including Sanmina] grouped together in the EMS sector as the larger companies, and all five of those [other] companies are customers of ours. I can give you one example where they view us pretty strongly as a competitor. I can give you another example where there's almost no talk of that. In fact, over the recent term we have increased market share with them as they were a fairly large customer of Hadco. We acquired Hadco, and that did not at all hinder or hurt the relationship. In fact, we've be able to expand it. Then maybe the other three guys are somewhere in between. So not everybody views us the same. It is important for me to say certainly we want to service all of our customers well.

Often, these other EMS companies need Sanmina to provide some high-end, more complex products going forward. We certainly have no intention of taking advantage of that need. We want to provide them with quality, delivery and competitive pricing they need to be successful as well. So I think that's kind of unique. I know some of the other companies out there offer similar services, and we've been told that they try to couple a lot of these services in with other services and package them together.

Often, if it's just bare boards, we're happy to participate at that level. If it doesn't make sense for us to do the systems, if a company is happy with one of our competitors doing those systems, then that's fine. We'll expend our energies elsewhere to try to win the account and maybe win it up front when it's first competitively bid.

MMI: In the current downturn, is Sanmina's vertical integration model an advantage or disadvantage?

Randy Furr: It can go both ways. I think if you break it down, the ability to pull in some additional business for our cable or our board or our enclosure operations is an advantage. So being a vertically integrated company can be an advantage. It can be an advantage because we're closely coupled together, and we can throttle the business up or throttle it down as necessary. We can probably react faster by being an internal operation than we could if this were all third party, arms length.

It certainly can be a disadvantage. In the circuit fabrication and enclosure businesses, the business model is a higher fixed, lower variable cost business. As a result, they are volume dependent. If you don't have enough volume, then obviously it will be tougher to maintain the level of profitability that we have achieved in the past. If you net all this out, we don't see it an overly significant disadvantage here.

We are clearly in a downturn here, a downturn unlike what any of us has experienced before, as rapidly as things have fallen off. We've been pretty quick to try to reduce cost all around our company. And we're going to continue to do that until we can see some end to this downturn. That includes reducing cost in the more vertically integrated operations that we have, specifically the boards, the cables and the enclosure end of the business. The important thing here is that we stay in close contact with our customers and, again, try to rightsize Sanmina to meet the near-term demand going forward.

From an overall point of view, we do believe that this thing will bottom out. And we do believe that there's tremendous upside to where we are today. The long-term demand for wireless technologies and certainly additional bandwidth, for which we think optical switch technology has tremendous growth potential, is very positive. We certainly want to maintain capacity to handle this business volume that we anticipate at some point later this year will certainly bottom out and start the other way.

MMI: As a result of the downturn, some top-tier players are taking the opportunity to restructure operations. Is Sanmina in that boat?

Randy Furr: I don't see huge restructuring today. Certainly on a constant basis, we rationalize our business and make sure each operation is needed. We do have 65 manufacturing sites in 13 countries. I don't want to rule out the possibility that a few, a very small number might be combined together. But we don't see any major restructuring going forward. We're still a profitable company. And certainly in the near term we expect to stay a profitable company going forward. We don't want to take any drastic measures at this point that are going to hurt our ability to grow.

MMI: What effect will the downturn have on the EMS industry? Will there be a further increase in consolidation, for example?

Randy Furr: I do think there will be a significant amount of industry consolidation. Some of us took advantage of great price-to-earnings multiples and strengthened our balance sheets for the long term. That puts us in pretty good position today, even with the downturn we're having. Sanmina, as a profitable company, is still well positioned today. I think a lot of companies in the industry who maybe were not in this "tier-one" category chose to grow by taking on debt. Today, that has put them in a very challenging position. Some of these companies were operating on razor-thin margins, even in good times, and buying the business, so to speak. With the downturn, now they're in trouble.

We have a corporate development department here that has never been as busy as they are today. They can't keep up with the phone calls that are coming in not only from the OEMs turning toward outsourcing and taking advantage of that opportunity, but also from these other companies in the industry that are clearly in trouble. They're in trouble because of their balance sheets, the amount of debt they have, and the challenge that it will be to turn a profit in this downturn.

How opportunistic we're going to be is the big question mark because you can't be like a kid in a candy store. With so many opportunities, you must choose the ones that make sense because you don't want to burn through the cash you have and then miss even greater opportunities in the future. Replenishing that cash will be much more difficult in today's environment than it was a year ago or nine months ago. So I think the next six months will be really interesting.

Several OEMs that are moving toward outsourcing have their packages out, and people are looking at them. Who does those deals and what they pay for those deals will be interesting because I think just an equal number of opportunities are going to come along behind them. So it'll be interesting to see who the real winners are in that area.

As far as the large guys being interested in the smaller companies, I think it will depend on what they add strategically because we don't need capacity today. We all have capacity. We have one opportunity that I can't discuss by name, but we were looking at a competitor that has gotten in trouble. We danced with them awhile and finally just decided we're better off to let this company, as sad as it sounds, not make it. That's because we stand to benefit more by picking up a customer base of a company that may not survive than by trying to acquire the company and do major surgery on it. So I think you're going to see a lot of that over the near term.

MMI: Do you want to add anything?

Randy Furr: There are two big issues out there. One is the inventory that's been built up in the pipeline. That's real. That ranges from the component manufacturers all the way through the service providers. The service providers have warehouses full of equipment that they ordered and don't have installed in the networks. It includes the OEMs; it includes the contract manufacturers.

My opinion is not necessarily shared by everyone, but I think the bigger factor is that service providers today really aren't spending any money. Their capital expenditures are significantly down, and we have to look at when that turns. Wall Street certainly isn't giving the industry the money that it did a year ago. The venture capitalists are not giving the industry the money that they did a year ago. So in addition to not spending any money, they don't have that much money to spend. This cycle could take six to nine months to get fully worked out. It will be a function of the service providers picking up the level of spending combined with us working through some of this inventory before we really see a clear upturn here.

Times may be tough, but the future, especially in the development of supply-chain networks, waits for no one. Much of the untapped potential for web-enabled networks revolves around collaboration (Jan., p. 4). For example, two vendors have recently introduced software that they believe will knit supply-chain partners together for collaboration. Neither company should be taken lightly because both have a growing list of EMS customers.

The first vendor, Datasweep (San Jose, CA), has a developed a Supply Chain Collaboration Portal that allows an OEM to track outsourced operations across multiple EMS sites of one or more providers from a single desktop view. In this scenario, the OEM's EMS providers would have to be Datasweep users. Is that too tall an order? Maybe not. Two out of the top three EMS providers and seven of the top 15 are Datasweep customers. Of course, the portal can also be used by a provider internally to obtain real-time manufacturing information on all of its plants worldwide.

According to Matt Holleran, Datasweep's VP of marketing and business development, the idea is to "give you one view of your plants around the world, make it personalized and make it active." This portal also helps you manage by exception, he adds.

Operations can be monitored from the global level all the way down to production line views within a specific plant. The portal triggers notifications by email, pager, and WAP phones and devices if performance indicators deviate from user-defined thresholds. Personalized views deliver production metrics tailored to the user's role within the company. Users can drill down on report parameters to isolate the cause of deteriorating trends in real time. In addition, the portal allows customers to view facility data integrated with data from other systems such as customer relationship management, product data management and ERP.

The Supply Chain Collaboration Portal is part of Advantage 4.0, the latest version of Datasweep's flagship product. Also new in this version are applications for RMA (return material authorization) and repair. These applications allow OEMs and their providers to capture all of the field defect, repair and upgrade information on individual units. As a result, users get traceability from cradle to grave. Four of the top 15 EMS providers are now using Datasweep for RMA and repair.

Starting price for the portal is $250,000, and the two applications for RMA and repair cost $20,000 each plus $4500 per concurrent user.

Another software vendor with a growing EMS client base is webplan (Newport Beach, CA). Like Datasweep, webplan has unveiled a new web service with the means to aggregate supply-chain partners for collaboration. This service, called eSupply-Chain.net, addresses one of the barriers to supply-chain collaboration - cost.

The new solution is aimed at companies that are put off by the price tag of webplan's high-end CeO product, which has an average selling price in the $900,000 range. As an alternative, the company is offering eSupply-Chain.net on a hosted basis for a monthly subscription fee of $10,000 to $30,000, depending on the level of services.

To keep the cost down, webplan has made eSupply-Chain.net less customizeable. But the new service still offers supply-chain visibility, analysis and trading partner collaboration. With eSupply-Chain.net, a provider can build one-to-many private trading networks. A company can be up and running with a trading network in 10 to 20 days, according to webplan. Its new service bridges the gap between existing ERP systems and the supply chain by pulling information out of these systems. Through this service, individual EMS subscribers can also be connected to CeO users in a many-to-many EMS network.

"We are not attempting to establish an industry-specific exchange. However, based on our existing dominance of the EMS space, we feel this will be a probable outcome with the introduction of eSupply-Chain.net," says Darryl Praill, webplan's VP of mar-keting.

EMS customers include EFTC, Jabil Circuit, MCMS, SCI Systems, SMTC and Viasystems Group.

In addition, webplan has introduced PLM Insight for product life cycle management. This product will assess the impact of a design change and allow the customer to determine the right time to make the change based on such factors as existing inventory levels and component availability.

Simclar International Ltd., a contract manufacturer based in Dunfermline, Scotland, has entered into an agreement to buy 71.3% ownership of Techdyne (Hialeah, FL), a CM that also does cable and harness assembly. The privately held Scottish company, which has small facility in Kenosha, WI, will gain a much larger presence in the US. Techdyne will add four US plants - Round Rock, TX; Milford, MA; Hialeah, FL; and Dayton, OH - plus a facility in Livingston, Scotland.

Simclar is buying this controlling interest from Medicore (Hialeah, FL) for $10 million and an earn-out of 3% of sales for three years. The earn-out has a floor of $2.5 million and a ceiling of $5 million.

For 2000, publicly held Techdyne earned net income of $565,000 on sales of $52.8 million, compared with net income of $303,000 and sales of $48.4 million in 1999. Techdyne employs about 440 people in a total of about 160,000 ft2. The CM is also affiliated with a Chinese company. Simclar, in comparison, has a work force of 800 and manufacturing capacity of 250,000 ft2. In Scotland, the company operates a vertically integrated facility.

"The alliance of Techdyne and Simclar will create a partnership that will allow both companies to have the critical mass needed to be recognized as a mid-tier contract electronic manufacturer," states Barry Pardon, president of Techdyne.

Techdyne serves the data processing, telecom, instrumentation and food preparation industries. Simclar's customers are involved in telecom, including base stations; medical equipment; rapid transit; peripherals; and datacom.

With a history in cable and harness assembly, Techdyne expanded its EMS business in 1997 by acquiring Lytton, a CM in Dayton, OH. "Now the majority of our business, over 50%, is either board or higher level assemblies. Cable and harness [assembly] is about 40%," says Pardon, who will stay on Techdyne's president.

He points out that the parties started discussions nine months ago so the downturn had nothing to do with this deal.

Medicore plans to use the proceeds to expand its medical supply and dialysis operations and to repurchase stock.

PartnerTech (Malmö, Sweden) has acquired a group of two contract manufacturing companies: EQ Elektroniq AB in Sweden and Baltic Microwave SP. Z.O.O. in Poland. Two sites in Poland - Gdynia and Sieradz - account for 80% of the group's production, while the remaining 20% is done in Spånga, Sweden. Employing 130 people, the group reports annual sales of more than SEK 150 million. The Swedish-Polish group produces cabling and prototypes and assembles finished products, primarily for the telecom industry.

"The acquisition reinforces our competence and supplements our resources, particularly in the area of radio frequency. It is very important for us to be able to start competitive production in Poland in this way," states Mikael Jonson, PartnerTech's CEO.

He adds that the deal will strengthen PartnerTech not only in manufacturing, but also as a design partner.

In addition, the acquisition is part of the CM's greater focus on internationalization. PartnerTech started an operation in Atlanta last year and is looking at other countries as well.

For the year 2000, PartnerTech was ranked as an MMI Top 50 EMS provider.

Oneida Nation Electronics (ONE), a contract manufacturer in Green Bay, WI, is looking for partner either to make a strategic investment in the company or to acquire it. The CM operates a facility of about 114,000 ft2.

"It's an underutilized facility with a good core base of business," says Tony Otten, CFO at ONE. The facility serves both Fortune 50 and smaller local customers.

ONE is owned by the Oneida Nation, a Native American tribe with gaming interests. The tribe went into contract manufacturing as a way to diversify. The Green Bay facility was built and equipped by the Oneida Nation, which then leased it to Plexus (Neenah, WI) in 1997. This affiliation with Plexus ended a little over a year ago, and the tribe has decided not to continue operating the EMS business on their own.

"I think they recognize they don't have the industry knowledge that is really necessary for a business to be highly successful within this industry. And I think they recognize the best way to make this a success is to find a strategic partner," says Otten.

According to Otten, ONE would entertain a financial buyer, but "I think the most logical fit would be within the industry."

He says the current downturn was not a factor in the decision to put the business up for sale.

Trident Systems International (Newport Beach, CA), a pubic company, has purchased Futronix, a CM in Homosassa, FL, from Salient Cybertech (Sarasota, FL), an Internet company. With a 35,000-ft2 facility, Futronix serves customers that include Peek Traffic, Tritheim Technologies, Amazing Smart Card Technologies and Axxon Corp.

Salient received 400,000 restricted shares of Trident and had to infuse Futronix with $600,000 before getting a series of cash payments totaling $425,000, according to an SEC filing. The transaction was valued at $8 million. Salient acquired Futronix last year.

New programs...Despite the current gloom and doom, Omni Industries (Singapore) says its outlook for the second half appears to be strong, with new and existing customers increasing their commitments. The provider has identified two new programs. Hewlett-Packard is expected to ramp a new program for servers and workstations in the second half of the year. Omni will also begin PCBA for instrumentation products from Agilent Technologies. The provider says it should also continue to benefit from the rising trend of outsourcing to Asia. Unless economic conditions worsen even more, Omni is forecasting revenue growth of more than 35% for 2001 with profit margins broadly in line with those in 2000....Agilent has also outsourced production of its 3070 in-circuit automated test system to the Singapore operation of Benchmark Electronics (Angleton, TX). Complete transfer of 3070 assembly from Colorado to Singapore is scheduled for completion this year....Solectron (Milpitas, CA) will manufacture broadband wireless access systems for Wi-LAN (Calgary, Canada)....Elcoteq Network (Espoo, Finland) has landed a multiyear contract from Cellport Systems (Boulder, CO) for the manufacture of a universal, hands-free system for mobile phones. Elcoteq's Monterrey, Mexico facility will serve as sole source for the system....Japan's Kyushu Matsushita Electric Co. is using Cal-Comp Electronics (Thailand) to produce cordless phones for KME. Cal-Comp, whose stock recently began trading on the Stock Exchange of Thailand, operates five plants in Thailand with 193,600 m2 and about 6000 employees and is planning to add a sixth plant. Taiwan's Kinpo Group holds 67.6% of Cal-Comp....DNA Enterprises has selected XeTel's new full-service Technology Center in Dallas, TX, as DNA's manufacturing partner. XeTel (Austin, TX) recently moved its Dallas operation a larger 50,000-ft2 facility, where the CM has added design, prototyping, test and preproduction services....PartnerTech and Sweden's Gyros AB have signed a several-year agreement for development and manufacturing of a new research tool for the pharmaceutical industry. Established last year, Gyros provides a platform that permits laboratory processes to be miniaturized and integrated on customized CDs. PartnerTech says this is its second big medical equipment win in a short period....Advanced Business Sciences (Omaha, NE) has selected Electronics Manufacturing Technology, a division of Ledvision Holdings (Ackley, IA), to manufacture a product used to track people on probation and parole....Sparton Corp. (Jackson, MI) has been awarded U.S. Navy contracts totaling $20.6 million for the design or manufacture of various sonobuoys plus a $900,000 production contract for a signaling device....Teledyne OptoElectronics (Los Angeles, CA), a unit of Teledyne Technologies, has received a $3.6-million order for prototypes and initial production quantities of OC-192 optical receivers. The order came from an unnamed fiberoptic components OEM....Test Technology, Inc. (Marlton, NJ) has won a manufacturing and repair contract from Shared Technologies Fairchild, a division of Intermedia Communications. The contract covers the division's Lexar PBX product line....Bonso Electronics International (Hong Kong) has received about $6-million worth of orders to produce over 500,000 units of walkie-talkies for TriSquare Communications (Hong Kong). Known as a producer of electronic scales, Bonso is promoting its EMS capabilities, which rely on manufacturing in China....National Manufacturing Technologies (Carlsbad, CA), a vertically integrated CM, is supplying Pioneer Magnetics, a new customer in the power supply industry, with board assemblies, machined parts and enclosures.

More outsourcing...Novatel Wireless (San Diego, CA), a supplier of wireless data modems and software, will move certain order fulfillment and other manufacturing-related activities to its contract manufacturers. The company is restructuring.

South Korea may not spring to mind as a contract manufacturing option, but at least one Korean company has started selling EMS in the US. Korea Computer (Seoul, South Korea) is now using its US subsidiary, Pacom International in Chatsworth, CA, to sell the services of the parent's EMS division. Pacom has added to its original mission of marketing Korea Computer's LCD monitors in the US.

Surprisingly, the Korean company has been contract manufacturing since 1974. This work takes place at a complex located in Kumi, south of Seoul. EMS programs have involved products such as LAN networking systems and ATM machines.

New names...Flextronics (Singapore) has dropped the word International from its name. The company says the old name was a holdover from the days when it was only in Asia....NatSteel Electronics Ltd. (Singapore), acquired this year by Solectron, has been renamed Solectron Technology Singapore Pte Ltd....Publicly held Chase Corp. (Bridgewater, MA) has put its EMS operations under a new banner, Chase EMS Group. The group consists of Sunburst (West Bridgewater, MA), a full-service CM focusing on Southern New England; NETCO Automation (Haverhill, MA), a prototyping and advanced technology house; and RWA (Melrose, MA), a CM targeting northern New England....Allied Components International Ltd. (Singapore), whose businesses include contract manufacturing, has changed its name to Flairis Technology Corp. Ltd.

New facilities...SMTC (Toronto, Canada) has started operations in a new 150,000-ft2 facility in Franklin, MA, along the Route 495 technology belt. The facility will offer services from concept and design through PCBA and fully integrated and tested enclosures....In Shanghai, China, Viasystems Group (St. Louis, MO) has opened a 150,000-ft2 plant as a full systems integration center (Aug. '00, p. 8-9). Capabilities include backplane and SMT assembly, metal fabrication, enclosure assembly and full subsystem and system integration....CTS Interconnect Systems, a unit of CTS Corp. (Elkhart, IN), has opened an 83,000-ft2 facility in Londonderry, NH, to supply custom backpanels and high-end systems integration to a growing customer base in North America. The new facility allows CTS to offer complete life cycle management including direct order fulfillment. The CTS Interconnect business launched its North American operation with a 20,000-ft2 facility in Hudson, NH, in late 1997. In addition to the new facility, CTS Interconnect Systems has operations in Glasgow, Scotland, its headquarters, and Tianjin, China....Jabil Technology Services, a division of Jabil Circuit (St. Petersburg, FL), has expanded a design center in the parent company's manufacturing facility located in Auburn Hills, MI. The newly expanded center includes a design laboratory and a specialized vehicle laboratory. Jabil's Auburn Hills site is geared for the automotive industry....Kimball Electronics Group (Jasper, IN), a unit of publicly held Kimball International, has opened a 40,000-ft2 microelectronics facility in Valencia, CA....Qtron (San Diego, CA) expects to have its new 200,000-ft2 complex in Poway, CA, ready for occupancy on June 1 (Nov. '00, p. 5). The CM will keep one 35,000-ft2 building at its current site....Cirtronics has relocated to 65,000-ft2 in the Milford Technology Center office park in Milford, NH. The new location increases the CM's space by 50% to support continued growth. Privately held Cirtronics projects that sales should exceed $22 million for its current fiscal year....CTI Technology (Springfield, MA) has expanded its recently acquired facility in Rosarito, Mexico, from 29,000 ft2 to 58,000 ft2 (Aug. '00, p. 7-8)....PEMSTAR (Rochester, MN) has opened an engineering office in Austin, TX. This office will support US-based customers on the process and test equipment side of PEMSTAR's outsourcing business and will form the basis for an NPI center, known as a ProCenter at PEMSTAR....Litton Interconnect Technologies, a supplier of custom backplanes and electromechanical subassemblies, is preparing to open a 60,000-ft2 facility in Fairfield, CA. Scheduled to open in May, this plant allows Interconnect Technologies to expand assembly operations into Northern California. Also, the Litton unit will undertake a $30-million expansion of its PCB operations in Springfield, MO, its home base. The project will nearly double these operations, which currently occupy a 225,000-ft2 plant. A new facility will be operational 15 months from the start of construction. Interconnect Technologies is a division of Litton Industries, now a subsidiary of Northrop Grumman.

Telecom standard emerging...For CMs serving the telecom industry, the bar has been raised for facility certification. A relatively new standard called Telecommunications Leadership 9000, or TL 9000, has been designed for quality assurance of telecom products. Reportedly, the standard is based on ISO 9000, but adds 83 requirements. Included in TL 9000 are performance-based metrics that measure the reliability and quality performance of products. Recently, the Corinth, MS facility of ACT Manufacturing (Hudson, MA) received certification to TL 9000. But Sanmina (San Jose, CA) lays claim to being the first CM to achieve TL 9000 registration. In November 2000, Sanmina's Toronto Enclosure Systems Division was certified to the telecom standard.

Plexus (Neenah, WI) has promoted six senior officers starting at the top. John Nussbaum, president and COO, will take over as CEO. He will retain the position of president. Peter Strandwitz will step down as CEO, but will continue as chairman of the board.

Moving into the COO position is Dean Foate, who has been executive VP of Plexus and president of Plexus' Technology Group. The company also promoted Tom Sabol, senior VP and CFO, to executive VP. He will continue his duties as CFO.

In addition, J. Robert Kronser, VP of sales and marketing, will become executive VP and chief technology and strategy officer. Michael Verstegen will go from executive VP of the Technology Group to president of the group. Steven diLoreto will be promoted to president of NPI Plus, Plexus' unit for new product introduction. He is stepping up from the position of VP of operations for the unit.

People on the move...Toshiaki Ogi, a 35-year veteran of Toshiba Corp., has joined Nam Tai Electronics (Hong Kong) as CEO. He is taking over duties from Shigeru Takizawa, current president and CEO. Takizawa is being promoted to chairman. Nam Tai has also appointed Joseph Li president. Li came to Nam Tai with its acquisition of the JIC Group, which he has led as chairman and managing director....SCI Systems (Huntsville, AL) has added two directors to its board: Shirley Jackson, Ph.D., president of Rensselaer Polytechnic Institute, and David Jones, chairman and CEO of Rayovac....Jabil Circuit has promoted David Couch to GM for Florida manufacturing operations at its headquarters in St. Petersburg. In his prior job, Couch was a business unit manager at the company's Auburn Hills, MI site. Within Jabil's new Technology Services division, the CM has filled several new positions. Israel Morejon has become director of design services; Jim Zboralski has assumed the role of director of advanced manufacturing technology; and Larry Church has taken on the job of director of sales and marketing. Church will be responsible for the division's IT infrastructure and Jabil's configurations management group....Manufacturers' Services Ltd. (Concord, MA) has promoted Tony Boyle to president of European operations. He was VP of Irish operations, a business that has expanded over the past five years under Boyle. Also, MSL has hired Richard Buckingham as VP and treasurer. His experience includes serving as VP of financial services and treasurer at Wang Global. Finally, Curt Wozniak, chairman and CEO of Electroglas, has joined MSL's board....Sanmina has named Michael Donner as corporate VP of marketing. At one time, Donner was corporate director of communications for Solectron, which he left for a position in the dot-com world....MCMS (San Jose, CA) has promoted Richard Latta to VP of technology. He had been director of engineering....Kenneth Pastewka has joined Viasystems Group as VP of global supply chain management. His more than 20 years of experience in global materials management includes serving as VP of purchasing for B/E Aerospace....William Anderson has rejoined IEC Electronics (Newark, NY) as VP of materials and supply chain management. In his previous stint with IEC from 1995 to 1999, Anderson held the positions of VP of materials and executive VP and GM. Most recently, he served as VP of materials and supply chain management at MCMS.

More management changes...Jeffrey Goettman, managing director at Thayer Capital Partners (Washington, DC), was recently elected chairman of the board at EFTC (Phoenix, AZ). In partnership with BLUM Capital Partners, Thayer acquired K*TEC Electronics (Sugar Land, TX) as well as controlling interest in EFTC. A proposal to merge the two CMs has been announced (Mar., p. 8). Goettman replaces former chairman Jack Calderon, who has joined Lincoln Partners (Chicago, IL), an investment bank. Also, EFTC has appointed James Van Horne from Stanford University's Graduate School of Business to the company's board....Sparton Corp. (Jackson, MI) has promoted Douglas Johnson from VP and GM of Sparton Electronics Division to COO. Recently additions to the company's board are David Molfenter, a former Raytheon VP and GM, and Richard Langley, Sparton's CFO. Molfenter's election fills the vacancy created by the death of John Smith, chairman emeritus. Smith had also served on the board of Cybernet Systems (Ann Arbor, MI), in which Sparton has invested to allow collaboration with Cybernet on projects with extensive design and software requirements, beyond Sparton's internal capabilities. David Hockenbrocht, Sparton's president and CEO, has taken Smith's place on Cybernet's board....CTI Technology (Springfield, MA) has promoted Robert Egan to president and COO. Formerly CTI's VP of business development, Egan joined CTI in April 2000 from ACT Manufacturing, where he was VP of business development. Taking over Egan's sales duties at CTI is Walter Grischuk, who has moved up to VP of sales and marketing. Grischuk joined CTI in October 2000 as director of business development for the Northeast region. Also, Victor Servello has been appointed executive VP and CFO at CTI. Servello was VP of operations and COO. George Davies remains CTI's chairman and CEO....FLASH Electronics (Fremont, CA) has hired Curtis Campbell as VP of worldwide sales. Before joining Flash, Campbell served two years as VP of sales for another CM, ISIS Surface Mounting of San Jose, CA. His experience also includes ten years at Avnet. In addition, Flash has appointed David Pellone as VP of finance, a new position in which he will serve as CFO. Prior to joining Flash, Pellone was VP of finance and CFO at RAE Systems and before that, Dual Systems. Both are Silicon Valley companies.

Still more people in motion...SMTC (Toronto, Canada) has hired Bruce Mann as VP of investor relations and corporate communications. Previously, he worked as VP of investor relations at MetroNet Communications, now AT&T Canada....Mark Hancock has joined XeTel (Austin, TX) as GM of its recently expanded Dallas facility. Most recently, Hancock served as senior director of manufacturing in Houston for Telxon Corp., a supplier of hand-held computers and wireless network products....Epson Portland Inc. (EPI - Hillsboro, OR), the US manufacturing affiliate of Japan's Seiko Epson Corp., has promoted Al Fella to director of purchasing/production control and Jim Sloan to director of sales and marketing. Contract manufacturing is one of EPI's activities....DDi Corp. (Anaheim, CA) a provider of interconnect services including backplanes, has named a new management team for its value-added business. Ed Johnson was appointed president of Value Added Operations. He formerly served as president of Hi-Tech Manufacturing, a CM that merged with SMTC, as well as president of SMTC. Joining Johnson on the division's management team are Brad Tesch, VP of operations, and Jim Laurion, VP of materials management and corporate development. The new team brings more than 50 years of combined experience to DDi's Value Added Operations, based in Dallas, TX, with three additional facilities in the US and England....Group Technologies (Tampa, FL) has hired David Monaco as VP of finance. He assumes financial duties from James Cocke, now president and CEO of Group-Tech. Monaco is a 21-year veteran of Motorola, where he most recently served as director of financial systems for the Fixed Wireless and Core Network Groups....UMM Electronics (Indianapolis, IN), a medical CM and member of the Leach Technology Group, has appointed Paul Mulqueen, Ph.D., director of new product development.

New structure...In a reorganization of business operations, Finland's Elcoteq has divided its activities into three areas, each under a group VP. The CM named group VP Christer Härkönen as head of Terminal Products, group VP Jouni Hartikainen as head of Communications Network Equipment, and group VP Jukka Jäämaa as head of Industrial Electronics.