![]()

Cover story

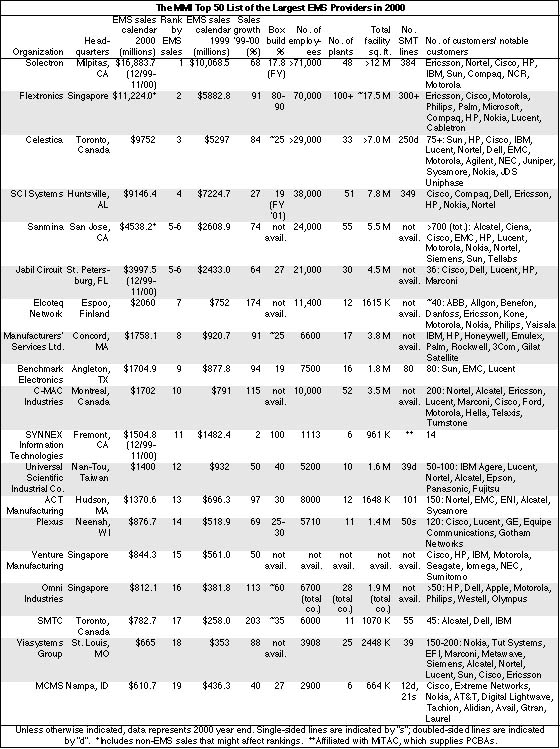

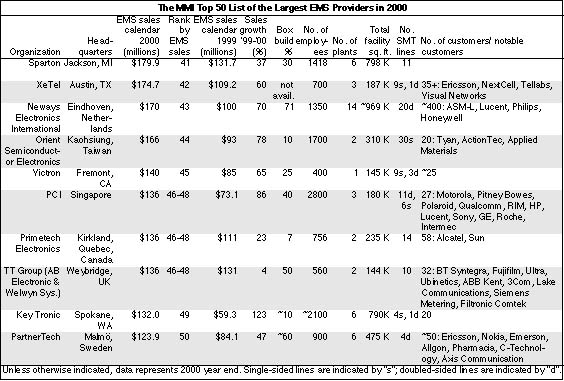

The MMI Top Rankings (three tables)

2001 Trend

Mid-Tier Players Take Global Stance

News

Although OEM demand has rapidly gone sour in recent weeks, last year was about as sweet as it gets for the EMS industry. Sales of the MMI Top 50 EMS providers in 2000 totaled an astounding $79.8 billion. That's greater than the size of the entire 1999 market for EMS. What's more, the Top 50 grew at a clip that by far surpasses any growth rate MMI has ever compiled for the largest CMs going back to 1992. In 2000, Top 50 providers combined for a growth rate of 67.6%, which may also stand as a record for years to come.

Now accounting for the bulk of EMS market sales, the MMI Top 50 pushed market size and growth well above levels forecasted for 2000. Based on Top 50 sales, MMI estimates that the 2000 EMS market actually measured between $112 billion and $115 billion. That means the market expanded by somewhere between 44% and 47% last year.

Leading the way on the growth parade were the top-ten providers, which together grew at a scintillating 70.3%. Top-ten sales amounted to $62.8 billion. Non-EMS sales of such items as PCBs and enclosures are mixed in with that total. Top-ten providers, particularly Flextronics and Sanmina, do not break out non-EMS sales. Even excluding non-EMS sales of maybe $2 to $3 billion, one can conclude that the top ten accounted for over half the EMS market in 2000. In 2000, it took sales of $1.7 billion to make the top ten, compared with $923 million the year before.

In 2000, Solectron solidified its position as number one in EMS sales. The company took over the top spot in 1999. Flextronics moved up to number two as long as its non-EMS sales came to less than about $1.47 billion. Celestica maintained its number-three position, while SCI Systems dropped to number four. At this point, however, it is unclear as to who owns the next two spots. Sanmina is fifth largest by total sales, but that figure includes some amount of non-EMS sales of PCBs. If the non-EMS portion was greater than $540 million, then the number-five slot belongs to Jabil Circuit. See tables below.

To be ranked in the MMI Top 50 for 2000, an EMS provider needed at least $123.9 million in sales. This minimum was largely unchanged from the 1999 figure of $120 million. Why was this the case when market growth was so high in 2000? The answer lies in why companies are deleted from and added to the Top 50.

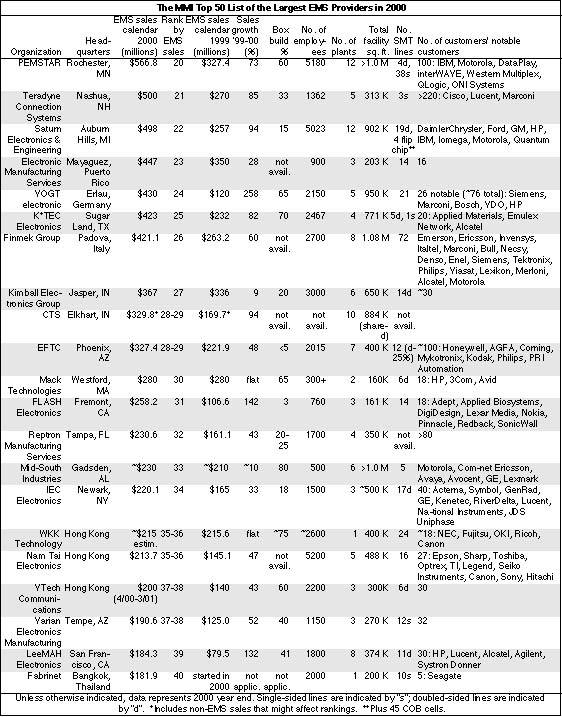

A total of 14 companies in the 1999 Top 50 disappeared from the 2000 list. Eight EMS providers were acquired - up from five the year before. Five companies did not respond, including one in Chapter 11 (see News, end). One company came off the list because sales declined after selling a business. MMI managed to replace all 14. All but two of the new members were added to the bottom 20, which effectively kept the minimum at status quo. So despite a significant loss of 1999 Top 50 providers, industry growth enabled MMI to find other companies that would qualify.

Of the new listees, seven are based outside of North America. From Asia, MMI added Fabrinet, which started in 2000 (Jan. '00, p. 9-10); Orient Semiconductor Electronics (OSE), whose Finished Products Group performs contract manufacturing; PCI, a CM publicly traded in Singapore; and VTech Communications, an OEM organization with a Contract Manufacturing Services division. Three Europe-based CMs made the Top 50 for the first time. They are Neways Electronics International, PartnerTech and VOGT electronic.

Six US-based providers and one Canadian CM also joined the Top 50 in 2000. US additions consist of CTS, FLASH Electronics, Key Tronic, LeeMAH Electronics, Victron and XeTel. From Canada comes Primetech Electronics.

However, not all the additions are appearing for the first time. OSE, PCI, Victron and XeTel have been included on past lists.

Top 50 data allow one to calculate several benchmark ratios. Based on data from 47 providers, revenue per employee averaged $205,700, while revenue per ft2 worked out to $870. Both averages were up from 1999 ratios of $188,100 per employee and $789 per ft2. The 1999 ratios were calculated from somewhat different sets of companies. But given the weighting of the top-ten providers, these increases are probably meaningful, indicating that CMs were squeezing more out their plants.

Among 47 providers that supplied the necessary data, revenue per plant averaged $121.5 million. In 1999, the ratio was $94.9 million.

Methodology. Companies whose businesses are based on enclosure manufacturing were not considered for the Top 50. Nor were suppliers who are mainly engaged in original design manufacturing. These distinctions follow MMI's past practice.

In some cases, sales of backplanes are included as part of EMS revenue. This is a gray area. Some might argue that as passive interconnects backplanes belong with PCBs, cables and harnesses. Nevertheless, a backplane is an assembly containing pins and connectors and increasingly, SMDs.

Sales figures supplied in foreign currencies were converted to US dollars by using average annual exchange rates from the Federal Reserve Bank of New York.

In all cases, companies were asked to exclude non-EMS sales for the purpose of ranking according to EMS sales. As more and more CMs pursue some form of vertical integration, non-EMS sales creep into their revenue through acquisitions of suppliers such as PCB fabricators or enclosure manufacturers. These CMs typically do not break out non-EMS sales. MMI has footnoted cases where non-EMS sales might affect the rankings.

A few years ago, OEMs with global manufacturing needs had two choices: offshore providers or a top-tier CM. Today, OEMs that can't or won't do business with the top tier want other options for global manufacturing. This opportunity has not been lost on the industry's mid-tier players. A growing number of them are following the big boys into regions within Asia and Europe (Jan., Outlook article).

Asia is especially attractive today for expansion. It offers both low-cost manufacturing and materials for OEMs seeking to preserve margins during the current slowdown. The region also holds the keys to the Japanese market.

Although Solectron has acquired a Sony operation in Japan and several other top-tier players have recently set up offices there (Feb., Japan article), they do not have the Japanese market to themselves. At least one mid-tier CM, PEMSTAR, has opened an engineering office in Japan. The new office, located in Yokohama, is initially focusing on engineering support for the process and test equipment side of PEMSTAR's outsourcing business. Unlike the typical CM, PEMSTAR can design and build equipment to automate the assembly of technologies such as optical components.

According to the PEMSTAR, it established the new office to respond to increasing demand from its customer base in Japan and to support customers outsourcing complex capital equipment. The manufacture of this equipment will take place in PEMSTAR's newly expanded Singapore facility.

In addition, the company plans to use this office as an NPI (new product introduction) center for EMS opportunities in Japan. In this capacity, the office will release products to PEMSTAR's low-cost Asian facilities. For low-cost Asian production, the company already operates in Thailand and China.

A second mid-tier player, MCMS, is also expanding in Asia. The provider will be opening a new operation of about 20,000 ft2 in Xiamen, China, within the next three to six months. The operation will provide board-level assembly services, with initial capacity already allocated to an existing customer. YJ Lim, MCMS' VP of Asian operations, will oversee this facility as well as the CM's existing facility in Penang, Malaysia.

Yet another mid-tier CM, SMTC, also has designs on Asia. The company plans to establish a presence in Asia some time this year.

Spurred by a rapid slowdown in demand, three top-tier players are restructuring operations, not only to cut costs, but also to prepare for future growth.

Flextronics (Singapore) and SCI Systems (Huntsville, AL) have said they will be closing an unspecified number of plants. Solectron (Milpitas, CA) has announced a one-year effort that will include consolidation of facilities that are not optimally located.

At Solectron, restructuring is taking place in two phases. In the first, Solectron is cutting manpower at various locations in response to a demand downturn primarily in the Americas. The company is also consolidating newly acquired NatSteel Electronics sites in Guadalajara, Mexico, and Budapest, Hungary, into Solectron sites. As a result, Solectron expects to cut its work force by about 8200. This reduction represents about 10% of the company's total employment of 79,000 at the end of its fiscal Q2.

"The second phase, designed to provide a forward-looking value proposition, will involve structural changes including a further consolidation of facilities that are not optimally located. Other facilities located in relatively high-cost regions will undergo mission changes from volume production to NPI sites with complex mix," said Susan Wang, Solectron senior VP and CFO, in a conference call with analysts. The idea is to continue to support fast time-to-market requirements, as volume production migrates to lower-cost facilities.

She reported Solectron is preparing to shift most of its business to regions with cost and logistics advantages and access to large regional markets.

Solectron expects to record a charge of $300 to $400 million in its fiscal Q3 to cover this restructuring program, which will last 12 months. The charge is greater than what Flextronics or SCI is planning.

According to Wang, Solectron had foreseen the need for a two- or three-year restructuring program in its long-range planning. Current market conditions caused the company to speed up efforts.

For Solectron's fiscal Q3, the company now expects a net loss of 4.25% to 5.55% of sales.

Flextronics has decided to close or downsize some facilities located primarily in higher cost regions of the world. Michael Marks, Flextronics chairman and CEO, told analysts that its enclosures business is the key area for these cuts. "When we acquired that business, it had quite a few locations," said Marks during the conference call. He explained that the company is moving away from stand-alone regional facilities in favor of industrial parks as well as larger centers, such as San Jose and Dallas.

"Part of this is a normal transition that we've been planning for that business, and the second portion of it is just more capacity than it looks like the telecom industry is going to use for some time to come," said Marks. As a result, Flextronics will cut a number of enclosure facilities in the higher cost areas.

The enclosures business is "the area that has the most overcapacity in our company because it has primarily served the telecom business. But we are taking the opportunity to make some cuts in other parts of the business as well," said Marks. The only cuts being made are in areas where Flextronics wants to reduce capacity permanently.

The company expects to take a restructuring charge of less than $100 million in the March quarter.

At the same time, Flextronics must prepare for new business such as the mobile phone operations outsourced by Ericsson (Feb., p. 7-8). "In my business career, I've been in downturns before, but never a downturn this severe where the upside is so visible," Marks commented. "We're in this unusual circumstance of cutting costs, which we would normally do in a downturn, while being prepared to take on billions of dollars of new business."

Despite making cuts in high-cost regions, Flextronics continues to expand operations in Dallas and New England. A number of expansions are also underway in low-cost locations.

Like Flextronics, SCI will also close some plants while expanding others. These moves, says SCI, are in response to current market conditions, reduced growth of PC activities, a rapid shift toward communications and enterprise computing business, as well as growth in the company's foreign operations. As a result, SCI expects to reduce its work force of 38,000 by about 10%. This realignment will cause the company to take a one-time charge this quarter in the range of $40 to $60 million.

"The program announced today is not expected to diminish top-line performance and should improve SCI's operating margins in future periods," stated Gene Sapp, SCI's chairman and CEO.

SCI has several plant expansions underway or under consideration timed to provide new capacity as the current softness abates and new customer requirements materialize. The company's objective is to optimize its footprint and capacity distribution for its shifting business mix and future growth opportunities.

Nokia has just provided one of those opportunities. SCI will acquire Nokia Networks' manufacturing operations in Haukipudas, Finland, and Camberley, UK. In Haukipudas, SCI will manufacture narrowband access products and later on units for 3G base stations. In Camberley, the provider will produce transceiver/receiver units for 2G base stations. This acquisition includes related engineering in both locations, and SCI will establish an Engineering Services unit to support Nokia and other customers. A multiyear supply agreement calls for SCI to provide development, manufacturing and sustaining-engineering at both facilities.

About 1250 Nokia employees will transfer to SCI. Subject to regulatory approvals, the transaction is expected to close before the end of Q2.

This deal expands the relationship between the two companies. In 1998, SCI acquired Nokia facilities in Oulu, Finland, and Motala, Sweden, and last year began building Nokia 2G base stations in Perth, Australia (Sept. '00, p. 7).

Nokia says the deal gives it more flexibility and is a natural step in its networked manufacturing strategy.

In January, SCI lowered guidance for the remainder of its fiscal year, which ends in June 2001.

While these top-tier players offer highly visible examples of capacity rationalization, they are not alone. XeTel (Austin, TX) plans to close its San Ramon, CA facility, an operation employing less than 40 people. The company expects to retain nearly all of the facility's customers and will begin to shift production to the CM's Austin, TX plant immediately.

Acquired from SBE in 1996, the San Ramon plant is the smallest of XeTel's three facilities and contributes less than 8% of trailing 12-month revenues.

Increased costs as well as low-volume production led to a less than optimal utilization of assets and resources at the San Ramon facility. "The need to continue to improve our capital asset and critical resource utilization lead us to take this path. In the long term, asset utilization should increase and, as a result, the company will realize continued improvements in gross margin and income as we start the new fiscal year in April," stated Angelo DeCaro, XeTel's president and CEO.

All equipment and other assets will be relocated to the Austin and Dallas facilities to handle increased demand at those locations.

Avaya Inc. (Basking Ridge, NJ), a Lucent spin-off, has decided to outsource most of its manufacturing to Celestica (Toronto, Canada) under a supply agreement worth about $4 billion over five years. As part of this deal, Celestica will acquire Avaya's operation that manufactures large business systems in Westminster, CO, and its repair and distribution activities in Little Rock, AR. In addition, Avaya will phase out manufacturing in Shreveport, LA, and the small business systems produced there will be moved to Celestica facilities.

Celestica will pay about $200 million for the two operations and certain other assets. The price is in a range from 1.5 to less than two times book value, depending on the amount of working capital. Using an earnings valuation, Celestica reports that this price represents an enterprise value of less than six times EBITDA on a one-year forward basis. Subject to union ratification and other conditions, the deal is expected to close in phases throughout Q2 and Q3.

About 1400 Avaya employees, including over 100 engineers, are expected to join Celestica. Of that total, about 1055 people work in Westminster within the Denver area, where Celestica will be taking over a facility of more than 400,000 ft2. The Little Rock facility is even larger at nearly 800,000 ft2, but Celestica plans to utilize around 250,000 ft2 of that space. Celestica will add about 320 people from Little Rock.

This deal makes Celestica Avaya's primary EMS provider for PCB and systems assembly and test, repair and supply chain management for a range of products. They include enterprise communications servers, interactive voice response systems, voice messaging consoles, wireless infrastructure, IP telephony products and call management systems.

In Avaya, Celestica gains a new customer, which will become a top-10 account, according to a Bloomberg interview with Eugene Polistuk, Celestica's chairman and CEO. During a conference call, the company provided a preliminary estimate of about $300 million in revenue from Avaya this year and probably $700 to $800 million next year.

Polistuk told analysts that the transaction is "strategic from the point of view of continuing to grow our communications base and increasing our diversification."

Once the agreement is fully implemented at the end of Avaya's fiscal 2002, the company expects to save about $400 million over the remaining term of the contract.

Both Avaya sites are unionized, and Celestica has worked out a five-year arrangement for the union labor. The company believes this arrangement will work well based on its experience with other unionized operations it has around the world. Still, union ratification must be obtained for the deal to go through.

"While this is one example of the new outsourcing opportunities for Celestica, we continue to see a significant pipeline for acquisitions to complement our solid organic growth opportunities with new and existing customers," remarked Polistuk in the conference call.

New alliance...Intrinsix Corp. (Westborough, MA), an ASIC and system design house, has teamed up with Sanmina (San Jose, CA) to provide design and manufacturing services. The two are supporting Midas Vision (Wrentham, MA), a supplier of automated optical inspection modules.

Fisher-Rosemount Systems, the process management division of Emerson, intends to sell the division's board manufacturing operation in Leicester, England, to ACT Manufacturing (Hudson, MA).

ACT and Fisher-Rosemount have signed an agreement in principle, whereby ACT will establish for Fisher-Rosemount a global, "straight-through" manufacturing process, from PCBA through final assembly.

Emerson, which has been an ACT customer for ten years, will become a top-five account for ACT when the transaction is completed. Subject to a definitive agreement, the deal is expected to be finalized over the first two quarters of 2001.

Fisher-Rosemount supplies such products as control valves, regulators, transmitters, analyzers and process management systems.

Deals done...Last month, Solectron (Milpitas, CA) completed the acquisition of Sony's facility in Kaohsiung, Taiwan (Oct. '00, p. 5-6). The facility adds 130,000 ft2 of capacity....Also in February, Celestica closed on its purchase of Motorola manufacturing assets in Dublin, Ireland, and Mt. Pleasant, IA (Dec. '00, p. 7).

New programs...Flextronics has won programs for printers and consumer electronics from Epson and Toshiba respectively. Manufacturing will take place in Central Europe. In addition, Flextronics has expanded its relationship with InFocus from PCBA to system build. The provider has been selected to provide nearly 100% of InFocus' product lines out of Asia. What's more, Flextronics will provide global logistics management for Palm. Finally, under a new contract from Ceragon Networks (Tel Aviv, Israel), Flextronics will supply Ceragon with additional manufacturing capacity for its FibeAir broadband wireless products....Emulex (Costa Mesa, CA), a supplier of storage networking products, has selected Manufacturers' Services Ltd. (Concord, MA) to provide a full range of EMS from design and test development support through direct shipment to Emulex's customers. MSL is supplying Emulex out of Salt Lake City, UT, and expects to start production in Europe by the first half of the year. Also, MSL has been chosen by Honeywell Aerospace Electronics Systems to provide circuit card assembly for high-end products used in commercial and private aviation. MSL's advanced manufacturing center in Arden Hills, MN, will provide design, test and production services. The center specializes in complex, high-mix manufacturing....Solectron will serve the turnkey manufacturer for upcoming products from Cinta Corp. (San Jose, CA), which is developing optical switching and transport systems....Under a multiyear program, IEC Electronics (Newark, NY) will provide GenRad (Westford, MA) with turnkey PCBA services for all of GenRad's products. GenRad is an existing customer of IEC, which has assembled and integrated GenRad's Worldwide Diag-nostic System. GenRad recently announced it would outsource all PCB assembly (Feb., p. 9). IEC will also deliver production services for RiverDelta Networks' family of products. RiverDelta (Tewksbury, MA) provides carrier-class broadband routing, switching and service management solutions....Comdial Corp. (Charlottesville, VA), a provider of integrated communications, will outsource a majority of its manufacturing operations to Boundless Manufacturing Services (Hauppauge, NY), a subsidiary of Boundless Corp. The two parties have signed a supply and asset purchase agreement. The Boundless unit will perform PCBA, assembly and test of telephones, and supply-chain support services in its Boca Raton, FL facility. Revenue over the initial term of the agreement is expected to exceed $20 million. Boundless will acquire inventory from Comdial and some specialized equipment. Comdial expects to save over $10 million a year by outsourcing all of its manufactur-ing....SpringBoard Technology (Springfield, MA), a minority-owned CM, has received a turnkey manufacturing contract from Acterna (Germantown, MD) to build a communica- tions test platform for telecom networks.

EFTC's board of directors has received a proposal from K*TEC Electronics to combine the two CMs, which have ownership in common.

Last year, Thayer Capital Partners in partnership with BLUM Capital Partners acquired K*TEC (Sugar Land, TX) from Kent Electronics (Oct. '00, p. 6-7). K*TEC became a privately held company. The two private equity investment firms also own a controlling interest in publicly traded EFTC (Phoenix, AZ).

Although K*TEC proposed a non-cash transaction, the non-binding offer did not describe how the deal would be structured.

EFTC's board of directors has appointed a special independent committee to consider the proposal.

The proposed combination is subject to the approval of EFTC's special committee, board of directors and shareholders, as well as negotiation and execution of a definitive agreement among other conditions.

CM in Chapter 11...Century Electronics Manufacturing (Marlborough MA) and three of its divisions have filed for bankruptcy protection under Chapter 11. Included in the filing are Century New England, Century Florida and Century California. The operations are working toward a reorganization plan. But Century's offshore operations, Century UK and Century Thailand, are not part of the filing.