![]()

![]()

Last year, there were questions about whether India would emerge as a center for hardware manufacturing (June 2004, p. 1-4). Now those uncertainties are being quelled, at least on the telecom side.

To take advantage of India’s booming telecom market, manufacturing for cell phones and infrastructure equipment is underway in India, with more to come. The minister for communications and IT expects that India will attract some $800 million in investment from telecom equipment manufacturers during the current fiscal year, according to Indian news sources.

Investment will come from OEMs and at least one EMS provider, Elcoteq. The company recently completed construction of plant in Bangalore. This new plant will employ about 1,000 people when fully operational with the widely reported capacity to produce 10 million handsets a year. Products manufactured in Bangalore also include communications network equipment. Elcoteq is claiming the position as the first global EMS company to manufacture telecom equipment in India.

On the OEM side, Nokia this month announced that it will set up a manufacturing facility for mobile phones in Chennai. The company estimates that it will invest $100 to $150 million in the India plant, which will eventually employ about 2,000 people when at full-scale production. Another handset maker, South Korea’s LG Electronics, has already started handset manufacturing in a new operation near Pune. Unconfirmed reports are circulating that some other handset makers are interested in or exploring the possibility of manufacturing in India.

Infrastructure equipment suppliers are also on the scene. Ericsson is manufacturing radio base systems at its factory in Jaipur. What’s more, Huawei Technologies, which has a software development center in Bangalore, reportedly plans to set up a manufacturing operation in India. Citing an executive at Huawei’s Indian unit, Reuters reported that the company intends to invest about $100 million in the operation.

A tier-one EMS provider, Jabil Circuit, has also cast its vote in favor of manufacturing in India. Jabil is building its second plant in India, a 175,000-ft2 facility near Pune (Jan., p. 7). Scheduled to be fully operational by midyear, the site is expected to serve not only the telecom industry, but also the consumer, instrumentation, networking and peripherals segments. The provider sees a growing need for full turnkey solutions to serve the Indian market.

The powerful stimulus of India’s telecom market is attracting a surge of investment in manufacturing. According to Elcoteq, cell-phone penetration is a mere 3%, and services are growing at more than 100% a year. For a number of telecom players, this stimulus is enough to overcome the drawbacks of manufacturing in India. As these larger plants go into operation, demand will increase for local sources of component supply. Once a component supply base is developed, a major hindrance to manufacturing in India will be gone. When that occurs, India will have arrived as a manufacturing center.

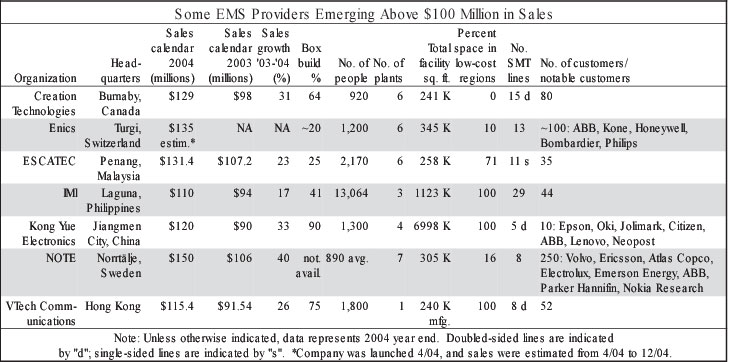

The EMS industry is consolidating, and the largest providers grow ever larger. MMI Top 50™ providers now control about 86% of the market. Has the door closed on opportunities to cross the $100-million line? Not so, according to data obtained in MMI’s annual Top 50 survey. The survey identified seven emerging providers with sales greater than $100 million but less than the $154 million it took to make the Top 50.

How have these emerging providers managed to push their revenues into nine figures? There is no single answer because these providers represent a cross section of the EMS industry. Some companies employ vertical integration, and some do not. Four out of the seven have all or a majority of their capacity in low-cost regions, but the remaining three do not. While Asia is home to four of these providers, two come from Europe, and one operates in North America. A majority have made acquisitions, but others have not. Design services include ODM work in at least two cases.

These emerging providers also followed different approaches to market segmentation. But four out of seven listed industrial electronics as contributing the largest percentage of 2004 sales. This reliance on one of the nontraditional EMS segments reflects increasing diversification within the industry.

Who are these emerging providers? See the table below for a list of them along with some data on each company. In addition, a short profile of each follows in alphabetical order.

Creation Technologies. This Canadian provider operates six manufacturing plants in North America – four in Canada and two in the US. The company does not have plants outside the region, but offers offshore manufacturing through partners in Asia. Creation gained its two US facilities by acquiring a Wisconsin provider in 2003 and a Texas operation in 2004 (Sept. 2004, p. 4). The provider wants to continue to expand throughout North America and is interested in the East Coast where it lacks a production site. Last year, Creation received a C$10-million investment from CIBC Capital Partners to fund customer growth requirements as well as US acquisition plans.

Creation is an employee-owned company, which is unusual for the EMS industry. The provider focuses on highly complex, medium- to low-volume product. Target markets consist of wireless telecom, medical, industrial controls, transportation and instrumentation. In 2004, the industrial and communications infrastructure segments amounted to 39% and 31% of sales respectively.

Founded in 1991, Creation achieved its 13th year of profitability in 2004.

Enics. A new company in 2004, Enics resulted from the sale of Elcoteq’s industrial electronics business. At present, Enics offers seven plant locations in Europe: four in Finland and one each in Switzerland, Sweden and Estonia. In addition, the company operates a 500-m2 production area in Beijing, China.

The European provider bills itself as one of the largest EMS companies in the industrial electronics field. Since Enics’ launch in April 2004, the company has grown quickly, with acquisitions playing a major role. When Enics started out last year, its annual sales were pegged at about 120 million euros. By Feb. 1, 2005, Enics had completed two deals: the addition of an ABB operation for PCB assembly and the acquisition of an EMS company owned by Ahlström Capital, principal shareholder in Enics (Feb., p. 6-7). With the completion of these two deals, Enics had upped its projected annual sales to 175 million euros.

This month, Enics announced yet another deal. The company will acquire Flextronics manufacturing operations in Malmö and Västerås, Sweden (see News, p. 6). With this acquisition, Enics’ annual sales will increase to about 250 million euros, or more than twice the annual rate that the company started with last year. Total employment will expand to some 1600 people.

ESCATEC. This vertically integrated design and manufacturing services provider offers medium- to high-volume manufacturing in Asia and prototyping, NPI and smaller series manufacturing services in Europe. The ESCATEC Group has three facilities in Malaysia, one in Singapore, one in Indonesia, and one in Switzerland. In addition, the company opened a new plastic injection molding and mold-making facility this month in Shanghai, China.

The provider’s vertical integration model not only includes plastics capabilities, but also coil and transformer assembly, metal stamping and mechatronic assembly. On the front end, the company has expanded its design services in Switzerland and Malaysia.

Asia-based ESCATEC is led by two Swiss executives – Markus Walther, COO, and Christophe Albin, executive chairman. Albin, one of the founders of ESCATEC, is its owner.

ESCATEC serves customers in the industrial electronics, high-end consumer electronics, audio/video, power tool, medical and automotive markets. In 2004, 39% of its sales came from the industrial segment, while consumer and handheld devices represented 36%.

The provider was founded in Singapore in 1974. Two years ago, ESCATEC acquired Wiltronic AG in Switzerland from Leica Geosystems AG. This deal added advanced electronic design, development, test, prototyping and NPI capabilities to the group.

IMI (Integrated Microelectronics, Inc.) Until recently, IMI’s manufacturing operations were confined to the Philippines, where the company had become one of the two largest providers based in that country. In February, IMI announced a deal that extended IMI’s footprint to the US West Coast. The company acquired two operations of Saturn Electronics & Engineering; one of them is located in Tustin, CA, and includes both EMS and ODM assets (Feb., p. 7-8). IMI also bought from Saturn a high-volume SMT operation in the Philippines.

Despite competition from China, IMI has maintained its position as a major EMS player in the manufacture of optical and hard disk drives (March 2004, p. 4-5). IT-related products accounted for 56% of IMI’s sales in 2004. IMI’s customers include Japanese OEMs who are leaders in the storage device market. Among other markets served by IMI are consumer and handheld devices at 18% of 2004 sales and industrial electronics at 17%. IMI reported that Japanese customers account for 70% of annual sales.

An IMI subsidiary, EAZIX, offers design services such as hardware and software design as well as ODM products.

Founded in 1980, IMI is a member of the Ayala Group.

Kong Yue Electronics & Information Industry Ltd. This Chinese EMS provider operates in an industrial park located in Jiangmen City within the Southern China province of Guangdong. Kong Yue is vertically integrated with facilities for plastic injection molding, rubber parts manufacturing and metal stamping. Services encompass manufacturing, sales distribution, post-sales services, logistics and reverse logistics. The company promotes its strength in the design and manufacture of opto-electromechanical parts and products. Kong Yue also emphasizes the international experience of its management team, made up of individuals from Canada, Hong Kong, Japan, Malaysia and Singapore.

Founded as a printer distributor in 1986, Kong Yue began contract manufacturing for Epson and Citizen printers in 1996. Although Kong Yue has a history of serving Japanese customers, the company wants to be known for more than that now. The provider also manufactures for Chinese brands such as Jolimark and Lenovo and for companies such as ABB and Neopost, both based outside Asia.

Kong Yue still relies on the IT industry for the bulk of its sales. Office equipment represented 75% of the company’s 2004 sales. The second largest portion of sales came from the automotive side. Besides printers, products manufactured by Kong Yue include electronic cash registers, car audio units and projectors.

NOTE AB. In recent years, this European provider acquired a number of electronics operations in Sweden and now operates five production facilities in the country, according the company’s website. In addition, NOTE has factories in Estonia, Finland and Lithuania and utilizes a network of subcontractors in Poland. The company has shifted its focus in Sweden from volume manufacturing to development, industrialization, and lower-volume, higher-complexity production. For global manufacturing needs, NOTE led the formation of the ems-ALLIANCE, a network of providers in Brazil, China, India, Sweden and the US.

Also, NOTE offers industrialization services close to key client areas through small units called Gateways. They are located in two areas of Sweden as well as in the UK and France. Like NPI centers, Gateways can act as a portal for connecting customers with other NOTE operations.

At 32% of 2004 sales, industrial electronics was the largest segment of NOTE’s business last year. The second largest was telecom accounting for 24%, followed by security systems at 18%.

NOTE made two acquisitions recently: an Ericsson operation in Sweden (Feb., p. 6) and a Finnish contract manufacturer (Jan., p. 6).

Publicly traded in Sweden, NOTE was founded in 1999 under the name EuroSupply.

VTech Communications Ltd. VTech offers circuit design, PCB layout, full mechanical design, board assembly and system build from its Southern China factory in Dongguan. The provider can also do its own plastic injection molding and tooling fabrication. When it comes to lead-free assembly, VTech was an early adopter, having implemented lead-free processing in 2002.

Products manufactured by VTech include switching power supplies, professional audio equipment, home appliances, RF modules and telecom products, mobile phones, medical products, and automotive products. Consumer and handheld devices made up 57% of VTech’s sales in 2004. The industrial segment contributed the second largest portion of sales with 25% of the total. Next was communications infrastructure at 12%.

On the design side, VTech specializes in industrial, electrical and mechanical design for RF/wireless products and audio electronics, among others. For systems assembly, design capabilities include structural layout, enclosures, cable harnesses and assemblies, and intelligent power supplies.

VTech Communications was founded in 1993 as a subsidiary of the VTech Group of Companies. The parent company is known as a manufacturer of cordless phones and electronic learning products.

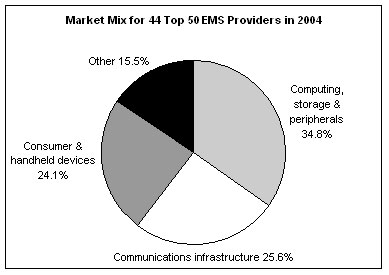

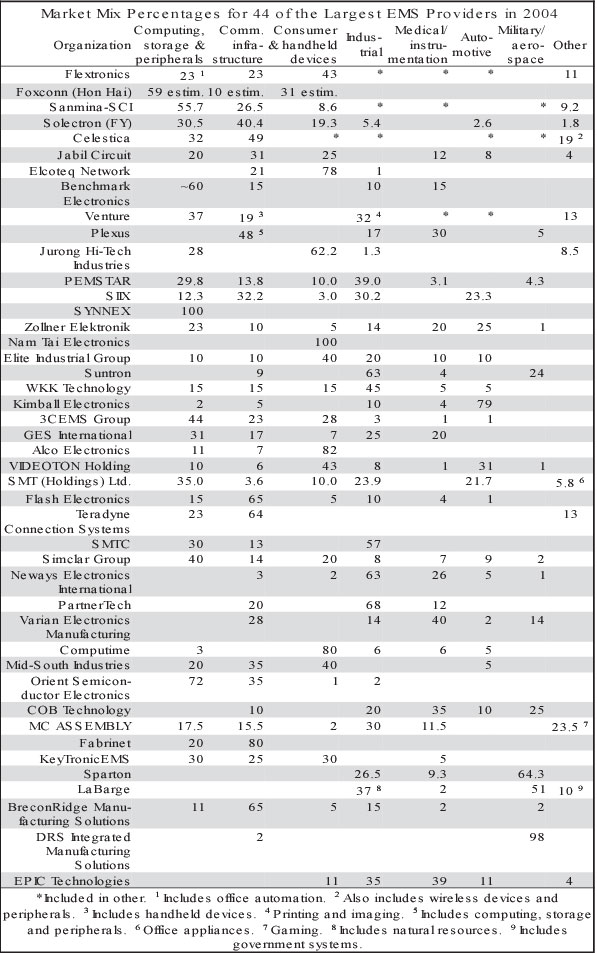

Where once there were two major segments of the EMS market, now there are three. Based on data from 44 MMI Top 50™ EMS providers, computer-related business and communications infrastructure still represent the two largest segments of the EMS industry. But consumer and handheld devices are now running a close third, reflecting growth in this segment, particularly in cell phones.

Consumer and handheld devices accounted for 24.1% of sales for this Top 50 group, compared with 19.4% of combined sales for 46 providers in the 2003 Top 50. This market share gain shows that sales from consumer and handheld devices grew faster than Top 50 revenue and, by extension, the entire EMS market. The growth of this consumer-oriented segment is one indication of the diversification that the EMS industry undertook in response to the business downturn that shook the industry a few years ago. When the downturn hit in 2001, the industry’s dependence on computer and communications business turned into a weakness.

Computing, storage and peripherals still comprised the largest segment in 2004, based on Top 50 data. But its market share shrank. Computer-related business took 34.8% of the Top 50 group’s sales last year, down from 41.7% calculated from Top 50 data in 2003. The computer industry, once the mainstay of the EMS business, now represents little more than a third of it.

Communications infrastructure, the hardest hit segment during the downturn, actually held its own vis-á-vis the other segments in 2004. For the 44 Top 50 providers in 2004, communications infrastructure contributed 25.6% of sales versus 24.3% for the 2003 group. Given that 2004 Top 50 sales grew by over 25%, a flat or slightly increased share for comm infrastructure (datacom and telecom) meant that this segment rebounded nicely last year.

Segment market shares were derived from segment percentages tabulated below for each of the 44 Top 50 providers. A few Top 50 providers were unwilling to furnish market segment data. Foxconn was among them. But the company’s size and impact could not be overlooked so Foxconn’s market segment data was estimated.

Note that since some top-tier providers did not break out their sales by industrial, medical and instrumentation, automotive or military/aerospace, market shares for these categories could not be computed. As a result, these four segments are lumped into the "other" category shown on the pie chart. This other category has now reached 15.5% of sales, up slightly from 14.6% computed from 2003 Top 50 data. From all effort that has gone into pursuing business from the four segments in the other category, one might have expected a greater increase in market share. The other category also includes some miscellaneous product areas (see table footnotes).

The 44 Top 50 providers, for which market segment data is available, generated combined sales of $90.92 billion in 2004, or 96% of Top 50 sales. The segment market shares calculated from this data are not precise. From the table on page 5, one can see that in some cases, based on how a company broke out its sales, one category is combined with another.

In yet another example of consolidation below the industry’s top tier, NASDAQ-listed SigmaTron International (Elk Grove Village, IL) has signed a non-binding letter of intent to purchase Able Electronics (Hayward, CA), a privately-held EMS company, for an undisclosed sum.

With over 200 employees, Able offers manufacturing capacity of 185,000 ft2 split between Hayward, CA, and Tijuana, Mexico. The provider serves OEMs in telecom, internetworking, medical instruments, computer peripherals, industrial controls, genetic research applications, and semiconductor testing. Following a vertical integration strategy, Able has the cable assembly, sheet metal fabrication, powder coating and silk screening to make its own custom enclosures. Able’s EMS menu ranges from design services and prototyping to systems integration and test, fulfillment, and sustaining services.

“This acquisition will give SigmaTron significant industry expertise in a number of new markets, which when combined with our existing customer base, will diversify and expand the number of industries we will serve,” stated Gary Fairhead, SigmaTron’s president and CEO. He said the deal will also expand the range of services offered by SigmaTron.

In Form 10-K for the company’s fiscal year ended April 2004, SigmaTron reported that its customers (in order of contribution) were in the appliance, gaming, industrial electronics, fitness, telecom, consumer electronics and automotive industries.

Another proposed transaction, announced the same day, will affect SigmaTron’s gaming business. The company has entered into a non-binding letter of intent to sell its Las Vegas, NV, operation, which serves customers primarily in the gaming industry. The buyer is Grand Products (Des Plaines, IL), a contract assembler of coin-op games and gaming machines. SigmaTron said the sale will allow it allocate more resources for expanding capabilities in higher growth locations. The company will use the proceeds and additional free cash flow to explore other niche acquisitions or invest in other operations.

Other manufacturing facilities sit in Elk Grove Village, IL; Acuna, Mexico; Fremont, CA; and Suzhou-Wujiang, China.

Flextronics (Singapore) is divesting two regional manufacturing operations in Sweden. Enics (Turgi, Switzerland), an EMS provider focused on industrial electronics, will acquire Flextronics’ EMS activities in Malmö and Västerås, Sweden. This will be Enics’ third transaction in recent months (Feb., p. 6-7).

“It brings highly qualified resources to us and enables Enics to expand its established based in Sweden, where we see solid and exciting opportunities for our company to grow. Furthermore, it comes with a rich portfolio of globally recognized OEMs, each one of which is perfectly matching our focus, and complements Enics’ strong position to provide full life cycle services to customers in the whole Scandinavian region,” stated Reijo Itkonen, president and CEO of Enics.

The Malmö and Västerås operations handle low to medium volumes and high mix. With a built-up area of 53,800 ft2 and about 160 employees, the Malmö activity has manufactured industrial, medical and mobile communications products. It also contains a design center offering services such as software design and hardware development. The Västerås operation has a total manufacturing area of 204,100 ft2, and its portfolio covers automotive, datacom and telecom, and industrial products. Both sites include Flextronics Network Services operations, which are not part of the sale.

Publicly-held Three-Five Systems (Tempe, AZ), which has evolved from a display company to an EMS provider, is working with SG Cowen & Co. to review alternatives for maximizing shareholder value. TFS is exploring a range of possible options, such as acquisitions, strategic alliances, business combinations, and the sale of a portion or all of the company.

The company has signed a definitive agreement to sell the assets of its small-form-factor display business to International Display Works. Under review are TFS’s large display, EMS and RF module manufacturing businesses. The company is currently in discussions with multiple potential buyers of the RF business and has received an initial offer from a potential buyer of the EMS business. TFS stated there is no assurance that any other transactions will result.

Deal done…Ambitech International (Chatsworth, CA) has sold Hunter Technology (Santa Clara, CA), a provider of PCB fabrication and EMS, to an investor group led by Hunter Technology management. Hunter specializes in high-mix, high-complexity products for the medical, aerospace, communications and capital equipment markets.

New programs…Netherlands-based Oce, a provider of document management technology and services, has entered into a manufacturing and supply agreement with Flextronics....Novadaq (Mississauga, Ontario, Canada) has selected Suntron (Phoenix, AZ) to manufacture Novadaq’s fluorescent imaging system for coronary artery bypass surgery. Also, Suntron will build HDTVs and light engines for Brillian (Tempe, AZ) under a multiyear agreement designed to ramp Brillian’s manufacturing capacity. The two companies had worked together for a year….US-traded Nam Tai Electronics (Tortola, British Virgin Islands) has won orders from a new customer, Taiwan’s Inventec Multimedia & Telecom, for production of LCD modules used in its Internet Protocol phones….Northstar Network (St. John’s, Newfoundland, Canada), a subsidiary of Northstar Electronics (Vancouver, BC, Canada), has landed a contract from Cathexis Innovations (St. John’s, NL, Canada) to manufacture its handheld RFID reader….Aegis Assessments (Scottsdale, AZ) has chosen CirTran (Salt Lake City, UT) to redesign and manufacture the SafetyNet RadioBridge, which interconnects incompatible radios at emergency sites.

New ODM product…Sanmina-SCI (San Jose, CA) has designed an entry-level network attached storage box to simplify storage management for small businesses, homes and media centers. The NAS box will be available through Bell Microproducts.

Jabil Circuit (St. Petersburg, FL) has announced a number of promotions. John Lovato has moved from his senior VP position to regional president – Europe. Lovato, who joined Jabil in 1990, has held positions of increasing responsibility, including senior VP, business development. Michel Charriau, who had been European COO, will assume the role of senior adviser and will work closely with Lovato. The company has made Kevin Mazula VP, sales – Europe. Mazula joined Jabil in 2003 with responsibility for European sales. Maurice Dunlop goes from senior director of business management for Western Europe facilities to VP, business development – Europe.

The company has advanced three people to the position of VP, global business unit. One of them is Carey Paulus, who most recently served as senior business unit director for accounts including Cisco and Philips. Another person earning this title is James Luginbill, who was responsible for taking the HP account to Jabil facilities worldwide. The third individual named to this position is Anthony Allan, who will head Jabil’s efforts in the medical marketplace. Allan has served as senior business unit director and worked to assimilate Jabil acquisitions in Europe.

Finally, Jabil has appointed Thomas O’Connor as VP, human resources, a newly created position. He most recently served as senior director, human resources – Americas.

More people on the move…Publicly held Sypris Solutions (Louisville, KY) has named Robert Sanders president of its Sypris Electronics subsidiary (Tampa, FL). He is replacing James Cocke, who previously served in that role. Sanders recently joined Sypris Solutions as group VP for its Electronics Group. He had served as a GM and site executive for the Defense & Space Electronics Systems division of Honeywell....Solectron (Milpitas, CA) has appointed Tony Princiotta as VP, enclosures systems business, and Hossein Saadat as VP of operations, enclosures….CTS (Elkhart, IN) has made Don Schroeder president of CTS Electronics Manufacturing Solutions (Moorpark, CA), a business unit of CTS and an MMI Top 50™ EMS provider. The CTS unit combines CTS’s interconnect business with the recently acquired SMTEK International. Schroeder will retain his position as corporate executive VP. ...Reptron Electronics (Tampa, FL) has hired Charles Pope as CFO. He most recently served as CFO of SRI/Surgical Express….I. Technical Services (Norcross, GA) has appointed Chuck Tillett as president and COO. An industry veteran of over 20 years, Tillett has held senior management positions with several EMS companies. Most recently, he served as VP for US and Mexico operations at MC ASSEMBLY.…Eric Olsen, Ph.D., former worldwide manufacturing educator for HP, has joined Venture Outsource Group (San Jose, CA) as a senior consultant. Dr. Olsen will work with the consulting firm’s clients to develop custom, lean manufacturing solutions....Plexus (Neenah, WI) has appointed Peter Kelly to its board of directors. Kelly is executive VP of the Global Operations Group of semiconductor supplier Agere Systems. He has experience as a COO and CFO for multinational corporations.

CEO pay listed…A recent special report by the New York Times (April 3, 2005) listed the 2004 pay granted to CEOs of 179 large companies. Three of these CEOs run tier-one EMS companies. Jure Sola, CEO of Sanmina-SCI, received total compensation of $15.0 million last year, up from $1.2 million in 2003, according to the newspaper. In 2004, the total pay of Michael Cannon, CEO of Solectron, decreased 68% to $6.2 million. Timothy Main, CEO of Jabil Circuit, saw his total compensation increase 128% to $4.3 million last year. To find total compensation, the New York Times added up base salary, bonus, restricted stock and long-term incentives, and option grant value.

Making changes in operations… Solectron will lay off 691 employees in Timisoara, Romania, over the next six months. The Romania operation will shift its emphasis from high-volume manufacturing to lower volume, higher mix, higher complexity and quality engineering services….Celestica (Toronto, Canada), which is undergoing another round of restructuring, will close two more plants, bringing to five the number of operations recently slated for closure (Mar., p. 7). News sources reported that the company will shutter its Fort Collins, CO, facility, and, according to Reuters, Celestica has also decided to close its plant in Barcelona, Spain….During Q1, Benchmark Electronics (Angleton, TX) closed its Manassas, VA, facility.

Top 50 correction: The sales used to rank Teradyne Connection Systems in the MMI Top 50 published last month were from 2003 instead of 2004. Based on the Teradyne unit’s 2004 sales of $244.0 million, the unit should have been ranked 34th, not 31st as was published. A revised electronic copy of the Top 50 is available for subscribers. To obtain a copy, email jbt@mfgmkt.com.

An April 3rd article in the New York Times ran with a disturbing headline: “Help Wanted: China Finds Itself with a Labor Shortage.” The article reported a shortfall of some two million workers in the Southern China provinces of Guangdong and Fujian. This shortage amounts to about 10% of the total migrant labor pool in the two provinces, according to the New York Times. Another publication echoed this theme. The Shenzhen Daily recently reported that Guangdong faces a labor gap of more than one million this year, based on a government survey.

These reports blast a hole in one of the bedrock beliefs about outsourcing to China. The assumption is that China’s supply of labor is inexhaustible. Apparently, this is no longer the case in Southern China. As the New York Times article described, some workers have left Southern China for better wages and working conditions in other parts of the country. The Yangtze Delta region, in particular, has emerged as major competition for migrant workers. This newer mecca for manufacturing, which includes Shanghai, is attracting workers who otherwise might have migrated to Southern China.

Is this shortage affecting the EMS industry in Southern China? As far as MMI can tell, the large US-traded EMS providers have said nothing about a labor shortage creating problems for them in China. If a shortage were to have a material effect on their operations, they are obliged to say so.

There is a good reason why this shortage would not have a significant effect on EMS operations in Southern China. EMS providers can afford to pay high enough wages to attract the workers they need. After all, labor content is a small portion of product cost. These providers have an advantage over smaller, labor-intensive factories where the pay is less and working conditions are not as good.

Take Nam Tai Electronics. The company met its Q1 target of hiring about 1,000 new employees for its factories in Baoan, Shenzhen, and has not encountered any hiring problem. Nam Tai believes the wages and benefits its offers are quite attractive when compared to those offered by other companies in the area. Since recruiting is not a problem, Nam Tai says there is no pressure to increase labor costs at present.

Still, this labor shortage is affecting wages elsewhere in Southern China. A government survey of 35,000 companies in Guangdong found that 40% of them are considering pay increases this year, according to the Xinhua News Agency. EMS operations such as Nam Tai’s might not need to increase their wages, but pay raises elsewhere in Southern China can potentially ripple through the supply chain of materials sourced in the region.

China is merely showing that it is no different than any other labor market. The torrid growth of manufacturing in China has created such a demand for labor that not only companies, but also regions are competing for workers. Migrant workers, which are the fuel for China’s manufacturing economy, are voting with their feet.