![]()

![]()

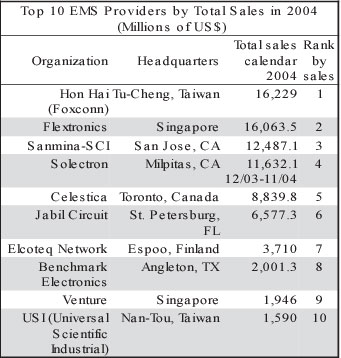

Two months ago, MMI estimated that consolidated sales of Hon Hai Precision Industry (also known by its Foxconn trade name) would rank second in the EMS industry for 2004. But MMI also raised the possibility that if the estimate were off, Flextronics’ hold on the top spot would be in question. Hon Hai has now reported its consolidated sales for 2004, and the Taiwan-based company has indeed taken over the number-one position as the largest EMS company by total sales. Hon Hai becomes the fourth company to lead the industry in sales.

For 2004, Hon Hai reported consolidated sales of NT$541.60 billion, or $16.23 billion based on last year’s average annual exchange rate (NT$33.372 = US$1) reported by the US Federal Reserve. As a result, Hon Hai edged out Flextronics, the former number one, whose 2004 sales were about $165 million below Hon Hai’s (see table). The company’s sales were up 39% in US dollar terms (34% in Taiwanese dollars).

Not only is Hon Hai the largest EMS company by sales, it’s also among the most profitable. For 2004, the provider earned net income of NT$29.76 billion, or $892 million, which equates to a net margin of 5.5%. By contrast, Flextronics earned net income of $281.6 million for the calendar year, or a net margin of 1.8%.

Nonetheless, the question of who is the largest EMS provider is still open to debate. Earlier this year, Hon Hai ranked itself as the number-three contract manufacturer worldwide on a promotional website. Perhaps the company was counting SMT capacity, which it reported as ramping to 350 SMT lines in Q4 2004. This is not the highest capacity in the industry. Or perhaps Hon Hai was excluding its substantial components business, where the company got its start. (Hon Hai is a major supplier of PC enclosures, heat sinks and connectors.) Still, if one looks at manufacturing space, Hon Hai wins hands down with 37 million ft2.

With much of its manufacturing in China, Hon Hai is known as a low-cost producer. The company operates four industrial parks in China, the largest of which employees over 80,000 people in Southern China. Among other facilities is an operation located in the Czech Republic and described by Hon Hai as the world’s largest PC assembly facility.

Evolving from a components supplier to a vertically integrated system builder, Hon Hai turned its low-cost position into a winning strategy. With an average growth rate of 55% over a decade, the company quickly rose through the ranks of the EMS industry. But until a few years ago, Hon Hai was largely unknown outside of Asia because it kept quiet about its operations. Although the company continues to provide few details about its operations (at least in English) other than what is required as a publicly listed company in Taiwan, Hon Hai’s financial results speak for themselves.

Like some others in the EMS industry, Hon Hai has been pursuing an ODM strategy to enhance its offerings. Last year, the company made a big move into the ODM business with its acquisition of a communications ODM, Ambit Microsystems. Now Hon Hai is extending its ODM capabilities to cell phones. Hon Hai’s handset spin-off, Foxconn International Holdings, which is controlled by Hon Hai, has entered into agreements through an FIH subsidiary to acquire 56.5% of the shares of Chi Mei Communications Systems (CMCS), a Taiwan-based ODM in the mobile phone industry. The price for this controlling interest is NT$2.50 billion, or $78.4 million. Hon Hai’s pursuit of CMCS was reported earlier (Feb., p. 7).

CMCS provides handset brand names with services including design, manufacturing, testing, and advanced wireless technology applications. The company focuses mainly on GSM, GPRS, and EDGE handsets and modules. It is well known that Motorola is a customer of both CMCS and Hon Hai. Established in 2001, CMCS is part of Taiwan’s Chi Mei Group, whose activities are in the petrochemical industry and other sectors.

According to Bloomberg.com, Hon Hai chairman Terry Gou in January gave a TV interview in Taiwan during which he said he expected company sales to grow 30% annually over the next four years. Although Hon Hai has grown faster than that rate in the past, 30% is still well above projected growth rates for the EMS industry.

One way Hon Hai can continue to grow is by obtaining more business from existing customers. Earlier this year, the company entered into a technology collaboration agreement with HP (March, p. 5). A May 19 report from Taiwan, if true, would indicate that Hon Hai continues to deepen its relationship with HP. Quoting an unnamed official at Hon Hai, the Taipei Times reported that Hon Hai will purchase HP’s computer assembly plant in Australia. In response to an earlier report, Hon Hai stated that it “has not acquired HP’s India nor Australia plants.” However, Hon Hai’s denial does not rule out the possibility that it will acquire the Australia plant.

Last year, Hon Hai entered the divestiture game with its acquisition of a Motorola handset operation in Chihuahua, Mexico.

The outsourcing space grows larger and larger, but it is also becoming more difficult to quantify. This ambiguity arises mostly from the ODM side of outsourcing. In recent years, high growth rates of the ODM business have meant that the ODM share of the outsourcing space has steadily expanded. With a greater share comes more influence on the total outsourcing market and the need to more accurately assess the effect of ODMs on the total space. Yet the ODM business is becoming harder to pin down.

What’s behind the uncertainty? Some Taiwanese ODMs have branched out into selling products under their own brand names. Companies such as Asustek Computer, BenQ and MiTAC are building own-brand businesses in addition to the other work that they do. But they don’t split out these growing businesses in their financial reports. This information is hard to come by, unless one can mine it from an annual report, typically written in Chinese. According to BenQ’s annual report, 63% of its business is ODM.

Then there are cases where an ODM is also doing EMS work. For example, it is well known that Wistron is a supplier of Microsoft’s Xbox game console. And Asustek has been identified as a builder of Sony’s PlayStation 2 console as well as a contract manufacturer for Apple. Again, these EMS businesses are not segmented within company total sales.

The motherboard industry further complicates matters. Distribution serves as a prime channel for motherboard sales. But some boards are sold directly to OEMs on an ODM basis. How many? One can only guess.

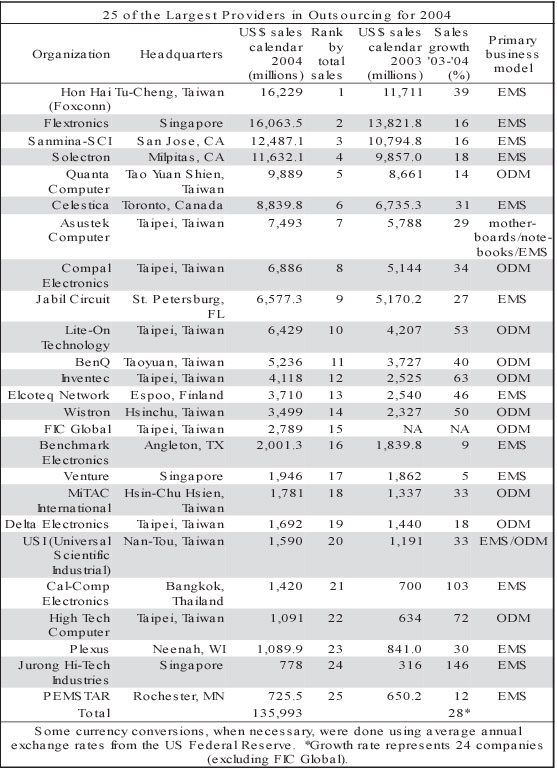

Despite ambiguities on the ODM side, MMI has attempted to provide a rough measure of the outsourcing market and its growth. To this end, MMI has compiled a list of 25 of the largest companies in the outsourcing space (see table). The list consists of 14 EMS providers and 11 companies in the ODM business. (The largest motherboard suppliers were not included except for Asustek, which is more diversified.)

Sales for the 25 outsourcing suppliers in 2004 totaled $136 billion, which gives an indication of two things: the size of the outsourcing space and the concentration of business. It is clear that the outsourcing market easily surpassed $136 billion last year. Any non-outsourcing business among the large ODMs was more than made up by sales of EMS providers and ODMs below the top 25. For example, the bottom 37 EMS providers in the MMI Top 50 accounted for $11.5 billion in 2004 sales.

With combined sales of $85.1 billion, the 14 EMS providers in the group represented 63% of its total sales. The remaining 37% came from the 11 ODMs, where in some cases own-brand and other EMS sales were mixed in.

Ten companies had sales over $6.4 billion, and 23 suppliers exceeded $1 billion in revenue. It took a minimum of $725 million in sales to make this top 25 list.

For 24 of the 25 companies, overall sales increased by 28%. (One company, FIC Global, did not report 2004 sales. It was listed in its current form last year.) This rate was higher than growth for the 14 EMS companies in the top 25 group by about 3%. ODM growth was responsible for this slight increase in outsourcing growth above the average for the EMS providers. Together, ten Taiwanese ODMs in the group increased sales last year by 34%, about nine points above the EMS companies in the group. So based on this data, the gap between ODM and EMS growth narrowed substantially from 2003 (May 2004, p. 1).

Nine out of 11 ODMs reported positive net income for 2004. Net margins for the 11 averaged 3.6%.

This month, Flextronics (Singapore) announced two important changes that will be made in its organization. The company has named a successor to CEO Michael Marks and has decided to divest two of its businesses.

Marks will retire as CEO on Jan. 31, 2006, and COO Michael McNamara will succeed him as the new CEO at that time. This plan was revealed at Flextronics’ analyst and investor meeting held in May. In addition, Marks will become chairman of the board upon his retirement, and the current chairman, Richard Sharp, will relinquish that role but remain on the board.

Under Marks’ leadership, Flextronics has grown from a $100-million company in 1994 when it went public to a $15.9-billion enterprise in its fiscal 2005. Marks has also left his imprint on the EMS industry in other ways such as pioneering the industrial park strategy and adopting the ODM model.

McNamara joined the company in 1994 through its acquisition of Relevant Industries, where he served as president and CEO. Through his time at Flextronics, he has taken on more and more responsibilities.

Flextronics has an agreement in principle to merge its Flextronics Network Services (FNS) subsidiary with Telavie AS, a company owned by Altor, a private equity firm focusing on investments in the Nordic region. In addition, Flextronics has held discussions with a number of companies about the potential sale of 100% of its Flextronics Semiconductor Design business.

Under the terms of the proposed FNS merger, Flextronics would receive an undisclosed cash payment plus additional contingent payments along with 30% ownership in the combined company. Assuming both transactions are completed, Flextronics would receive cash totaling between $550 and $600 million plus the contingent payments. Completion of the FNS merger is subject to, among other things, consultation with the FNS unions in Sweden.

Although these divestitures would reduce Flextronics’ sales by about $840 million, they are not expected to have a meaningful impact on fiscal 2006 EPS. That’s because the company expects to use the proceeds to repurchase stock or debt or some combination. “We don’t think we need any additional cash to manage the core business,” said Marks during the analyst and investor meeting.

He gave two reasons for the divestiture of FNS. Ericsson and other customers perceived FNS to be in competition with them. Secondly, the synergies between FNS and the parent company lessened as FNS drew closer to the carriers and farther from its hardware customers.

In the case of the semiconductor design business, Marks said, “We can’t really sell to our competitors who could use this service.”

Earlier during Flextronics’ April conference call, Marks said the board had recommended that the company evaluate five businesses outside its core EMS operations and related strategies to increase shareholder value including potential divestitures, IPOs and spinoffs. In addition to FNS and the semiconductor design operation, the other businesses on this review list are Multek, Flextronics’ PCB fabrication unit; the company’s India-based software products and services operation; and its cell-phone components business.

One option being considered is a transaction similar to Hon Hai’s spinoff of its handset operations into a public company majority-owned by Hon Hai.

Flextronics is already familiar with this approach. Flextronics Software Systems Limited, a major piece of Flextronics’ software business, is a publicly-held company in India. Flextronics, which owns 69.7% of the Indian outfit (formerly known as Hughes Software Systems Limited), proposes to acquire the outstanding shares at an estimated cost of $125 to $150 million.

Besides announcing the two divestitures, Flextronics also said it is considering further restructuring of other operations that could result in charges in the range of $100 million in fiscal 2006. The idea is that when McNamara takes over as CEO “he starts with as clean a sheet of paper as we can get,” said Marks at the May meeting.

Jabil Circuit (St. Petersburg, FL) plans to acquire assets of Emtac Technology (Hsinchu, Taiwan), a GPS technology company with its own GPS product line. Emtac’s GPS technology is expected to benefit Jabil in mobile products, automotive telematics and other applications.

The focus of the acquisition is Emtac’s expertise in design, manufacturing engineering and systems architecture.

According to Ralph Leimann, VP of engineering services at Jabil, the Emtac acquisition enables Jabil to provide customers valuable design capabilities from Taiwan. Not only does the acquisition offer tax benefits, potential government assistance, and a location in the prestigious Hsinchu Science-Based Industrial Park, engineering costs are still very competitive in Taiwan, said Jabil.

The deal is expected to be completed in June. Jabil will acquire a majority of Emtac, and the purchase will not include Emtac’s business in low-temperature co-fired ceramics, according to a report from DigiTimes.com.

Micro Dynamics Corporation (Eden Prairie, MN), an EMS provider, and Logic Product Development (Minneapolis, MN), a supplier of product development services and embedded computing products, have merged. By combining product development with manufacturing, the merged company believes its offering is at a level of sophistication that customers would normally find only in larger providers.

“Streamlining new product development and manufacturing activities is a top priority of original equipment manufacturers (OEMs) worldwide, and addressing that challenge requires a tightly controlled combination of product design insight, technology integration experience, and manufacturing expertise,” stated Mike Brown, CEO of Micro Dynamics. “The merger of Micro Dynamics and Logic integrates these capabilities to offer a new flexible electronic manufacturing services (EMS)/product development model that in the past has only been available to high-volume customers.”

Logic Product Development will maintain its brand identity and will function as a subsidiary of Micro Dynamics. The new company will operate three core business units: Product Development Services, Embedded Computing Products, and EMS Services. Its integrated product development and new product introduction solutions include user research and product design; embedded computing modules; rapid prototyping and test development; and manufacturing, fulfillment and logistics services. These integrated offerings are designed to simplify product development and accelerate time to market.

Founded in 1981, Micro Dynamics is a privately-held EMS company, which operated three facilities in Minnesota prior to the merger. Last year, the company generated sales of around $55 million, which represented growth of 51%. Sales for 2005, including Logic, are projected to be $70 to $75 million. With the merger, Micro Dynamics has increased its work force from about 360 people to about 435.

The two companies have worked together for at least four years.

CHB Capital Partners and Wells Fargo Bank served as financial partners in the transaction. Micro Dynamics engaged the companies last year to provide financing for its growth initiatives.

Fabrinet (Bangkok, Thailand), an MMI Top 50 EMS provider, intends to purchase JDS Uniphase’s manufacturing facilities in Fuzhou, China. The deal will expand Fabrinet’s operations into China. JDS also plans to divest manufacturing facilities in Ewing and Mountain Lakes, NJ, to Fabrinet as part of broader cost-savings initiatives. The New Jersey facilities will give Fabrinet its first manufacturing sites in the US.

In China, Fabrinet will acquire Fuzhou plant assets and operations including R&D and the manufacture of products such as crystals and precision optics. The 225,000-ft2 plant employs over 500 engineers, technicians and operators, all of whom are expected to transfer to Fabrinet. The company intends to utilize management and technical expertise at the site to grow its optical component business in China and in other regions Fabrinet serves.

“Expanding our Asian operations to China and growing our optical component manufacturing operations in that market will enable Fabrinet to provide greater flexibility and support to our existing customers and additional resources to attract new customers,” stated Tom Mitchell, founder and CEO of Fabrinet.

Transfer of the Fuzhou plant is expected to be completed prior to June 30, while the New Jersey facilities are scheduled to be transferred by the end of the current quarter.

These prospective transactions will follow an earlier deal between the two companies. In December 2004, Fabrinet acquired JDS’s manufacturing facilities in Bintan, Indonesia, and Singapore (Nov. 2004, p. 6). JDS has been a Fabrinet customer since 2000.

JDS will also consolidate its Ewing, NJ, and Melbourne, FL, manufacturing to its Shenzhen, China, facility and to the facilities of two contract manufacturing partners.

Two EMS providers have announced deals – one proposed and one completed – where the acquisition target operates apart from the EMS industry. These deals show that diversification can take place not only within the industry but also outside it.

In the first case, Sparton (Jackson, MI), an MMI Top 50™ EMS provider, has signed a binding letter of intent whereby Sparton plans to acquire the HDJ Company (Lancaster, PA), which manufactures and sells a variety of specialized medical products, generally involving precise, high-quality machining. The acquisition also includes HDJ’s wholly owned subsidiary, Specialized Medical Products.

HDJ’s unaudited sales for 2004 totaled about $9.4 million, and its earnings are described as strong. The company’s largest market is orthopedic products, including plates, screws and systems for implantation by a surgeon.

Sparton intends to operate the business as a wholly-owned subsidiary at its present location and with the current management and staff. The acquisition is subject to the completion of a due diligence review and execution of a definitive purchase agreement. Closing is expected before July 31.

The second example of external diversification involves another MMI Top 50 provider, Simclar Group (Dunfermline, Scotland). Simclar has acquired UP Mex (Preston, UK), which manufactures chair mechanisms.

Although the acquired company is not doing EMS work, there is a connection to Simclar. “Some of what we do in Europe is assembly of sheet metal. So it’s not a far-flung acquisition,” said Barry Pardon, president of Simclar, Inc. (Hialeah, FL), which is a publicly-held member of the Simclar Group.

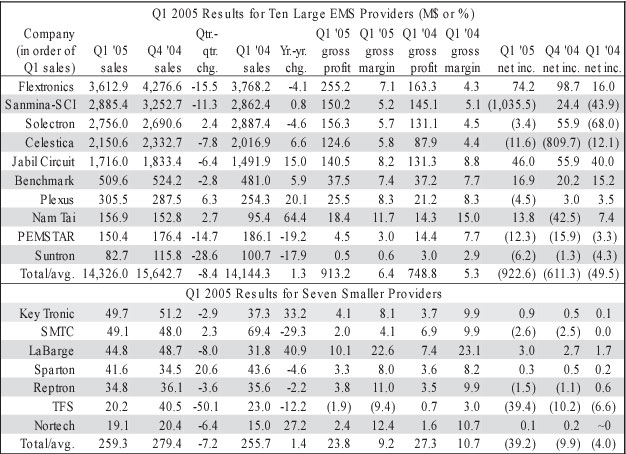

Takeover target?...The May 23 edition of BusinessWeek presented a list of 15 potential takeover targets, screened from a database of 5,875 companies. Solectron (Milpitas, CA) made the list, which was based on six financial measures.

New alliances…Libra Industries (Mentor, OH) and Surface Mount Technology (Holdings) Limited (Hong Kong) have entered into an agreement calling for Libra to act as a North American distributor and sales representative for SMT (Holdings) Ltd., an MMI Top 50 provider that operates three manufacturing facilities in China. As a distributor for the Hong Kong-based provider, Libra will provide logistics, warranty services and program management to mid-market OEMs. In addition, Libra will supply new product development, low-volume manufacturing, and end-of-life support from the company’s US-based facilities. As a sales representative, Libra will market SMT (Holdings) Ltd. to large OEMs with direct purchasing capability…. ICP Electronics (Taipei, Taiwan), a publicly-held EMS provider listed on the Taiwan Stock Exchange, has entered into an alliance with Premio (City of Industry, CA) for North American markets. Premio builds its own family of products as well as offering its manufacturing facilities to EMS customers….Global Solutions (Spokane, WA), which offers design and manufacturing through a global network of providers, has formed a long-term relationship with EP Star, an EMS provider in Shenzhen, China. EP Star is a subsidiary of Australia-based Entech Group, a vertically integrated provider of printed circuits, graphics products and EMS.

San Diego, CA-based Kyocera Wireless Corp. (KWC), a Kyocera Group company that specializes in the design and sales of CDMA mobile handsets, has decided to outsource the manufacture and delivery of its products to Flextronics. During Flextronics’ analyst and investor meeting this month, company CEO Michael Marks described the Kyocera win as “about a billion-dollar piece of business.”

KWC will phase out its handset production in Tijuana, Mexico, and sell certain manufacturing equipment and inventory to Flextronics. The transfer of KWC’s manufacturing to Flextronics will take place in stages over the next three months.

This outsourcing deal covers all manufacturing of handsets designed by KWC, which account for a large majority of the mobile phone business of Japan’s Kyocera Corporation, the Kyocera Group’s parent. In total, the group produces about 13 million handsets a year worldwide. Although KWC would not disclose its handset volumes, a KWC spokesman did tell MMI that 10 million handsets a year is not out of line with what wireless industry analysts estimate for KWC. Historically, KWC has sold about 1 million mobile handsets per month, mainly in the Americas. The Kyocera Group forecasts mobile phone production of about 15 million units for its fiscal year ending March 2006.

By outsourcing to Flextronics, Kyocera aims to boost profits, as it reinforces its business by leveraging the efficiencies provided by Flextronics’ vertically integrated model, according to a statement from Kyocera. At the analyst and investor meeting, Flextronics COO Michael McNamara said there is the potential to provide such things as camera modules, PCBs, plastics and ODM phones.

Flextronics competed with other companies for the KWC business. The provider believes that its vertical offering gave it a compelling advantage.

KWC has used several contract manufacturers, including Flextronics, in the five years since KWC was founded. (The company was formed when Kyocera acquired QUALCOMM’s terrestrial handset division.) For example, KWC has worked with Flextronics and other contract manufacturers to produce phones for Brazil. McNamara described the past outsourcing from KWC as “an off-and-on kind of thing…highly tactical in nature.”

Kyocera is in the process of restructuring its mobile phone business, and the new outsourcing will enable KWC to focus on R&D, engineering, design, sales and marketing. Some 1700 jobs will be eliminated from the mobile-phone business in the US and Mexico, while between 150 and 200 jobs will be cut as a result of the outsourcing move. KWC’s Tijuana operation will remain open, producing other Kyocera products.

Besides Kyocera, Flextronics won another major Japanese account recently. The company expects that revenue from Japanese accounts will increase to $2.28 billion in fiscal 2006 from $927 million in the prior year.

The KWC win is a boon for Flextronics, which expects its core cell-phone business to drop by an estimated $800 million from fiscal 2005 to fiscal 2006.

More new programs…Redbox (Oak Brook, IL), a wholly-owned subsidiary of McDonald’s, has chosen Solectron as the exclusive worldwide manufacturer of Redbox’s automated DVD rental kiosks. Redbox plans to deploy 1,200 kiosks domestically this year….Taiwan’s Leadtek Research will place all of its graphics card production with Hon Hai Precision Industry (also known as Foxconn) this year, versus 40% in 2004, according to DigiTimes.com....Emulex (Costa Mesa, CA), a supplier of storage networking products, has added top-10 provider Venture Corporation (Singapore) to Emulex’s EMS supply base. Venture will manufacture and supply Emulex Fibre Channel switches and host bus adapters. The relationship with Venture enables Emulex to meet increased demand in the Asia Pacific region and to augment worldwide manufacturing as well….Among the 11 significant new manufacturing programs won by Plexus (Neenah, WI) in the March quarter were orders from GE Healthcare, Siemens Medical, Juniper Networks, AMX, Tellular and Honeywell….Under a new manufacturing agreement with StarBak Communications (Waltham, MA) , SMTC (Markham, Ont., Canada) will provide full system integration, configure to order, global end-customer distribution and after-sales support for StarBak’s complete line of integrated network video products….EMS provider NOTE (Norrtälje, Sweden) has inked a two-year agreement with Norway’s Network Electronics, and the program is valued at about 50 MSEK ($6.9 million). NOTE has also obtained a two-year contract from an existing customer, Dresser Wayne (Austin, TX), which makes petroleum dispensing equipment and retail automation systems.

More restructuring…Late last month, Solectron announced a new round of restructuring that will reduce its work force by about 3,500 employees, the majority of which are in non-US locations, and will consolidate about 850,000 ft2 of facilities in Europe and North America. This plan will result in charges estimated at $100 to $115 million….Under additional restructuring, PEMSTAR (Rochester, MN) will eliminate 100,000 ft2 from its San Jose, CA, facility, consolidate its Americas engineering team into a single unit, and reduce its domestic work force by 6%. The company is also reviewing options for its Mexico operation, which would likely involve a sale or downsizing. As a result, PEMSTAR expects to take a restructuring charge of about $14 to $18 million over the next two quarters.

Consolidation…Jabil Circuit is in the process of closing its Rocklin, CA, plant, one of three facilities that came with the acquisition of Varian’s electronics manufacturing business. According to Jabil, the plant closing was planned by Varian prior to the Jabil acquisition....CTS’s Electronics Manufacturing Solutions unit (Moorpark, CA) will consolidate its Marlborough, MA, operation into its Londonderry, NH, operation. The Marlborough operation was acquired in January as part of the purchase of SMTEK International.

People on the move…Celestica (Toronto, Canada) has hired Craig Muhlhauser as president and executive VP, worldwide sales and business development. Most recently, Muhlhauser was president and CEO of Exide Technologies, a major producer of lead acid batteries. Before that, he was VP of Ford Motor Company and president of Visteon Automotive Systems. Muhlhauser and Celestica CEO Steve Delaney worked together at Ford. In a related move, Marvin MaGee, Celestica’s former president and head of worldwide business development, has been named executive VP, worldwide operations. MaGee also held this position from October 1999 until February 2001….James Bass resigned this month from his position as president and CEO of Suntron (Phoenix, AZ). COO Michael Eblin also resigned at the same time. The company’s new president and CEO is Hargopal (Paul) Singh, who formerly served as VP of operations at Suntron’s largest facility located in Sugarland, TX. Before joining Suntron in 2004, Singh was executive VP of new business ventures at PEMSTAR….Erik Stenfors, CEO of NOTE (Norrtälje, Sweden), has reached an agreement with NOTE’s board to leave the company during 2005. Vice CEO Kjell-Åke Andersson assumes responsibility for the group. Stenfors said he made this decision in order to spend more time with his family.

Margins, or a lack thereof, have always been a nettlesome issue for the EMS industry. OEMs will only allow providers so much profit – and that’s in the good times. When end markets tank, as they did during the downturn, already thin margins evaporate. Although the financial deck is to some extent stacked against the EMS industry, many providers remain committed to improving their margins, especially in today’s uncertain market. One solution widely touted for margin expansion is ODM work. It is said that by controlling product design ODMs can build in more margin for themselves. But no business model is without flaws, and the ODM scheme is no exception.

ODM work is usually portrayed as a high-margin business. But some recent financial results dent this image. For the first nine months of last year, 11 ODMs combined for an operating margin of just 2.7% (Nov. 2004, p. 2 and 4). Price competition among ODMs, particularly in the laptop arena, has driven margins downward. In an effort to obtain better pricing, OEMs can play one ODM supplier against another where a market is mature and one design is basically as good as another. So the argument that ODMs can control their margins goes away in such cases.

Flextronics has found that the operating margins it had planned for its ODM cell-phone business will not work in the real world. In a recent interview with BusinessWeek, Flextronics CEO Michael Marks reported that companies are not willing to pay the 8% operating margin that Flextronics had thought it could get for the handsets it designed. He told BusinessWeek that instead these companies want to pay an assembly margin of 3% plus design costs.

Another attraction of the ODM business is that has grown much faster than the EMS industry has in recent years. And market forecasters are projecting that the ODM market will continue to do so by a margin of 5% or more. This delta may hold up, but the growth dynamics for the ODM side are somewhat different from those of the EMS market. When ODMs heavily penetrate a sector such as notebook computers, their overall growth in that sector largely depends on market demand for the product. Outsourcing becomes a secondary effect. As ODMs conquer other product areas, their growth will increasingly be subject to end market demand. If end markets go south again, ODMs could be more, not less, vulnerable than more diversified EMS providers.

If the ODM model were such a can’t-miss proposition, most EMS providers would be scrambling to adopt it. This is not happening. Top-tier providers have had plenty of time to adopt the ODM model, and only half of them are pursuing it.

Still, the ODM model is here to stay. MMI believes it will remain indispensable for PC and consumer products. How far the ODMs can migrate into other product areas is the big question. For unique designs, ODMs will likely enjoy a margin advantage. But for commodity designs, OEMs will ultimately control margins, just as they do on the EMS side.