![]()

![]()

In recent years, low-cost centers in Eastern Europe have taken their lumps from Asia in general and China in particular. China has become the heavyweight champion in the fight for high-volume outsourcing, especially in consumer products. Eastern Europe has lost to China significant amounts of business in areas such as cell phones and low-end printers. Is Eastern Europe then down for the count?

The answer is no, according to interviews with providers operating in Eastern Europe. EMS business in the region may not be booming overall, but there are pockets of growth. What’s more, providers are finding new opportunities that bode well for the region’s future as a destination for outsourcing.

Who is growing in Eastern Europe? Sanmina-SCI, for one. This year, the company has hired at least 900 people for its Hungarian operations, which now employ some 5,000 workers. Over the last couple of years, the provider has transferred business from Western Europe to Hungary and has also won new business for Hungary.

Sanmina-SCI manufactures xSeries servers and professional PCs for IBM plus notebooks and professional PCs for HP in Székesfehérvár. This operation ships about 200,000 to 250,000 systems a month, all for the European market. A site in Tatabanya does PCB assembly for the likes of Ericsson, Nokia and EchoStar and recently began supplying automotive electronics. Sanmina-SCI also maintains an enclosure operation in Miskolc.

Growth at a Hungary site of another provider has created the need for more space. In Szombathely, Jabil Circuit is adding a second, larger factory, which will provide 250,000 ft2 by August. Jabil needed the new space to accommodate its fast growing Global Services activity there as well as new EMS business in the works. This new plant shows that “Hungary, Poland, some other Eastern or new European countries are still offering growth possibilities,” said Jabil’s Michel Charriau, senior adviser – Europe. In Eastern Europe, the company also has a second site in Hungary as well as operations in Poland and Ukraine.

Of these possibilities, one is system integration. “You see a lot of systems integration business moving from Western Europe into Eastern Europe, and that’s mainly driven by logistics and duty benefits that you have today out of Hungary,” said Oliver Digel, Sanmina-SCI senior VP of business development for Europe and the Middle East (soon to be senior VP for the company’s automotive division worldwide). As far as duties go, a provider in Hungary, a new member of the EU, can operate as if the company were in the middle of Western Europe. The same is almost true for freight, Digel reported. Yet Hungary still offers labor costs that are below those in Western Europe. Sanmina-SCI sees a significant growth opportunity in system integration over the next 12 to 18 months.

The fast-growing market for flat-screen TVs and plasma display products is creating system integration opportunities in Eastern Europe where EU duties can be avoided. Taking advantage, Flextronics is assembling both types of products in Eastern Europe. In this case, some parts such as the panels are shipped from China.

Hungary’s entry into the EU has helped Sanmina-SCI’s set-top box business there. Before membership, there was a 40% duty on products shipped from Hungary with a TV tuner to the EU. This fee is going away, Digel reported.

For Hungary-based VIDEOTON Holding, the recent addition of Hungary, Poland and the Czech Republic to the EU has been a plus. “Since the EU enlargement, the net gain has been clearly positive,” said Ottó Sinkó, co-CEO of VIDEOTON. “We have experienced more migration [of work].”

Fulfillment of Asia-made products is emerging as another opportunity for Eastern Europe. Although there has been an exodus of consumer products from Europe to China, often they must be configured for European customers. “As these products migrate toward China, there will still be the need for fulfillment within the European region to meet these end market demands,” said James Rowan, the new president of Celestica, Europe. According to Rowan, cell phones and low-end printers are examples of products in this category.

Yet another area with growth potential revolves around customers with lower volume, higher mix products. “What we see in general terms is a real underpenetration of the EMS market for these sorts of customers,” said Herbert Schoeffmann, Flextronics VP of European sales. That’s why Flextronics has set up its Special Business Solutions Group to pursue this type of business, which the company believes will create demand in both Eastern and Western Europe. Flextronics sees the lower volume, higher mix segment as offering double-digit growth potential.

“Most of the low-hanging fruit has already been transferred from Western Europe to a lower cost site. Thus, the majority of topics [opportunities] arising today implies huge diversity,” said Péter Lakatos, co-CEO of VIDEO-TON. This diversity will require substantial indirect labor and overhead resources, he added. Lakatos believes Western European opinion and politics will be more sensitive about losing these higher-competence projects, and outsourcing them will require greater determination on the part of OEMs.

Looking to add new business in the face of Asia competition, the EMS industry in Eastern Europe is making changes. And not everybody has the same idea. Solectron is downsizing its Romanian operation and changing the mission there from high volume production to lower volumes, higher mix, and higher complexity along with engineering services. High volume work is being sent elsewhere, presumably to Asia.

Sanmina-SCI has decided to move some business out of Hungary into China. This is not a major move, said Digel, but it’s part of the trend to move low-end PCB assembly work into China and then supply those assemblies to Hungary for system integration.

Flextronics still has a high level of commitment to Hungary and Poland, according to Schoeffmann. “We don’t see any kind of overall weakening or softening of demand, which would lead us into situations of laying off people” in Eastern Europe, he said. In fact, the company is adding capacities related to high-end, high-mix products.

With the largest EMS capacity in Hungary outside of Flextronics, VIDEOTON does not need additional capacity to expand its business there. Instead, the company plans to expand primarily in technology competence. Although the number of employees in Hungary is decreasing to some degree, sales are increasing. VIDEOTON also operates a plant in Bulgaria, where labor costs are lower than in Hungary.

While Solectron is downsizing in Romania, Celestica is taking the opposite approach. The company recently opened a plant in Romania and is running limited production there. This Romanian site, designed for modular expansion, will serve as Celestica’s ultra-low-cost solution in the region. According to Celestica’s Rowan, the Romanian facility will complement the company’s operations in the Czech Republic. Evertiq, an Internet source, reported that Celestica will consolidate some work being done by company’s two sites in France into its Czech operations. Reportedly, the company intends to end manufacturing at the French sites.

Jabil Circuit is not only adding a factory in Hungary, but also plans to build its own plant in Ukraine, where the company currently leases space. The company sends products with high manual labor content and low transportation cost to Ukraine. Jabil’s Charriau estimates that direct labor in Ukraine costs around $1-plus an hour, compared with about $3.50 an hour in Hungary or Poland.

But the new Ukrainian government, which has changed policies for tax benefits and special economic zones, has not made things easy for Jabil. In an effort to fight corruption, the new government quickly did away with special economic zones, which were also being used for illicit purposes. Charriau expects that by July new legislation will be in place allowing Jabil’s operation in Ukraine to continue growing. The government’s action caused Jabil to delay plant construction by a few months.

Although Ukraine can compete with China’s labor rates, Ukraine lacks China’s network of suppliers. “It will take years to add local suppliers,” said Charriau. A local supply base is essential for any Eastern European country positioned as an ultra-low-cost solution on par with China.

At least two other providers are monitoring developments in Ukraine. Flextronics, which already has software engineering operations in Ukraine, is watching the country closely. For VIDEOTON, Ukraine is the next target for expansion.

Component suppliers will have much to do with determining whether or not countries such as Ukraine, Romania and Bulgaria will emerge as ultra-low cost centers for EMS. Meanwhile, established low-cost centers in Eastern Europe are finding new avenues for business development.

By Clive Jones, Managing Director of Economic Data Resources LLC

There is no shortage of information about the China operations of global EMS providers. Their role in the booming EMS business in China has been well chronicled. But indigenous Chinese providers of electronics manufacturing and design services often receive scant attention. Yet these domestic providers constitute a significant segment of the outsourcing business in China.

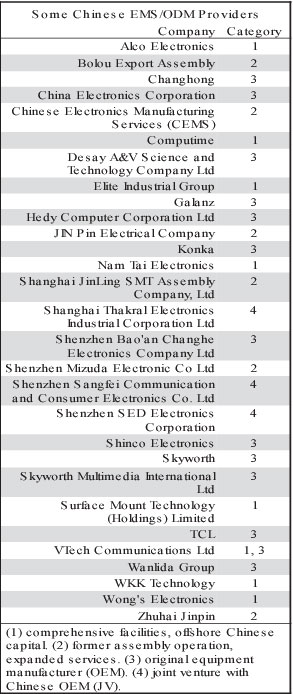

Research has identified 50 of the largest Chinese electronics manufacturing services and design providers generating total revenues of about $15 billion. When smaller operations are added in, the number of indigenous providers grows large. It is estimated that there are more than 1000 domestic outsourcing providers in China.

The 50 largest Chinese EMS/ODM providers fall into four major categories: (1) comprehensive manufacturing facilities in mainland China of Hong Kong-administered companies or other off-shore Chinese interests, (2) former assembly-only operations that began in mainland China and now offer a broader array of manufacturing services, (3) Chinese OEM subsidiaries providing manufacturing services (also called “OEM services”) and ODM capabilities, and (4) joint ventures with Chinese partners. (See table below.)

Generally, indigenous Chinese EMS/ODM providers are smaller than the global EMS players, but are rapidly adding design to their service offerings. These Chinese providers are concentrated near Hong Kong in the Pearl River Delta and around Shanghai in the Yangtze River Delta. The rapid growth of semiconductor and components production around Shanghai gives the Yangtze River Delta an edge in coming years as local sourcing becomes important. Currently, the Pearl River Delta boasts greater contract manufacturing employment, more than 85,000 in 2003 for Guangdong Province, according to Boy Lüthje of Hawaii’s East-West Center.

Product specialties include cell phones and lower-end telecom products, televisions and other audiovisual products such as DVD players, and computer peripherals.

Advantages of Chinese EMS/ODM providers include price, ability to service smaller size contracts, and the local Chinese company’s facility in dealing with Chinese customs. Disadvantages arise in ease of communication, quality control, and intellectual property (IP) protection. Some Chinese EMS/ODM companies attack the communications problem with US or European offices and/or sales persons and managers recently hired from Silicon Valley.

One of the largest Chinese companies providing manufacturing and design services is China Electronics Corporation (CEC), a conglomerate under the direct supervision of the Chinese government with more than $4 billion in 2004 revenues. CEC controls subsidiaries and share-holding companies in semiconductors, software and communications. Its Shenzhen Sangfei Communication and Consumer Electronics Company Ltd and Shenzhen SED Electronics Corporation provide EMS/ODM services in the handset and communications fields. CEC companies also produce military and dual-use goods.

Several of the most successful Chinese EMS/ODM providers have roots in Hong Kong and set up manufacturing operations on the mainland in the 1980s or 1990s. Companies such as Alco Electronics, Computime, Elite Industrial Group, Nam Tai Electronics, Surface Mount Technology (Holdings), WKK Technology, Wong’s Electronics, and VTech Communications are well known and have revenues in the range of $100 million to $1 billion. Nam Tai, which reported calendar year 2004 revenues of $533.7 million, is the largest of this group (March, p. 2-3).

Other Chinese EMS companies are less well-known. With 2004 revenues estimated at $225 million, JIN Pin Electrical Company Ltd Zhuhai S.E.Z. offers manufacturing and design services in televisions. The Wanlida Group, another conglomerate, produces DVD players, home theater systems, and, through a joint venture, medical electronics. Its 2004 exports were $114 million, according to Chinese Customs. Shenzhen Bao’an Changhe Electronics Company Ltd is a designer and manufacturer of corded phones and network equipment with an estimated $95 million in sales.

A few of the larger Chinese EMS companies, such as Kong Yue Electronics & Information Industry, are privately held (April, p. 3). Others began as state-owned enterprises, but now issue stock, often with a Chinese government agency as principal shareholder. Some, such as the Boluo Export Assembly with more than $100 million in electronics exports in 2004, remain state-owned enterprises.

Many Chinese contract manufacturers report revenues in the $10- to $60-million range. Often these were centers for consignment or semi-knocked down (SKD) and completely knocked down (CKD) assembly, and now offer PCB prototyping, mechanical assembly, insertion, testing, packout, and logistics. Shanghai JinLing SMT Assembly Company, Ltd boasts a gold list of clients including Philips, Matsushita, Mitsubishi, and Chinese giants such as Shanghai Bell. Servicing more than 50 OEMs worldwide, Shenzhen Mizuda Electronic Company Ltd specializes in VCD/DVD player design and manufacturing. Chinese Electronics Manufacturing Services (CEMS) is based in Hong Kong with American-based documentation, engineering, and program management. CEMS targets customers in the industrial, instrumentation and medical segments. According to Kevin Yan of the China Printed Circuit Board Association (CPCA), companies in this category came under pressure from global EMS providers and ODMs in 2004, triggering a scramble to add design services.

The boundaries between EMS and ODM operations and business activities of many Chinese electronics OEMs are fuzzy. Most Chinese electronics OEMs with revenues in the $100-million to $1-billion range perform manufacturing for other brands (also called “OEM services”) and offer design services, in addition to promoting their own brand. Examples include the Hedy Computer Corporation Ltd, one of the largest suppliers of PC peripherals in China, and Desay A&V Science and Technology Company Ltd, a manufacturer of home and car DVD players and home theater systems. Both companies report 2004 revenues in excess of $300 million, offer OEM and ODM services, and promote their own brand in local and Asian markets.

China also has several multibillion dollar OEMs offering design services focused around product families such as TVs, satellite/cable receivers, or cell phones. Examples include Changhong, Galanz, Konka, Shinco, Skyworth, and TCL. Skyworth Digital Technology Company Ltd, a subsidiary of the Skyworth Group, provides OEM and ODM services for digital TV set-top boxes and satellite/cable receivers. As much as one-third of Skyworth’s $4 billion-a-year television business is estimated to be ODM-based (Michael Liu, China-Outlook). Guohe Yang, president of Hong Kong Konka Ltd in charge of Konka’s exports and design operations, reports that EMS contributes 60% of Konka’s revenues from foreign sales of CRT TV sets.

Many Chinese JVs have significant exports, solicit contracts, provide services beyond assembly, and offer targeted design help, while promoting the brand of their OEM partner or even their own brand. Their share of China’s electronics exports has declined in recent years, because of relaxed rules for wholly foreign owned enterprises and acquisitions in China. There are many significant JVs, however, such as Shanghai Thakral Electronics Industrial Corporation Ltd, a JV between Shanghai and Singapore interests that manufactures DVDs and other audiovisual products for major Japanese and other OEMs.

JVs appear to be targets for acquisition by global EMS players. Two examples are Elcoteq’s acquisition of IBM’s holdings in Shenzhen GKI Electronics Company, Ltd and Beijing GKI Electronics Company, Ltd in late 2002.

Probably the biggest competitive threat to Chinese EMS/ODM providers is the vertical integration of global EMS services in large industrial parks in South China. These pressure smaller Chinese EMS operations. Fewer overflow contracts are available, provider lists are trimmed, and contracts are pushed farther up the supply chain. The backward- and forward-integration of services by global EMS companies also challenges Chinese OEMs, who reportedly have lost market share in the Chinese domestic cell phone market to global players, according to the United States Information Technology Office.

The strategic position of China’s indigenous EMS and ODM providers, therefore, depends on which segment a company is in: comprehensive manufacturing facilities, former assembly-only operations offering only a few extra services, subsidiaries of Chinese OEMs and joint ventures with Chinese partners. If the company’s position gives it access to both technology and financing, then it will likely enjoy more success in competing with the global EMS providers and ODMs.

Finally, the scale of electronics manufacturing and design services in China greatly exceeds estimates based on public data and other available information. Research from public records, company announcements and interviews identifies about $15 billion in Chinese EMS/ODM revenues for 2004. But China-based market researchers report an additional $30 billion or more in Chinese electronics manufacturing and design services for that year. These additional sales are embedded in broader operations of Chinese OEMs or in complex joint ventures or alliances.

For further information, contact Clive Jones at 408-694-3038; e-mail cjones@economicdataresources.com.

Having abandoned New England during earlier restructuring, Solectron (Milpitas, CA) will return to the region through the purchase of Teradyne’s printed circuit board assembly unit in North Reading, MA. In addition, Solectron has acquired ServiceSource Europe Limited (Warrington, UK), which focuses on providing outsourced inventory and logistics solutions for the supply and repair of electronic parts.

In the first deal, Solectron has entered into a definitive agreement to buy the Teradyne unit, which produces low-volume, high-mix (LVHM) boards for Teradyne’s semiconductor test products. Teradyne is already a Solectron customer. The provider is making this purchase through its FinePitch Technology unit, which will extend the unit’s NPI (new product introduction) and LVHM capabilities to the Boston area as a result.

Terms of the deal were not disclosed. The transaction, which Solectron does not consider material, is scheduled to close on June 17.

Solectron said it is focused on increasing sales in the area of NPI and LVHM and expanding its business with LVHM customers. The company will use the Teradyne operation as a means to serve the needs of other LVHM customers in the New England area.

“The timing was right for us to expand our NPI and LVHM capabilities to the East Coast, since it is something that our customers have been requesting. This new geography for FinePitch presents an excellent area of growth and [a] great opportunity for Solectron,” stated Doug Britt, Solectron’s executive VP of sales.

Solectron is promoting its FinePitch business as offering the flexibility and speed typical of smaller EMS companies along with the materials procurement leverage and global footprint of a tier-one EMS company.

As to the ServiceSource Europe acquisition, Solectron is presenting that deal as expanding its Global Services offering of after-market solutions for top-tier customers. Principal activities of ServiceSource Europe (SSE) are related to the movement of service spare parts around Europe. SSE offers service parts support from electronic parts brokering to full outsourcing of OEM warranty support. A key element of SSE’s offering is their ability to buy and sell electronic parts and systems in the open market.

Solectron said it will expand and leverage SSE capabilities beyond Europe.

“Demand for outsourced electronics after-market services continues to ramp at a fast pace. The market continually drives us to extend our capabilities to be the one-stop shop for services on a global scale. SSE’s knowledge, processes and speed in materials planning, warranty support, and parts brokering complement our offerings and align extremely well with our strategy to be a global full-service provider of after-market solutions,” stated Craig London, executive VP, strategy, marketing, Global Services, and corporate development.

SSE’s main area of focus is the PC market, according to the company website. Founded in 1987 under a different name, the company began as a broker of computer spares.

As in the first deal, terms of the SSE purchase were not revealed. Nor was the transaction deemed material.

PartnerTech (Malmö, Sweden), an MMI Top 50™ EMS provider listed on the Stockholm Stock Exchange, has signed an agreement to acquire all shares of KSH-Productor Oy, a Finnish contract manufacturer. The deal expands PartnerTech’s Nordic footprint to Finland and doubles the company’s sales in medical equipment.

With some 180 employees, KSH-Productor generated sales of about 22 million euros in 2004. The estimated purchase price is about 7 million euros plus an additional amount. PartnerTech will take over the Finnish operations right away, and the acquisition is expected to boost its EPS immediately.

Most of KSH-Productor’s programs are in medical technology. Among the references listed on its website are Elekta Neuromag Oy, Orion Diagnostica and Perkin-Elmer Life & Analytical Sciences.

KSH-Productor is based near Helsinki in Espoo, where the company operates development and production units. The company’s main plant in Espoo focuses on mechanics, assembly and associated testing, while a smaller plant does assembly. Development and manufacturing also take place in a plant located in the city of Åbo, where most production involves electronics, assembly and testing. KSH-Productor also has a smaller assembly and calibration unit in Åbo.

Mikael Jonson, PartnerTech’s CEO, describes the deal as a vital step in the company’s strategy of bringing its concept to more customers and markets. “Based on the advanced expertise available at the acquired units, we should soon be able to offer all PartnerTech services to both existing and prospective customers in a number of business sectors in Finland,” said Jonson.

PartnerTech will pay half of the purchase in cash and finance the other half by issuing new shares based on their average price for a ten-day period. The company is buying KSH-Productor from its two managers of operations and from Bio Fund Management, a European venture capital firm.

In addition to the facilities being acquired in Finland, PartnerTech operates four plants in Sweden, two in Poland, and one in the US (Atlanta, GA). Offering contract development and manufacturing, the provider serves companies primarily in telecom, IT, the engineering sector and medical technology. Sales in 2004 were $235.8 million (March, p. 3).

In a move to add RF design capabilities, Flextronics (Singapore) has told MMI that the company is acquiring Wavebreaker (Norrköping, Sweden), a developer of silicon IP for emerging wireless systems. Flextronics confirmed that the deal will strengthen its capabilities in radio development of communication systems for 3G, WLAN, and WiMAX.

Wavebreaker provides IP-based design services with a focus on multiple-channel RF transceivers and MIMO signal processing ASICs. The firm also offers a radio development platform and licensing of wireless IP.

Flextronics has signed separate agreements for the sale of Flextronics Network Services (FNS) and Flextronics Semiconductor. Previously, the company had announced its intention to divest both businesses and to merge FNS with Talvie AS, wholly-owned by Altor 2003 Fund, a Nordic private equity firm (May, p. 4). Now Flextronics has agreed to sell its semiconductor business to AMIS Holdings, parent company of AMI Semiconductor (Pocatello, ID), for an unspecified amount of cash.

As a result of these two transactions, Flextronics will receive cash totaling more than $550 million plus additional deferred and contingent payments and a 30% stake in the merged network services company. Subject to customary closing conditions, both transactions are expected to close before the end of the September quarter.

For the record…Flextronics and Nortel have delayed the closing of the balance of the outsourcing transaction between the two companies. Flextronics was originally scheduled to take over Nortel operations in Chateaudun, France; Calgary, Canada; and Monks-town, Northern Ireland, in the first half of 2005. Nortel now plans to transfer these operations by the end of Q1 2006.

Preco Electronics (Boise, ID), a maker of vehicle communication products, has sold its EMS operation in Morton, IL, to Vansco Electronics LP (Winnipeg, Manitoba, Canada), which provides electronics primarily for the heavy equipment industry.

Employing about 230 people, the Morton Division specializes in building ruggedized electronics. Among its largest customers is Caterpillar (Peoria, IL). With SMT, PHT and box build capability, the Morton facility runs production characterized by low to medium volumes, high mix and complex assembly.

Vansco portrayed the deal as expanding its capacity to provide advanced electronics design and manufacturing services in North America. The acquisition supports the company’s plans for continued growth, both geographically and in product offering. Vansco said the Morton operation has the potential to be expanded with the addition of Vansco standard products and design services. The Morton operation will gain product development capabilities from Vansco.

In explaining Vansco’s strategy for making this deal, John Lion, Vansco VP of sales and marketing, said the Morton operation is a very good manufacturing facility centrally located where potential customers and some existing ones are. In addition, the Morton facility is certified to automotive quality standard ISO/TS 16949, “something some of our customers are asking for,” he said. Some potential customers are also requesting it.

Vansco expects to offer employment to all personnel at the Morton facility and plans to grow the work force as it brings in additional business.

Offering both off-the-shelf products and custom designs, Vansco specializes in the design and manufacture of electronic, electro-mechanical, and electro-hydraulic controls and instrumentation. An estimated 80% of Vansco’s existing business is custom. In addition to the Morton location, the company manufactures at two other sites – Winnipeg, Canada, and Valley City, ND.

With the Morton acquisition, Vansco will expand its work force to around 970 employees. Its run rate will increase from about C$110 million to about C$170 million, or about US$136 million.

Last year, Vansco was acquired by Kilmer Capital Partners and Borealis Private Equity.

Lincoln Partners (Chicago, IL), an investment bank, initiated the Morton transaction and served as financial advisor to Preco in this sale.

Preco established the Morton Division in 1986 to provide EMS.

Consolidation among EMS players is becoming a global trend as exemplified by the proposed merger of two Asia-based providers. Integrated Microelectronics, Inc., or IMI (Laguna, Philippines), has entered into a conditional merger agreement with Speedy-Tech Electronics Ltd., or STEL (Singapore), an EMS company publicly listed in Singapore. The merger will give IMI, whose manufacturing facilities are located in the Philippines, a presence in China, where STEL operates three facilities – two in Shenzhen and one in Jiaxing. STEL also has a plant in Singapore and one in the Philippines.

Under the terms of the proposed merger, IMI will acquire all outstanding shares of STEL for a total consideration of S$201 million, or about US$120 million. STEL shareholders can accept cash, new IMI shares, or a combination of the two. Upon completion of the transaction, which will be subject to shareholder and regulatory approvals, STEL will become a wholly-owned subsidiary of IMI and will be delisted from the Singapore stock exchange.

STEL is the larger of the two companies by 2004 sales. For last year, STEL reported a net profit of S$16.1 million on sales of S$248.3 million. Sales were up 68% over 2003. Q1 2005 sales increased 38% year over year to S$66.1 million; net profit for the quarter went up 7% to S$3.6 million.

If combined, the 2004 sales of the two companies would total some S$436 million, or about US$261 million at current exchange rates.

The two providers listed several benefits of the merger. First, the greater scale of the combined company will achieve cost savings through integration of operational functions and consolidation of purchasing volumes. Increased scale may also lead to larger contracts. Second, the merged entity will broaden its geographic presence, with IMI gaining a foothold in China. According to IMI, STEL will benefit from IMI’s experience and engineering resources in the Philippines and in the US. (IMI operates a design center in Tustin, CA.) In addition, the merged group will have a more diversified customer base. IMI’s customers are largely Japanese multinationals, while STEL’s come from China, the US, Europe and Singapore. According to the two companies, there is minimal customer overlap between them.

Cross-selling opportunities are also anticipated. STEL will be able to offer its customers full design and software engineering services through IMI’s EAZIX subsidiary as well as plastic injection and metal stamping capabilities. Likewise, IMI customers will have access to STEL’s competencies as a power electronics ODM.

“Our goal is to become a strong tier-two global EMS player, and expanding both our product competencies and geographical footprint is critical to our success. We felt that it was especially important to have a China presence in order to provide our customers with a broader range of customized solutions for their engineering and manufacturing needs,” stated Arthur Tan, president and CEO of IMI.

The merger is expected to be completed in Q4.

Established in 1985, STEL was listed on the Singapore Exchange in January 2004. Among STEL’s clients are its top customer Canon, Dentsply, EBM-Papst, Emerson Network Power, Fiberxon, Guest, HP, Huawei Technologies, Hypercom, LG Electronics, NEC, Nippon Antenna, Printronix, Shimadzu, and Videojet Technologies.

IMI was recently identified here as one of seven providers emerging above $100 million in sales (April, p. 3). The provider is 79% owned by Ayala Corporation, a large conglomerate in the Philippines.

Deal done…Fabrinet (Bangkok, Thailand) has completed its acquisition of three JDS Uniphase manufacturing sites, one each in Mountain Lakes and Ewing, NJ, and a third in Fuzhou, China (May, p. 5). The Fuzhou operation will retain the name Casix and continue to manufacture primarily crystals and precision optics for Fabrinet’s internal consumption and external customers. Plans are to consolidate the New Jersey sites into one location specializing in standard and synthetic glass products for optical communications, medical and industrial markets.

New programs…More Energy Ltd., a subsidiary of Medis Technologies Ltd., has signed a design and engineering agreement with Celestica (Toronto, Canada). Under the agreement, Celestica will design a semi-automated production line that will be used to produce Medis’ fuel cell Power Packs. Celestica has also been named the EMS partner of choice for future manufacture of the products....With production in China, Nam Tai Electronics (Tortola, British Virgin Islands) has landed an order from Sweden’s Anoto Group AB to manufacture scanner pens. Anoto is a new customer….TOMRA (Asker, Norway), a developer of systems for returning beverage cans, has selected PartnerTech (Malmö, Sweden) to handle production, assembly and distribution for TOMRA’s new reverse vending machine. Covering one product initially, the agreement will potentially boost PartnerTech’s revenue by more than SEK 200 million (about $27 million) over three years….Publicly-held Incap (Kempele, Finland) and the Assa Abloy Group have signed a new agreement that gives Incap the status of global supplier to the Assa Abloy Group. Having been a supplier to Abloy Oy for about 20 years, Incap is now an approved supplier for other companies in the Assa Abloy Group. The first product to be supplied under the new agreement is a programming device for electronic lock systems, the newest version of which has been redesigned by Incap in cooperation with Solid AB. Incap is aiming for sales growth primarily through deeper relationships with strategic customers....Formation (Moorestown, NJ) has received a $4-million contract from Panasonic Transportation Systems to manufacture 660 digital communication systems for a subway car program in New York City…. LaBarge (St. Louis, MO) has landed a $1.2-million contract from O-I to manufacture inspection machines that detect flaws in glass containers.

Military contracts…DRS Technologies has received about $50 million in new orders to provide production, spares and engineering services for US Navy display workstations. DRS Laurel Technologies (Johnstown, PA), a unit of DRS, will handle manufacturing. The contracts came from Lockheed Martin Maritime Systems & Sensors Tactical Systems (Eagan MN)….Boeing has awarded LaBarge a contract to provide engineering support and manufacturing services for an unmanned combat air system developed by Boeing. The contract is expected to exceed $1 million. Also, LaBarge has secured a multiyear contract from Raytheon Missile Systems to provide cables and harnesses for a GPS-based glide weapon launched from US Navy aircraft. The contract has a total estimated value of about $24 million from 2005 to 2012.

People on the move…Celestica has appointed James Rowan as president of Celestica, Europe. He had been VP, European operations at Flextronics for five years....Solectron has named Michael Busselen VP of corporate communications and public relations. He joins the company from Fleishman-Hillard, where he most recently was a senior partner and GM of the San Diego office….Nortech Systems (Wayzata, MN) has appointed Curtis Steichen to the new position of VP sales and marketing. Previously, he held both North American and international sales and marketing assignments with Graco (Minneapolis, MN), a manufacturer of fluid-handling systems and components….Vanguard EMS (Beaverton, OR) has promoted Chris Smith to senior director of sales. In this role, he will lead the company’s sales and marketing organization.....James Jurgens has resigned from his position as interim CFO of Three Five Systems, or TFS (Tempe, AZ), for health-related reasons. Also, Carl Young, a managing director and founding member of Bridge Associates, will act as TFS’s chief restructuring officer. TFS has retained Bridge to assist in restructuring.