![]()

Cover Story

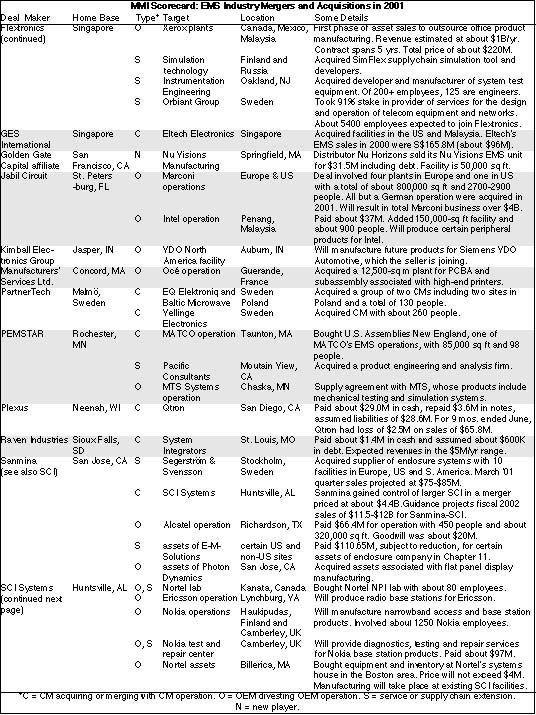

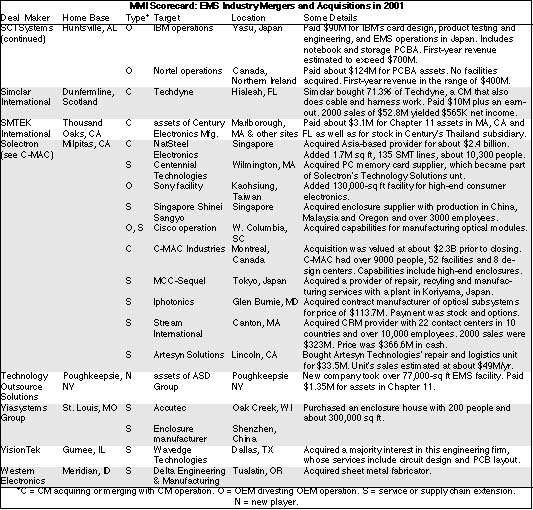

MMI Scorecard: EMS Industry Mergers and Acquisitions in 2001

EMS Industry Alliances and Equity Partnerships in 2001

News

Solectron in Talks with Lucent

After hitting an all-time high in 2000, M&A activity in the EMS industry took a nose dive last year. MMI's annual Scorecard of industry mergers and acquisitions lists a total of 75 deals closed in 2001, down 32% from 111 transactions in 2000. Indeed, 2001 was the first year that the number of M&A deals decreased since MMI started keeping track of them in 1994 (see graph). Last year's deal-making fell off so much that it sank below the M&A activity in 1998.

Although the downturn in end markets may not have been solely responsible for this drop in M&A deals, the downturn certainly exerted a chilling effect on M&A activity. Burdened with overcapacity, EMS providers were more selective about acquiring additional operations either from OEMs or other providers. On the OEM side, the deal pipeline did not produce as many deals as one might have expected. Some deals were pulled and others were delayed as OEMs struggled with their own restructuring problems. Furthermore, the downturn made financing acquisitions more difficult, as stock deals became less attractive and some providers looked to conserve their cash.

As in past years, MMI has used basically the same system for classifying deals in the MMI Scorecard below. Once again, acquisitions of divested OEM assets were the most popular type of deal done in 2001. OEM divestitures usually involve the acquisition of manufacturing assets, but OEMs may also sell other assets.

These OEM divestitures (designated "O" in the Scorecard) totaled 32 last year, compared with 44 such deals in 2000. So the number of OEM asset deals declined by 27% in 2001. Although 2001 was down in absolute numbers, the year saw more megadeals involving multiple sites and annual revenues near or exceeding $1 billion. There were four of these transactions last year versus two the year before.

In the second deal category, one EMS provider acquires a competitor or some assets from another provider (designated "C" in the Scorecard). This activity, which dates back at least a decade, had been increasing in recent years - until 2001, that is (see chart below). For 2001, MMI identified 17 acquisitions of EMS operations, down 47% from 32 in 2000. As mentioned above, overcapacity worked against such deals.

Another type of deal (designated "S") occurs when an EMS provider acquires an operation to broaden its service capabilities or create a more vertically integrated supply chain. Typical capabilities that can be added or enhanced include product engineering on the front end and repair services on the back end. This activity continued in 2001. But 2001 also marked the emergence of optical acquisitions, of which there were four. Sometimes a provider will carve out a services niche through acquisition. For example, Flextronics and Solectron are doing this in network and CRM (customer relationship management) services respectively, as shown in the Scorecard.

Providers also made acquisitions for supply-chain integration in memory cards, cables, plastics and enclosures.

In 2001, providers acquired 24 firms that added service capabilities or supply-chain integration. In addition, OEMs divested four operations that gave providers enhanced capabilities.

Although 2001 was a tough year, it did not dissuade some companies from entering the EMS industry. Three new EMS players (designed "N") emerged last year, two from the sale of EMS assets and one from an OEM divestiture. These compare with five new players in 2000.

One type of deal made in 2000 disappeared last year. There were no acquisitions of EMS operations from OEMs. In 2000, seven such deals were closed. While OEM withdrawals from the EMS business seemed to end last year, the saga of OEMs in contract manufacturing is not over. Philips re-entered the EMS business last year (Dec. 01, p. 8), and other OEMs such as Sanyo and Siemens continue to maintain EMS operations.

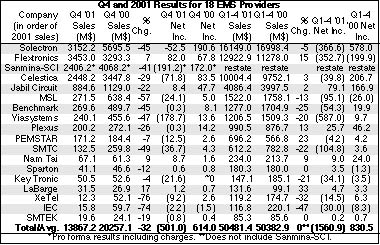

Who was the most active deal maker in 2001? Flextronics, Solectron together with C-MAC, and the Sanmina-SCI combination formed a three-way tie with 12 deals apiece. The previous year's high by a single provider was 24 deals, made by Flextronics.

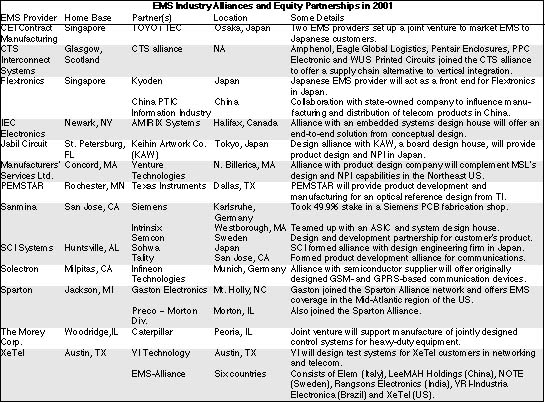

While the downturn put a damper on deal-making, it didn't hold back the formation of alliances and ventures in 2001 (see table above). In fact, this activity increased in 2001 when 18 alliances and equity partnerships were either formed or added to. The previous year, 16 comparable partnerships were made (including a Nam Tai Electronics investment that was not listed).

Alliances have become an increasingly popular way to supplement a provider's design capabilities. Of the 18 alliances and ventures listed for 2001, ten were design-related. Alliances can also be formed for geographic reasons. Four EMS providers entered into alliances to penetrate the Japanese market. Three additional partnerships also give providers greater geographic coverage.

Solectron (Milpitas, CA) is negotiating with Lucent Technologies to purchase specialized equipment and usable inventory from Lucent's North Andover, MA facility for about $275 million in cash. As part of this deal, Solectron would get a multiyear contract to provide supply-chain services for certain Lucent optical networking products. The provider confirmed it is in talks with Lucent after union officials disclosed in press reports that discussions were taking place.

According to a statement from Solectron, the company is negotiating to buy equipment and inventory. There was no mention of purchasing the North Andover facility, which spans about 1.95 million ft2. Lucent has been exploring ways to divest a portion of the optical plant's manufacturing operations and put the rest in a system integration center (Aug. '01, p. 6-7). The company plans to outsource the manufacture of certain of its optical product lines.

The facility currently employs 2700 people, about 400 of which had already accepted a voluntary offer last fall and are staying on at the company's request until March 31. Lucent recently announced that an additional 800 facility employees will be separated by the end of March. Some people in this group will join the EMS provider that buys the assets, according to Lucent.

Of about 1500 employees remaining with Lucent, several hundred - Lucent estimates 400 to 600 - will be part of the system integration center. Lucent has not specified the location of the center, but it will be in the area.

To ensure the continuity of supply and facilitate the transfer of employees, Lucent wants the EMS buyer to have a location within the area.

The parties have not reached agreement on the prospective contract, and Solectron said there is no guarantee that a deal will be struck. One of the matters to be settled is a labor agreement for the unionized Lucent employees that would be transferred. Solectron is in talks with the Communications Workers of America, which represents hourly workers at the North Andover facility.

In August when Lucent told MMI of its plan to divest operations at North Andover, employment stood at about 4000, and the number of affected employees was far greater - 1600 to 1800.

Meanwhile, Lucent has also been talking with Solectron about shifting work from Lucent's plant in Nuremberg, Germany, to a contract manufacturer. The plant's products include wireless base stations. Lucent had targeted this plant for outsourcing last year (Aug. '01, p. 7).

Sanmina-SCI (San Jose, CA) intends to acquire Alcatel's manufacturing facilities in Cherbourg, France; Gunzenhausen, Germany; and Toledo, Spain. As part of this deal, Sanmina-SCI will get a four-year supply agreement worth more than $1.3 billion in total revenue.

The three plants enclose a total of about one million ft2, and about 1500 employees at these sites will join Sanmina-SCI. The Cherbourg facility produces point-to-point microwave systems, allowing Sanmina-SCI to offer full system integration and test services in Europe for RF and microwave products. The Gunzenhausen plant, which manufactures high-end voice switching and data transmission systems for central office applications, will become Sanmina-SCI's first EMS operation in Germany. Finally, the Toledo facility produces wireline access products.

"We view this transaction as a major extension of our already broad relationship with Alcatel, and we look forward to future outsourcing opportunities with Alcatel," said Randy Furr, Sanmina-SCI president and COO, in a conference call with analysts.

The company stated that these facilities, which are located close to key European markets, will accelerate its effort in international business development. The acquisition will also broaden Sanmina-SCI's manufacturing capabilities, especially in final system build and test, and will give the provider European Centers of Excellence in wireline access and RF microwave products.

The asset purchase of each facility will close separately. Sanmina-SCI expects the Gunzenhausen and Cherbourg transactions to close in its fiscal Q2 and the Toledo purchase to close in fiscal Q4. Completion is subject to regulatory approvals in the US and Europe and to consultation with workers councils in each location. Financial terms such as the purchase price were not disclosed.

Sanmina-SCI expects the deal will be just above a break-even point in fiscal 2002, about one cent accretive in fiscal 2003 and two cents accretive in fiscal 2004.

Last month, Sanmina-SCI was also identified as the buyer for a Hewlett-Packard PC manufacturing operation in Isle d'Abeau, France, near Lyon (Jan., p. 4-5). More recently, the provider released some information about this deal. Having reached a tentative agreement with HP, Sanmina-SCI expects to take over the French manufacturing site and add 450 full-time employees from HP. As part of this deal, Sanmina-SCI will receive a three-year supply agreement and expects the transaction to generate more than $3 billion in revenue over the three years. The provider estimates the deal will be about one cent accretive in fiscal 2002 and two cents accretive in fiscal 2003.

This acquisition is an extension of Sanmina-SCI's business with HP as the provider already services HP for the North American and European market for desktop PCs.

What's more, Sanmina-SCI quietly acquired Davos Group, a privately-held designer and manufacturer of complex enclosure systems, for about $14.7 million in cash. The acquisition took place in January and includes a manufacturing facility in Shenzhen, China, and a sales office in Hong Kong.

While the new OEM deals are creating positive buzz, some other business is requiring corrective action. Sanmina-SCI has discovered five to ten existing programs that are causing losses. Sanmina-SCI's Randy Furr told analysts, "We're going to remedy or discontinue unprofitable programs. This will mean a reduction in top-line revenue of approximately $200 million per quarter as a result of these cancellations." According to the company, none of these programs are in the PC space, and most center around prior transactions with OEMs.

Sanmina-SCI attributed these losses to pricing problems resulting from recently committed cost reductions, the inability to hit production rates anticipated in quotations, and costing errors.

"We are reviewing the pricing of some of the programs that have been booked there. And there are certain businesses where we are either going to get the prices that we want or we're going to walk away from [them]," said Jure Sola, chairman and CEO of Sanmina-SCI, during the conference call.

The company also disclosed that the former SCI operations in Europe and Latin America are losing money. "We have to fix that. I do believe that is fixable," said Sola.

Another issue that surfaced was some unrealistic forecasting in new program wins for fiscal Q2.

Sanmina-SCI listed a number of actions to fix post-merger problems. Program repricing or cancellation is one step. Other actions are to transfer some low-margin programs from Mexico to China, accelerate the closure of certain facilities, conduct a detailed cost review of all major programs, adopt financial reporting and forecasting systems used by Sanmina, aggressively implement an ERP system, and cut costs further.

Deal done...This month, Celestica (Toronto, Canada) completed its acquisition of Cisco assets in Salem, NH (Dec. '01, p. 1).

New programs...Solectron has won the repair contract for Microsoft Xbox game consoles that will be sold in Japan. The provider is also exploring options for the Australian market. Solectron already handles Xbox repair in North America....Tellium (Oceanport, NJ) has selected Jabil Circuit (St. Petersburg, FL) to provide EMS for board assemblies and subassemblies used in Tellium's family of core optical switches....Elcoteq (Espoo, Finland) will manufacture corded system terminals for Ascom Enterprise Communications, a division of the Swiss high-tech company Ascom. This box build program will be carried out in Pécs, Hungary, starting in the summer. Elcoteq has also landed a program to manufacture the electronics for a new generation of KONE elevators. Elcoteq serves as KONE's preferred electronics supplier....MSL (Manufacturers' Services Ltd. of Concord, MA) has won a PCB assembly contract for Samsung's new flat screen technology....Plexus (Neenah, WI) has landed a program from GE, an existing customer, for full system build of a new ultrasound platform....The Taunton, MA facility of PEMSTAR (Rochester, MN) is providing engineering and turnkey manufacturing services for multi-networked media servers from ThinkEngine Networks (Marlborough, MA). Also, PEMSTAR has announced two more new customers - LGC Wireless (San Jose, CA), a supplier of wireless networking systems, and Welch Allyn (Skaneateles, NY), which sells medical, data collection and lighting products. Another new program involves a Seagate data storage product....According to Reuters, CEI Contract Manufacturing Ltd. (Singapore) has received a three-year contract from PerkinElmer Instruments (Boston, MA), an existing customer. CEI will act as sole supplier of PCB assemblies to PKI, a maker of analytical instruments.

National security contracts...Sypris Electronics (Tampa, FL), a subsidiary of Sypris Solutions, has been awarded a three-year contract to manufacture trunk encryption devices for the National Security Agency. The initial order is valued at $4.0 million, and NSA has options that would increase the contract value to $22 million....LaBarge (St. Louis, MO) has received contracts worth a total of $10.5 million to produce airport security equipment for PerkinElmer Detection Systems, a division of Perkin-Elmer Instruments. In addition to producing electronic and box-level assemblies, LaBarge will integrate these assemblies into higher level electronic equipment for an inspection system that uses X-rays to detect the presence of explosive materials, weapons or other contraband.

People on the move... Antti Piippo, founder and principal shareholder of Elcoteq, will not stand for re-election to the company's board at its annual meeting in March. Piippo temporarily stepped down as company chairman last year following an incident at his summer house (Sept. '01, p. 7). Recently, he was informed that he would face assault charges stemming from the incident. Piippo will not consider standing for election until this matter is settled. He has said he will not reduce his holding in Elcoteq, which gives him voting power of 44.67%. Also, Lasse Kurkilahti became president and CEO of Elcoteq as of December 1, 2001. Kurkilahti had been managing director and CEO at Nokian Tyres and Raisio Group. He replaced Hannu Bergholm, who had served as interim president following the unexplained resignation of Tuomo Lahdesmaki in the summer of 2001....Susan Wang, long-time senior executive and former CFO at Solectron, intends to retire after 18 years with the company. As executive VP of corporate development, Wang oversees the company's business development and M&A activity. Her business development duties will pass to CFO Kiran Patel. ....MSL has hired Santosh Rao as COO. Rao comes from Sanmina-SCI, where recently he was named executive VP of Asia Pacific operations (Jan., p. 7). He has also worked for Solectron and IBM. In addition, Bruce Leasure has joined MSL as senior VP of worldwide marketing and sales. Most recently, Leasure served as corporate VP of marketing and sales at SCI Systems, prior to its merger with Sanmina. Before SCI, he held executive positions with Solectron, WorldPartners Company and AT&T. Both Leasure and Rao worked with MSL's new CEO and president, Robert Bradshaw, at SCI. Bradshaw has also been appointed to MSL's board.