![]()

Cover story

Researchers Agree on Long-Term Growth

Market Focus

Industrial Segment Draws Attention

Design

Celestica Unveils Workstation Design

Sanmina-SCI To Buy Server Developer

News

MSL To Gain Assets and Business from Ingenico

More news on the technology side

Solectron Said To Be Preparing To Divest

Last Word

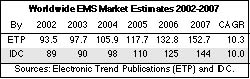

Two market research firms have come up with nearly identical five-year growth rates for the global EMS industry. Electronic Trend Publications, or ETP (San Jose, CA), and IDC (Framingham, MA) are forecasting that the industry's compound annual growth rate from 2002 to 2007 will be at or slightly over 10% (table). This is a far cry from the industry's boom years when long-term CAGR projections were often well above 20%. Despite a still largely untapped market for outsourcing, a more conservative outlook has taken hold after two straight years of EMS market decline.

ETP has just published its EMS market forecast in the tenth edition of its report, The Worldwide Contract Electronics Manufacturing Services Market. The ETP report is projecting modest growth of 4.4% for the 2003 EMS market, which will reach $97.7 billion. In contrast, IDC's forecast presented here last month calls for a flat 2003 and a somewhat smaller EMS market size (table).

The ETP report sees most of 2003 growth occurring in the second half as first-half results look weak. In 2004, market growth should increase to 8.4%, predicts ETP, followed by successively higher percentage increases in subsequent years through 2007. Next year, the EMS business will break the $100-billion barrier and reach $105.9 billion, according to the ETP forecast. Growth in 2005 is expected to increase to 11.2%, resulting in a $117.7-billion market. Projected annual growth will rise to 12.9% in 2006 and 15.0% in 2007, and the EMS market will exit 2007 at $152.7 billion.

Interestingly, ETP calculates that the top ten EMS providers have lost market share from 2000 to 2002. In 2000, they accounted for 65.6% of industry sales, according to the ETP report. The top-ten share then declined to 64.6% in 2001 and 63.6% in 2002. The report states, "Based on this trend, it seems reasonable to conclude that a growing percentage of business is being captured by mid- and lower-tier CMs, which have experienced more steady growth than large CMs, reflecting perhaps a preference by the market to move away from first-tier suppliers in favor of local suppliers."

While these calculated results may indicate an unexpected trend, it's no surprise ETP is forecasting that Asia will continue to pick up EMS market share. Asia's piece of the EMS pie will increase from 28% in 2002 to an industry-leading 37% in 2007. The North American share of the market will decline from 41% in 2002 to 34% in 2007, predicts ETP, and Europe's percentage will decline from 29% to 27% over the forecast period.

ETP estimates that the Asian region accounted for a 33% increase in EMS revenues last year as the industry underwent massive restructuring and a shifting of production to low-cost operations in Asia, particularly China. The report foresees that this transfer of outsourcing to Asia will continue in the future, but at a slower rate.

Based on ETP's forecast, the EMS industry will not lose its heavy dependence on the communications and computer/peripherals segments. Together, the two segments will account for 75% of the EMS market in 2007, just as they did in 2002. Communications, which represented 40% of the EMS market in 2002, will also finish up at 40% in 2007, says ETP. The computer/peripherals sector will start and end the forecast period at 35%.

Consumer products at 6% of the 2002 market, industrial equipment at 7% in 2002, and medical products at 6% are expected to remain roughly at parity. ETP foresees some of the highest growth rates occurring within the automotive sector, followed closely by growth rates for medical products.

To rank EMS providers, the report uses a performance rating based on a weighting of financial metrics. In 2002, Benchmark Electronics received the highest rating, followed by Elcoteq.

For more on the ETP report, go to www.electronictrendpubs.com.

You know an EMS segment has arrived when the CEO of the second largest EMS provider singles it out during an investor conference. That happened to the industrial segment in April when Solectron's president and CEO, Mike Cannon, declared, "The EMS industry has not had significant penetration in the industrial market. I think there's tremendous opportunity for that."

Based on the latest figures from one market research firm, EMS penetration of the industrial segment is below average for the EMS market as a whole. Electronic Trend Publications (San Jose, CA) estimates a 12.8% penetration of the available industrial assembly value. ETP puts EMS sales in the industrial segment at $6.8 billion out of $52.8 billion in total available market for industrial assembly in 2002. According to ETP, the least penetrated subsegment of the industrial market was control/processing at 7.0%.

Industrial electronics becomes another segment - along with consumer products, medical equipment, automotive and military/aerospace - with the potential for portfolio diversification. The question is: Can the industrial market yield lots of new business for all the EMS tiers?

Despite Solectron's putative push in the industrial market, there are reasons why tier-one providers have not listed the industrial segment in sales breakdowns. The segment is fragmented, and industrial programs generally do not yield big revenue numbers.

But industrial business can and does drive growth at smaller EMS providers that cater to the segment. One of them is TotalEMS of Logansport, IN, a provider with a run rate of about $30 million. After taking over a preexisting operation a little over a year ago, TotalEMS has sales growing at more than a 25% rate. "A lot of that has to do with the markets that we're going after, the markets that we serve," said John Yerger, president of TotalEMS. The industrial segment is a major part of this growth because it's the company's main focus. Indeed, some 2/3 of the more than five customers that TotalEMS has added since its launch have come from the industrial market, which the company broadly defines as nonconsumer products in applications other than computers and communications.

Canada's Creation Technologies, based in Vancouver, British Columbia, considers industrial controls a growth market for a company its size. "There's enough growth opportunity in the industrial controls market just from organic growth," said Dave Pettigrew, executive VP of business development for Creation. Out of 13 customers that the company added in the last 12 months, five were industrial. Creation expects that the industrial portion of its sales will increase from about 22% of total revenue to 26-28% in fiscal 2004 ending in May.

At MEC, headquartered in Milwaukee, WI, an estimated 80% of sales comes from industrial business, which includes automotive customers that the company considers part of this business. Industrial sales have not disappointed the company, which has plants in Milwaukee, WI; Milwaukie, OR; and Tecate, Mexico. "Our industrial business has grown each of the last two years during this recessionary time," said Michael Stoehr, president of MEC. Not only has MEC added a number of industrial customers, but established customers have upgraded products during the downturn to gain a leg up on the competition.

But to expect a booming business from the industrial segment may be asking too much, especially as EMS company size goes up. Just ask Plexus. "I don't know that it has been a boom sector for us. But it's been a steady sector," said Kristian Talvitie, Plexus director of strategic marketing and communications.

Does the industrial segment make sense for the largest providers? Industrial customers "don't fit the really huge tier-one, tier-two companies in general because they don't have the volume for them," said Yerger of TotalEMS. Randall Sherman, president of New Venture Research (Nevada City, CA) and an author of ETP's EMS report, finds only superficial market share among top-tier EMS providers in the industrial segment. "This means the majority of outsourced assembly is being done by second- and third-tier EMS companies since this [activity] often involved low-volume, high-mix assemblies," said Sherman.

Nevertheless, there is interest in the industrial market among top-tier providers. The foregoing statement by Solectron's CEO is one indication. Here is another. "We've had two or three engineering opportunities where tier ones have actually bid on projects," said MEC's Stoehr. This had never happened before at MEC. The bidding involved large industrial customers, not mid-sized or smaller ones.

Indeed, performing design work for an industrial customer can lead to winning a manufacturing program. For example, Plexus is incorporating Transmeta's TM5800 processor in Plexus' design of two industrial controllers - one for the printing industry and the other for the heavy-duty white goods industry. The first controller is scheduled for production this year. Plexus is also looking at using the energy-efficient processor in industrial communications.

Industrial customers often display attributes that set them apart. In the US, many of them are located in the Rust Belt, an area not usually associated with technology. Creation Technologies and TotalEMS report that the high mix and lower volumes of their industrial customers are not suited to production in Asia. On the other hand, Mexico is an option that MEC and TotalEMS are offering their industrial customers. Also, industrial business can be less volatile than what one might see in, say, communications. Less volatility means easier forecasting. Product lives may also be longer.

For providers who find these attributes desirable, the industrial market is not an easy one to target. Because the industrial market is highly fragmented, it's hard to grasp in its entirety. For example, MEC's industrial business consists of 17 different industries. These can range from a relatively obscure niche such as the control and monitoring of street lights to MEC's bread-and-butter products such as industrial dryer and diesel engine controls. What's more, there is no universal definition of the industrial segment.

But with Solectron pursuing the segment, it's bound to receive more attention. For MEC's Stoehr, the attention is overdue. "The technology sector gets all the press, but the industrial sector is a good stable base of technology application," he said.

A growing number of EMS providers are offering reference designs as an entree to the outsourcing of entire products (March, p. 4-6), and Celestica is no exception. The provider has introduced an Intel Itanium 2 processor-based reference design for workstations and already has more than one customer for it.

But unlike those providers who package their reference designs in an ODM offering, Celestica won't attach the ODM label to the new reference design. Instead, Celestica considers the workstation design as CDM, or collaborative design and manufacturing, business. The difference? Celestica defines CDM as ODM activity without private labeling and without customers worrying about their intellectual property. "We're very adamant about making sure we protect the IP of the customer," said Dan Shea, senior VP, group general manager and chief technology officer at Celestica. The company also believes it has a much larger capability for worldwide order fulfillment than ODMs have.

Celestica will be offering two 64-bit workstation products. The single-processor product serves as an entry-level solution, while the dual-processor design is geared to the performance workstation user. In either case, the product can be supplied with the upcoming Itanium 2 processor 6M, codenamed Madison, or the upcoming low-voltage Itanium 2 processor, codenamed Deerfield. The single-processor workstation will be available to the OEM market in the fall of 2003, and the dual-processor version will be ready for the market in the spring of 2004.

The provider also plans to introduce reference designs for other products. "We have put a roadmap in place for both servers and workstations going forward," said Shea. "...The focus of the roadmap is to plug gaps in the roadmaps of our customers." Those gaps occur, he said, because customers can't afford to do the design work or give other projects priority because of limited resources.

The restructuring that Celestica customers have undertaken has been a silver lining for Celestica's CDM efforts. "We're finding a much more open collaborative environment now than we did a few years back," said Shea.

Sanmina-SCI has continued its ODM thrust with an agreement to acquire Newisys (Austin, TX), a privately-held developer of enterprise-class servers. Financial terms were not disclosed. The deal is expected to close in several business days from its announcement on July 17. Newisys will become a wholly-owned subsidiary of Sanmina-SCI.

According to Sanmina-SCI, Newisys will add a deep competency in developing enterprise-class server technology. Utilizing the AMD Opteron processor, Newisys' server designs allow enterprise customers to make a nondisruptive transition from 32-bit to 64-bit computing. Newisys' technology will be combined with Sanmina-SCI's manufacturing services in the enterprise computing and storage space. Sanmina-SCI will now be able to provide server platform designs on a build-to-order and configure-to order basis globally.

This acquisition will strengthen Sanmina-SCI's high-end ODM offering. The company has embarked on an ODM strategy in certain segments as illustrated by its introduction of an ODM line of InfiniBand products (March, p. 5, June, p. 7). Newisys' experience in ASICs, chipsets, BIOS, software and systems management will augment Sanmina-SCI's ODM offerings for enterprise computing and storage OEMs.

"With the expected growth in the enterprise server market and our companies' combined design, engineering, manufacturing, and global no-touch order fulfillment capability and experience, we have a real opportunity to capitalize on the market's migration from 32-bit to 64-bit designs," stated Phil Hester, Newisys CEO and cofounder. The company was started in August 2000.

Sanmina-SCI is promoting Newisys' capabilities in AMD Opteron-based 64-bit server technology, symmetric multiprocessing and remote management for standards-based, high-performance server design. Newisys has introduced the 2100 enterprise-level platform and the scalable 4300 server, the latter with four Opteron processors.

Newisys has announced reseller agreements with Colfax International (Sunnyvale, CA), APPRO (Milpitas, CA) and RackSaver (San Diego, CA). In addition, Newisys has engaged a distribution partner, Avnet Applied Computing (Phoenix, AZ).

Sanmina-SCI and Newisys share some unnamed OEM customers.

Note that Sanmina-SCI is not the only EMS provider tapping the market for Opteron-based servers. Celestica will build barebones and fixed-configuration systems under AMD's Validated Server Program (see News, p. 6). System builders APPRO and RackSaver, mentioned earlier, are also offering Opteron-based servers produced by Celestica.

Establishing a manufacturing presence in the US, Canada's Creation Technologies (Vancouver, British Columbia) has acquired Eder Industries, an EMS provider in Milwaukee, WI. Creation bought all of the outstanding shares of Eder from its parent company APW, a supplier of custom enclosures.

With annual sales of about $35 million, Eder employs 210 people and operates a 75,000-ft2 facility. Founded in 1953, the company provides design and manufacturing services to the industrial control, wireless, transportation and instrumentation markets.

"We have seen a substantial increase in new customer inquiries over the past year, particularly in the US, as OEM customers look for strong partners to outsource their manufacturing to. We have been actively increasing our US presence through direct sales and manufacturing representatives, and the establishment of a manufacturing facility in the US was our next step," stated Geoff Reed, CEO of Creation Technologies.

Eder is one of two businesses that APW is divesting under a financial and operational restructuring plan. APW also intends to sell its technical furniture manufacturing business, Wright Line. The two sales will allow APW to return cash to investors while retaining a working capital reserve. APW considered Eder a noncore asset because there was not enough of an overlap between APW's global OEM customer base for custom enclosures and Eder's more regional EMS customers.

Although Eder's customer base helps to diversify Creation's business, there were more important reasons to make the deal. "More important was the way they run their business and their corporate culture," said Dave Pettigrew, executive VP of business development for Creation.

According to Creation, Eder's design capabilities and inventory management processes will strengthen Creation's offerings for medium-volume, complex manufacturing. Creation will manage the Eder facility as an independent business unit and integrate the skills, service offerings, processes and sales efforts of the two companies.

Creation plans to make more acquisitions in the US. "We plan to further acquire a plant in the US Northeast and the Great Lakes region and possibly do an Asian alliance to provide a higher-volume manufacturing alternative," said Pettigrew.

Established in 1991, Creation Technologies is an employee-owned company with four manufacturing facilities in Canada. The provider has two facilities in British Columbia and two in the greater Toronto area. The addition of Eder gives Creation a total of 14 SMT lines and 229,000 ft2. Now employing 830 people, Creation provides services from design support and new product development to final assembly, packaging and product distribution. Described as a top 100 EMS provider, the company focuses on manufacturing of complex electronics for the wireless telecom, medical, industrial controls, transportation and instrumentation markets.

With the acquisition of Eder, Creation is forecasting revenue of $120 million for its fiscal year ending May 2004, compared with about $80 million in fiscal 2003 sales. The company has achieved 12 consecutive years of positive earnings.

Techdyne (Hialeah, FL), a provider of EMS and cables and harnesses, has obtained a presence in Mexico with its acquisition of AG Technologies, an EMS company with headquarters in Schaumburg, IL, Asian partners, and a factory in Matamoros, Mexico.

AG, a private company, generated 2002 sales of $11 million, most of which came from its 40,000-ft2 plant in Matamoros. The net purchase price for AG was $1.6 million in cash plus an earnout of up to $1.3 million over three years based on reaching sales targets during that period.

"We have been searching for the right acquisition to expand into Mexico for over a year; in AG, we believe we have found that right company. This new facility will enable us to be competitive in the higher volume arena for assembly in North America," stated Sam Russell, Techdyne's chairman.

The UK's Simclar (Dunfermline, Scotland), a privately-held provider, owns 71.3% of the stock of Techdyne, a public company. The plan is to add sheet metal and plastic injection molding capabilities in Mexico to enable the Simclar Group to offer a total low-cost solution for volume production in North America.

The Matamoros plant is served by a bonded warehouse in Brownsville, TX. AG also has design and manufacturing relationships in Asia, and Taipei, Taiwan, serves as AG's primary Far East location. Its Schaumburg headquarters handles customer service, quoting, tracking, billing and some procurement.

Techdyne operates four US manufacturing locations: Hileah, FL; Round Rock, TX; Dayton, OH; and North Attleboro, MA.

SMTEK International (Moorpark, CA) has acquired an SMT line for NPI work and an undisclosed number of production personnel from the Philips Center for Industrial Technology North America (Sunnyvale, CA), a division of Royal Philips Electronics of the Netherlands. The NPI line has been moved to SMTEK's Santa Clara, CA facility.

An asset purchase and cooperative agreement allows the two companies to work together on NPI and engineering projects. SMTEK expects that it will end up with a majority of the consignment revenue generated by the line, which serviced customers both inside and outside Philips. Philips Center for Industrial Technology (CFT) told MMI that it will treat SMTEK as a preferred supplier. In addition, SMTEK will gain access to the Philips CFT Design Group for its existing customers.

"We are very excited about strengthening our relationship with one of our largest customers and about the potential new business opportunities this agreement could bring us," stated Edward Smith, president and CEO of SMTEK.

"Our medical group has successfully utilized SMTEK for years and, consequently, we feel comfortable in entering into this agreement," stated Jaap Stulp, GM of Philips CFT North America.

Philips divested the NPI line because it was underutilized. "We just didn't have enough load for the line," said David Hammett, director of engineering and manufacturing at Philips CFT North America.

For the most part, the line has been used for consumer electronics work. "Most of the work is centered around semiconductors that are for the consumer market," said Hammett. He pointed out that most of the line's prototype builds were never intended to go into volume production.

With more than 1200 employees worldwide, Philips CFT supports Philips product divisions and outside companies in all aspects of product creation such as mechatronics, electronics, process technology, materials analysis and assembly.

Groupe Ingenico (Paris, France), a maker of electronic payment systems, has chosen MSL (Concord, MA) as its primary global strategic supplier to support globally Ingenico's line of electronic payment terminals. As part of this multiyear agreement, an Ingenico subsidiary in Barcelona, Spain, will transfer to MSL its manufacturing employees with expertise in electronic funds transfer point-of-sale and secure payment products, as well as certain assets and manufacturing space in Barcelona.

The Barcelona plant, formerly Ingenico's only internal manufacturing site, produces about 600,000 terminals a year, or about 40% of the company's global demand. MSL will provide manufacturing, build-to-order, order fulfillment and repair services to Ingenico from Barcelona and from additional locations worldwide.

"MSL's selection by Ingenico strengthens our position as an EMS industry leader in retail systems," stated Bob Bradshaw, MSL's chairman, CEO and president. "Given Ingenico's leadership in smart card and wireless technologies, this relationship enables us to participate in faster growing segments of the POS market and represents an attractive growth opportunity for MSL."

More new programs...Sierra Wireless (Vancouver, BC, Canada), a supplier of wireless PC cards and other wireless products, has transferred global fulfillment and CDMA product manufacturing to Flextronics (Singapore). Fulfillment services had been provided by Globalware, while CDMA production had been handled by Sanmina-SCI. Solectron and Creation Technologies remain as EMS providers to Sierra Wireless. Also, Dow Jones is reporting that Flextronics will produce digital minilabs in Poland for the UK's Photo-Me International, a photo booth manufacturer....Celestica (Toronto, Canada) will build barebones and fixed-configuration servers under AMD's new Validated Server Program. Powered by AMD Opteron processors 800 and 200 series, these servers are intended initially for system builders, system integrators and value-added resellers in North America, with a global rollout expected in the second half of the year. System builders initially offering servers manufactured by Celestica include APPRO, Aspen Systems and RackSaver. Also, Intransa (San Jose, CA) has awarded Celestica a manufacturing and testing program for Intransa's IP5000 Storage System, a product for IP-based storage area networks. Finally, Reuters is reporting that Celestica has started producing some Palm PDA models in Jaguariuna, Brazil....Exabyte (Boulder, CO), a supplier of tape backup systems, has agreed to outsource its Depot Repair Service operation to Teleplan International (Westlake, Village, CA). This agreement includes a cash payment to Exabyte for repair-related fixed assets, including equipment and tooling, service parts inventory and swap pool inventory. In addition, Exabyte will receive royalties relating to future depot repair services. The repair process will be transferred to Teleplan's operations, which will perform all in-warranty and out-of-warranty depot repairs of Exabyte storage products....GE Aircraft Engines has awarded LaBarge (St. Louis, MO) a $2.5-million contract to manufacture high-temperature cables for a jet engine in the US Navy's F/A-18 E/F Super Hornet fighter.

Adding equipment...To meet increasing customer demand, Nextek (Madison, AL) has expanded capacity with additional SMT assembly equipment for advanced PCB assemblies utilizing BGA, CGA and CSP packaging as well as standard SMT. The company also installed additional dispense and UV cure equipment in its Class 10,000 clean room to meet greater demand for microelectronic and optoelectronic assembly of fiberoptic transceivers and medical devices....Nam Tai Electronics (Hong Kong) recently installed a new flexible printed circuit (FPC) subassembly line at a cost of $4.2 million. In the past, Nam Tai purchased FPC subassemblies to assemble LCD modules, PDAs and other products. The company plans to use the new line to manufacture FPC subassemblies ordered by an unnamed customer for color LCD modules used in cell phones. This FPC assembly process includes a precise power IC attachment and the application of lead-free solder.

More news on the technology side...Solectron (Milpitas, CA) has begun volume production of lead-free computer battery packs at its site in Kaohsiung, Taiwan. Solectron's lead-free volume production now extends to six countries (April, p. 1). Lead-free customers include Olympus Technologies (March, p. 7) and Sony....Sanmina-SCI Enclosure Systems, a division of Sanmina-SCI (San Jose, CA), and Delphi Harrison Thermal Systems, a supplier of thermal products to automotive and other markets, have formed an alliance to develop thermal solutions for large-scale computer equipment, including Sanmina-SCI's high-performance line of enclosure products. Delphi Harrison is a division of automotive supplier Delphi Corp.

Supplier awards...Microsoft has named Flextronics its 2003 vendor of the year. Flextronics is not only the primary contract manufacturer of the Xbox console, but also produces PC hardware devices for Microsoft....Dell has given its Platinum Award for the best overall production supplier to Taiwan's Foxconn, primarily for standards-based servers and desktop computers.

According to a report from Bear Stearns (New York, NY), Solectron has identified noncore businesses for divestiture over the next 12 months.

The company told investors in April that it was reviewing its portfolio of businesses. "If we find that certain businesses and activities for whatever set of good reasons are no longer core or may not be strategic to the future direction of the company, then those are businesses that we are going to look to potentially divest," said Mike Cannon, Solectron's president and CEO, during the company's investor conference.

Bear Stearns analyst Thomas Hopkins told MMI that Solectron is targeting business units that have operating losses now and units with a disproportionate amount of SG&A expenses.

A Solectron spokesperson said the company would not comment regarding the divestitures as it is still finalizing details. She added that Solectron has not set forth a timeline in public remarks.

Some financial news...Jabil Circuit (St. Petersburg, FL) is issuing $300 million in senior notes due 2010 and bearing an interest rate of 5.875%. The company expects to use the net proceeds for repayment of outstanding debt under Jabil's revolving credit facility and for general purposes....Rep-tron Electronics (Tampa, FL) has reached a term sheet agreement to restructure its 6 3/4% subordinated convertible notes due August 2004. The agreement calls for the notes to be exchanged for new notes and common shares expected to represent about 92% to 95% of shares outstanding. Also, the company's indebtedness of $76.3 million from the original notes will be reduced to $30 million. If the transaction is completed as outlined in the term sheet, Reptron expects its debt-to-equity and liquidity positions to improve markedly....For the fiscal year ended April 30, publicly-held SigmaTron International (Elk Grove Village, IL) reported that revenue increased 9.9% to $93.2 million. Net income amounted to $5.4 million, up from $1.5 million the year before, and diluted EPS were $1.61 versus $0.52 in the prior year. Fiscal Q4 sales grew 33% from a year earlier to $25.8 million....As a result of noncash charges announced on June 19, Solectron was not in compliance with minimum tangible net worth covenants required by its undrawn, $450-million credit facilities. The company has since obtained amendments to covenant definitions and, as a result, is in compliance with all of its debt covenants....San-mina-SCI is calling for redemption on August 7 of its 4 1/4% convertible subordinated notes due 2004. The principal amount outstanding is about $263.6 million....MSL has arranged for private placement of $25 million of its 4.5% Series B convertible preferred stock. The placement includes warrants to purchase 1.17 million shares of common stock over five years. The company intends to use the net proceeds for general purposes, including working capital to support new growth, capital expenditures and potential acquisitions....Nam Tai Electronics has announced a three-for-one stock split. For Q2, the company has achieved a new quarterly sales record of $116 million, up over 120% from $52.3 million a year earlier. Nam Tai attributes this growth mainly to increasing sales in telecom component subassemblies. This result represents the third consecutive quarter that sales have reached new highs.

Maintaining stock listings...The common stock of SMTEK International will continue to be listed on The Nasdaq SmallCap Market through a temporary exception from listing requirements that the company failed to satisfy. The exemption is contingent on SMTEK satisfying a $1.00 minimum bid price through a reverse stock split, maintaining a closing share price of at least $1.00 for ten consecutive trading days, demonstrating shareholder equity of at least $2.5 million, and filing a form 10-K. All of these conditions have deadlines. SMTEK's common stock has been delisted from the Pacific Exchange....Nasdaq has notified SMTC (Toronto, Canada) that its common stock has failed to maintain a minimum bid price of $1.00 per share over 30 consecutive trading days, as required by Nasdaq rules. Nasdaq has given SMTC a grace period until November 17 to regain compliance with this requirement. To regain compliance, the stock must achieve a closing bid price of at least $1.00 for at least ten consecutive trading days unless Nasdaq specifies a longer period, generally not more than 20 consecutive days.

Another restructuring move...Under a new restructuring program, PEMSTAR (Rochester, MN) will consolidate its San Jose and Mountain View, CA operations into one site and will also close four of its smaller, leased locations. Together, these measures will reduce the company's domestic work force by about 5% and the leased space it occupies by 70,000 ft2. As result, PEMSTAR expects to take an after-tax charge of about $7.8 million over the June and September quarters. Citing SARS, continued weakness in the communications market, and lower volume in the company's development, test and automation business, PEMSTAR has reduced its guidance for the June quarter.

People on the move...After a 15-year career at GE, Marc Onetto has joined Solectron as executive VP of worldwide operations. Most recently, he served as VP of GE's European operations. Under the leadership of Solectron's new CEO, Mike Cannon, the provider has also brought in a key executive to run sales and account management (March, p. 8). Also, Arthur O'Donnell has left Solectron Global Services, where he held positions as president and COO of its Americas organization. O'Donnell joined Symbol Technologies as senior VP and GM of the Symbol Global Systems and Services Group....Timothy Fox has returned to IEC Electronics (Newark, NY) as director of business development. Fox worked at IEC from 1993 through 1997 and formerly held the position of business development manager. He is the third senior executive to rejoin the company in the last 18 months....Integrex (Bothell, WA) has promoted Joe Yabuki from director, program management to VP, operations. Yabuki will replace Mark Johnson, formerly senior VP operations at Integrex and now VP of operations for Philips Oral Healthcare. Johnson will become chairman of the newly formed Operations Advisory Board at Integrex.

Correction...Due to a transcribing error, last month's Q&A article on page 3 contained the wrong abbreviation for communications network equipment OEMs referred to by Elcoteq's Bill Coker. The correct acronym for these OEMs is CNE.

Time was, if an EMS provider wanted to expand into a new market or add a capability, the provider would usually look to buy the requisite skill or market position. But excess capacity and cash conservation have providers exploring other ways to achieve their ends. And this goes for even the largest providers.

For example, Celestica, Flextronics and Solectron have all made recent moves into new areas without making the proverbial acquisition. Celestica has entered the automotive sector to add diversity to the company's portfolio of customers. Did Celestica acquire an automotive supplier as some others have done? No, the company has taken a more subtle approach. Celestica's automotive push includes partnering with IBM to build telematics devices (May, p. 6-7). Not only does Celestica gain access to IBM's telematics technology, the provider can also piggy back on IBM's knowledge of and contacts in the automotive sector.

Flextronics wanted to add power supply manufacturing to its offering. Instead of purchasing a power supply manufacturer, Flextronics struck a licensing deal that allows it to manufacture power supplies for the customers of Celetron, an India-based provider that makes power supplies among other things (May, p. 7). Reportedly, Flextronics also invested in Celetron.

Solectron was after a piece of the outsourcing market in cell phones supplied to China. Rather than make an outright acquisition, Solectron formed a joint venture with a Chinese cell phone provider. Solectron treats this joint venture as an alliance, and its president and CEO, Mike Cannon, recently told investors that alliances can be equal to or better than acquisitions (May, p. 1). Clearly, Solectron has signalled its intention to add alliances to its tool kit.

Tier-one providers do not hold the exclusive rights to creative thinking. Take Nam Tai Electronics. Nam Tai has made relatively small equity investments in companies that have ownership in Chinese handset suppliers. These investments established relationships that helped Nam Tai win business from two cell-phone suppliers in China - JCT Wireless and TCL Mobile. In the latter case, Nam Tai owns stakes in both TCL and its parent company.

Moreover, creativity has become crucial for mid-tier and smaller providers who have faced weak end markets and a major shift of production from high- to low-cost areas. They must find ways to stay viable or attempt to sell out in a buyers' market. The downturn continues to take its toll on some providers but others are finding ways to bolster their offerings. And often they're not resorting to acquisitions.

Teradyne Connection Systems effectively added design capability through an arrangement with Design Solutions, which opened a design center within a Teradyne facility in New Hampshire (April, p. 6). Suntron expanded into remanufacturing through a partnership with MasterWorks, which provides asset recovery services (March, p. 6).

Are alliances and partnerships the answer for a down market? Not in and of themselves. But tough times require adding creative approaches to the tool box.