![]()

Cover Story

World Markets

Survey Assesses SARS Effect on Shift to China

Q&A

Market Trend

Arrow Building System Integration Business

News

Singapore-Based Providers To Merge

Linsang To Go Public Through Merger

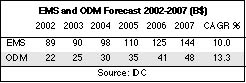

Those who were hoping that the EMS industry would resume growth this year will be disappointed by the latest forecast from IDC (Framingham, MA). The market research firm has lowered its projection for 2003 from $94 billion to $89.5 billion. Based on the new forecast, 2003 will be essentially flat compared with IDC's 2002 figure of $88.75 billion.

"This is based upon a very bad first quarter," said IDC analyst Kevin Kane. For the large EMS companies IDC tracks, it found a year-over-year decline of 1.2%, "the first year-over-year decline we have seen in several quarters," noted Kane. "Also, guidance from vendors for Q2 equals a year-over-year decline of 2.3%. So while we should see year-over-year increases in Q3 and Q4, they're not enough to make up for declines in the first half of the year. Overall, IT spending is supposed to remain weak in 2003, and the telecom slump is expected to continue with declines in capex spending expected again this year."

IDC is expecting a recovery to start in 2004 and extend into 2005 (see table). The firm is projecting EMS growth rates of 10% in 2004 and 12% in 2005, "which are pretty strong when working on a base of $100 billion," said Kane. "We think that end market demand will return, and the outsourcing trend will stay strong."

According to IDC, EMS growth drivers will come from storage and servers, consumer electronics and other segments such as automotive, medical, industrial and military.

The market research firm projects a somewhat higher 2002-2007 CAGR for the ODM market than for the EMS business. IDC justifies 13.3% for ODM versus 10.0% for EMS by citing the ODM market's smaller revenue base. "For growth drivers for ODM, we expect that the notebook business will stay strong, and the vendors will use that to help them to continue to expand into other segments such as handsets, storage and servers," said Kane.

In a recent survey of electronics manufacturing firms, most respondents expect SARS to have either a minor impact or none at all on the shift of electronics production to China. Based on 117 interviews, the study was conducted by the International Finance Corporation (IFC), the private sector arm of the World Bank Group, and management consulting firm Booz Allen Hamilton.

Of the executives polled, 64% expect SARS to have a slight temporary impact on the movement of electronics manufacturing to China, and 22% believe SARS should have no effect on this trend. Only 14% of respondents expect the disease to have a moderate impact. In addition, none of the respondents expect SARS to have a significant impact on the long-term growth of electronics production in developing markets.

The study estimates that electronics production in China will reach $80 billion by 2005, exceeding $73 billion in estimated production for Western Europe. From 2001 to 2005, China will increase its share of global electronics production from 8% to 14%, according to the study, with growth that is twice as fast as any other region. China will capture 77% of the growth in developing countries, the report predicts. By 2005, 45% of all high-volume assembly will occur in China, which the study says is evolving into the hub of electronics manufacturing.

Booz Allen and IFC found that electronics production activity in emerging markets will nearly double from $65 billion in 2001 to $125 billion by 2005. In those markets, final assembly, displays and semiconductors will provide the highest level of growth through 2005. Computers and peripherals will account for $47 billion in production growth between 2001 and 2005, followed by consumer electronics at $20 billion, handheld devices at $16 billion, and automotive electronics and telecom, both at $11 billion.

In addition, higher value services such as engineering and design functions will increasingly migrate to developing nations over the next few years, although this movement will trail the more rapid shift in production. India and Russia, in particular, have an abundance of highly skilled labor that can cost up to 80% less than in the developed world.

Despite ranking seventh in the MMI Top 50 last year, Finland's Elcoteq Network is not a household name in the American EMS market. But maybe it's time that more attention be paid to Elcoteq because it stands out in several respects. For one thing, it's growing. Elcoteq is projecting 2003 sales of about 2.5 billion euros and an enviable growth rate of 40% this year. For another, Elcoteq is already positioned with most of its capacity in low-cost geographies. Not everyone can say that. Yet Elcoteq, unlike its peers, remains focused on just one segment.

Why isn't Elcoteq diversifying? Where is this growth coming from? What is the company doing about the US market? These are just some of the questions MMI posed to Bill Coker, director of sales and marketing, Elcoteq Americas (Irving, TX). Coker, whose 20 years in the EMS industry include stints at Sanmina-SCI, SCI and Flextronics, was brought in to lead Elcoteq's sales effort in the Americas. Here's what he had to say about these and other questions.

MMI: Elcoteq is focusing on communications as its main market, while a number of other providers are reducing their dependence on communications by diversifying into other markets. Why is Elcoteq betting so heavily on communications, while other providers are not willing to do so?

Coker: One of the things that I learned along the way in making the transfer from a huge tier-one provider to Elcoteq, a tier-two, is that my previous employer and the other tier-one players are having a tremendous amount of difficulty managing ten-plus billion-dollar companies that service all seven market segments on a global basis. These companies must support all of those segments, all of those customers and all of those different pieces of business with a limited amount of resources to go around.

I think the most current trend in the tier-one group is to take their companies from being horizontally oriented and turn them sideways so that they become vertically integrated in market segments. So you'll find that those companies will align themselves along technology sectors like communications, computing, industrial, medical, aerospace. One of the true advantages that Elcoteq has is that, being focused the way we are in communications technology only, we're already there. We've aligned our company. It's focused on a specific segment that today is somewhat depressed by the economy. But if you look at the growth potential numbers for the next number of years, the outsourcing opportunities in communications far exceed those of the other segments. So the company has decided to focus its attention, its resources and its expertise in one area, and that's what we call communications technology products and customers.

Today, we're a major player in comm tech. If you just look at our comm tech revenues and compare those across the other contract manufacturers, it's somewhat debatable whether we're number two or number three. But we're a close second or third no matter how you look at it. So within the segment, we're a major tier-one player in communications technology work.

A high percentage of our business is with Nokia and Ericsson, and a lot of that is European dependent. So if you look at the rest of the communications technology market, the Americas has a huge total available market. It may not be growing at the moment, but it's still out there. It's still accessible. And we find that the customers in the marketplace are looking for a fresh, new business model from a contract manufacturer that will manage the business and provide its services a little bit differently from what they're used to.

MMI: In light of SARS and the weakening US dollar, Elcoteq has lowered its growth forecast to 40% for 2003. Still, most providers would be quite happy with 40% growth. How do you explain this growth?

Coker: A certain amount of that is public in terms of the revenues derived from the GKI acquisition (Jan., p. 5). So some of that growth is by acquisition. But the rest of it is coming from organic growth.

The company has put a major emphasis in the last year on expanding its sales organization globally. I'm part of that expansion in terms of hiring some seasoned veterans from contract manufacturing to help develop customers and new business globally.

MMI: Ericsson and Nokia, which you mentioned earlier, together accounted for 78% of Q1 sales. Does Elcoteq plan to reduce its longtime dependence on these two customers?

Coker: Our goal going forward is that 30% of our business should come from customers in terminal products, which would be handsets. 30% ought to come from CNE customers, which are the communications network equipment OEMs. And 30% ought to come from what we call CDM, which is contract design manufacturing. Here we're developing platform solutions like handsets and maybe some other CNE type technology platforms and providing solutions to the customer as opposed to just being a build-to-print contract manufacturing service.

It is not uncommon for a contract manufacturer to have one or two major customers that dominate their business. The good news is we have them. The bad news is we have to convince the rest of the world that they can be a big fish in a small pond, and they don't have to compete for resources with Nokia and Ericsson. That's part of creating value propositions that solve the customer's manufacturing and distribution needs.

When I first looked at this job in the Americas, I saw it as interesting in that from an Americas standpoint it's really a start-up contract manufacturing job. But I have the resources of a two-billion-dollar contract manufacturer. So the risk is very much minimized. I take that very same argument back to my potential customers who say, "Yeah, but you do a lot of work with Nokia or Ericsson." It actually turns into a huge advantage from a technology, global footprint and capacity standpoint.

MMI: As a European company, Elcoteq is not widely known throughout the US market. What can you say about Elcoteq's plans for the US market? Is it true that the company has set a goal of 25% of its sales coming from the US market by 2005?

Coker: It's absolutely true. When I started, even I had to answer the question for myself, "Elcoteq, who?" The major players on the handheld side in the US like Motorola, like Kyocera, know who we are because we're such major players in handset manufacturing for their competitors. The challenge for us is to expand our name and our brand recognition across the rest of the comm tech industry, which includes a lot of the CNE companies that are doing business in the US today.

There are a couple of strategic initiatives that make up our Americas strategy. For the first time in the US, we've put together a pretty seasoned sales organization, and we've targeted specific customers both in handsets and in the infrastructure business. As we penetrate those accounts and start to win that business, automatically our visibility goes up, not only in the industry but with the supply base and the other competing customers that make similar products. So sales is an important key.

The other one is we made a decision, which is part of our strategy, to expand our service capability in North America by providing regional and localized prototype and NPI services. The intent there is to provide a certain level of localized service and harvest customer relationships geographically from NPI providers. So we're not looking to grow NPI from a greenfield standpoint. Our strategy is to identify small companies that do prototype and NPI work and have a fair amount of communications technology content, make those acquisitions, get a better local presence, and then harvest those customers for opportunities to expand our business to our low-cost geographies and global footprint.

So the first deal we pulled the trigger on was an NPI center in Dallas (March, p. 7). We did that a couple of months ago, and that relationship is working out really well. They've provided us a couple customers that we could move to our low-cost factories. At the same time, we've added to their mix customers that need their services either on a local basis or as a gateway to a low-cost geography.

We're in the process of closing on a similar relationship in the Bay Area in Northern California. From there, we're going to look at the East Coast and the Midwest to do very similar acquisitions. We're really not looking to add huge amounts of brick and mortar and lots of domestic capacity. What we're looking for are small engineering-oriented prototype centers with good customer relationships that we can use as business incubators.

Last but not least, a lot of what we're trying to do from a marketing standpoint is to establish the brand and name recognition in the industry by participating in interviews, trade fairs, technology forums and speaking sessions.

MMI: With the Dallas NPI center, did you pick up any comm equipment customers in the corridor down there?

Coker: Absolutely. That's part of the strategy. We don't want an NPI center doing industrial products or medical products. We focus our attention and search on companies that are doing communications technology, and this NPI center is right in the middle of the technology corridor here in Dallas.

MMI: Like Flextronics, Elcoteq is now selling design platforms for mobile phones. This is an ODM activity, yet Elcoteq has told MMI that it does not want to be called an ODM. Please explain Elcoteq's position with regard to the ODM market.

Coker: We're an electronics manufacturing services company with design capabilities. We don't want to change that classification to ODM because we're really not an ODM. We're an EMS company that has ODM-type solutions available to its customers. There's a big difference between us and an ODM designing products, building hundreds of thousands or maybe millions of them, and trying to sell those products off the shelf to whomever will buy them. The distinction comes from the fact that we will not speculate on a design or speculate on inventory. We're just developing hardware and software platforms in the handheld space, providing those to our OEM customers, and letting our customers decide where those fit in their product portfolios.

We can quickly turn those platform solutions. If customers decide that they will go with the existing plastic and all we're going to do is put their name on it, we can bring it to market in a very short period, 60 to 90 days. The supply chain and the cycles for material are so short that we can do it. If the customer wants to change what we have today as a platform design, it takes a little bit longer. But we can still bring that to market very fast at a cost that's significantly less than what the OEM would spend developing the product internally.

So it really becomes a cost economics decision. Does the OEM design internally? Or does it buy that design externally? It's a make-buy decision. And there are a lot of dollars on the table. I've heard that it could cost as much as ten million dollars to develop a handset. In a CDM or an ODM environment, an OEM can add an off-the-shelf or almost off-the-shelf product to its portfolio for less than a million dollars. So it's almost a ten-to-one ratio in terms of R and D. That's a huge advantage for companies.

I think more and more OEMs will try to expand the number of product offerings that they have in the marketplace, which will create more variation in product mix and higher part-number counts. This will complicate the supply chain in terms of product that's available, different configurations and how you manage that. I think this trend differentiates us from a pure ODM. An ODM wants to build high volume, probably in Taiwan or China, and distribute the product around the world. But the OEM, as it grows the number of products that it has, needs to have more flexibility, more agility. The OEM needs to be able to configure phones faster on the fly so that there's not a lot of inventory sitting in the supply chain. Elco-teq's global footprint becomes a major differentiator between us and a traditional ODM.

We have OEM customers today that come to us and want the phone built in Europe. Or they want the phone made for the Americas or China. We will build and localize it in the geography where they need to have it done. We even benefit from situations where an ODM will win a design from an OEM, and the OEM will want to build in a geography or finally configure in a geography where that ODM isn't present today. We have a couple situations where we actually become the manufacturer of that product licensed by the ODM, and we deliver it directly to the end OEM.

MMI: In handset outsourcing, Flextronics is number one and Elcoteq is number two. In the handset market, how can Elcoteq be successful competing against Flextronics, a much larger company?

Coker: Costs come from two areas - material and labor and overhead. I think from a materials standpoint on the supply chain side, we're just as competitive as a Flextronics. Here's the way I look at it. If Flextronics is 10 billion dollars plus, all of that spend on material is not necessarily communication-type products such as resistors and capacitors, the comm-tech centric chip sets, plastics and metal. So there's a certain amount of their spend that is comm-tech related. Almost all of our spend is comm-tech related. In terms of total dollars going into that segment with those types of suppliers, we're a major player in material consumption on the radar screens of those types of companies. So we get very competitive prices on a global basis.

The other component is overhead and labor. One thing that differentiates us from the rest of the players is we haven't made huge divestiture acquisitions. And we're not burdened by the cost of huge underutilized facilities that increase our SG&A. So we're a very lean company. For the most part, we've grown by greenfield operations and not by acquisition. So our overhead numbers to compete in this business are much lower than those that have grown by M and A.

From a labor standpoint, for the most part our factories are in low-cost geographies in Eastern Europe, Mexico and China. So we're not trying to build products in high-cost domestic plants just to give us a return on an investment made in a divestiture acquisition. We're going to take the work and build it in a low-cost geography that makes the most sense for the customer. And that makes us very competitive.

MMI: Is Elcoteq accepting business that is outside communications and industrial electronics?

Coker: Our focus is communications technology. If you look at what our core competence is in that space, it's in the area of wireless. And if you look at wireless closely, you'll find lots of applications for wireless technology in the communications sector. But there are also wireless applications in some of the other sectors too, like PCs, industrial and medical. So we don't draw a line and say if you're not a Lucent, a Nortel, or an Alcatel, we're not interested. We look at this from a technology perspective and ask if our core competencies in wireless can be used anywhere else. If the answer is yes, then we'll apply them across a somewhat broader spectrum than just the communications sector.

MMI: We hear that includes telematics.

Coker: Even though some people put telematics in the automotive bucket, it's really a series of wireless products. We do a lot of telematics products today, especially here in the US. We're doing this for Sony Ericsson, and Sony Ericsson has helped us identify other customers for this manufacturing technology.

MMI: Does Elcoteq plan to add capacity in China or anywhere else?

Coker: We're considering a number of different acquisitions at this moment. They're not geography centric. We're not saying we just want to be in China, or we just want to be in Eastern Europe. We look at it from a comm-tech standpoint. Is it an acquisition that adds to what we're doing and our strategy to grow our comm-tech business? So we are looking at acquisitions in Europe, North America and China.

MMI: In Q1, capacity utilization rates were lower in Mexico than in Europe and China. What role will the Mexico plant have going forward?

Coker: The Mexico plant was a greenfield operation designed to support the business activity that was generated in the Americas. Although we put capacity on line faster than the sales organization could create opportunities for that factory, I can report that the utilization rates going forward in that factory will be much higher. We've won some major business over the last couple months that will start the end of this summer and will definitely show up in our Q3, Q4 revenue and capacity utilization numbers.

We built 100,000 excess square feet on the factory just when the market turned south. So there's a lot of growth expansion available in the factory. Today, we do a lot of terminal manufacturing in that factory. We're setting up the second half of that factory to support the communications network equipment business that we're focused on selling and winning in the US. There's good news coming out of Mexico right now.

The outsourcing of OEM system integration is seen as an important source of future growth for the EMS industry. But EMS providers aren't the only ones looking to win outsourcing from OEMs who don't want to build their own products. Distributor Arrow Electronics through its OEM Computing Solutions unit (Englewood, CO) provides supply-chain management, manufacturing and system integration to industrial OEMs and other customers. These value-added services are an extension of the unit's business in selling computer products to OEM customers.

Although Arrow does not break out the sales of OEM Computing Solutions, the unit's system integration business is growing. "One of our primary focuses is to grow that business," said Steve Ramsland, VP and GM of OEM Computing Solutions. An estimated one third of the unit's business involves some form of manufacturing.

For example, OEM Computing Solutions recently completed the first year of a manufacturing and integration contract with Peribit Networks (Santa Clara, CA), which has developed products for WAN performance. The Arrow unit handles Peribit's materials procurement, integration, assembly, testing and packaging and soon will take over order fulfillment. Arrow has also disclosed another customer for system integration - Texas-based Schlumberger.

The unit has at its disposal a 212,000-ft2 integration center in Phoenix, AZ, where the work force is ramping to 207 employees. Of that total, 155 people are dedicated to the integration center, with the remainder shared with Arrow's logistics or other operations. On the sales side, OEM Computing Solutions maintains an organization of just under 200 people.

Given the range of value-added services such as those provided to Peribit, the Arrow unit positions itself as more than a traditional system integrator. But the unit does not view itself as an EMS operation. "We don't bill ourselves as a contract manufacturer in any sense of the word," said Jim Markisohn, VP of business development for Arrow's North American Computer Products Group.

OEM Computing Solutions, which is part of Markisohn's group, differs from a typical EMS provider. For one thing, OEM Computing Solutions does not have capability for PCB assembly. When necessary, the unit relies third parties for board assembly. Also, customers typically settle on industry-standard architecture, which allows Arrow to use off-the-shelf technology in the customer's product. "Where we get involved is to integrate that technology into some kind of final product and provide design and engineering services where necessary," said Markisohn. This building-block approach means that OEM Computing Solutions is often starting out with board-level subsystems sourced from its product lines.

The unit's franchised lines of computer products such as displays, disk drives and motherboards cover over 90% of customers' product requirements, according to Ramsland. Indeed, Arrow's franchise privileges become a major selling point.

Looking to outsource noncore activities, customers come from segments that include telecom, medical, industrial and gaming.

OEM Computing Solutions offers a different route to system integration from what is offered by the EMS industry. But the Arrow unit is still taking a slice from the outsourcing pie. And that slice is part of a system integration wedge projected to take a greater share of the pie.

The stage has been set for the proposed merger two Singapore-based EMS providers, Beyonics Technology Limited and Flairis Technology Corp. This merger of two MMI Top 50 providers will create a company whose combined EMS sales would have amounted to about S$900 million, based on audited results. That's about $518 million at current exchange rates. As the surviving entity in the merger, Beyonics will become a more significant EMS player in the Asia Pacific region.

The Singapore Exchange has granted in-principle approval for the issuance of 278.9 million shares of Beyonics stock in connection with the merger. Flairis shareholders will receive 0.6 Beyonics share for each Flairis share. An additional cash consideration will be offered if Flairis satisfies a certain minimum for net tangible assets. When the merger is completed, Flairis will become a wholly-owned subsidiary of Beyonics.

"The combined entity will have the scale and size to go after bigger outsourcing contracts and customers especially the Japanese OEMs," stated Chay Kwong Soon, chairman of Beyonics. He said the two companies are complementary in terms of products, customers and operations.

Besides offering a full range of EMS, Beyonics can also draw upon its capabilities in plastics injection and mold making and precision stamping for vertical integration. Similarly, Flairis offers plastic injection molding and precision coil winding in addition to PCBA and turnkey system assembly. Both companies have manufacturing facilities in Singapore, Malaysia, Indonesia and China. Beyonics also manufactures in Thailand.

With the merger, the two companies will expand into each other's low-cost manufacturing facilities as well as further develop capabilities and capacity in China. It is expected that the combined entity should be able to consolidate and streamline its operations in each of the countries it is in.

The larger scale of the combined company is expected to lead to economic benefits in sourcing, capacity utilization, marketing and cross selling.

Each company brings its own customer base, and this diversification will mean less exposure to any one customer. Beyonics counts among its key customers Seagate, HP, Quantum, Hauppauge, IBM and Baxter. For example, Beyonics recently entered into a new two-year supply agreement with Seagate, and the revenue from the contract is estimated at about S$300 million. Flairis provides PCBA for multinationals, particularly Japanese OEMs, in telecom, computer peripherals and consumer electronics.

As of 2002 year end, the combined company would have had a total of 6500 EMS-related employees, 19 plants and 1.8 million ft2 of facility space (March, p. 3).

Pending shareholder approvals, the merger is slated for completion next month.

Suntron (Phoenix, AZ) has purchased substantially all of the assets of Trilogic Systems (Wilmington, MA), a provider of system solutions to OEMs. This move will strengthen Suntron's Northeast presence in design services and add to its customer base. Terms were not disclosed.

Founded in 1986, privately-held Trilogic offers design, NPI, manufacturing, and product life cycle man-agement to customers in the communications, military, medical instrumentation and industrial control markets. The company can provide integration through level 5.

Suntron will move Trilogic's employees and customer services into Suntron's Northeast facility in Lawrence, MA. Trilogic has operated a 27,000-ft2 facility in Wilmington.

"Trilogic Systems' comprehensive suite of design and integration capabilities, including hardware engineering, software integration, testing and product life cycle management, provides Suntron an outstanding opportunity to increase our customer base, add additional revenue, and expand our Northeast presence," stated James Bass, Suntron's president and CEO.

The acquisition provides Suntron with architectural and system-level design to extend Suntron's current design services offering, which applies below the system level. "Trilogic Systems is a great complement to our existing design services capabilities and will accelerate our design services offering, which is a key growth engine for Suntron," said Michael Eblin, Suntron's COO.

According to Suntron, Trilogic was profitable.

Privately-held Linsang Manufacturing, Inc. (LMI), an EMS provider in Beltsville, MD, intends to merge with Cheshire Distributors (New York, NY), a publicly-held company with no reported revenue. The current owners of LMI will control the resulting EMS company, whose stock will then be publicly listed.

A subsidiary of Cheshire will merge with and into LMI, which will become a wholly-owned subsidiary of Cheshire. When the merger is completed, the current owners of LMI will own about 85% of the outstanding stock of Cheshire, which will change its name to LMIC, Inc. Plans for the transaction include Cheshire undertaking a reverse stock split and obtaining accounts receivable financing.

Started in January 2000, LMI offers design and prototyping services, PCBA and test, electromechanical subassembly, box build, system integration and test, optical assembly and test, as well as field services, repair and upgrades. LMI operates in 135,000 ft2.

The provider serves OEMs in the networking and telecom, wireless, high-end computer, and industrial and medical instrumentation markets. Customers also include the US Department of Defense, the US Office of Homeland Security and other federal entities. Over 30% of LMI's customer base comes through federal contracts.

The two companies do have a prior connection. In February, Cheshire loaned $2 million to LMI.

New programs...Solectron (Milpitas, CA) during its May quarter signed 13 new customers including Samsung Electronics, for whom Solectron will provide EMS and in-warranty service engineering for a satellite set-top box product. Other new wins include NEC, IPWireless (Jan., p. 6) and Seagate. Also, the world's largest semiconductor manufacturing company has chosen Solectron to provide NPI and manufacturing of server blades and wireless products as well as the design and manufacturing of Ethernet switch blades. Although Solectron would not release the name of this semiconductor company during its earnings call, Intel is the only company fitting that description....HP has selected Flextronics (Singapore) to take over printer logistics in Memphis, TN....Voltaire (Bedford, MA) has chosen Sanmina-SCI (San Jose, CA) to manufacture Voltaire's InfiniBand connectivity systems. Sanmina-SCI also becomes the provider of choice for ODM InfiniBand platform products such as host channel adapters. Earlier, Sanmina-SCI introduced a line of InfiniBand products as part of an ODM offering (March, p. 5)....In Monterrey, Mexico, Celestica (Toronto, Canada) will manufacture cables and connectors, geophone strings and other seismic equipment for Input/Output (Houston, TX). Also, Celestica will provide design and manufacturing services for Festino system card solutions offered by Agere Systems (Atlanta, GA) for multiservice network equipment....A Fortune 150 automotive electronics supplier has selected MSL (Concord, MA) as a strategic supplier for complex PCB assemblies. This production will take place at MSL's site in Valencia, Spain. An analyst has written that the automotive supplier is Lear Corp., but MSL would not confirm the customer's identity. MSL has also won a PCB assembly contract from Cummins Power Generation. What's more, this analyst has reported that MSL landed European repair work from Hon Hai and Compal of Taiwan, but again MSL would not confirm this report. Finally, Colubris Networks has chosen MSL to manufacture its family of 802.11 (Wi-Fi) wireless networking products....Venture (Singapore) will provide expertise to reduce the cost of manufacturing and development of an Agilent product line for wireless network optimization....Sony Computer Entertainment will use Nam Tai Electronics (Hong Kong) as one of the contract manufacturers to build a USB camera for the Sony PlayStation 2 game console. In addition, Nam Tai has received orders from OmniVision Technologies to manufacture CMOS image sensor modules. Note that the PlayStation camera makes use of an OmniVision chipset....Lung Hwa Electronics of Taiwan, a consumer electronics manufacturer that is expanding into EMS, will produce a line of Internet/DVD players for Video Without Boundaries (Fort Lauderdale, FL)....Under a new contract valued at about $9 million, LaBarge (St. Louis, MO) will provide Northrop Grumman with additional equipment for a mail sorting system used by the US Postal Service.

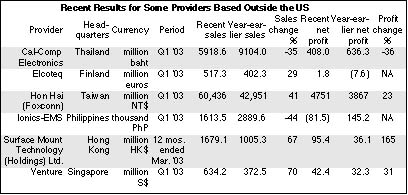

New facilities... In order to capture computer peripherals business, Cal-Comp Electronics (Bangkok, Thailand) has decided to invest about 340 million baht for a second plant in China....Surface Mount Technology (Holdings) Limited (Hong Kong) plans to build a new factory in Southern China during its fiscal year ending March 2004 and is considering a location near Shenzhen....Entronix International (Plymouth, MN) and Airborne Logistics Services, or ALS (Seattle, WA), have teamed up to offer repair, remanufacturing and reverse logistics. Entronix has opened an asset recovery and repair facility colocated with ALS warehousing facilities at the Airborne Commerce Park in Wilmington, OH.

Some financial news...For the quarter ended May 31, Solectron reported a net loss of $3.1 billion on sales of $2.8 billion, which were flat compared to the prior quarter and below year-earlier sales of $3.0 billion. This loss included pretax charges of $2.8 billion for the revaluation of goodwill, intangible assets and deferred tax assets. Excluding these charges and a pretax restructuring charge of $223 million, Solectron had a pro forma net loss of $79 million, which reflected no tax benefit. The prior quarter enjoyed a tax benefit rate of 56%. The company also recorded charges for impairment of goodwill and intangible assets in its August 2002 quarter.... In the May quarter, Jabil Circuit (St. Petersburg, FL) increased revenue by 43% year over year to $1.2 billion. Net income amounted to $4.5 million. Core earnings after taxes increased 56% from a year earlier to $38.2 million.

Correction...In last month's issue on page 6, a transaction was not reported correctly. Siemens Dematic Electronics Assembly Systems did not sell the Advanced Assembly Technology Center to Engent. Engent has acquired the rights to the facility, but is leasing it from Siemens. Siemens Dematic continues to focus its efforts on advanced technology through its Technology Network.