![]()

![]()

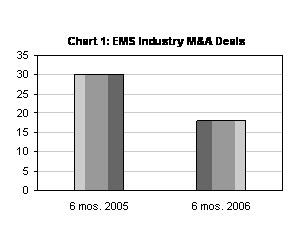

A count of EMS transactions reveals that the pace of deal-making during the first half of 2006 slowed markedly from the year-earlier period. As tallied by MMI, M&A deals done in the first six months of this year totaled 18, down 40% from 30 transactions completed in the first half of 2005 (Chart 1). MMI believes that an inward focus on operational improvement among tier-one providers contributed to the drop-off in transactions. Fewer acquisitions by smaller providers in the first half also played a role in this decline.

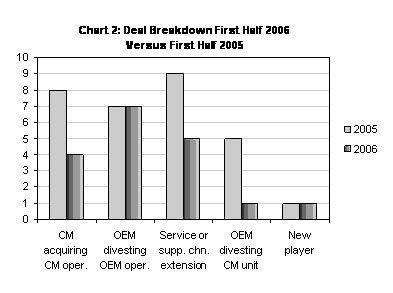

Still, a breakdown of transactions by category shows some interesting results. Not every category declined. In particular, the number of OEM operations divested – seven – held steady in the first half of 2006 versus a year earlier (Chart 2). Despite popular thinking that OEM divestitures are going the way of the dial-up modem, divestitures remain a part of the M&A mix. Although tier-one providers are typically unwilling to acquire OEM operations in high-cost geographies, circumstances can override this reluctance. A program can be so large and so attractive that a provider has no choice but to take over OEM facilities in high-cost areas. The recently completed Flextronics-Nortel deal is a prima facie case.

Another overriding reason to acquire a high-cost facility could be its niche in a desirable market segment. Kimball Electronics Group made two first-half acquisitions of operations in high-cost European locations. Each operation specializes in a nontraditional segment – medical in one instance and automotive in the other – which is largely virgin territory for outsourcing.

Five out of seven OEM asset deals closed in the first half involved acquiring operations in high-cost locations. Besides the two Kimball acquisitions in Europe, Flextronics acquired a Nortel facility in Canada; Fabrinet took over a JDSU operation also in Canada; and Sanmina-SCI gained an Adaptec facility in Singapore. Of course, this ought not to be a surprise. The operations OEMs usually want to get rid of are in high-cost locations.

In recent years, OEM asset deals have increasingly taken the form of what could be called “divestiture-lite.” In this scenario, the EMS provider buys OEM inventory and equipment and may take on OEM employees but does not acquire a facility. Because these deals don’t involve a facility takeover, they are often not as visible as the classic OEM divestiture. MMI suspects that the over the years a substantial number of lite deals have escaped the public eye.

Such was not the case, however, when Verigy, an Agilent spinoff in the semiconductor tester business, selected Flextronics as its primary contract manufacturer earlier this year. Verigy is shifting its production to Flextronics facilities in China (March, p. 6). As part of this deal, Flextronics bought about $19 million of inventory and about $2 million worth of machinery and equipment, as reported by Verigy on SEC form 10-Q. Flextronics will also pay Verigy additional consideration of $3 million, the purpose of which was not reported. But clearly, this payment is over and above the book value of the assets purchased.

Flextronics also assumed about 85 Agilent employees, who will work exclusively on Verigy products. The EMS provider received about $7 million from Agilent (which was reimbursed by Verigy) for severance and other employee-related benefits associated with the transferred employees. Verigy will also pay Flextronics about $3 million in employee benefits liabilities extending into the future. Since the two companies anticipate future severance costs and an employees’ date of termination from Flextronics, the transferred employees will only have temporary jobs under Flextronics. Their system-on-chip tester manufacturing will end up in China.

While OEM asset divestitures remained constant in the first half, deal-making in three other categories fell off versus a year earlier in keeping with the overall drop in EMS transactions. Half as many contact manufacturing operations were acquired by competitors in the first half of 2006 as in the same period of 2005. Four such deals occurred in the first half of 2006 compared with eight a year ago (Chart 2).

Why were fewer EMS operations bought by competitors in the first half? Nowadays, acquisitions of this type for the most part take place among providers in the lower tiers. The largest providers have little motivation to acquire a smaller competitor unless they are looking for a particular market niche or skill set or are expanding into a new territory such as India. In contrast, EMS acquisitions appeal to regional providers who want a larger footprint. Such deals can also boost revenue and add needed capabilities. But the number of potential buyers in North America and Europe has declined over the years with industry consolidation. In addition, an improved business environment for small providers in North America (Oct. 2005, p. 1) may have dissuaded some from putting their operations on the block.

OEM sales of contract manufacturing units also dropped in the first six months after resurging in 2005 (Chart 2). The sharp decline from five sales in the first half of 2005 to one in the latest period shows that the number of OEMs with EMS divisions continues to dwindle. Only a tiny group of OEMs can justify the low margins and capital requirements associated with owning an EMS operation.

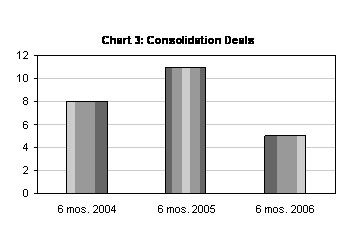

Fewer acquisitions of independent or OEM-owned EMS providers by competitors meant a reduction in first-half consolidation deals, as tracked by MMI. A consolidation deal represents the loss of an EMS player from acquisition by another EMS provider. Five contract manufacturers (four independents plus one OEM-owned operation) disappeared in this year’s first half through acquisition. By comparison, 11 consolidation deals took place in the first half of 2005. (Two of the 13 EMS operations acquired then were excluded because they came from providers with other operations.) As a result, consolidation deals in the first half of 2006 fell by 55% from a year earlier. This reduction follows a 38% increase in such deals from the first half of 2004 to first half of 2005 (Chart 3).

Acquisitions of service or supply chain capabilities also occurred less frequently in the first half of 2006. Providers made five of these deals in the first half, compared with nine in the year-earlier period (Chart 2). Tier-one providers have a history of making such transactions, but in the first half of 2006 there were only two instances of a tier-one company acquiring service or supply chain capability.

Note: This analysis does not include three cases where an EMS provider made a first-half acquisition unrelated to the EMS industry.

A new forecast projects that the total market for outsourced manufacturing services will grow at a steady but uninspiring pace over the next five years.

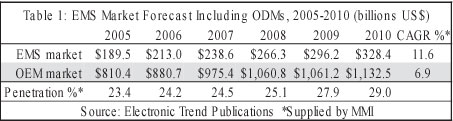

Electronic Trend Publications (San Jose, CA) has released its latest study of the EMS market, which it defines as consisting of both EMS providers and ODMs. The new ETP report, entitled The Worldwide Electronics Manufacturing Services Market, Third Edition, forecasts that the ETP-defined EMS market will expand at a compound annual growth rate (CAGR) of 11.6% from 2005 to 2010. This rate reflects a view that the high-flying days of the outsourcing business are over.

According to the ETP report, the EMS market (EMS plus ODM) reached $189.5 billion in 2005 and will grow by 12.4% this year to $213.0 billion. ETP sees year-over-year increases declining slightly over the forecast period, with 2010 growth ending up at 10.9%. In 2010, the EMS market will generate estimated sales of $328.4 billion (see Table 1).

While EMS market growth rates may never return pre-downturn levels, they are still above what is expected for the total assembly market of both outsourced and in-house manufacturing. The report predicts a five-year CAGR of 6.9% for total assembly value. Hence the EMS market’s CAGR forecast is 4.7 percentage points greater than the CAGR for total assembly. Total assembly value amounted to $810.4 billion in 2005 and will hit $1.13 billion in 2010, according to ETP.

As the EMS world should know, the degree to which outsourcing providers have penetrated the total assembly market shows how much business potentially remains to be outsourced. Based on ETP’s forecast, outsourcing providers have not even come close to penetrating a majority of the assembly market. In 2005, the penetration rate was an estimated 23.4%, rising to 27.9% in 2009 and 29.0% in 2010 (see Table 1).

But it is unfortunate that researchers do not agree on penetration rates, which are so important to understanding the growth potential for the outsourcing business. Take market researcher Technology Forecasters, Inc. (Alameda, CA). Last year, the firm’s 2004-2009 forecast yielded a penetration rate of 18.8% in 2005, which increased to 23.7% in 2009 (Oct. 2005, p. 2-3). In large part, TFI and ETP differ on the size of the total market available to outsourcing providers.

ETP’s forecast for regional market share reflects a continuing migration of EMS production from high- to low-cost regions. However, ETP says this shift in production is starting to wane, as labor cost advantages are declining when weighed against total costs including transportation and logistics. As a result, the shift will take place at a more moderate pace than in the past, predicts ETP.

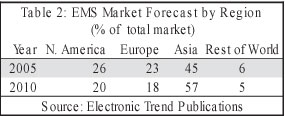

North America, Europe and the rest of the world will lose market share from 2005 to 2010, while Asia will gain share over the period, according to the forecast. North America’s share of the worldwide EMS market will decline from 26% in 2005 to 20% in 2010. Also, Europe’s slice of the outsourcing pie will shrink from 23% of the total market to 18%. In contrast, Asia will see its portion of the EMS market grow from 45% in 2005 to 57% in 2010 (Table 2).

Over the forecast period, the computer and communications segments will remain the first and second largest sources of EMS revenue respectively, according to ETP. In 2005, the computer industry accounted for an EMS market share estimated at 39%, which ETP expects will rise to 41% by the end of the period in 2010. The report projects that communications’ share of the market will increase slightly from 27% in 2005 to 28% in 2010. On the other hand, the consumer segment will lose share, starting at 15% in 2005 and ending up at 13% in 2010, according to ETP. The industrial and medical markets represented 7% and 6% of the 2005 market respectively, and ETP predicts that those percentages will remain unchanged in 2010. Commercial aviation, automotive and defense/other transportation combined for an estimated 6% of the market in 2005; these segments will finish the forecast period with a total share projected at 5%.

To compare 2005 performance of EMS companies and ODMs, the report uses a rating system based on a weighting of certain financial metrics. The highest rated company in 2005 was HTC, a Taiwanese ODM, followed by Elcoteq, an EMS provider based in Finland. HTC received high rankings in a number of categories including net income, ROA, ROE, revenue per employee, revenue per square foot, inventory turns and debt ratio.

The ETP report also contains profiles of 90 EMS companies and ODMs. For more information, email saberry@electronictrendpubs.com.

Gartner Dataquest also sees the EMS market exceeding $200 billion this year. According to a report in Electronic Business, Jim Walker, a Gartner Dataquest VP, estimated in a Semicon West speech this month that the EMS market would increase from $200 billion in 2005 to about $230 billion in 2006. In the report posted online, Walker attributed this increase to rapid growth on the consumer side.

Under a new relationship, Flextronics (Singapore) will gain a portion of Juniper Networks’ global outsourcing. Flextronics will provide some part of new product introduction, manufacturing and logistics services on a worldwide basis for Juniper’s security and networking products.

Juniper (Sunnyvale, CA) has manufacturing relationships primarily with Celestica and Plexus, according to Juniper’s most recent SEC form 10K. As Plexus’ largest customer, Juniper accounted for 19% of the provider’s sales for the quarter ended July 1.

MMI asked Juniper what effect this new relationship with Flextronics would have on Juniper’s two existing contract manufacturers. Juniper’s PR department released the following statement to MMI: “Plexus and Celestica remain valued partners and an integral part of Juniper’s supply chain. While we transition to our EMS providers in China to source products, Plexus and Celestica will continue to be important and significant partners to Juniper, and we believe we will continue to be a significant revenue contributor to them. We remain pleased with Plexus’ and Celestica’s performance and expect the companies to continue as responsive and cost-effective partners to Juniper Networks.”

During a July 27 conference call to discuss financial results, Dean Foate, Plexus president and CEO, described the Flextronics announcement as “old news.” He said Plexus has been working with Juniper for well over a year on its global manufacturing strategy. According to Foate, Juniper has a plan identifying “which products would move to Flextronics both from us and the other current provider to Juniper. And we also understand which products would likely come to Plexus.”

When Plexus looks ahead four to five quarters, the growth rate with Juniper “is looking slightly up,” said Paul Ehlers, president of Plexus Electronic Assembly, during the call. “That’s a combination of product shifts and end market growth that they’re projecting.”

More new business…Plexus (Neenah, WI) will serve as manufacturing subcontractor for 3D foot gauges, which the UK’s QinetiQ will supply to Clarks Shoes. Clarks recently awarded QinetiQ a £4.6-million ($8.6-million) contract for the foot gauges, intended for Clarks’ UK stores….Kimball Electronics Group (Jasper, IN), an MMI Top 50 EMS provider, has secured a contract to manufacture a material identification system for XStream Systems (Vero Beach, FL). Under the agreement, Kimball Electronics will assemble, test, service and repair the system, which is based on energy-dispersive x-ray diffraction….Top 50 provider PartnerTech (Malmö, Sweden) and Electrolux Laundry Systems (ELS), a division of the Electrolux Group, have expanded their relationship through a new agreement calling for PartnerTech to provide control units for professional laundry systems. Worth about SEK 60 million ($8.2 million) a year, the agreement extends PartnerTech’s production for ELS to China. PartnerTech already manufactures control units in Sweden and Poland for delivery to ELS units in Europe. The China operation will supply ELS’s new plant in Thailand, with initial production estimated at SEK 20 million ($2.7 million) a year. This agreement covers the entire product life cycle….Bantam Electronics (Austin, TX), a provider of custom manufacturing solutions and supply chain services, is taking over hardware manufacturing for irrigation control units of Acequia (Austin, TX), a supplier of irrigation water conservation solutions. Bantam is also providing parts and finished product inventory management, shipping and logistics services, and warranty/RMA support….LaBarge (St. Louis, MO) has received a $10.7-million contract to continue to provide Northrop Grumman with electromechanical subsystems and modules for an automated mail sorting system. Also, Raytheon Missile Systems has awarded LaBarge a $2.1-million contract to supply additional cables for the Joint Standoff Weapon system, a GPS-guided weapon launched by US Navy strike aircraft.

Two Taiwan-based news services are reporting that Hon Hai Precision Industry (Tucheng, Taiwan), the world’s largest EMS company, intends to enter the LCD TV assembly business.

Hon Hai, also known by its Foxconn trade name, has hired Lu Po-yien, a former executive with LCD panel supplier AU Optronics, as GM of Hon Hai’s LCD business, according to China Economic News Service (CENS) and DigiTimes.com. The two sources report that his duties will include overseeing Hon Hai’s LCD TV assembly business and the setup of 7.5-generation LCD panel production.

Innolux, a member of the Hon Hai group, is a supplier of LCD panels and monitors.

Meanwhile, Hon Hai plans to move the headquarters of its China operations from Shenzhen in southern China to Beijing in northern China, CENS reports.

This month, Hon Hai announced through statements posted on the Taiwan Stock Exchange a series of five indirect investments in China totaling $184.5 million. The funds are intended for Chinese companies in Jincheng, Shanxi province; Shenzhen, Guangdong province; Kunshan, Jiangsu province (two companies); and Yantai, Shandong province. Main business areas of these companies are chassis and stamping parts, sub-1000-volt plugs and sub-80-volt cable and components, notebook cases, computer components, and handsets and components. Hon Hai stated that it is making the investments to enhance its eCMMS (e-enabled component, module, move, service) model.

These latest capital inflows follow three indirect investments made in April totaling $123.8 million and a June investment of $30 million, all earmarked for Chinese companies. Therefore, since April Hon Hai has invested $338.3 million in China operations of affiliated companies.

New facilities…According to CENS, Hon Hai’s R&D center in Tucheng, Taiwan, is due to be finished this summer. The company broke ground on the project two years ago. Reportedly, Hon Hai will invest NT$12 billion ($367 million) in the center over three years….Plexus (Neenah, WI) plans to double the manufacturing footprint of its Xiamen, China, facility, which focuses on complex high-mix, mid-to-low volume production. An extension to the leased facility will add a three-story office and about 60,000 ft2 of production space, which will bring total capacity there to 120,000 ft2. The new addition is expected to be completed by mid-2007, and production is slated to begin 60 to 90 days thereafter….Inventec Appliances (Taipei, Taiwan), one of MMI’s Top 25 outsourcing providers, plans to invest up to about $4 million in a new operation in the Czech Republic to provide back-end assembly and close-to-market logistics for ODM customers….Elcoteq (Espoo, Finland) has increased its capacity in Pécs, Hungary, by leasing a further 7,000 m2 of storage and manufacturing space. The additional capacity will increase the number of employees in Hungary by roughly 10%....Incap (Oulu, Finland), a publicly held EMS provider, has begun shipments from its new factory building in Kuressaare, Estonia (March, p. 6). The 3,700-m2 building, which is leased, is triple the size of Incap’s old facilities in Kuressaare. The old premises will be used for box build as well as training. Incap employs 125 people in Kuressaare.

Top 10 EMS provider Venture (Singapore) proposes to acquire all the issued shares of publicly held GES (Singapore), an original design manufacturer of point-of-sale (POS) systems and other industrial applications. The deal will enhance Venture’s design capabilities in niche product areas and allow it to address a wider market segment.

Venture will pay S$1.25 in cash for each GES share. The maximum value of the deal is about S$980 million ($620 million).

In the March 2006 quarter, ODM activities in POS systems accounted for 67% of GES’s revenue, while 8% came from ODM business on the industrial side, including industrial controllers and metering products. GES also maintains an EMS business, which represented 25% of March quarter sales. Revenue in the quarter totaled S$157.1 million, up 11% year over year, and net profit increased 35% to S$13.1 million.

For the nine months ended March 2006, GES reported sales of S$497.6 million and net profit of S$39.8 million, amounting to 9% and 28% growth respectively. GES operates manufacturing facilities in China, Singapore, Malaysia and the US.

According to Venture, the acquisition is consistent with its focus on niche, high-mix businesses that also exhibit high growth and stable margins. The deal will allow both companies to cross-sell their products and services to an enlarged customer base.

In addition, Venture believes that combining the complementary design capabilities of the two companies will result in a range of design services that extends beyond existing offerings. Venture will also strengthen its position in the higher margin ODM business.

Economies of scale provide another reason to make this deal. Consolidation of purchasing volumes will enable the two companies to enjoy increased purchasing power and better management of the supply chain.

The transaction is expected to be earnings accretive to Venture shareholders.

Merger…Elitegroup Computer Systems, a Taiwan-based motherboard supplier, plans to acquire notebook ODM Uniwill Computer through a merger transaction in which two shares of Uniwill will be exchanged for one share of ECS. According to CENS, this deal will make ECS Taiwan’s sixth largest supplier of outsourced notebooks, with combined output expected to exceed 3 million notebooks in 2006.

European deals done…EMS provider Lövånger Electronik AB (Lövånger, Sweden) has acquired another Swedish provider, Elektronikprodukter i Järlåsa AB….TES Electronic Solutions (Langon sur Vilaine, France), a provider of design and manufacturing services, has acquired DAnalyse, a German firm that will be integrated with TES’s design center in Berlin, according to two Europe-based electronics publications. The acquired firm adds capabilities in process and device characterization, reports ElectronicsWeekly.com. …NOTE AB (Norrtälje, Sweden) has completed its acquisition of PCB design firm Nordic-PrintDesign AS (June, p. 5).

OTC-traded providers…TXP Corporation is now the official name for a Richardson, TX-based provider of pre-manufacturing services. Effective July 14, the company’s common stock is being listed on the Over-the-Counter Bulletin Board under the new symbol TXPO. TXP reflects an abbreviation for the company’s original operating division, Texas Prototypes. The company also operates divisions in photonics and packaging….The common stock of EMS provider Probe Manufacturing (Costa Mesa, CA) started trading this month on the OTC Bulletin Board under the symbol PMFI.OB. Probe is a low- to medium-volume EMS company offering NPI, collaborative design, materials management, product manufacturing, warranty repair, and end-of-life support. Sales for the March quarter amounted to $2.0 million, up from $1.4 million in the year-earlier period.

Benchmark Electronics (Angleton, TX). Q2 sales of $749.2 million were 13.5% above the high end Benchmark’s guidance and 33.6% higher than sales for the year-earlier quarter. Despite this growth, the company still managed to raise its non-GAAP operating margin to 4.7% in Q2 from 4.5% in the prior quarter. Benchmark reported double-digit growth year over year in all of its market segments. Q2 net income amounted to $27.5 million, up 47.2% from a year earlier. The company raised its 2006 guidance. Benchmark now expects sales between $2.76 and $2.85 billion and non-GAAP EPS of between $1.61 and $1.69. At guidance midpoint, 2006 sales growth would be 24%.

Elcoteq (Espoo, Finland). Sales in Q2 rose 5% year over year to 1,029.6 million euros. Q2 operating income was 12.2 million euros, down from 15.9 million euros in the year-ago period, while net income came to 4.4 million euros, versus 8.3 million euros in Q2 2005. Cash flow after investing activities went negative to -71.5 million euros. The company still maintains a positive outlook for Q3 and Q4. Previously, Elcoteq estimated that sales in 2006 would increase clearly faster than forecasted growth of roughly 10% for the EMS market in communications technology. The company is now projecting that 2006 sales will increase at the same rate as the market average. Behind this lowered forecast is a temporary decrease in demand in the Americas.

Flextronics (Singapore). The provider’s June quarter results exceeded its sales and earnings guidance for the quarter. Sales from continuing operations totaled $4.06 billion, up 6.2% year over year, while core EMS business increased by 11.6%. Non-GAAP net income increased by 4.1% from a year earlier to $103.7 million, as GAAP net income rose by 43.9% to $84.5 million. Non-GAAP operating margin improved to 3.1% from 2.9%. The cash conversion cycle was at 12 days. Flextronics’ CEO reported a “re-acceleration of significant growth in our core EMS business.” For the fiscal year ended March 2007, the company expects revenue from continuing operations to grow in the range of 25% to about $19 billion, and it estimates that non-GAAP EPS will increase in the range of 15% to about $0.80. The CEO said startup costs from accelerated growth create a drag on earnings.

Plexus (Neenah, WI). For the fiscal Q3 ended July 1, Plexus reported record sales of $397.4 million, up 26.7% year over year and 17.6% sequentially. Net income was $25.1 million, or $0.53 per diluted share, compared with a net loss of $21.5 million in the year-prior period. Gross margin reached 11.5% for fiscal Q3, and operating margin expanded by 75 basis points to 6.0%. Return on capital employed advanced to 34.0%. A new unnamed defense customer accounted for 10% of sales; this company joins Juniper and GE as 10% or greater customers. Plexus expects fiscal Q4 sales in the range of $390 to $405 million, corresponding to full-year growth of 18.3% to 19.5%. Fiscal Q4 guidance for diluted EPS before restructuring or special items is $0.46 to $0.50. In addition, Plexus’ CEO said the company’s value proposition and market focus support revenue growth of 15% to 18% in the next fiscal year.

Sanmina-SCI (San Jose, CA). Until a special committee of Sanmina-SCI’s board completes its investigation of the company’s stock option practices, the company is not providing detailed financial information for fiscal Q3 ended July 1 (June, p. 5-6). However, the company did report revenue for the quarter as $2.71 billion, up from $2.67 billion in the prior quarter, but down from $2.83 billion in the year-earlier period. Fiscal Q3 revenue was at the low end of company guidance. Earlier, Sanmina-SCI lowered non-GAAP EPS guidance for the quarter to a range of $0.06 to $0.07 from previous guidance of $0.08 to $0.10. The company attributed the shortfall in financial results to a less favorable product mix, less than expected profitability in the computing business, and slower than anticipated improvement in the enclosure business. New business won in the quarter totaled $600 million. Sanmina-SCI is targeting sales of between $2.7 and $2.8 billion for fiscal Q4.

More financial news…Jabil Circuit (St. Petersburg, FL) has completed a $200-million stock repurchase program authorized last month by its board of directors….PEMSTAR (Rochester, MN) has entered into lease settlement agreements that the company estimates will result in more than $2.5 million in restructuring provisions being returned to operating profits in the June quarter….For the fiscal year ended April 30, SigmaTron International (Elk Grove Village, IL) saw revenue increase 32% to $124.8 million. Net income amounted to $1.9 million, down from $4.7 million in fiscal 2005. Sales increased in the industrial electronics, life sciences, semiconductor and appliance segments, primarily due to the July 2005 acquisition of Able Electronics. However, this acquisition had a negative impact on fiscal 2006 profits.

People on the move…Solectron (Milpitas, CA) has named Marty Neese as executive VP of operations to fill the vacancy created when lean guru Marc Onetto resigned from the company (June, p. 7). A 15-year veteran of the EMS industry, Neese joined Solectron in 2004 and most recently served as executive VP, program management. Previously, he worked at Sanmina-SCI, where he oversaw all customer relationship activities, as well as Jabil Circuit....Nortech Systems (Wayzata, MN) has named Michael Jepson as GM of its Aerospace Systems division.

More restructuring…Plexus will close its Maldon, England, facility to reduce manufacturing capacity in the UK. Maldon production will be will transferred to the company’s facility in Kelso, Scotland….A Foxconn operation in Pécs, Hungary, is being closed, according to Hungarian source Hungary Around the Clock….Suntron (Phoenix, AZ) has decided to transfer its contract manufacturing business in Lawrence, MA, to other Suntron sites. Two other business units within the Lawrence facility will be unaffected by this restructuring.

Hon Hai’s site in Longhua, China, has recently been the subject of online “news” reports, many of them hinging on one bit of information from a June article in the Mail, a British newspaper. (See p. 3-4 in last month’s edition.) Online sources used this information – the pay ascribed by the article to a single female employee – as an indication of working conditions at the Longhua site. MMI believes that the worker’s pay reported in the article is suspect, and sources that relied on this pay did no good for themselves or the EMS industry.

It’s not that the Mail, or any other publication for that matter, doesn’t have the right to report on the operations of an EMS company such as Hon Hai. Indeed, the article’s premise, which was to show readers where the iPod is made and what goes into it, was valid. The public should understand the supply chain behind a product like the iPod.

However, the Mail’s conclusion that Hon Hai pays low wages by China’s standards is easily challenged. The article claimed that the worker earned about $50 a month for working 15-hour days, which Hon Hai says is false information. This alleged pay was well below the local government’s monthly minimum of $72.50 without overtime (which was subsequently increased). It makes no sense that Hon Hai would pay such a wage when there is a large shortage of workers in Southern China. If Hon Hai’s pay were substandard, workers would go elsewhere, and the company would be unable to sustain the pace of its rapid growth in China. Company management, which has made Hon Hai by far the largest EMS company worldwide, is much smarter than that. In fact, just the opposite is true. Hon Hai must offer workers a package of wages and benefits that will dissuade them from choosing another employer in the region.

Furthermore, if Hon Hai were underpaying workers, don’t you think that someone other than a British newspaper reporter would uncover this fact. After all, the Longhua operation has been audited by none other than HP, a prime mover in the Electronics Industry Code of Conduct. Given HP’s reputation for promoting social responsibility, one wonders how the operation could have passed HP’s audit if workers were mistreated in this manner.

As China’s largest exporter, Hon Hai is a big target for anyone on a crusade against sweatshops. That Hon Hai would leave itself open to sweatshop charges doesn’t ring true. The company would be burning its bridges with customers such as HP and Apple. Again, Hon Hai, it would appear, is too smart for that.

Still, the Hon Hai case does raise the question of whether national labor laws are being enforced locally. If Hon Hai is limiting overtime to 20 hours per week, as one executive is reported to have said, then in two weeks workers could exceed the national overtime limit of 36 hours per month. This is a question that goes well beyond Hon Hai to the Chinese government.

What’s bothersome about this case is not so much the Mail article – reporters are not perfect – but the way in which information from the article was picked up and spread over the Internet. Republishing this information without presenting Hon Hai’s side of the story was unfair to Hon Hai. Websites that engage in such activity merely repackage information gathered by others. They are not, in this writer’s opinion, legitimate sources of news for the EMS industry. Caveat emptor.

Nevertheless, Hon Hai could have made things easier on itself. The company did respond, but its side of the story was posted on the Taiwan Stock Exchange website, which is not easy to navigate. A press release issued by Hon Hai over a news wire would have helped its cause. Also, relationships with media outside Taiwan would have given Hon Hai other channels for its response.

While much attention has been given to worker pay, the article also leveled two other charges at Hon Hai. The female employee alleged that workers are made to stand still for hours, and that overtime is mandatory. A Hon Hai executive told a China source that the company doesn’t force employees to work overtime. Hon Hai also stated there is no incident where Hon Hai took advantage of labor.

Given the article’s allegations, Apple felt the need to respond. It has a reputation to protect and a supplier code of conduct to enforce. The company has launched what it describes as a “thorough audit” of Hon Hai’s iPod manufacturing plant in Longhua to ensure adherence to Apple’s code of conduct. One wonders if Apple would have done anything differently had the article not received so much play over the Internet.

Apple’s role should also be examined. The company implemented its supplier code of conduct last year, according to its website. To this writer, implementing the code means conducting supplier audits. Since Hon Hai is a major supplier to Apple, one would assume that Hon Hai would have been atop the list of companies to audit. It would seem that Apple had plenty of time to conduct an audit of the Longhua plant by now. If no prior audit was done, then one must question how effective Apple has been in implementing its code. On the other hand, if an audit has already taken place, why is there a need for another one? Neither scenario will buff Apple’s image.

If there is a moral to this story, it may be that relatively anonymous EMS companies can be engulfed in an unpleasant wave of Internet publicity, especially if the story involves a high-profile customer such as Apple. This is not to condone the practice of repackaging information and presenting it as news. But repackagers are an unfortunate product of the wired world. There is a reason why these websites stay in business. People use them. They provide a fast way to obtain information without having to hunt for the original source of it. Most of us, therefore, bear some responsibility for the existence of the Internet publicity machine.

Both OEMs and EMS providers should take heed. Being caught in that machine is generally not a good thing. The machine is looking for hot-button issues such as labor conditions in underdeveloped countries. One defense against becoming fodder for the machine is to have a supplier code of conduct fully implemented. It’s not a bulletproof defense. But it does leave a company less vulnerable to the kinds of allegations that have hounded Hon Hai.