![]()

![]()

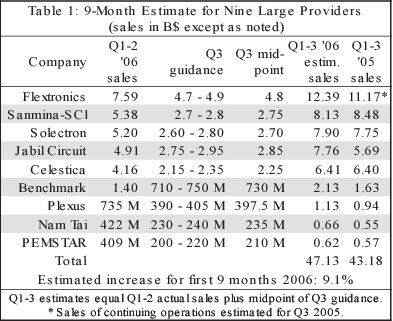

Based on guidance for Q3, combined sales for the nine largest US-traded providers are gaining momentum as providers enter the second half of 2006. MMI estimates that overall sales growth for these providers will amount to 9.1% for the first nine months (see Table 1). This nine-month rate represents a not-too-shabby doubling of growth from the first-half, in which sales increased by 4.6% (Table 2). For each provider, nine-month sales were estimated by adding the midpoint of the company’s Q3 guidance to its revenue for the first half.

Nevertheless, there is a wide disparity among projected growth rates for the first three quarters. Four of the nine US-traded providers have supplied guidance that will give them nine-month growth rates of 20% or better at guidance midpoint. They are Jabil Circuit, Benchmark Electronics, Plexus and Nam Tai Electronics. Two of these, Jabil and Benchmark, will exceed 30% growth in the first three quarters, if they at least reach the midpoint of their Q3 guidance. Jabil tops the list with a projected 36% growth rate at guidance midpoint.

In contrast, two providers, Solectron and Celestica, show little or no estimated growth through nine months, while sales for a third company, Sanmina-SCI, are projected to decline by 4% in the period.

According to MMI’s projections, the provider with the greatest change in growth rate from the first half to the first nine months is Flextronics. The company’s estimated nine-month growth rate of nearly 11% is 7+ points higher than its first-half rate (Table 2).

Nine-month projections reveal something else. The order of the top-five US traded providers is changing. When ranked by estimated nine-month sales, Jabil comes in ahead of Celestica, instead of behind Celestica as was the case for 2005 (March, p. 2). What’s more, Jabil’s sales are closing in on Solectron’s. Using these projections, one finds that Jabil’s revenue for the first three quarters is only about $140 million below Solectron’s level for the period.

Q2 sales for the nine largest US-traded providers showed significant sequential growth overall. Revenue for the nine totaled $15.86 billion in Q2, up 10.6% from the prior quarter (Table 2). Six of the nine companies posted double-digit growth quarter over quarter. Year over year, aggregate growth for Q2 amounted to 7.8%, with growth rates ranging from -4.3% (Sanmina-SCI) to 33.7% (Jabil).

Combined gross margin (GAAP) for Q2 represented eight providers instead of nine because Sanmina-SCI has not yet made its Form 10-Q filing of financial results for the fiscal quarter ended July 1 (see News section). Q2 gross margin amounted to 6.3% overall, unchanged from the year-earlier quarter. One provider, Plexus, enjoyed a gross margin of 11.4%; Plexus was the only company to hit double digits for this metric.

Q2 operating margin (GAAP), on the other hand, increased by 100 basis points in the aggregate. Together, the eight providers produced an operating margin of 2.5% for the quarter, up from 1.5% in the year-ago period. Nam Tai Electronics reported the highest Q2 margin at 9.4%, but this figure includes a $9.3-million gain on the disposal of assets held for sale. The second highest margin of 6.0% was posted by Plexus.

Net income (GAAP) for the eight providers in Q2 totaled $236.3 million, a 28% improvement over Q1. On a year-over-year basis, Q2 net income more than quadrupled. Only one provider, Celestica, posted a GAAP net loss for Q2 2006. A year earlier, three EMS companies reported losses. Aggregate net margin for this year’s second quarter was 1.8%.

Total net income for the first half of 2006 also showed dramatic improvement over a year earlier. The group of eight generated a combined first-half net income of $420.6 million, more than double the first-half total in 2005. Again, only one provider recorded a net loss for the first half of 2006.

Combined inventory for the group of eight expanded in Q2 in keeping with expectations for program ramps. Inventory at end of Q2 was up 18% from the prior quarter.

Since Sanmina-SCI did report its Q2 sales, one can compute first-half sales for the nine largest providers traded in the US. Together, they produced sales of $30.20 billion in the first half of 2006, compared with $28.87 billion in the year-earlier period. Three providers saw their sales decline in the first six months of 2006, while five companies experienced double-digit revenue increases of 15% or more.

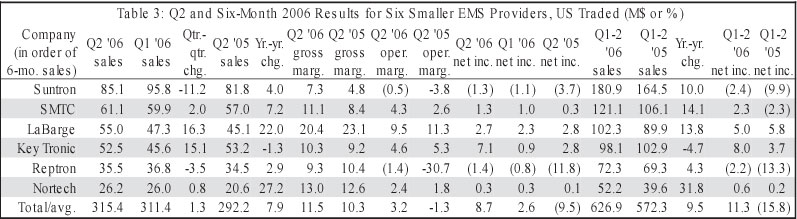

MMI also tracks performance of smaller providers that are publicly held (Table 3). Combined Q2 sales for six of these providers, all traded in the US, rose by 7.9% year over year, virtually the same increase produced by the nine large providers treated earlier. In Q2, two smaller providers, LaBarge and Nortech Systems, attained year-over-year growth rates above 20%, while the rest of their group produced single-digit growth or in the case of one provider a slight sales decline. The group’s sequential growth of 1.3%, however, was well below that put up by the larger companies.

In the EMS world, small is not always beautiful, but there are advantages to being a smaller provider. One of them is the ability to generate margins. Smaller providers often specialize in lower-volume, high-mix niches where margins are not so tight. Indeed, in Q2 the six smaller providers achieved a collective gross margin of 11.5%, compared with 6.3% for the large providers. The smaller-provider prize for the highest gross margin went to LaBarge, which racked up a margin of 20.4%. Overall gross margin for the smaller companies improved by 120 basis points from the double-digit level of Q2 2005.

When it came to operating margins, however, the difference between large and small was not as great in Q2. The group of smaller providers generated an overall operating margin of 3.2% versus 2.5% for the large companies. A year earlier, operating margin for the smaller providers was in the red as a result of one company’s operating loss.

Although the smaller companies managed to put up a combined Q2 net margin of 2.8%, two of them, Suntron and Reptron, reported net losses for the quarter. Note that this net margin is propped up by a $5.0-million deferred tax asset recognized by Key Tronic for its fiscal quarter ended July 1. Without this tax benefit, aggregate net margin for this group would have been 1.2%, which is below the 1.8% net margin generated by the eight large providers. Thus the smaller providers needed a tax credit to show that they were more profitable as a group in Q2 than the large companies.

For the first half of 2006, aggregate sales of the six smaller providers grew more than twice as fast as that of the nine large providers. The six smaller companies combined for sales of $626.9 million, which represented an increase of 9.5% over the same period a year ago. This growth rate was more than double the large-provider rate of 4.6%. Among the smaller providers, first-half sales growth ranged from -4.7% (Key Tronic) to 31.8% (Nortech) year over year.

The bottom-line result for the smaller providers swung from a collective net loss of $15.8 million in the first half of 2005 to net income of $11.3 million in the first six months of this year. Five out of six companies improved their bottom lines, but two of these (Suntron and Reptron) remained in the red for the first half of 2006.

A new agreement with Eastman Kodak (Rochester, NY) will make Flextronics (Singapore) a major producer of digital cameras. Under this new agreement, Flextronics will manufacture and distribute Kodak consumer digital cameras on a global basis and will handle certain camera design and development functions. This move is in line with Kodak’s emphasis on margin expansion for its consumer digital business.

Kodak will outsource its entire digital camera manufacturing requirements to Flextronics, including assembly, production and testing. Flextronics will also manage operations and logistics services for Kodak’s digital still cameras. Kodak will retain its intellectual property; will continue to develop high-level system design, product look and feel, and the human interface; and will conduct advanced R&D for its digital still cameras.

The deal includes Flextronics purchasing select manufacturing assets for about $35 million in cash, and about 550 employees are expected to move from Kodak to Flextronics.

Flextronics will obtain the digital camera manufacturing, assembly and warehousing requirements and related employees of Kodak Electronics Products, Shanghai Co. Ltd. in China. As a result, Kodak camera production will be transferred to a Flextronics facility in China. Flextronics will also acquire a significant portion of the Kodak Digital Product Center, Japan, Ltd. in Chino and Yokohama, Japan, along with associated camera design functions and employees. Subject to regulatory approvals and other conditions, closing is expected to occur during Q3 2006.

“With Flextronics taking over these activities, we will achieve our goal of maximizing the variable cost component of this business in a more flexible, lower cost, less capital intensive method of serving this market,” said Antonio Perez, Kodak’s chairman and CEO, during an Aug. 1 conference call with analysts. He said Flextronics gives his company scale in purchasing and in low-end product manufacturing that Kodak does not have. Flextronics also brings to the party a logistics system “perfectly designed to deal with this type of products,” added Perez. He said Kodak, lacking such a system, has no desire to build one.

“The expansion of our business relationship with Kodak adds significant strategic value to Flextronics’s Consumer Digital market segment. The design expertise we will acquire from Kodak’s operations in Japan and the transferring of its production into our China facility will broaden the scope of the competitive services we can provide on a global scale as well as leverage operating efficiencies for both companies,” stated Greg Westbrook, president of Flextronics’ Consumer Digital market segment.

This is Flextronics’ second deal this year in the digital camera arena. Earlier, the company acquired digital camera developer World Wide Licenses Limited (Feb. p. 6). Archrival Hon Hai Precision Industry (Tucheng, Taiwan), otherwise known as Foxconn, has also staked a claim in the digital camera business with its plan to acquire Premier Image Technology, the largest digital camera maker in Taiwan (June, p. 3).

While the two largest EMS providers are looking to build outsourcing businesses in digital cameras, there are mixed signals about the growth of the digital camera market. Kodak, for one, believes that digital camera revenue worldwide peaked in 2005 and that unit volumes will reach their zenith this year. In contrast, Taiwan-based Market Intelligence Center (MIC) sees global unit growth continuing. According to a recent report in the Taipei Times, MIC forecasts that shipments of digital still cameras will increase to 102.3 million units in 2007 from an estimated 95.3 million units this year.

Kodak’s sales of consumer digital capture products, which include digital cameras, accessories, memory products, imaging sensors, and royalties, decreased 15% in Q2 versus the year-earlier quarter, primarily reflecting volume decreases and unfavorable price/mix. Through May, Kodak maintained a top-three market share for consumer digital cameras worldwide, according to the company’s most recently filed Form 8K.

Digital capture products in turn are part of the Consumer Digital Imaging Group, which also includes kiosks and media, home printing and consumer digital services. For Q2, Consumer Digital sales amounted to $628 million.

Kodak’s Perez reported that since 2003 the company has pursued an “asset-light strategy” for manufacturing within its consumer business. That means concentrating on the upper end of the supply chain and looking for partners with greater scale and flexibility. “We’ve done a lot of that in kiosk already, and we are in the same path with every other single thing that we do including CMOS [sensors],” he said.

In an MMI exclusive, Flextronics has confirmed that it acquired Iwill (Taipei, Taiwan), a manufacturer of motherboards, security appliances, and barebones servers and workstations. The deal puts Flextronics in the motherboard business, an activity that the company had avoided under former CEO Michael Marks. At one time, he told investors that Flextronics did not want to enter the motherboard business because of the inventory requirements.

But times change, and Flextronics informed MMI that the company now has a good reason to develop a motherboard capability. “Over the last 9 to 12 months, our Computing team has been focusing on building a world-class mechanical design and system integration capability while utilizing partnerships with various motherboard companies to provide solutions to our OEM customers. We have now been very successful with this system integration capability that we have built at our design center located in Taiwan and have been encouraged by several of our customers to develop a motherboard capability to provide an even better product solution,” reported Sean Burke, president of Flextronics’ Computing market segment.

It turns out that Iwill was one of the motherboard partners that Flextronics used for system integration in its Computing segment.

“The early partnership [with] and now acquisition of Iwill will provide our customers with additional alternatives to improve their competitiveness as well as opening the door to opportunities for Flextronics that we would have previously not been considered for,” Burke added.

By acquiring a company with the ability to design high-performance (dual processor) motherboards, Flextronics has put together an ODM capability in computing that it did not have before. But now there is a question to be answered. What sort of computing products will Flextronics target for ODM projects? Will Flextronics concentrate on high-performance computing, or will the company also pursue commodity desktop products? Stay tuned.

Flextronics, which has divested several non-core businesses, has sold yet another unwanted unit. The provider sold the assets of Flextronics Photonics (Hillsboro, OR) to nLight (Vancouver, WA), a manufacturer of high-power semiconductor lasers.

The acquired packaging design and high-volume manufacturing builds on nLight’s current capabilities, according to a statement from the company.

For Flextronics, this sale means that the company is withdrawing from the photonics business, which suffered through the protracted downturn of the telecom industry.

More EMS business…Flextronics’ Youngsville, NC, operation will gain business from Parata Systems (Durham, NC), a Flextronics customer known for its automatic prescription dispensing system. After acquiring McKesson’s Automated Prescription System (APS) unit, Parata will move production of APS products from Alexandria, LA, to North Carolina. Of the 75 new jobs to be added in North Carolina, ten will be in manufacturing and will go to Flextronics’ facility in Youngsville. According to the Triangle Business Journal, $5 million worth of equipment will be transferred from the Louisiana operation to Flextronics in Youngsville….Jabil Circuit (St. Petersburg, FL) will manufacture in the US a color reader for PreMD’s skin cholesterol test for assessing the risk of heart disease. PreMD is a predictive medicine company based in Toronto, Canada….Retailer Target has chosen Top 50 EMS provider Alco Electronics (Hong Kong) as exclusive supplier of Target’s TruTech brand of LCD TVs. In cooperation with Target buyers, Alco designed and delivered an assortment of LCD TVs within six months of the go-ahead date. Alco has also developed various consumer electronics products for Wal-Mart stores under the Durabrand and ilo brands and has also supplied Best Buy, Circuit City and RadioShack. Recently, Alco started delivering XM Satellite radios to Harley Davidson for the motorcycle after market.…The Atlanta, GA, facility of PartnerTech (Malmö, Sweden) has begun production of new chemical and explosives detection devices for Isonics (Golden, CO). The handheld and portable units utilize Ion Mobility Spectrometry technology that identifies trace amounts of deadly substances such as Sarin and mustard gas, as well as explosives….ZTEC Instruments (Albuquerque, NM) has named LaBarge (St. Louis, MO) sole supplier of PCB assemblies, and initial orders are valued at about $1.6 million. These PCBAs go into oscilloscopes, waveform generators and digitizers that constitute ZTEC’s modular instrument platform….TXP (Richardson, TX), a provider of pre-manufacturing services, has delivered its first 300-pin transponder product for Essex (Columbia, MD), a supplier of optoelectronic imaging and signal processing solutions. TXP-Photonics will provide a variety of prototyping and optical assembly services, including material procurement, PCB assembly, back-end optical assembly and testing, and product shipment for Essex’s Commercial Communication Product Division.…Enablence Technologies (Ottawa, Canada) has selected Advantech Advanced Manufacturing Services (Cornwall, Ontario, Canada) to serve as Enablence’s local contract manufacturer, responsible for the production of low to medium volumes of the company’s fiber-to-the-home modems.

Publicly traded IPTE (Genk, Belgium), an EMS provider and a supplier of PCB and final assembly automation equipment, and Barco (Kortrijk, Belgium), a developer of visualization products, have signed a letter of intent by which Barco proposes to sell the Electronic Manufacturing activity of Barco Manufacturing Services division to IPTE.

Electronic Manufacturing is the surface mounting activity of Barco Manufacturing Services and generates 60 million euros in annual sales. The activity has manufacturing sites in Poperinge, Belgium, and Kladno, the Czech Republic, and employs about 400 people.

The proposed sale reflects Barco’s strategy not to invest any further in its contract manufacturing activity. As for IPTE, the deal is in line with its strategy to expand its Connect Systems activity.

Both parties expect a final decision regarding this transaction by the end of September.

For fiscal 2005, IPTE posted sales of 127 million euros, 78 million of which came from its contract manufacturing activity.

Apple has reported the findings of its audit of Hon Hai Precision Industry’s manufacturing site in Longhua, China, where Apple iPods are assembled. The audit followed the June publication of a British newspaper article that was picked up by online sources. This article in the Mail newspaper alleged poor working conditions and questionable dormitory living at Hon Hai’s Longhua site. (See June, p. 3-4; July, p. 7-8.) Apple’s investigation found that Hon Hai complies with Apple’s Code of Conduct in the majority of areas audited, according to a report posted on Apple’s website. However, Apple did find violations to its Code of Conduct, as well as other areas that the company is working with Hon Hai to improve.

Worker compensation was among the items on Apple’s audit list. The company’s investigation confirmed that all workers earn at least the local minimum wage, and Apple’s sample audit of payroll records showed that more than half were earning above minimum wage. This finding dispels a charge in the Mail article, which claimed that Hon Hai was paying wages below China standards.

However, Apple did find that the pay structure was unnecessarily complex, making it difficult for employees to understand. This structure fell short of Apple’s Code of Conduct, which requires that a supplier must clearly convey how it pays its workers. According to Apple, Hon Hai has since implemented a simplified pay structure that meets the Code of Conduct.

The audit also discovered that the process for reporting overtime, while not a violation of the Code, was subject to human error and relied too much on memory for dispute resolution. To address this issue, Hon Hai will link the payroll system and electronic badge system, which will automate the recording of hours worked and pay calculations.

Overtime was another area investigated. The Mail article interviewed a Longhua worker who said employees must work overtime if they are asked to. But Apple found no instances of forced overtime, and employees confirmed in interviews that they could decline overtime requests without penalty.

Still, the audit revealed that employees worked longer hours than permitted by the Code of Conduct, which limits normal work weeks to 60 hours and requires at least one day off each week. Apple reviewed seven months of records from multiple shifts of different production lines and found that the weekly limit was exceeded 35% of the time, and employees worked more than six consecutive days 25% of the time. Although the Code allows overtime limit exceptions in unusual circumstances, the company considered these percentages excessive.

According to Apple, Hon Hai has enacted a policy to enforce the weekly overtime limits set by Apple’s Code, and a management system is in place to track compliance. Supervisors must receive approval from upper management for any deviation.

Apple also looked at worker treatment. In the Mail article, a Longhua employee reportedly said that if female employees broke the rules by moving around, they would be made to stand still for longer periods as punishment. During interviews with employees, auditors asked every line worker whether they had ever been subjected to or witnessed objectionable disciplinary punishment. The audit team interviewed over 100 randomly selected employees, of which 83% were line workers. Two employees reported that they had been disciplined by being made to stand at attention.

While Apple did not find this practice to be widespread, the company says it has a zero tolerance policy for any instance, isolated or not, of any treatment of workers that could be interpreted as harsh. The company reported that Hon Hai has launched a manager and employee training program to ensure such behavior does not occur in the future.

As for labor standards, the audit team found no evidence whatsoever of the use of child labor or any form of forced labor. During this review, auditors examined security records with the aim of uncovering false identification papers.

The audit also included the working and living environment of the Longhua campus, which, according to Apple, supports over 200,000 employees. (Apple uses less than 15% of that capacity.) Auditors inspected a wide range of dormitories, both Hon Hai-owned and off-site leased facilities that together house over 32,000 people. No violations of the Code of Conduct turned up in the audit of on-site dormitories. Contrary to what was reported in the Mail article, visitors are permitted in the dormitories, although a sign-in process is required for security purposes.

But Apple was not satisfied with the living conditions at three off-site leased dormitories, which have served as interim housing during a period of rapid growth. Two of the dormitories, originally built as factories, now contain a large number of beds and lockers in an open space. Apple felt this environment was too impersonal. The third building held triple bunks, which in Apple’s opinion didn’t provide reasonable personal space. To address this temporary housing issue, Hon Hai is building new dormitories that will increase total living space by 46% during the next four months. This project was underway before the audit.

For future auditing, Apple has engaged the services of Verité (Amherst, MA), a non-profit organization whose mission is to ensure safe, fair and legal working conditions around the world. Apple sought this help because it recognized that some aspects of workplace auditing such as health and safety lie beyond the company’s current expertise. The company said it will complete audits of all final assembly suppliers of Mac and iPod products this year.

In addition, Apple has joined the Electronic Industry Code of Conduct Implementation Group, whose members include the six largest EMS providers.

New China facilities…Benchmark Electronics (Angleton, TX) intends to bring up its second China plant in the second quarter of 2007 (April, p. 6). The provider expects that the capital expenditure for the new plant will be in the $12- to $15-million range. This new building will have a “pretty significant box build capability,” said Benchmark president and CEO Cary Fu during the company’s July conference call. The company operates 115,000 ft2 in Suzhou….Nam Tai Electronics (Tortola, British Virgin Islands) plans to construct a new factory complex in Wuxi, located in China’s Jiangsu Province. The company believes there is a huge potential opportunity in the eastern coastal region of China. This expansion plan is subject to the local government’s final approval of an environmental license….Kimball Electronics Group (Jasper, IN) has also targeted Jiangsu Province. KEG, the EMS subsidiary of Kimball International, has opened a 132,400-ft2 manufacturing facility in Nanjing, the capital of Jiangsu Province. In addition to providing PCB assembly, system subassembly and final product assembly, the new facility will supply engineering services along with supply chain support for all KEG facilities. KEG said it is in the final planning stages for two different programs with existing automotive and industrial customers that are committed to the China operation. According to KEG, the location of this operation takes advantage of a highly qualified work force, well established logistics for exporting products, and proximity to industries served.

Facility acquisition…Nortech Systems (Wayzata, MN) has completed the acquisition of a 140,000-ft2 manufacturing facility in Blue Earth, MN, from Telex Communications (Feb., p. 8). The acquired facility will provide Nortech with the space necessary for its fast-growing Aerospace Systems division.

Since the investigation of stock option practices at Sanmina-SCI (San Jose, CA) is not complete, the company has been unable to file its Form 10-Q for the quarter ended July 1 (July, p. 6; June, p. 5-6; May, p. 8). As a result, NASDAQ has notified the company that it is not in compliance with NASDAQ rules for continued listing. In addition, the trustee for holders of two Sanmina-SCI notes totaling $1 billion in principal has informed the company that it has violated certain covenants as a result of its failure to file Form 10-Q.

While the investigation by a special committee of Sanmina-SCI’s board is still ongoing, the committee’s preliminary review has discovered potential discrepancies between the actual dates of measurement used for accounting purposes and the recorded grant dates of certain stock option awards. As a result, the company cannot determine yet the financial impact to its financial statements including the amount of any non-cash stock compensation charges, any resulting tax, or which accounting periods might be affected.

The special committee is investigating stock option practices dating back to January 1, 1997. It is being assisted by independent outside legal counsel and accounting consultants.

Sanmina-SCI has requested a hearing before the NASDAQ Listing Qualifications Panel. Pending a decision by the panel, the company’s shares will remain listed on the NASDAQ Stock Market.

In addition, the company is asking the aforementioned note holders for a waiver, until Dec. 14, 2006, of any default that might arise from the company’s failure to file with the US Securities and Exchange Commission and furnish certain reports to the trustee and note holders. Sanmina-SCI is offering consent fees totaling as much as $12.5 million if all note holders accept the waiver offer. Without the waiver, the trustee and certain holders have the right to accelerate the maturity of the notes, if the company has not made that SEC filing by Sept. 14.

The company has already received a waiver from its credit line lenders. This waiver extends through Sept. 5 or one day prior any obligation to prepay any notes, whichever is earlier. Receivables purchasers have given Sanmina-SCI a waiver through Oct. 10.

Other financial news…According to a report in DigiTimes.com, Hon Hai Precision Industry, the world’s largest EMS company, has joined two other groups to make a combined investment of $1.5 billion in a joint venture involving chemical production and the plastics-chemical and energy industries in China. A Hon Hai spokesman told DigiTimes.com that this investment in Shanxi is aimed at furthering Hon Hai’s vertical supply chain. …Celestica (Toronto, Canada) recently sold its plastics injection molding business, which operated primarily in Asia and represented less than 1% of total operations. The company obtained this business as part of its 2001 acquisition of Omni Industries. …Kimball International saw Q2 sales of its Electronic Contract Assemblies segment (Kimball Electronics Group) reach $173.0 million compared with $108.0 million in the year-earlier quarter. Two acquisitions closed in Q2 2006 contributed sales of $61.5 million in the quarter. Segment net income from continuing operations increased $2.0 million from the same period a year ago.

People on the move…Koo Ming Kown, founder of Nam Tai Electronics, will retire as the company’s non-executive chairman on Dec. 31, 2006. He plans to remain a board member until Nam Tai’s next general meeting in June 2007. On Jan. 1, 2007, Charles Chu, a non-executive director, will succeed Koo as non-executive chairman….Eric Miscoll, former COO of industry consulting firm Technology Forecasters Inc., has joined TXP (Richardson, TX) in the newly created position of vice president. His responsibilities for the pre-manufacturing services provider will include corporate strategy, operational structure and management, business development, and marketing. In addition, TXP has hired Robert Walden as chief information officer, also a new position. Most recently, he served as chief architect and manager for emerging technologies at 7-Eleven. Another new hire, David Heim, has joined TXP as director of design for manufacturability. Heim has over 20 years of electronics industry experience; for example, he was director of supply chain for Dallas Semiconductor.

Assembly discounts…Screaming Circuits (Canby, OR), which specializes in quick-turn prototyping and short-run PCBA, is now offering discounts on assembly services to universities and non-profits involved in research projects related to communications, robotics, control or similar 21st century technologies. The program will accept a limited number of qualified organizations. Screaming Circuits is a division of Milwaukee Electronics Companies (MEC).

Provider rating system…Recently, Technology Forecasters Inc. (Alameda, CA) released customer ratings for 16 EMS providers and ODMs from around the world. TFI conducted interviews with nearly 150 outsourcing executives/managers. Ratings appear in the first edition of the EMS/ODM Report Card and Buyers’ Guide. TFI analysts asked customers to rate their three largest suppliers by spending in five performance categories. According to TFI, outsourcing decision makers have “until now been without benefit of a third-party, objective rating system for the world’s major suppliers.”

Correction…The July edition’s page-one list of articles contained a keyboarding error in one headline. The headline should have read, “Flextronics Wins Business from Juniper.”

The EMS business like other industries has developed its own argot. This unique language serves at least two purposes. First, it separates those who know the meaning of these expressions, i.e., people with industry experience, from those who have little or no background in the business. Industry argot offers a quick way to assess how familiar a person is with the EMS business. If a new business contact starts talking about facility expansion when you ask about push-outs, then you know that person is probably a newbie. The second reason for using argo is that often provides a shorthand description for things that industry people commonly refer to. Rather than saying a customer increased its demand above the forecasted level, you would merely use the word upside. Argot has its place, but sometimes it can outlive it usefulness. MMI believes that the expression tier 1, and its corollaries, tier 2, 3 and 4 are terms whose time has come and gone.

The basic problem with the tier system today is that its distinctions have lost any precision that they might have had. At the turn of the century, there was no question about who the tier-1 providers were. The industry’s six largest EMS companies were in a class by themselves. Back then, these providers formed a top tier because they had a scale and global footprint that others did not possess. In 2000, it took sales of about $4 billion to make the industry’s first tier. But if you applied that cutoff as of the end of 2005, there would be seven providers in tier 1 (March, p. 2). Yet most people today still think of tier 1 as representing the six largest providers.

Some might argue that tier 1 by definition continues to refer to the six largest EMS providers. But why set apart the six largest EMS companies? If scale and global footprint are the criteria, six is an artificial distinction. More than six companies fit that bill. The so-called tier-1 providers aren’t the only ones with a global footprint that extends to low-cost geographies.

Definitions become even murkier once you venture below the top tier. What distinguishes a tier-two provider from a tier-three? MMI frankly has never been clear on this point. Are the dividing lines between the tiers based on revenue? If so, using revenue to divide tier two from tier three is purely arbitrary. You cannot say that a $600-million-a-year provider, for example, belongs a category separate from a $450-million provider. Footprints don’t work either. There are providers that have a more global footprint than some of their larger peers.

The tier system should be retired. It no longer serves as useful argot. If people want to continue to group the six largest providers, they can still do so. But the argot should be top six, not tier 1.