![]()

![]()

Although the nine largest US-traded EMS providers did not light up the sky with their combined growth in the first half of 2006 (see Aug., p. 1-2), rolled up results for a larger group of publicly held providers, comprised of both EMS companies and ODMs, point to an outsourcing trend that remains robust.

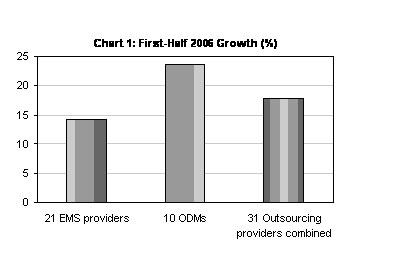

A tally of first-half 2006 sales for 31 large providers of outsourcing services showed aggregate first-half growth of 17.8% from the year-earlier period. A growth rate of 17.8% growth is not only healthy, it exceeds long-term CAGR forecasts that have been made been for the outsourcing business of EMS plus ODM offerings (July, p. 3). This global outsourcing group, consisting of 21 EMS providers and 10 ODMs, produced combined sales of $87.0 billion for the first six months, up from $73.8 billion in the first half of 2005.

As in the past, ODMs enjoyed an advantage when it came to sales growth. The subgroup of 10 Taiwanese ODMs generated an overall growth rate of 23.6% in the first half, based on consolidated results converted into US dollars. (Sales in non-US currencies were converted to US dollars by using six-month averages based on monthly data from the US Federal Reserve.) Combined first-half growth in US dollars for the 21 EMS providers amounted to 14.3%, 9.3 percentage points below the ODM rate (See Chart 1).

This growth rate disparity indicates that ODMs continue to take market share from their EMS counterparts. Propelled by higher rates, ODMs have come a long way in the last five years or so. In fact, 2006 marks a milestone of sorts for them. The 10 large ODMs tracked by MMI now account for more sales than do the nine largest US-traded EMS providers. Take away the smallest ODM for a nine-on-nine comparison, and the ODMs still win by over $3 billion. It is somewhat ironic that the outsourcing business, once defined by the US-traded EMS companies, now finds them behind these large ODMs in terms of revenue (Table 1).

Still, the EMS industry taken as a whole outsells the ODM side by a considerable margin. For the first half, the 21 EMS providers totaled $52.5 billion in revenue, compared with $34.5 billion for the 10 ODMs. EMS sales represented 60.3% of the first-half outsourcing revenue compiled by MMI.

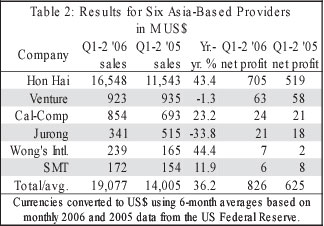

In addition to the nine US-traded providers, the EMS group included six Asia-listed companies and six Europe-based firms. Asia-listed providers had by far the highest first-half growth rate thanks to Hon Hai Precision Industry, the world’s largest EMS provider, which continues to defy conventional wisdom by producing high growth despite its massive size (Chart 2).

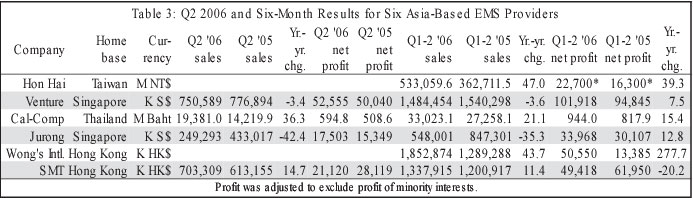

For the first half, Hon Hai’s consolidated sales reached $16.5 billion, up 43.4% in US-dollar terms (47.0% in NT dollars). (See Tables 2 and 3.) These results include the company’s handset subsidiary, Foxconn International Holdings, which recorded first-half revenue of $4.4 billion, representing a gain of 86.4% from the year-earlier period. (At this level, FIH would be a top-six EMS provider in its own right.) Hon Hai’s bottom line nearly kept pace with revenue growth, as first-half earnings (adjusted to exclude profits of minority interests) increased 35.9 % in US dollars (39.3% in NT dollars). The company’s operating margin for the first half of 2006 remained virtually unchanged from the year-earlier margin of 5.6%.

Given Hon Hai’s consolidated sales for the first half and the expected seasonal effects of the second half, MMI expects that the company will easily surpass $30 billion in revenue for 2006, further distancing itself from its nearest EMS competitor. Merely matching first-half revenue in the second half would put Hon Hai at $33 billion for the year. Hon Hai’s size means that its numbers have the weight to skew results for the entire EMS industry. As mentioned earlier, the 21 EMS providers grew sales at an aggregate rate of 14.3% in the first half. But without Hon Hai, combined growth dropped almost 10 points to a less appealing 4.6%, the same rate produced by the US-traded companies. Excluding Hon Hai, first-half growth rates among the Asia-, Europe- and US-traded groups varied between 2.7 and 5.8% (Chart 3). Hon Hai’s rapid growth in the first half stands in stark contrast to these averages. It’s almost as though Hon Hai obeys rules different from those that apply to the rest of the industry.

What is Hon Hai’s secret? Part of the answer may lie in Hon Hai’s model. Some aspects of its model – vertical integration of items such as connectors and magnesium cases and a substantial motherboard business – diverge from the rest of the industry. But underneath it all, MMI believes there is one constant theme for winning business: to be the low-cost producer. This strategy has won Hon Hai blue chip customers that continue to contribute to its growth.

Demand for low-cost Asian operations is transforming the EMS industry. So it is natural to look for revenue growth in Asia-based providers. But not every Asia-listed provider posted first-half growth. Venture, which replaced high-volume telecom business with high-mix accounts, reported a slight year-over-year decline in sales for the period. Jurong Technologies experienced a substantial drop in the first-half, largely due to the transition of certain wireless programs from turnkey to consignment as well as lower volumes in line with seasonality (Tables 2 and 3). Still, four out of six companies in the Asia-listed group enjoyed double-digit sales growth in the first half, and Wong’s International joined Hon Hai as the second company with revenue growth above 40%. All the Asia-traded providers except Surface Mount Technology (Holdings) Limited increased first-half net earnings from the same period a year ago. Wong’s took top honors for the greatest improvement in earnings.

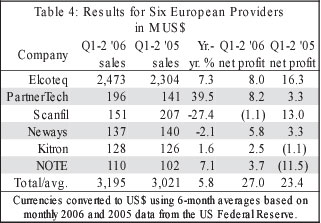

Like the Asian group, the six Europe-traded companies are dominated by one EMS provider. Elcoteq accounted for 77% of the European group’s revenue expressed in US dollars (Tables 4 and 5). Although the group only averaged a 5.8% revenue gain for the first half, PartnerTech increased its first-half revenue by 39.5% in US dollars, or 48.6% in SEK (Swedish krona). Counting comparable units only, the SEK increase was 20.5%. Therefore, more than half of the SEK gain, or 28.1%, stemmed from acquisitions. PartnerTech acquired a Finnish provider in 2005 (June 2005, p. 5-6) and a Norwegian contract manufacturer in 2006 (Feb., p. 6-7).

Of the six European providers, only telecom-heavy Scanfil saw a drop in first-half sales from a year earlier. Telecom customers accounted for about 73% of first-half sales. The provider is shutting down its Belgian plant and will dismiss most of the employees in its Oulu, Finland, plant. On the other hand, Scanfil is adding production area in Estonia and Hungary (see News, p. 7) and is planning to buy more equipment for its China operation.

Scanfil’s net earnings for the first half declined year over year as did Elcoteq’s. But the other four European providers increased their earnings (Tables 4 and 5). What’s more, combined net profit for the European group in the first half improved by 15.5% in US dollars, well above aggregate sales growth of 5.8%. NOTE made the largest gain in earnings from a year earlier.

Although Elcoteq’s first-half sales registered a 12.2% gain as expressed in euros, the company does not expect to maintain double-digit growth for the full year, according the company’s latest guidance. Elcoteq now estimates a full-year sales increase of around 5% with operating income below last year’s level. Previously, the provider forecasted that sales would grow by about 10% in 2006, and operating income would improve slightly from 2005 (July, p. 6). The company said it lowered guidance mainly because of weaker than expected development of manufacturing volumes in Europe and unsatisfactory profit growth in the Americas.

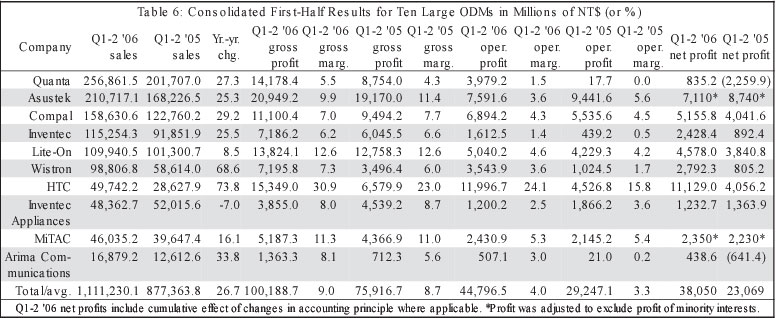

ODMs in the MMI group not only grew their first-half consolidated sales by a healthy amount on a combined basis but also improved margins overall. Aggregate gross margin for the ODMs’ first half went up by 30 basis points year over year to 9.0%, while operating margin increased by 130 basis points to 4.0% (Table 6, p. 4). The company with the highest margins by far was High Tech Computer. Only Quanta Computer and Inventec reported first-half operating margins below 2%.

The ten ODMs tracked by MMI continue to enjoy a margin advantage over their EMS counterparts. For the first half, eight large US-traded providers (excluding Sanmina-SCI) yielded an average gross margin of 6.1%, or 290 basis points below the ODM average. The US-traded operating margin for the period amounted to 2.2% overall, down 180 basis points from the ODM figure.

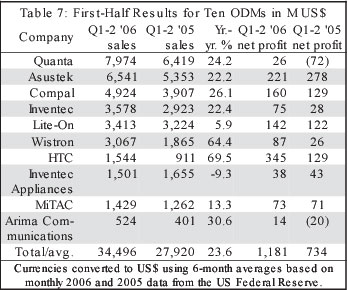

While the group of ten ODMs combined for first-half sales growth of 23.6% in US dollars (26.7% in NT dollars) year over year, two companies, Wistron and High Tech Computer, delivered increases above 64% (68% in NT$). (See Tables 6 and 7.) Only one ODM, Inventec Appliances, experienced a revenue decline for the period.

ODM net profits in the first half increased much faster than sales did. Aggregate net profit grew 60.9% in US dollars (64.9% in NT$) versus the year-earlier period. (In two cases, earnings were adjusted to exclude profits of minority interests.) All the ODMs were profitable in the first half, but two of them – Asustek Computer and Inventec Appliances saw net earnings decrease from a year ago.

Net profits of the 30 outsourcing providers (sans Sanmina-SCI) can be rolled up in US dollars from the three EMS groups and the ODM group (Table 8). These companies together accounted for first-half profit of about $2.5 billion, which corresponded to a year-over-year increase of some 58%. Based on this number, one could conclude that the outsourcing business as a whole grew significantly more profitable in the first half. Collectively, the eight US-traded providers (excluding Sanmina-SCI) showed the greatest improvement in profits. While the EMS and ODM groups achieved comparable increases in net profit, the ODM group’s net margin of 3.4% for the first half of 2006 was 70 basis points higher than the EMS group’s margin. Overall net margin for the 30 outsourcing providers stood at 3.0% for period.

Editor’s note: At least two Taiwanese companies, Asustek and Hon Hai, follow a hybrid business model serving both OEMs and the channel. As such, their sales and profits are not limited to outsourcing. Unfortunately, these companies do not break out sales to the channel. In addition, vertically integrated providers sell components to non-outsourcing customers. By counting total company sales and profits, this analysis has included some revenue and earnings that cannot be attributed to outsourcing. Therefore, rolled-up results are approximations of outsourcing revenue and profits.

Flextronics (Singapore) aims to add small-form-factor liquid crystal displays to its vertical integration capabilities for cell phones and other products equipped with these LCDs. The provider has entered into a definitive agreement to acquire International DisplayWorks, or IDW (Roseville, CA), which specializes in the manufacture and design of small-form-factor LCDs, LCD modules and assemblies for applications including cell phones, MP3 players, industrial and commercial products, and eventually digital cameras. Among other things, the deal will give Flextronics the ability to manufacture passive matrix LCDs.

Under the agreement, Flextronics will acquire IDW in a stock-for-stock transaction with a value of about $300 million, based on an IDW share price of $6.55. This price represented a 10.1% premium above IDW’s stock price on Sept. 1, the last business day prior to the deal’s announcement. A system of collars will be used to determine the number of Flextronics shares to be exchanged.

Expected to close in Q4, the deal is subject to customary closing conditions, including IDW shareholder approval and regulatory approvals. When the transaction is completed, IDW will become a wholly owned subsidiary of Flextronics. The company expects the transaction to be neutral to diluted ESP in the first 12 months and accretive thereafter.

Following completion, Flextronics intends to combine IDW’s LCD operations with Flextronics’ Camera Module Group, TV tuner and Wifi and TFT module assembly operations to create a new business unit within Flextronics’ Component Division. This new unit will employ about 8,000 people across six factories. While Flextronics is already a top customer of IDW, Flextronics aims to move as much LCD sourcing to IDW as possible. Flextronics plans to identify and implement synergies that capitalize on the strengths of both organizations. Also, the provider intends to build upon IDW’s existing business and customer relationships.

For IDW’s fiscal year 2005, five customers, Creative Technology, Flextronics, Honeywell International, Jabil and Ecowater Systems, contributed 57.5% of IDW’s total sales revenue, according to its Form 10-K. Among customers listed in the 10-K are Kyocera and Qualcomm in cell phones; Hasbro in handheld games; Honeywell and United Technologies/Carrier in thermostats; Hypercom in point-of-sale products; Creative and SanDisk in portable media players; Abbott Labs, Omron and Philips in medical devices; Ecowater, LG Electronics and Whirlpool in white goods; and Denso, Motorola, Panasonic and Visteon in automotive products.

For the nine months ended July 31, IDW recorded revenue of $83.1 million, amounting to an increase of 29.2% from the prior-year period. IDW operates 466,000 ft2 of manufacturing facilities in China.

Meanwhile, Flextronics has completed the previously announced sale of its software development and solutions business to an affiliate of Kohlberg Kravis Roberts & Co. (April, p. 4). Flextronics has retained a 15% equity stake in the software business. The transaction values the entire business at about $900 million.

PartnerTech (Malmö, Sweden) has extended its European footprint to the UK by acquiring the Hansatech Group, an EMS provider in the UK.

Hansatech operates four plants totaling some 101,000 ft2 in three UK locations: Cambridge, King’s Lynn and Poole. With about 320 employees, the UK provider has annual sales of about GBP 20 million ($38 million). According to a statement from PartnerTech, Hansatech offers a highly developed customer base, a strong balance sheet and stable profit generation.

PartnerTech will pay an estimated sum of about GBP 5.8 million ($11 million), or GBP 4.7 million on a debt-free basis, for a 100 percent stake in Hansatech. The deal also includes an earn-out. Payment will consist of GBP 2 million in PartnerTech shares and the remainder in cash.

“The acquisition provides us with a platform in the UK and fits well into our strategy of linking proximity to our customers to production, suppliers and expertise in other parts of the world,” says PartnerTech CEO Mikael Jonson.

The UK market for non-consumer products in the area of electronics is highly fragmented, according to PartnerTech. The company reports that the Hansatech Group is among the five largest EMS companies in the UK market for non-consumer products, which is PartnerTech’s focus.

PartnerTech expects the acquisition to boost its EPS immediately, with estimated annual accretion of SEK 0.60-0.80 ($0.08-$0.11). Surplus values and goodwill are estimated at about SEK 20 million ($2.8 million).

Founded in 1972, Hansatech offers turnkey EMS to customers in sectors ranging from mobile and satellite communications, audio mixing consoles and in-car hi-fi to ion implantation, spectrophotometry and drug delivery systems. To offer volume manufacturing in Asia, Hansatech has an alliance with Integrated Microelectronics Inc., based in Laguna, Philippines. According to IMI, this alliance will continue.

Another acquisition in the UK… EMS provider AWS Electronics in Newcastle-under-Lyme, UK, has acquired Jantec Electronic Services, also a UK company. The acquisition of Jantec reinforces AWS’s position in product development at the front end and asset management or maintenance, service and repairs at the back end, said AWS. Jantec, which is based in Bedfordshire, has expertise in product design, development, prototyping, low-volume manufacture, diagnostic testing and repairs.

Under a newly signed supply agreement, Elcoteq (Espoo, Finland) will serve as manufacturer of Andrew Corporation’s high-volume filter products in Europe and North America. In addition, Elcoteq will acquire Andrew’s manufacturing unit in Arad, Romania. Andrew (Westchester, IL) anticipates purchasing about $100 million in products manufactured by Elcoteq during the first year of this multiyear agreement.

Elcoteq will pay about $20 million for the manufacturing assets in Arad, Romania, including inventory, facility leases, employment contracts, and manufacturing and testing equipment. According to Andrew, Elcoteq will retain all of the approximately 250 employees in the Arad unit. The provider will take over the unit’s 1,500-m2 leased facility immediately. Located close to the Hungarian border, the unit will continue to provide final assembly, tuning and testing services for network equipment products mainly filters.

The Romanian plant gives Elcoteq entry to a new country where it sees good opportunities for expanding its operations. Romania has been used as a low-cost European location by the likes of Celestica and Solectron.

As part of the deal, Elcoteq will also begin to manufacture Andrew’s products in St. Petersburg, Russia. In the Americas, Elcoteq will start to offer manufacturing and related services from its Juarez facility in Mexico. This business is expected to ramp up during Q4.

Andrew is ceasing filter production in Amesbury, MA, and eventually Nogales, Mexico, and is centralizing future North American filter production with Elcoteq in Juarez. Filter manufacturing at Amesbury will be transferred to Mexico and China. The company also intends to discontinue high-volume filter production at Capriate, Italy.

But Andrew will continue to operate its high-volume filter manufacturing location in Shenzhen, China. Also being retained are low-volume filter production and functions such as testing, R&D, NPI, product engineering, design, and quality control in key regions around the world. Matt Douglas, an Andrew VP in filter operations, told MMI that the company did not keep its low-cost facility in Romania largely because the facility required significant capital investment.

“Elcoteq’s expertise will help us achieve our goals of lowering costs, reducing complexity, and increasing flexibility in our filter supply chain,” states Mickey Miller, Andrew’s newly named executive VP and group president, Wireless Network Solutions.

According to Elcoteq, the agreement further strengthens its position as a strategic supplier to Andrew in Europe and the Americas. Andrew has been an Elcoteq customer since 2001.

More EMS business…Solectron (Milpitas, CA) has won a multiyear contract from Sun Microsystems for its legacy StorageTek product line. As part of the agreement, Sun will transfer to Solectron the operations at its StorageTek manufacturing facility in Puerto Rico. Sun, which acquired StorageTek last year, is a longtime customer of Solectron. The provider said the contract further deepens its relationship with Sun….Psion, a UK-listed company, and Flextronics have entered into a manufacturing agreement by which production of the main logic board for a Psion Teklogix handheld computer will move from existing suppliers to Flextronics’ facility in Nanjing, China. According to PopPhoto.com, Flextronics is the production partner for reintroduction of AgfaPhoto digital cameras, which have been licensed to a European supplier, plawa….The Globe and Mail reports that Research In Motion (Waterloo, Ontario, Canada) has contracted with Elcoteq to meet any excess demand for RIM’s new Blackberry Pearl that RIM cannot handle internally….UK design firm Plextek has won a $50-million contract for manufacturing LoJack’s vehicle recovery unit, according to Electronics-Weekly.com. Reportedly, production is being subcontracted to a Malaysia company, Clarion….CPAC Systems (Göteborg, Sweden), a system integrator for embedded control systems, has selected Enics (Baden, Switzerland) as preferred strategic supplier. In this expanded relationship, Enics will provide engineering and manufacturing services across the product lifecycle for CPAC’s growing range of products. Manufacturing services are estimated to reach 40 million euros ($51 million) over the next three to five years. Enics will also handle manufacturing of CPAC’s new product line, a telematic solution for heavy equipment.…Automated Engineering Corporation (Tampa, FL), the EMS subsidiary of US Energy Initiatives Corporation, has entered into a manufacturing agreement with EdgeAccess, a technology developer and integrator specializing in satellite communications. The contract is expected to bring in $3 million for 2007….Raytheon has selected EMS provider PRIMUS Technologies (Williamsport, PA) as a subcontractor for seven defense programs worth some $15 million. Under these contracts from Raytheon Missile Systems, PRIMUS will supply electronic assemblies for the Maverick Missile Program (over $8 million), the Joint Standoff Weapon program ($3 million), and the Excalibur guided artillery projectile ($1 million) and will support four precision guided bomb programs (over $3 million)….LaBarge (St. Louis, MO) recently announced five contract awards. The largest of these is an agreement with an existing customer, Owens-Illinois, which is expected to place orders worth about $30 million in the first year. As a result, LaBarge will expand its Owens-Illinois work, which includes control systems, automated optical inspection equipment and spare parts used in the manufacture of glass containers. LaBarge has received $8 million in contracts from Raytheon Missile Systems to provide complex cable assemblies and an integrated firing unit assembly for the Tactical Tomahawk cruise missile. Under a $5.5-million contract from Northrop Grumman, LaBarge will continue to produce an electronic chassis used in the fire control radar system of the F-16 fighter aircraft. Raytheon’s Space and Airborne Systems has awarded LaBarge a $5.5-million contract for continued production of backplane assemblies for the F-22 stealth fighter. Finally, the provider has secured an additional $1.3-million contract from Boeing to continue to supply wire harness assemblies for a US Air Force training jet….Kitron (Lysaker, Norway) has increased deliveries to Kongsberg Protech (Kongsberg, Norway), part of Kongsberg Gruppen. The additional orders, related to deliveries of Protector weapons control systems, are worth NOK 25 million ($3.8 million) for the period until March 2007. The Protector is a remotely controlled weapon station.

Alliance…Solectron and ATEK Medical Manufacturing (Grand Rapids, MI) have formed an alliance to jointly pursue outsourced medical work, reports The Grand Rapids Press. The alliance will offer capabilities in both electronics and disposable devices.

New facilities…Plexus (Neenah, WI) will purchase an additional manufacturing facility in Penang, Malaysia. The new facility, Plexus’ third plant in Malaysia, will provide 364,000 ft2 of manufacturing space and bring Plexus’ manufacturing capacity in Malaysia to about 630,000 ft2. Production at the new facility is expected to begin late in the March 2007 quarter. The company will initially spend about $13.0 million for the new facility, followed by an estimated investment of $25.0 million in fiscal 2007 (ended September 2007) for building improvement and expansion and initial equipment. Plexus says the new facility furthers its strategy to develop a center of excellence in its manufacturing and engineering services hub in Asia. The provider will also construct additional space at the new site for offices and laboratories as part of the continuing expansion of its local engineering and design capabilities.…Surface Mount Technology (Holdings) Limited, or SMT (Hong Kong), has partnered with FAW Qiming to build an automotive electronics R&D and manufacturing base at Changchun City in the Jilin Province of China. The R&D center, main offices and the manufacturing plant will be completed by the end of 2006. Production could begin in Q2 2007. SMT aims to work closely with FAW-Qiming to explore China’s booming automotive industry. FAW Qiming is a wholly owned subsidiary of FAW Group, billed as China’s oldest and largest automotive group. The new base is located within the FAW Qiming Software Park, being constructed as China’s largest automotive-related IT technology park….Minnetronix (St. Paul, MN), a provider of design and manufacturing for medical devices, has completed a 23,600-ft2 addition, which doubles the size of its facility….Scanfil (Sievi, Finland) is adding capacity at two low-cost locations in Central/Eastern Europe. The provider expects that 5,100 m2 of new space in Estonia will be in use by the end of Q3 and a 5,800-m2 expansion in Hungary will be completed by the end of the year. Also, Scanfil is planning to invest in more equipment for its Hangzhou, China, operation during the second half of 2006.

Facility closures…Suntron will close its 60,000-ft2 operation in Olathe, KS, and phase out about 190 jobs there, according to an SEC filing. This business will be moved to other Suntron sites….Next month, the contents of a 70,000-ft2 EMS facility in Caguas, Puerto Rico, will be auctioned. The facility was formerly operated by Manufacturing Technology Services….According to news reports, TT electronic manufacturing services Ltd, a UK provider, will close its Blyth, UK, facility.

Although the investigation of stock option practices at Sanmina-SCI by a special committee of its board is not yet complete, the committee has reached one conclusion (Aug., p. 7; July, p. 6; June, p. 5-6; May, p. 8). It has found that the actual date of determination for certain past stock option grants differed from the originally selected grant dates for these awards, as reported in an SEC filing.

Because the prices at the originally selected grant dates were lower than the prices on the actual dates of determination, Sanmina-SCI will incur additional charges to its stock-based compensation expense that were not included in its financial statements for fiscal years 2003, 2004 and 2005 and for the quarters ended Dec. 31, 2005 and April 1, 2006. As a result, the company will need to restate results for these periods. Such charges will have an effect on previously reported earnings and retained earnings reported on historical GAAP financial statements.

In addition, because of the investigation, Sanmina-SCI has yet to file SEC Form 10-Q for the quarter ended July 1 (fiscal Q3). Without a waiver, the trustee and certain holders of Sanmina-SCI notes totaling $1 billion in principal had the right to accelerate maturity of the notes if the company had not made that SEC filing by Sept. 14 (Aug., p. 7). The company did receive the necessary consents from note holders for a waiver until Dec. 14.

Sanmina-SCI intends to issue restatements and to file Form 10-Q for the quarter ended July 1 as soon as practicable after the investigation is completed and the company has reviewed and redone its past financial statements and finished auditing.

Jabil Circuit (St. Petersburg, FL) has delayed release of its complete financial results for the fourth fiscal quarter ended Aug. 31. But the company did report revenue of $3.0 billion for the quarter, up 45% from the year-earlier period.

Fiscal Q4 and 2006 results were originally scheduled for reporting on Sept. 26. On a conference call made that day, Timothy Main, Jabil’s president and CEO, told analysts that when a review of the company’s stock option practices is complete, the company would publish results as rapidly as it can. As previously reported, a special committee of Jabil’s board is conducting this review (June, p. 5-6). The company anticipates filing its Form 10-K by the November 14th filing deadline.

Jabil is in the process of reviewing general guidance recently issued by the SEC in connection with the numerous evaluations by public companies of their past option grants.

Main is on record as saying, “There was no backdating [of stock options].” He made that statement in May at the company’s analyst meeting (June, p. 6).

The company expects revenue for the November quarter (Q1 fiscal 2007) in the range of $3.1 to $3.3 billion. Fiscal 2007 guidance calls for revenue growth of about 20%. Revenue for fiscal 2006 increased 36% to $10.3 billion.