![]()

![]()

Jabil Circuit, which eschewed vertical integration in the past, intends to a make a deal that will give it a vertical capability for mobile phones and other consumer products. Through a tender offer, Jabil plans to acquire the outstanding shares of publicly held Taiwan Green Point Enterprises (Taichung, Taiwan), a plastics supplier with a 12% market share in handset casings. The purchase price is estimated at between $875 and $900 million.

Green Point’s sales for 2006 are projected at $517 million, representing growth of better than 40% from last year. GAAP operating margin for the plastics supplier is 11%. Key customers are presented as Motorola, Sony Ericsson, Compal, LG, Samsung, Siemens, Apple and RIM. The acquisition includes seven plants in China – three in the North, three in the East and one in the South – plus one in both Taiwan and Malaysia. Under the proposed deal, about 30,000 Green Point employees, including the current management team, will join Jabil.

Why is Jabil opting for vertical integration now in view of the company’s history as a horizontal-only supplier? According to Tim Main, Jabil’s president and CEO, electromechanical integration in the consumer and mobile products market is consistent with Jabil’s strategy to provide sector-specific supply chain solutions. “What this is really about for us is completing the supply chain solution, particularly as it relates to electromechanical parts of the product, for the consumer and mobile products segment,” Main told analysts in conference call this month.

Green Point is strong in materials science and decorative capabilities, Main reported. This know-how is important to Jabil because attractive physical packaging is an attribute of winning products in the consumer and mobile products market.

Jabil estimates that its revenue from consumer and mobile products will exceed $4 billion for fiscal 2007. The company believes that acquiring Green Point will help sustain growth of this segment and contribute to expanding market opportunity and market share in the space. In addition, Jabil said the deal will help it become self-sufficient in emerging markets such as India that lack an adequate supply base.

This vertical integration move is also in line with the offerings of two major competitors in the mobile products space, Flextronics and Foxconn International Holdings, both of whom can draw on a vertical supply chain for cell phones.

Still, for Jabil the deal is not a wholesale endorsement of vertical integration. “We really do not believe that vertical integration will necessarily be a competitive advantage in all other industry segments or in many other industry segments,” said Main. “And we’re going to retain our leveraged supply model and continue to use our supply base of strategic partners to meet our electromechanical needs.”

Green Point manufactures injection molded plastics for the communications, computer, electro-optics, consumer electronics and automotive sectors. The company’s website lists its main products as plastic parts for cell phones, land mobile products, battery chargers, back-light modules, lenses and motor vehicle structures as well as injection molds and molding machines. According to the website, Green Point utilizes over 100 injection molding machines.

“We have a high level of confidence that there are very good synergies between our customer base and Green Point’s customer base,” said Main during the conference call. “We’ll be able to bring electronic capability, global footprint and systems to their customers. And we’ll be able to bring some of this electromechanical innovation to some of our customers.”

Although Jabil describes Green Point as having scale in production of advanced plastics and metals for mobile products, Green Point does not manufacture magnesium handset casings, predicted as a high-growth area. Referring to magnesium type casings, Main said the company has “a couple of things under development that we think will be good long term.”

If the tender offer is successful, the deal is expected to close in the quarter ending May 2007. Shareholders owning about 42.7% of Green Point’s stock have pledged their shares to Jabil.

Green Point will retain its name and will operate as an independent business within Jabil.

Jabil expects that the acquisition will be neutral to fiscal 2007 earnings and accretive to fiscal 2008 earnings.

While a number of analysts viewed the deal in positive terms, Fitch Ratings placed Jabil on a negative ratings watch following the tender offer announcement. Fitch said it would resolve the ratings watch after reviewing final financing plans for the acquisition.

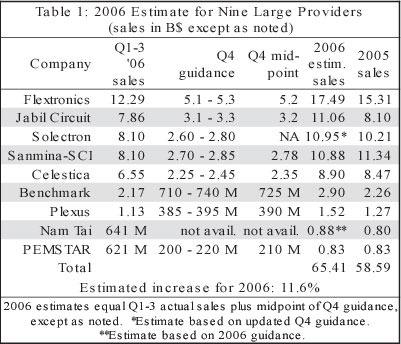

After getting off to a collectively slow start in the first half of the year, the nine largest US-traded providers will finish the year with double-digit growth overall, according to MMI’s latest estimates (Table 1). MMI projects that the nine providers will increase 2006 revenue by 11.6% in the aggregate, which is close to long-term CAGRs forecasted for the EMS industry by at least two market research firms. (Look for more on these forecasts next month.) Estimated sales for these nine providers total $65.41 billion for 2006.

A projected double-digit growth rate comes as welcome news for this EMS industry sector, which saw its collective sales slip by 1.8% in 2005 (Feb., p. 7).

For all but two providers (see Table 1 footnotes), 2006 revenue was estimated by adding the midpoint of a company’s Q4 sales guidance to its revenue for the first nine months.

Based on providers’ guidance, there will be some change to the order of these largest providers, when ranked by 2006 revenue. In MMI’s projection, Jabil Circuit leapfrogs from fifth position by 2005 sales to second by estimated 2006 sales (Table 1). This predicted feat, which is no sure thing, reflects a combination of Jabil’s high growth this year (36.5% at Q4 guidance midpoint) and a lack of such growth from the three providers that immediately preceded it in 2005. Leading Jabil by over $6 billion in estimated 2006 sales, Flextronics will easily retain its number-one rank as the largest of the US-traded EMS companies (number two overall).

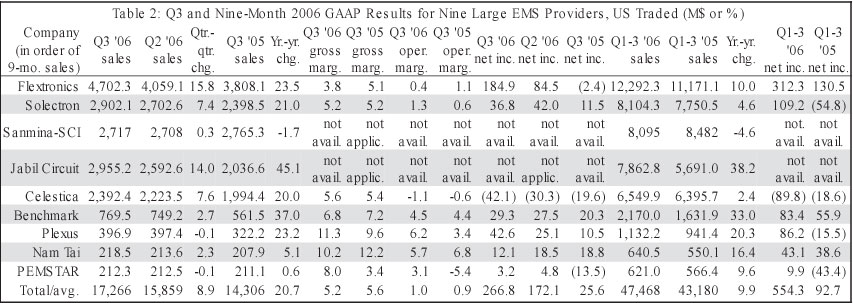

Nine-month sales for the group of nine US-traded providers amounted to $47.47 billion, up 9.9% from the year-earlier period (Table 2, p. 3). Actual growth surpassed MMI’s nine-month estimate by 80 basis points (Aug., p. 1). Still, as expected, growth rates varied widely among the group. On the high end, Jabil and Benchmark Electronics notched nine-month growth rates above 30%, while at the other end Sanmina-SCI recorded a 4.6% reduction in revenue. Five out of nine companies achieved two-digit growth rates.

The group’s overall sales growth in the third quarter was robust as sequential and year-over-year increases equaled 8.9% and 20.7% respectively. Five providers posted year-over-year growth of 20% or better (Table 2).

Two providers, Jabil and Sanmina-SCI, did not report full GAAP results for Q3 (see p. 5-6). For the remaining seven, combined gross margin (GAAP) in Q3 decreased by 40 basis points from a year earlier to 5.2%, while operating margin rose by 10 basis points to 1.0%, still far from a sparkling result.

But collectively, the seven providers did show great improvement in net income for the first nine months. Their net profits totaled $554.3 million, up from $92.7 million in the year-ago period.

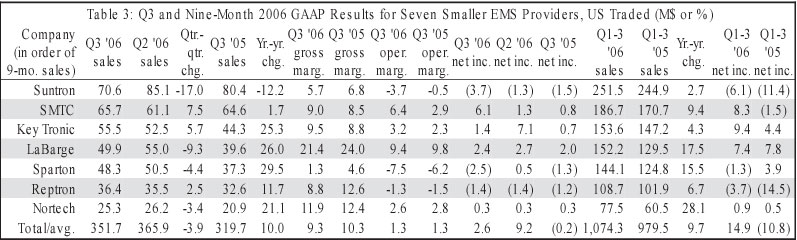

MMI also tracks seven smaller providers, whose aggregate sales growth of 9.7% for the first nine months nearly equaled that of the large-provider group. In Q3, these seven smaller providers, all US traded, combined for a 3.9% sequential drop in revenue, but produced aggregate sales growth of 10.0% year over year (Table 3). Both results fell well below comparable figures for the large-provider group in the quarter. Still, five out of seven smaller providers produced double-digit sales growth compared with the year-earlier quarter.

While overall gross margin for the smaller providers’ Q3 declined by 100 basis points from a year earlier to 9.3%, operating margin held steady at 1.3% (Table 3). Note that this operating margin was only 30 basis points above the combined margin of the seven large providers mentioned previously.

Q3 net income for the smaller providers totaled $2.6 million, down by 72% from the previous quarter. Three out of seven companies reported net losses for Q3.

Benchmark Electronics. Record revenue of $769.5 million in Q3, representing year-over-year growth of 37.1%, exceeded prior guidance of $710 to $750 million. Benchmark reported strong demand across the board during Q3. On a year-to-date basis, the provider experienced double digit year-over-year growth in each of its segments except for telecom. Customer forecasting challenges resulted in an unusually high level of finished goods on hand at the end of the quarter.

Excluding restructuring charges and stock-based compensation, operating margin came in at 4.6%, 10 basis points below the prior quarter’s margin. The company attributed the margin slippage primarily to product mix changes and associated inefficiencies.

GAAP net income for the quarter amounted to $29.3 million, a 44.5% increase over a year earlier. Non-GAAP net income was $30.0 million, or $0.46 per diluted share, which also beat guidance.

Q4 sales guidance of $710 to $740 million means that Benchmark has raised its 2006 revenue expectation, which now calls for sales of $2.87 to $2.91 billion. The midpoint of this guidance corresponds to revenue growth of 28% for the year. Excluding special items, guidance for Q4 EPS is $0.41 to $0.44, while Benchmark expects non-GAAP EPS of $1.70 to $1.73 for 2006. Among the factors baked into Q4 guidance is the phase-out of an Agilent program.

Benchmark’s top two customers accounted for 49% of its Q3 revenue, with the largest customer, Sun, representing 39% of sales. Sales to these customers increased 65% year over year. The company anticipates that sales to Sun will decline in both dollars and as a percentage of sales.

As reported earlier, Benchmark has signed a definitive agreement to acquire Pemstar (Oct., p. 6-7).

Celestica. Q3 revenue of $2.39 billion came in above the high end of guidance, which was $2.35 billion. Revenue growth was 7.6% sequentially and 20.0% year over year, fueled largely by the growth in Celestica’s consumer, automotive and medical segment, which was up 36% from Q2 2006. Business other than comm and IT rose to 30% of Q3 sales versus 27% in the prior quarter and 24% a year earlier. Operating margin (non-GAAP) grew sequentially by 50 basis points to 2.7%.

The company’s Q3 GAAP loss of $42.1 million included restructuring charges of $82.4 million. Adjusted net earnings amounted to $40.5 million, or $0.18 per share, versus $27.1 million, or $0.12 per share, for the year-earlier quarter.

As Celestica has discussed in its Q1 and Q2 conference calls, the company has been working on operational issues in Mexico and Europe. Profitability improvements in both Mexico and Europe have progressed slower than anticipated. The provider continues to experience efficiency shortfalls in Mexico caused by the growth and complexity introduced there. The Mexico operation is still incurring losses of about $7 million. Q3 losses in Europe remained flat in Q3 at roughly $6 million. Lower demand in Europe offset expected improvements from restructuring in the region during the quarter. The company said restructuring should help raise European profitability in Q4, and Celestica’s efforts over the next several quarters are focused on bringing more growth to this region.

Asian operations continued to perform well with operating margins of 4.8%. Margins in the Americas increased 40 basis points to 1% of sales, but the company was disappointed with this result because of a $6-million inventory charge and the slower than expect progress in Mexico.

Q4 sales guidance of $2.25 to $2.45 billion reflects a seasonal decline in Celestica’s consumer business from the prior quarter partially offset by growth in traditional markets.

Elcoteq. Third-quarter revenue of 1.17 billion euros ($1.54 billion at current rates) increased 13.5 % sequentially, but declined 2.1% year over year. Underlying the lack of growth were weaker than forecasted volumes especially for terminal products in Europe. Operating income for the quarter amounted to 16.6 million euros, or 1.4% of sales, down from 25.6 million euros, or 2.1 % of sales in the year-earlier period. EPS came in at 0.19 euro, compared with the year-earlier result of 0.44 euro.

The company attributed weaker than expected profitability to unsatisfactory performance in the Americas and low production volumes in Europe. Despite growing revenue by 8.2% year over year, Americas operations showed sequentially weaker performance due to some ramp-up challenges, inventory problems associated with projects either completed or close to completion, and redundancy costs. One-time costs in the Americas burdened Q3 results by around 3 million euros.

Ericsson and Nokia accounts together contributed 63% of Q3 sales, versus 73% in same period a year ago. These figures do not include business with Sony Ericsson. Sales from customers outside the Ericsson and Nokia groups increased by more than 30% both sequentially and year over year.

Terminal Products (mobile phones) activity represented 83% of Q3 revenue, while the Communications Network Equipment business accounted for the remaining 17%.

Elcoteq continues to derive a majority of its sales from Europe, which supplied 57% of Q3 revenue. That percentage was unchanged from a year earlier. Asia-Pacific and the Americas represented 26% and 17% of Q3 sales respectively. Sales from all three geographical areas rose by double digits compared with Q2 2006. Sequential increases ranged from approximately 10% for Europe to about 29% for the Americas.

The company reaffirmed its September forecast, which projected that Q4 sales and operating income would be at the third quarter’s level.

Flextronics. Sales in the September quarter (Flextronics’ fiscal Q2) totaled a record high of $4.70 billion, up 23.5% year over year. The provider also earned record net income (GAAP) of $184.9 million in the September quarter, compared with a net loss of $2.4 million in the year-earlier period. Included in net income for the September quarter was an after-tax gain of about $171 million from the sale of Flextronics’ software development and solutions business, which brought over $600 in cash (subject to post-closing adjustments) plus a $250-million note. Non-GAAP net income increased 15.2% year over year to $116.7 million, or $0.20 per diluted share.

September-quarter sales went up 15.8% from the prior quarter, and all of Flextronics’ segments except computing showed sequential increases. Leading in quarter-to-quarter growth were consumer digital and mobile with 21% and 33% increases respectively. When combined, these two segments accounted for $560 million in additional sales over the June quarter. Compare that to company’s overall sequential increase of $643 million.

Operating margin (non-GAAP) for the September quarter came in at 3.1%, which represented an improvement of 10 basis points over the core EMS margin in the year-ago quarter.

ROIC amounted to 11.0%, up from 9.5% a year earlier.

Cash flow from operations in the September quarter was $49 million, despite an inventory increase of $371 million. This increase was primarily related to anticipated revenue growth in the December quarter. Flextronics also pointed out that its Nortel transaction was expected to increase inventory. In an October conference call, Flextronics said it has about $800 million worth of Nortel inventory. The provider plans to reduce inventory for all customers by $300 to $400 million over the next three quarters.

For its ODM business in mobile phones, Flextronics expects to produce 15 to 17 million phones – with 17 million described as a “best guess” – in the current fiscal 2007 and probably about 30 million units in fiscal 2008. The company considers break-even at 13 to 14 million phones.

Flextronics confirmed prior fiscal 2007 guidance, which called for revenue from continuing operations to grow in the range of 25% to about $19 billion and non-GAAP EPS to grow in the range of 15% to about $0.80 (July, p. 6). For the December quarter, the company expects sales from continuing operations to increase by 25 to 30% year over year to a range of $5.1 to $5.3 billion; it projects non-GAAP EPS to grow 10 to 15% year over year to a range of $0.22 to $0.23.

Hon Hai Precision Industry (also known by its trade name Foxconn). The world’s largest EMS company reported non-consolidated results for the first nine months. That means these results did not include revenue from such subsidiaries as Foxconn International Holdings, Hon Hai’s handset unit, in which Hon Hai holds a majority interest. As is typical of a publicly held company in Taiwan, Hon Hai only reports consolidated results, which incorporate revenue from all subsidiaries, twice a year – for the first half and the full year.

For the first nine months of 2006, non-consolidated sales were up 34.0% year over year to NT$589.76 billion ($18.16 billion at today’s rates), while operating income rose 42.4% to NT$19.60 billion. Operating margin for the nine-month period improved by 20 basis points from the year-ago period to 3.32%. Gross margin for the first nine months, however, slid by 26 basis points to 5.51%.

While these results do not reflect revenue from certain subsidiaries, they do include earnings from ownership in subsidiaries and affiliates. Hon Hai recorded nine-month revenue of NT$27.01 billion from equity method investments; this investment income represented 58.6% of profit before taxes, which totaled NT$46.10 billion. Net income (after taxes) for the period amounted to NT$37.82 billion, up 38.3% from a year earlier.

Jabil Circuit. The company has yet to issue its full financial results for the quarter and fiscal year ended August 31, pending completion of Jabil’s review of its stock option practices (Sept., p. 8). As a result of this review, the company concluded this month that it will need to restate financial results for fiscal 2005 and possibly other periods. Jabil missed the Nov. 14 deadline for filing its SEC Form 10-K and has filed for a 15-day extension.

In that filing for an extension, the provider stated that its fiscal 2006 results will contain significant changes from fiscal 2005 results. Jabil attributes these changes primarily to its evaluation of stock option practices, the restructuring plan initiated in the August quarter, and certain other changes from its business operations, including an increased level of sales.

If Jabil does not deliver its 10-K to its credit facility lenders within 15 days of the extended deadline, it would violate a credit facility covenant and have 60 days to cure the breach.

Still, Jabil did report sales for the August quarter and its fiscal 2006 (Sept., p. 8). Revenue for the quarter rose 45% year over year. Nokia and Philips represented 20% and 12% of fiscal 2006 revenue respectively.

Jabil expects sales for the November quarter to be up 5% to 12% sequentially.

Nam Tai Electronics. Q3 sales of $218.5 million, which equated to a 5.1% increase year over year, were in line with the company’s revised guidance. On Sept. 1, Nam Tai lowered sales and earnings guidance for the quarter in view of lower than expected sales and a change in product mix along with lower margins.

Although non-GAAP operating income per share and non-GAAP EPS exceeded revised expectations due to implementation of cost controls, the company was disappointed by overall Q3 results compared with Q3 2005 performance and its original guidance. Non-GAAP EPS for the third quarter stood at $0.28, down 20% from Q3 2005 while at the low end of its original EPS guidance.

Despite a challenging business environment, the company improved gross margin to 10.2% in Q3 from 9.7% in the prior quarter. Nam Tai also pointed to its success in controlling SGA and R&D expenses, which decreased to 4.5% from the year-earlier quarter’s 5.4%, which included $960,000 in severance expenses, or 0.5% of sales.

The provider confirmed its revised outlook, which calls for sales growth of about 10% for 2006, followed by growth of about 12% in 2007 and 2008 respectively. In September, Nam Tai lowered its sales growth targets from 25% for each of the three years. The company will no longer provide quarterly sales and EPS guidance.

Within China, Nam Tai expects that in the summer of 2007 it will start construction for a new factory in Shenzhen and facilities in Wuxi, Jiangsu Province.

Plexus. The provider reported record net income of $42.6 million for the September quarter (Plexus’ fiscal Q4), which included a $17.7 million positive adjustment regarding deferred tax assets. Non-GAAP net income was $25.5 million, or $0.54 per diluted share, which surpassed the guidance midpoint by $0.06. September quarter sales increased 23.2% year on year to $396.9 million, but were essentially flat quarter over quarter. Operating margin expanded by 20 basis points from the previous quarter to 6.2%.

Revenues in the company’s defense, security and aerospace sector contracted sharply in the quarter, reflecting completion of first production orders from a significant defense customer. Plexus expects revenues in the sector to shrink further in the December quarter as volumes from this major military program decline to minimal manufacturing levels. Volumes depend on “extremely lumpy purchase orders” from the US military, said Plexus. The company forecasted that production for additional orders would begin in the March 2007 quarter.

Juniper Networks represented 17% of September quarter sales, while multiple divisions of General Electric together accounted for 12%. During the quarter, the company won 11 significant new manufacturing programs, worth about $112 million in additional revenue on an annualized basis. Plexus also landed about $10 million in new product development business.

Plexus expects December quarter sales in the range of $385 to $395 million, slightly below September’s level. Virtually no revenue will come from the aforementioned military program in the December quarter. This lack of military revenue will temporarily stall overall growth in the quarter and lower margins. December quarter earnings will also be affected by other factors including a change in the effective tax rate. Plexus projected EPS (before any restructuring costs) for the quarter in the range of $0.31 to $0.35. The company is targeting revenue growth of 15% to 18% in fiscal 2007, with strong revenue growth expected in the June and September quarters.

Sanmina-SCI. As a result of Sanmina-SCI’s investigation of its stock option practices, the company will need to record additional stock-based compensation expenses, which will require restatement of financial results. (Sept., p. 7-8). As of this writing, the company’s GAAP results for the July 1 and Sept. 30 quarters (fiscal Q3 and Q4) were still unavailable. However, Sanmina-SCI did release non-GAAP guidance for the two quarters.

The company reported sales of $2.72 billion for the September quarter, basically flat compared with sales of $2.71 billion in the prior quarter and down 1.7% from the year-earlier quarter. Gross margin (non-GAAP) expected for the September quarter declined to about 4.8% from 6.1% expected in the previous quarter, while operating margin decreased to about 1.2% from 2.6% expected in the prior period. For the September quarter, Sanmina-SCI estimated non-GAAP EPS in the range of one cent negative to one cent positive.

Gross margin guidance for the September quarter was below expectations, partly as a result of the company’s decision to exit certain ODM product lines. The company will realign its ODM business to focus on joint development manufacturing services, which reduce the company’s risk because revenue is guaranteed. This decision resulted in charges of about $15 million, primarily associated with obsolete inventory. Two other factors contributed: an underperforming PC fabrication business and charges associated with warranty claims and doubtful collection of receivables. These items reduced gross profit by about $32 million in the quarter.

Fiscal year 2006 sales amounted to $10.96 billion, down 6.6%. The company attributed most of this decline to its personal and business computing segment, whose revenue went down 21% to about $3.2 billion in fiscal 2006 revenue.

Sanmina-SCI also announced that it would separate its personal and business computing unit from its core EMS business. The company said that creating a stand-alone personal and business computing unit would help the company to pursue strategic alliances for component vertical integration, product design and growth. This arrangement will also allow the company to consider potential opportunities to maximize the value of the unit. All options are open, and that includes bringing in a financial partner, said Sanmina-SCI’s CEO during a conference call this month. He pointed out that the margins and growth of the unit are not acceptable.

Separating the personal and business computing unit, realigning the ODM business, and potentially consolidating operations in higher-cost geographies will result in charges of $125 million to $150 million during fiscal 2007.

For the December quarter, Sanmina-SCI expects revenue of $2.70 billion to $2.85 billion and non-GAAP EPS of between $0.06 and $0.08.

Solectron. Sales for the August quarter (Q4 fiscal 2006) totaled $2.90 billion, up 7.4% over the prior quarter and 21.0% from the year-earlier period. Non-GAAP operating margin improved sequentially by 40 basis points to 1.8%. Non-GAAP profit after tax amounted to $54.8 million, or $0.06 per share, which was at the top end of the guidance range for the quarter. Compare this result with non-GAAP profit of $38.9 million in the previous quarter and $41.4 million in the year-earlier period. For the August quarter, GAAP profit after tax from continuing operations was $38.8 million versus $42.4 million in the previous quarter and $11.8 million a year earlier.

Revenue from the networking market increased 27% sequentially in the August quarter. This growth came predominantly from Cisco Systems, which accounted for $588 million in revenue, or 20% of total sales in the quarter. Cisco business grew by $149 million from the previous quarter.

Solectron posted high year-over-year growth in two non-traditional markets. In the August quarter, its sales to the industrial segment grew by 56% from the year-earlier quarter, while its consumer business climbed 40%.

Sales in fiscal 2006 totaled $10.56 billion, a slight increase of 1.1% over the previous fiscal year, but second-half revenue grew by $610 million year over year.

Cisco is shifting to a lean manufacturing model, which involves Solectron and its other EMS providers (April, p. 1-2). Solectron’s implementation of a lean supply chain for Cisco was expected in the November quarter and would have cost Solectron up to $150 million in November quarter sales. But the supply chain program has been delayed, with implementation planned for subsequent quarters of fiscal 2007. As a result, Solectron expects to meet or exceed its November quarter sales guidance of $2.6 billion to $2.8 billion. The company is maintaining its non-GAAP EPS guidance at 4 cents to 6 cents.

Solectron also announced a new restructuring plan, reported here last month (Oct., p. 7).

Venture. Q3 revenue of S$799.2 million ($517.5 million at current rates) was down 2.6% year over year, but up 6.5% quarter to quarter. Profit attributable to shareholders came to S$59.0 million, an increase of 14.4% from a year earlier and 12.2% from the prior quarter. Excluding foreign exchange adjustment, EBITDA in Q3 rose by 11.9% year over year. Net profit margin has improved for three straight quarters, reaching 7.4% in Q3.

The provider reported quarter-on-quarter improvement across all segments. Year to date, the test and measurement/others segment grew 33%, reflecting higher business volume in test and measurement equipment, power rectifier/systems, medical products and laser systems. Similarly, Venture’s printing and imaging business expanded by 26% as activities involving new platforms increased. Yet nine-month sales from the computer peripherals and data storage segment declined by 26%, and networking and communication business fell 29%. Both of these declines resulted from Venture’s continued efforts to replace high-volume products with high-mix business.

For Q4, the company sees good prospects in its test and measurement/others segment, with medical business looking promising. The Q4 outlook for Venture’s printing and imaging business is stable, while the company anticipates short-term softness in its networking and communication and storage businesses, which are expected to improve in 2007.

Stephen Delaney has resigned his position as CEO of Celestica (Toronto, Canada) to pursue other business interests, according to a statement from the company. Craig Muhlhauser, previously Celestica’s president, succeeds Delaney as president and CEO, effective immediately.

Before joining the company in May 2005, Muhlhauser was president and CEO of Exide Technologies, a battery producer. Prior to that, he was a VP at Ford and president of Visteon Automotive Systems. It is perhaps ironic that Muhlhauser and Delaney worked together at Ford.

Delaney’s tenure as CEO lasted less than three years. The announcement was unexpected.

TT electronics (Weybridge, Surrey, UK), whose businesses include sensors, components and EMS, has acquired Apsco, an EMS provider whose facility is located in Perry, OH. This acquisition gives TT electronics an EMS presence in the US to complement the group’s existing EMS facilities in China, the UK and Malaysia.

The purchase price is £14.9 million ($29.1 million) in cash for gross assets of £13.5 million ($26.4 million) as of Dec. 31, 2005. Net asset value then was £9.6 million ($18.7 million). For 2005, Apsco reported pre-tax profits of £1.9 million ($3.7 million) on sales of £28.5 million ($55.6 million). The transaction also includes a maximum earnout of £1.0 million ($2.0 million).

With 350 employees, Apsco has well established positions in the office machine, industrial, medical, defense and communication markets.

As one of the deal’s synergies, TT electronics’ EMS operation in China will gain access to previously untapped US customers.

Deals done…Flextronics (Singapore) has acquired Ceres Integrated Technologies (San Jose, CA), about a $60-million-a-year machining company mostly focused in semiconductor equipment. This acquisition adds machining to Flextronics’ vertical offerings….Earlier this year, Solectron (Milpitas, CA) quietly bought ConFocus (Norcross, GA), which has developed software for cable, satellite and IP set-top boxes.…Venture (Singapore) expects to obtain all the shares of ODM GES International (Singapore) by Nov. 29. The acquisition was reported previously (July, p. 5).

New business…Flextronics has a new EMS relationship with Cisco Systems, which has awarded Flextronics an unspecified number of new products. Also, the provider has begun producing semiconductor test units in Asia for Agilent spinoff Verigy. Flextronics believes that this is the most complex product built today in Asia, either by EMS providers or ODMs. …Sanmina-SCI (San Jose, CA) has won business from Allied Telesis, a provider of secure Ethernet/IP access solutions. Also, Sanmina-SCI will serve as lead contractor for a portable radiation detector project awarded by the US Department of Homeland Security. In yet another new program, Sarantel (Wellingborough, UK), a maker of filtering antennas for wireless devices, has signed an MOU whereby Sanmina-SCI will provide Sarantel with procurement, manufacturing and logistics services from its Singapore facility….Novint Technologies (Albuquerque, NM) has selected VTech’s Contract Manufacturing Services business to manufacture a new game controller enabling 3D touch.

New facilities…Last month, Flextronics opened the first building in its planned 8-million-ft2 industrial park in Chennai, India. The 250,000-ft2 building is sold out, reported CEO Mike McNamara during Flextronics’ analyst meeting in October. The company has already booked enclosures, cell phones and set-top boxes for India manufacturing. A second 250,000-ft2 building for plastics, metalwork and assembly is due to open in December. Flextronics also launched last month 400,000 ft2 in Ciudad Juarez, Mexico, the first phase of a projected 1.9-million-ft2 facility there. The Juarez operation will offer BTO/CTO and other services. McNamara said this building is also sold out. In Ukraine, Flextronics is opening 200,000 ft2 this quarter. …Zhengjiang Pound Precision Electronics Manufacturing, a new EMS company, is establishing in Jurong, China, a 17,000-m2 plant that will start out with 430 people….Fawn Electronics has announced plans for a new 47,000-ft2 facility in the Nashville Business Center in Nash County, NC. Fawn’s original EMS plant in Elm City, NC, was destroyed in a fire in December 2005 (Jan., p. 8). The operation was relocated to a temporary facility in Wilson, NC, and has since resumed full production.

Collaboration...Under a collaboration agreement, HP’s image processing technology will correct and enhance digital images in Flextronics-designed and -manufactured camera modules....Celestica and India’s HCL Technologies, a global IT services company, have agreed to form a joint venture to provide complete concept-to-manufacturing solutions.