Based on an historical analysis of Surface Mount Technology (SMT) market data, New Venture Research (NVR) recently found that the worldwide installed base of SMT lines approximates 70,176 in 2019, probably increasing to 73,231 in 2020, despite the Corona crisis. Together, these SMT lines annually process up to 8 trillion active and passive components that populate some 33 billion printed circuit boards, which form the heart of our Smart Phones, Notebooks, FTVs and future IoT applications.

Based on an historical analysis of Surface Mount Technology (SMT) market data, New Venture Research (NVR) recently found that the worldwide installed base of SMT lines approximates 70,176 in 2019, probably increasing to 73,231 in 2020, despite the Corona crisis. Together, these SMT lines annually process up to 8 trillion active and passive components that populate some 33 billion printed circuit boards, which form the heart of our Smart Phones, Notebooks, FTVs and future IoT applications.

Roughly 70% of the installed SMT capacity represent High-End assembly lines, composed of increasingly integrated, modular Chip Shooting and Multifunction Placement platforms which are capable of mixed IC / PCB assemblies. The remaining 30% are Low-End assembly lines typically composed of lower performance machines. Capex requirements per SMT line vary widely, but, on average, range from US$ 1.2 million on the low end to US$ 2.8 million on the high end.

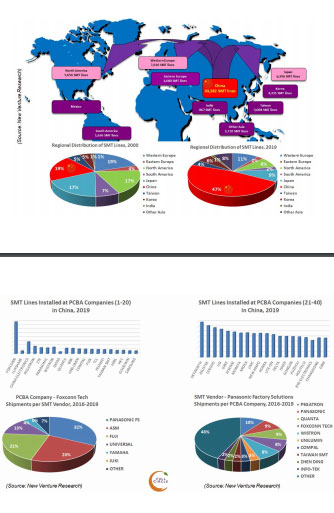

Worldwide SMT capacity has grown at a cumulative aggregate rate of 6% during the past five years, with China capturing more than 50%, in real terms. Taking into account a normal replacement cycle and initial purchases of new SMT lines, China now accounts for 47% of all installed SMT lines, up from 19% in the year 2000, thus dwarfing the former manufacturing centers of America, Europe and Japan.

While this should no longer surprise anyone active in the electronics manufacturing sector, to date, even industry experts continue to wonder who provides this capacity, and, more importantly, who absorbs it to manufacture the advanced products demanded by an increasingly global market. The industry structure in China remains far from transparent, with a complex mix of parent companies and subsidiaries, whose names still sound exotic and often go unnoticed, with significant opportunity costs in terms of business development.

For this reason, NVR developed a unique database, dedicated to China, that relates almost 1,000 parent companies and 1,800 subsidiaries, many of which designated High Tech Enterprises, operating in various Free Trade Zones and Tech Parks. During the period 2016-2019, these OEMs, ODMs, EMS providers, PCB manufacturers, Component suppliers and Semiconductor assembly companies imported almost 60% of China’s automatic placement machines from 40 SMT (mounting) and FCB (bonding) equipment vendors.

Using an exclusive set of customs data, we tracked and traced each shipment of new versus used SMT mounters and FlipChip bonders, including their invoice value, relating vendor to buyer. We, then, identified parent companies and subsidiaries, PCB assembly sites, and the number of SMT lines installed in each city and province. We double-checked the outcome against several hundreds of highly detailed factory audits to ensure an overall accuracy ratio of at least 80%.

The final result is a very comprehensive database that comes full circle (360°) in providing a perfect (100%) market view, which permits both general overviews and detailed drill down analyses around multiple pivot points: equipment provider, product model, product category, product configuration, mounter units, unit price, customer destination, company type (state-owned, collective, private, foreign, JV), number of SMT lines, number of employees and even contact details.

This database is an excellent tool for corporate executives and business development staff employed by a wide variety of electronics manufacturing companies interested in SMT capacity development in China, from a competitive point of view. It enables them to drill down and rank hundreds of competitors, big and small, qualifying their SMT capacity and factory expansion plans.

Conversely, the database is highly instrumental to SMT and FCB equipment vendors interested in boosting marketing and sales to electronics manufacturers in China, that is, from a business development point of view. It enables them to drill down hundreds of OEMs, ODMs, EMS providers and other potential customers, assess their SMT capacity, future demand, as well as share of wallet held by existing competitors.

To learn more about this information offering, including pricing, please feel free to contact:

Frank Klomp, NVR, The Netherlands

Tel. +31 6 4100 9362

Randall Sherman, NVR, United States

rsherman@newventureresearch.com

Tel. +1 530-265-2004

Leave A Comment

You must be logged in to post a comment.